|

시장보고서

상품코드

2063253

지하 가스 저장 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Underground Gas Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

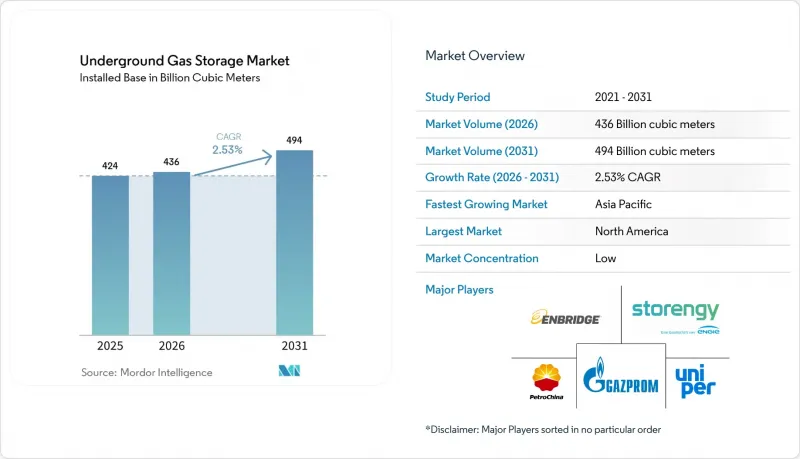

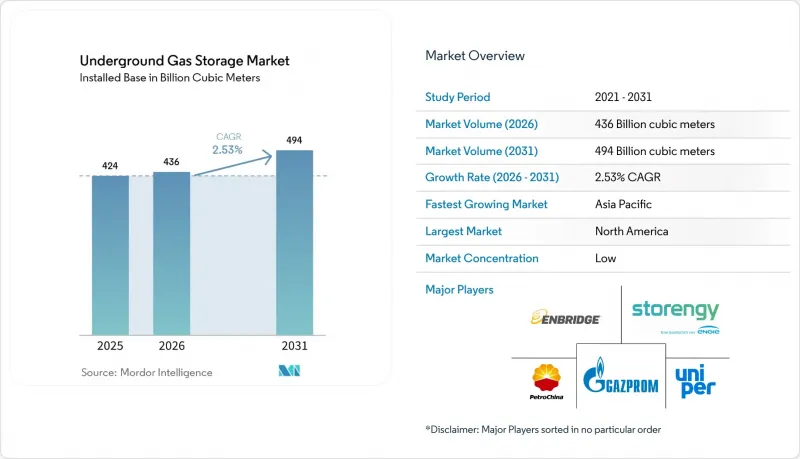

Mordor Intelligence에 의하면, 지하 가스 저장 시장 규모(설치용량 기반)는 2025년 4,240억 입방미터로 평가되었고, 2026년 4,360억 입방미터로 추정되고, 2031년까지 4,940억 입방미터로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 2.53%를 나타낼 것으로 예측됩니다.

본 보고서는 유형별(고갈된 저류층, 소금동굴 등), 저장 용량 등급별(10억 입방피트 미만, 10억-50억 입방피트, 기타), 용도별(계절적, 전략적, 기타), 최종 사용자별(유틸리티, 산업용, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 부피(bcm) 단위로 제시되어 있습니다.

세계의 지하 가스 저장 시장 동향 및 인사이트

계절별 및 전략적 용도의 가스 수요

계절적인 난방 수요와 법적 구속력이 있는 저장 의무가 가동률을 뒷받침하고 있습니다. 독일은 2024년 겨울을 대비해 78 TWh의 비축을 의무화한 반면, 유럽연합(EU)은 매년 11월 90%의 충전률을 의무화하는 규정을 마련하여, 이에 따라 유틸리티 사업자들은 더 많은 가동 가스와 주입 능력을 확보해야 하는 상황에 놓여 있습니다. 인도는 2025년도 예산에서 고갈된 가스전에 3-4bcm을 추가로 확보하는 2단계 전략적 가스 비축 사업에 7억 달러를 편성하여, LNG 수입 의존도를 낮췄습니다. 중국석유(페트로차이나)는 55억 9,000만 달러에 기존 생산 유전을 임베디드하고 60억 입방미터의 가동 용량을 추가함으로써 북부 각 성의 계절적 수요 변동을 안정화시켰습니다. 이러한 정책 주도형 확장은 구조적인 이용률의 하한선을 형성하여 사업자를 현물 가격의 급변동으로부터 보호하고, 장기적인 투자를 뒷받침하고 있습니다.

가스 화력 발전의 확대 및 피크 절감 수요

석탄에서 가스로의 연료 전환과 재생에너지의 간헐성으로 인해, 단주기 저장 시설의 가치가 높아지고 있습니다. NERC의 보고서에 따르면, 하루 70억 입방피트(Bcf) 이상 공급 능력을 확보하면 북미의 전력 회사들은 터빈의 과도한 가동을 피하면서도 일일 수요 변동에 대응할 수 있다고 합니다. 염동 저장 시설은 1시간 단위의 주기적 수요를 충족시킵니다. 온타리오주의 엔브리지(Enbridge)가 운영하는 던 허브(Dawn Hub)는 석탄 화력 발전소 폐쇄에 따라, 해당 주의 송전망에 하루 1.5 Bcf 공급 능력을 추가하기 위해 4억 달러를 투자하고 있습니다. 인도는 2030년까지 가스 화력 발전 용량을 3배로 확대할 계획이며, 몬순으로 인한 수요 감소를 상쇄하기 위해 구자라트주와 라자스탄주에서 대수층 및 고갈된 유전 개발 프로젝트가 필요합니다.

막대한 자본 비용에 더해, 버퍼 가스 비용 부담

CEDIGAZ는 2035년까지의 누적 투자 수요를 1,000억-1,700억 유로로 추산하고 있으며, 고갈된 저장층의 전환에는 1MWh당 190유로, 신규 동굴 프로젝트에는 1MWh당 235유로의 비용이 소요됩니다. 대수층 프로젝트에서는 용량의 45-80%가 베이스 가스로 고정됩니다. 2025년 현물 가격이 1MMBtu당 3달러 수준일 경우, 10Bcf 규모의 사이트에서는 1,500만-2,400만 달러가 고정 비용으로 발생하여 수익을 창출하지 못하게 됩니다. 인도 정부는 전략적 프로그램에 최대 20억 달러를 예산으로 편성했으나, 재정적 압박으로 인해 일정이 지연될 가능성이 있음을 시사하고 있습니다.

부문별 분석

2025년에는 고갈된 저류층이 용량의 78.5%를 차지했으나, 이는 20-40%라는 양호한 완충 가스 비율을 반영한 것입니다. 한편, 염동굴은 1시간 단위의 주기적 운영과 수소 저장 기능이 가능하기 때문에 연평균 성장률(CAGR) 9.1%의 성장 궤도에 올라 있습니다. 염동굴 저장 시설의 지하 가스 저장 시장 규모는 대수층보다 더 빠르게 확대될 것으로 예측됩니다. 이는 염동굴이 하루 10억 입방피트(Bcf) 이상 공급 능력을 갖추고 있어, 재생에너지 비중이 높은 전력망의 균형 조절에 있어 필수적인 특성 때문인 것입니다.

자본 효율성 측면에서는 계절적 요인을 고려할 때 고갈된 유전이 여전히 유리하지만, 수소 관련 규제 지원에 힘입어 염층 저장 시설의 매력이 높아지고 있습니다. 독일 연방경제기후행동부(BMWK)는 2045년까지 250곳의 저장층이 수소 저장 시설로 전환되어 76-80 TWh의 수소 저장 용량이 확보될 것으로 전망하고 있습니다. 센트리카(Sentrica)는 2050년까지 540억 입방피트(Bcf) 규모의 러프(Rough) 저장층을 수소 활용에 대비해 20억 파운드를 투자하겠다고 밝혔으며, 이는 탈탄소화가 진행되는 가운데 기존 기업들이 지하 가스 저장 시장 점유율을 지키기 위해 자산 재편을 추진하고 있음을 보여줍니다.

2025년에는 20Bcf를 초과하는 유전이 설비 용량의 54%를 차지했으며, 라프(Rough)나 골든 트라이앵글(Golden Triangle)과 같은 메가 저류층이 주도했습니다. 이는 규모의 경제와 간소화된 인수 계약을 제공합니다. 그럼에도 불구하고, 중견 기업들이 산업 집적지 인근의 유휴 광구를 인수함에 따라, 5-20 Bcf 규모의 시설은 연평균 6.8%의 성장률을 보일 것으로 전망됩니다. 윌리엄스 컴퍼니가 루이지애나주와 미시시피주에서 115 Bcf 규모의 시설을 19억 5,000만 달러에 인수한 사례는 이러한 규모 확대 전략을 여실히 보여주고 있습니다.

규제가 통합을 촉진하고 있습니다. EPA의 메탄 규제는 일일 처리량이 50 MMcf를 초과하는 경우에 적용되며, 소규모 시설에서는 감당하기 어려운 규정 준수 비용이 발생합니다. 그 결과, 투자자들은 수익원이 다양하고 단위 비용이 낮은 대규모 자산에 관심을 기울이며, 지하 가스 저장 시장의 상위 용량층으로의 이동을 가속화하고 있습니다.

지역별 분석

2025년, 북미는 지하 가스 저장 시장 점유율의 37.9%를 차지했으며, 이는 총 4.8조 입방피트(Tcf)의 가동 용량을 갖춘 400개 이상의 시설에 의해 뒷받침되고 있습니다. 미국에서는 EPA의 2024년 메탄 규제를 준수하기 위한 개조 공사를 통해 검증된 최대 용량이 700억 입방피트(Bcf) 증가했습니다. 한편, 캐나다의 던 허브 확장 계획에서는 하루 15억 입방피트(Bcf)의 신규 공급 능력 확보를 목표로 하고 있습니다. 식스 스트리트(Six Street)와 칼리체(Kaliche)와 같은 사모펀드 기업들은 인플레이션에 대비한 안정적인 현금 흐름을 확보하기 위해 센트럴 밸리 스토리지(Central Valley Storage)와 골든 트라이앵글 스토리지(Golden Triangle Storage)를 인수했습니다.

에너지 안보의 필요성이 유럽의 설비 확충을 주도하고 있습니다. 독일은 '재충전 명령'에 따라 2024년 말까지 78TWh를 저장할 예정이며, 연방 경제·기후부(BMWK)는 2030년까지 2-7TWh의 수소 저장을 예상하고 있습니다. 영국은 라프 저장 시설을 재개하고 수소 전환에 20억 파운드를 배정했습니다. 한편, 덴마크의 릴 트루프 동굴 저장 시설은 2030년까지 네덜란드까지 이어지는 550km 길이의 파이프라인에 연결될 예정입니다. 러시아는 여전히 상당한 규모를 유지하고 있지만, 제재로 인해 수출이 동쪽으로 이동하고 있어 상황은 불투명합니다.

아시아태평양은 2031년까지 연평균 11.5%의 성장률을 기록하며 가장 빠르게 성장할 것으로 예상되는 지하 가스 저장 시장입니다. 중국은 60억 입방미터의 용량을 증설하고, 59억 달러를 투자해 109.7억 입방미터의 유효 가스량을 확보함으로써 세계 6위로 올라섰습니다. 인도의 2단계 계획에 따르면, 2030년까지 30억-40억 입방미터 규모의 자금이 투입될 예정이며, 일본의 오사카가스는 지하 저장 시설에 연결되는 내진 설계 파이프라인에 4억 6,900만 달러를 투자하고 있습니다. 한국의 여수 및 울산 LNG 터미널은 지질학적 제약 없이 피크 시간대 공급 능력을 강화하고 있는 반면, 아세안(ASEAN) 국가들은 신축 가스 화력 발전 설비를 지원하기 위한 시범 사업을 검토하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the underground gas storage market size in terms of installed base is projected to expand from 424 billion cubic meters in 2025 and 436 billion cubic meters in 2026 to 494 billion cubic meters by 2031, registering a CAGR of 2.53% between 2026 and 2031.

This report is Segmented by Type (Depleted Reservoirs, Salt Caverns, and More), Storage-Capacity Class (Below 1 Bcf, 1-5 Bcf, and More), Application (Seasonal, Strategic, and More), End-User (Utilities, Industrial, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (bcm).

Global Underground Gas Storage Market Trends and Insights

Demand for Seasonal & Strategic Working Gas

Seasonal heating cycles and binding storage mandates underpin utilization levels. Germany required 78 TWh of reserves for winter 2024, while the European Union set a 90% fill rule each November, pushing utilities to secure more working gas and injection capacity. India earmarked USD 700 million in its 2025 budget for Phase II strategic gas reserves that will add 3-4 bcm in depleted wells, trimming LNG-import exposure. PetroChina added 6 bcm of working capacity by purchasing former production fields for USD 5.59 billion, stabilizing seasonal swings in northern provinces. Such policy-led expansions create a structural utilization floor, shielding operators from spot-price shocks and supporting long-cycle investment.

Growing Gas-Fired Power Generation & Peak-Shaving Demand

Coal-to-gas switching and renewable intermittency boost the premium on rapid-cycle storage. NERC reports that deliverability above 70 Bcf per day lets North American utilities meet intra-day ramps without over-scheduling turbines . Salt caverns satisfy hourly cycling; Enbridge's Dawn Hub in Ontario is investing USD 400 million to add 1.5 Bcf per day of deliverability for the province's grid as coal plants retire . India plans to triple gas-fired capacity by 2030, requiring aquifer and depleted-field projects in Gujarat and Rajasthan to modulate monsoon-related demand troughs.

High Capital Plus Cushion-Gas Cost Burden

CEDIGAZ pegs the cumulative investment need at EUR 100-170 billion through 2035, with depleted-reservoir conversions costing EUR 190 per MWh and greenfield caverns EUR 235 per MWh . Aquifer projects immobilize 45-80% of capacity in base gas; at 2025 spot prices near USD 3/MMBtu, a 10 Bcf site locks up USD 15-24 million that yields no revenue. India's government budgeted up to USD 2 billion for its strategic program, showing how fiscal pressure can delay timelines.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Security Diversification after Russia-Ukraine Crisis

- Integration of UGS with Low-Carbon Hydrogen Hubs

- Battery Storage & LNG Regasification as Competing Peakers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Depleted reservoirs delivered 78.5% of capacity in 2025, reflecting their favorable cushion-gas ratios of 20-40%, yet salt caverns are on a 9.1% CAGR trajectory because they enable hourly cycling and hydrogen storage. The underground gas storage market size for salt caverns is projected to expand faster than aquifers because caverns support deliverability of 1 Bcf per day or more, a crucial attribute for balancing renewable-heavy grids.

Capital efficiency still favors depleted fields for seasonal roles, but regulatory pushes toward hydrogen raise the appeal of caverns. Germany's BMWK foresees 250 caverns converting for 76-80 TWh hydrogen capacity by 2045. Centrica committed GBP 2 billion to ready the 54 Bcf Rough site for hydrogen by 2050, showing incumbents repositioning assets to defend the underground gas storage market share amid decarbonization.

Sites above 20 Bcf controlled 54% of installed capacity in 2025, led by mega-reservoirs such as Rough and Golden Triangle, which offer economies of scale and simplified offtake contracts. Still, 5-20 Bcf facilities will grow 6.8% annually as midstream operators acquire stranded fields near industrial clusters. Williams Companies' USD 1.95 billion purchase of 115 Bcf in Louisiana and Mississippi illustrates this scaling tactic.

Regulation nudges consolidation upward. The EPA methane rule applies to throughput above 50 MMcf per day, adding compliance costs that smaller sites struggle to absorb. Consequently, investors gravitate to larger assets with diversified revenue and lower unit costs, reinforcing a tilt toward the upper capacity tiers of the underground gas storage market.

Geography Analysis

North America held 37.9% of the underground gas storage market share in 2025, underpinned by more than 400 facilities totaling 4.8 Tcf of working capacity. The U.S. added 70 Bcf of demonstrated peak capacity after retrofits aligned with the EPA's 2024 methane rule, while Canada's Dawn Hub expansion targets 1.5 Bcf per day of new deliverability. Private-equity firms such as Sixth Street and Caliche bought Central Valley and Golden Triangle Storage to capture stable, inflation-hedged cash flows.

Energy-security imperatives drive Europe's capacity build. Germany stored 78 TWh by late 2024 under its refill decree, and BMWK foresees 2-7 TWh of hydrogen storage by 2030. The UK reopened Rough and earmarked GBP 2 billion for hydrogen conversion, while Denmark's Lille Torup caverns will tie into a 550 km pipeline to the Netherlands by 2030. Russia remains sizable but opaque as sanctions steer exports eastward.

Asia-Pacific represents the fastest-growing underground gas storage market, expanding 11.5% per year to 2031. China moved to sixth globally after adding 6 bcm of capacity and acquiring 10.97 bcm of working gas for USD 5.9 billion. India's Phase II program funds 3-4 bcm by 2030, and Japan's Osaka Gas invests USD 469 million for quake-proofed pipelines linked to underground storage. South Korea's Yeosu and Ulsan LNG terminals enhance peaking supply without geological barriers, while ASEAN states explore pilots to backstop nascent gas-fired power fleets.

- Gazprom

- PetroChina (CNPC)

- Royal Dutch Shell plc

- TotalEnergies SE

- Chevron Corp.

- Uniper SE

- Enbridge Inc.

- TC Energy Corp.

- NAFTA a.s.

- Eni SpA

- Storengy (ENGIE)

- Centrica Storage

- Kinder Morgan

- RWE Gas Storage

- INEOS Energy Storage

- Linde Engineering (Hydrogen Caverns)

- Enagas S.A.

- Osaka Gas Co.

- Gasunie (Gasunie UGS)

- Energinet DK

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for seasonal & strategic working gas

- 4.2.2 Growing gas-fired power generation & peak-shaving demand

- 4.2.3 Energy-security diversification after Russia-Ukraine crisis

- 4.2.4 Integration of UGS with low-carbon hydrogen hubs

- 4.2.5 Digital-twin & AI reservoir optimisation boosts economics

- 4.2.6 Methane-leakage regulations incentivising retrofit projects

- 4.3 Market Restraints

- 4.3.1 High capital plus cushion-gas cost burden

- 4.3.2 Environmental, seismic & brine-disposal risks

- 4.3.3 Battery-storage & LNG regasification as competing peakers

- 4.3.4 Net-zero policy uncertainty for long-lived gas assets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Depleted Gas Reservoirs

- 5.1.2 Salt Caverns

- 5.1.3 Aquifer Reservoirs

- 5.1.4 LNG Re-injection Facilities

- 5.2 By Storage-Capacity Class

- 5.2.1 Below 1 Bcf

- 5.2.2 1 to 5 Bcf

- 5.2.3 5 to 20 Bcf

- 5.2.4 Above 20 Bcf

- 5.3 By Application

- 5.3.1 Seasonal Storage

- 5.3.2 Strategic Reserve

- 5.3.3 Peak Shaving

- 5.3.4 Balancing and Load Management

- 5.4 By End-user

- 5.4.1 Gas and Power Utilities

- 5.4.2 Industrial and Petrochemical

- 5.4.3 Commercial/Residential Distributors

- 5.4.4 Mid-stream Operators

- 5.4.5 Government and Emergency Agencies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Gazprom

- 6.4.2 PetroChina (CNPC)

- 6.4.3 Royal Dutch Shell plc

- 6.4.4 TotalEnergies SE

- 6.4.5 Chevron Corp.

- 6.4.6 Uniper SE

- 6.4.7 Enbridge Inc.

- 6.4.8 TC Energy Corp.

- 6.4.9 NAFTA a.s.

- 6.4.10 Eni SpA

- 6.4.11 Storengy (ENGIE)

- 6.4.12 Centrica Storage

- 6.4.13 Kinder Morgan

- 6.4.14 RWE Gas Storage

- 6.4.15 INEOS Energy Storage

- 6.4.16 Linde Engineering (Hydrogen Caverns)

- 6.4.17 Enagas S.A.

- 6.4.18 Osaka Gas Co.

- 6.4.19 Gasunie (Gasunie UGS)

- 6.4.20 Energinet DK

7 Market Opportunities & Future Outlook

- 7.1 Hydrogen-ready cavern conversions

- 7.2 Digitalised smart-storage optimisation

- 7.3 Rising strategic stockpiles in emerging Asia

- 7.4 Modular micro-cavern solutions for LNG-to-gas projects