|

시장보고서

상품코드

2063256

웰헤드 컴포넌트 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Wellhead Component - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

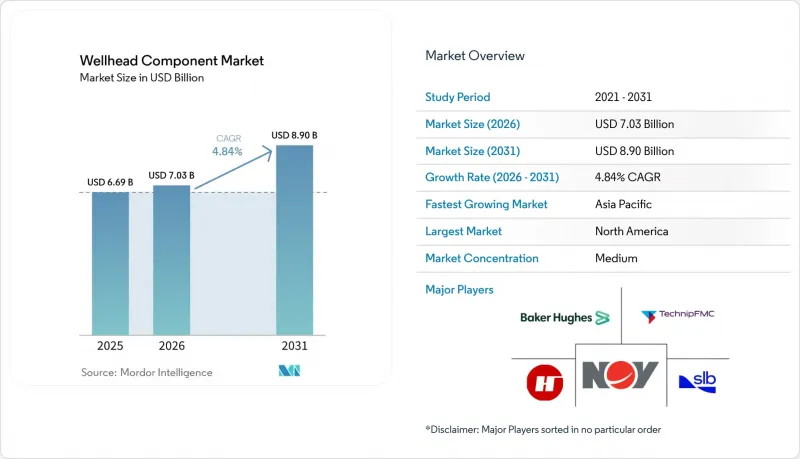

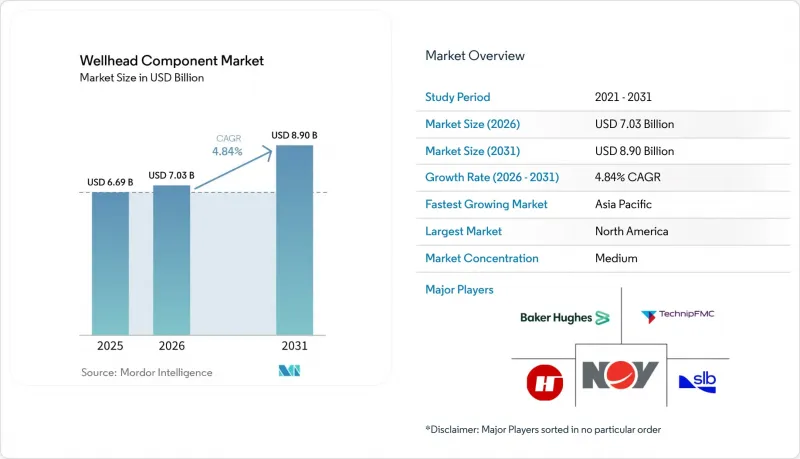

Mordor Intelligence에 의하면, 웰헤드 컴포넌트 시장 규모는 2025년에 66억 9,000만 달러로 평가되었고, 2026년에 70억 3,000만 달러로 추정되고, 2031년까지 89억 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 4.84%로 성장할 것으로 전망됩니다.

본 보고서는 컴포넌트별(케이싱 헤드, 케이싱 스풀 등), 내압 등급별(3,000 psi 이하 등), 설치 장소별(지상, 해저), 용도별(육상, 근해, 심해 및 초심해), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 웰헤드 컴포넌트 시장 동향 및 분석

전 세계 E&P 활동의 확대

2025-2026년, 광범위한 시추 작업이 아닌 수익성이 높은 자원에 초점을 맞춘 탐사 및 생산 예산의 선택적 회복이 예상됩니다. 쉐브론의 2026년 프로그램(180억-190억 달러)에서는 황화수소에 내성이 있는 15,000 psi 헤드가 필요한 퍼미안 분지와 텡기즈 유정에 예산의 60%가 배정되었습니다. 사우디아라비아의 1,000억 달러 규모 자프라 비전통 가스 프로젝트는 2030년까지 일일 20억 입방피트의 생산을 목표로 하고 있으며, 누출 배출을 억제하기 위해 15,000 psi의 메탈 씰 시스템을 채택하고 있습니다. 그 결과, 시추구 설비 수요는 절대적인 시추 장비 수에 좌우되는 것이 아니라 배럴당 50달러 미만의 프로젝트 손익분기점에 연동되게 되었으며, 설비 발주는 기존의 활동 지표와 분리되는 양상을 띠고 있습니다.

비전통 셰일 및 타이트층에 대한 투자 확대

2025-2026년 미국 셰일 분지에서는 더 긴 수평 시추공과 고밀도 패드 배치를 통해 20-30%의 효율 향상이 실현되었으며, 1에이커당 유정 부품 소비량이 증가했습니다. 580억 달러 규모의 데본-코텔라 합병을 통해 퍼미안 분지의 광구가 통합되었으며, 8-12개 유정의 패드가 최적화되었습니다. 이로 인해 케이싱 헤드나 행거에 가해지는 주기적인 압력 하중이 증가하고 있습니다. 아르헨티나의 바카 무에르타에는 2025년에 50억 달러의 해외 투자가 유입되었습니다. 현지 조달 규제로 인해 공급업체는 아르헨티나의 단조 업체와 제휴해야 하는 의무가 있어, 리드타임이 길어지고 공급망이 세분화되고 있습니다. 중국 쓰촨성에서 진행되는 타이트 가스 개발 사업에서는 15%의 황화수소 유량을 처리하기 위해 2상 스테인리스 스틸 헤드 사용이 의무화되어 있어, 수입된 고품질 연결 기술에 대한 수요가 발생하고 있습니다.

원유 가격 변동

2025-2026년 브렌트유 가격이 배럴당 55달러에서 85달러 사이에서 등락한 결과, 가격이 60달러 아래로 떨어졌을 때 서아프리카와 동남아시아에서 프로젝트의 15-20%가 연기되었습니다. 데본과 코테라의 합병과 같은 업계 재편으로 인해 소수의 통합 기업에 구매력이 집중되면서, 공급업체들은 이익률 하락을 감수하도록 압력을 받고 있습니다. TechnipFMC의 JXT-3 5,000 psi 트리와 같은 표준화된 사전 엔지니어링 플랫폼을 통해, 원유 가격이 60달러일 때도 프로젝트를 경제적으로 진행할 수 있게 되었습니다.

부문별 분석

밸브 어셈블리는 웰헤드 컴포넌트 시장에서 가장 빠르게 성장하고 있는 분야로, 2026-2031년 연평균 성장률(CAGR) 7.5%로 확대될 것으로 전망됩니다. 엑스프로(Expro)의 '솔러스(Solus)' 싱글 밸브 시어 앤드 씰 시스템은 2026년에 API 17G 인증을 획득하여 설치 시간을 절반으로 단축하고, 더 소형화된 BOP 스택에 적합함으로써 물류 비용을 20-30% 절감합니다. 케이싱 헤드는 압력 제어 및 유정 무결성 유지에 있어 필수적인 역할을 수행하고 있어, 2025년 웰헤드 컴포넌트 시장 점유율의 30.9%를 차지했습니다. 그러나 개보수 프로그램과 디지털 감시 기술의 도입으로 인해 수명이 연장되면서, 그 결과 교체 수요는 감소하고 있습니다. 튜빙 헤드, 스풀, 행거는 미국 내 셰일 패드 시추 활동 증가와 메탄 배출 규제를 준수하기 위한 금속 씰 인터페이스로의 전환으로 인해 수요가 크게 증가하고 있습니다. 또한, 운영자가 첨단 트리 시스템과의 호환성을 확보하기 위해 기존 유정을 업그레이드함에 따라 어댑터 스풀의 사용도 증가하고 있습니다. 또한, 밸브, 씰, 센싱 모듈을 결합한 통합 패키지를 제공하는 공급업체들은 웰헤드 컴포넌트 시장에서 경쟁력을 높이고 있습니다.

통합형 컴포넌트 제품군으로의 전환 추세는 운영사가 단일 공급업체의 보증을 선호하는 심해 타이백 분야에서 가장 두드러집니다. Plexus사가 2025년에 슈룸베르제(Schlumberger) 및 테크닙 FMC(TechnipFMC)에 POS-GRIP 라이선스를 부여함에 따라, 메탈 씰공급이 확대되어 2028년까지 미국 내 개조 수요의 15-20%를 차지할 것으로 전망됩니다. 한편, 캑터스 웰헤드(Cactus Wellhead)가 2026년에 베이커 휴즈(Baker Hughes)의 지상용 압력 제어 제품 라인의 65%를 인수함에 따라, 중동 및 라틴아메리카 전역에 턴키 방식의 헤드 플러스 밸브 키트를 공급할 수 있는 역량이 강화될 것입니다. 디지털 트윈이 표준화됨에 따라, 하드웨어의 차별화는 20년에 걸친 현장 수명 기간 동안 예측 유지보수 플랫폼에 데이터를 제공할 수 있는 임베디드 센서 어레이에 달려 있을 것입니다.

초고압 장비(5,000 psi 초과) 시장은 멕시코만, 브라질의 프레솔트층, 나이지리아의 심해 유전에서의 20,000 psi급 수요에 힘입어 연평균 성장률(CAGR) 7.9%로 확대될 것으로 전망됩니다. 2024년 20,000 psi 헤드를 사용하여 가동을 시작한 셰브론의 '앵커' 시범 프로젝트는 수심 7,000피트에서 해당 기술의 신뢰성을 입증했습니다. 이에 이어, Dril-Quip사의 20,000 psi 대응 머드라인 설계인 'BigBore II'는 서아프리카에서 2025년 계약 물량을 확보했습니다. 저압 헤드(3,000 psi 이하)는 2025년 유정 입구 부품 시장 규모의 41.5%를 차지했습니다. 이는 성숙한 육상 유전에서 광범위하게 사용되고 있기 때문입니다. 그러나 몇몇 주요 생산 지역에서 분지 개발이 포화 상태에 가까워짐에 따라 성장이 둔화되고 있습니다.

수심 100-400피트에서 비용 효율성이 중요한 동남아시아 및 중동의 대륙붕 가스전에서는 여전히 중압(3,001-5,000 psi) 시스템에 대한 수요가 주류를 이루고 있습니다. TechnipFMC사의 JXT-3 트리는 정격 5,000 psi임에도 불구하고 기존 설계보다 40% 가벼우며, 2025년에 말레이시아의 BIGST 및 인도네시아의 Mako 가스 프로젝트 수주를 따냈습니다. 멕시코만, 브라질, 나이지리아에서는 15,000-20,000 psi의 수압이 지정되어 있지만, 중동 및 북미의 육상 지역에서는 인필 유정을 대상으로 3,000 psi 이하로 설계된 설비의 재주문이 이어지고 있습니다.

지역별 분석

북미는 페르미안 분지에서 4,500개의 시추 작업이 시작되고 멕시코만 심해에서의 제재 해제가 재개된 데 힘입어, 2025년 매출의 40.1%를 차지했습니다. 그러나 Tier 1 셰일 매장량의 고갈과 브라질 및 서아프리카의 심해 프로젝트에 대한 설비 투자에 대한 관심이 높아짐에 따라, 해당 지역의 성장은 둔화되고 있습니다. 캐나다의 베이 뒤 노르(2028년 첫 원유 생산 예정)는 저수심용 시추 장비에 대한 틈새 수요를 창출하는 반면, 멕시코의 얕은 해역 프로젝트 입찰은 어려운 재정 여건으로 인해 정체되어 있습니다.

아시아태평양은 인도네시아의 노던 허브(6.6조 입방피트), 말레이시아의 BIGST(8억 입방피트/일), 그리고 2026년 4분기에 락 다 반에서 첫 원유 생산을 기록한 베트남의 심해 개발 프로젝트 덕분에 연평균 성장률(CAGR) 7.3%로 가장 빠르게 성장하고 있는 지역입니다. 파푸아 LNG, 스카버러 LNG 및 중국 남중국해 광구에서는 2028년까지 총 150기 이상의 해저 헤드가 필요하지만, 현지 조달 요건과 합금 단조품 공급 부족으로 인해 리드타임이 18-24개월로 늘어났습니다.

유럽에서는 노르웨이의 요한 스베르돌프 3단계(2025년 최종 투자 결정)와 영국의 로즈뱅크(2026년 첫 생산)가 고사양 주문에 대한 지속적인 수요를 뒷받침하고 있는 반면, 플렉서스의 2025년 북해 기본 계약은 폐쇄 및 폐광 수요를 흡수하고 있습니다.

중동 및 아프리카에서는 사우디 아람코의 자프라 프로젝트만으로도 2030년까지 수천 개의 15,000 psi 헤드가 필요할 것으로 예상되며, 2025년에 자금 조달이 이루어질 ADNOC의 하일 앤 가샤 산성 가스 프로젝트에서는 15,000 psi 등급의 내식성 합금 헤드 수요가 예상됩니다. 나이지리아의 봉가 노스나 앙골라의 새로운 프리솔트 탐사는 심해 개발의 성장을 뒷받침하고 있지만, 정치적 요인이나 현지 조달률 요건과 같은 장애물로 인해 일정이 지연되고 있습니다.

남미 시장은 브라질의 프레솔트 복합 개발을 원동력으로 성장하고 있으며, 2026년에는 부지오스 9호 및 메로 4호 FPSO가 인도되었습니다. 이들 모두는 15,000 psi 시스템을 갖춘 8-12개의 해저 시추공에 연결되어 있습니다. 아르헨티나의 YPF-페트로나스 LNG 합작 사업은 2025년 최종 투자 결정(FID)을 목표로 하고 있으며, 거시경제의 안정성이 유지된다면 2030년까지 2만 개의 신규 셰일 유정을 뒷받침하게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the wellhead component market size is projected to be USD 6.69 billion in 2025, USD 7.03 billion in 2026, and reach USD 8.90 billion by 2031, growing at a CAGR of 4.84% from 2026 to 2031.

This report is Segmented by Component (Casing Heads, Casing Spools, and More), Pressure Rating (Up To 3, 000 Psi, and More), Installation Location (Surface, Subsea), Application (Onshore, Offshore-Shallow, Offshore-Deep/Ultra-deep), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wellhead Component Market Trends and Insights

Growing Global E&P Activity

Selective rebounding of exploration and production budgets in 2025-2026 focused on high-margin resources instead of broad drilling campaigns. Chevron's USD 18-19 billion 2026 program earmarks 60% for Permian and Tengiz wells that require hydrogen-sulfide-resistant, 15 000-psi heads. Saudi Arabia's USD 100 billion Jafurah unconventional-gas project targets 2 billion cubic feet per day by 2030 and specifies metal-seal 15 000-psi systems to curb fugitive emissions . As a result, wellhead demand now follows project breakevens under USD 50 per barrel rather than absolute rig counts, decoupling equipment orders from traditional activity indicators.

Higher Investment in Unconventional Shale & Tight Plays

Efficiency gains of 20-30% in U.S. shale basins during 2025-2026, enabled by longer laterals and dense pad layouts, raised wellhead component consumption per acre. The USD 58 billion Devon-Coterra merger consolidated Permian acreage, optimizing eight-to-12-well pads that place heavier cyclic-pressure loads on casing heads and hangers. Argentina's Vaca Muerta attracted USD 5 billion of 2025 foreign investment; local-content rules oblige suppliers to partner with Argentine forges, widening lead times and fragmenting the supply chain. China's Sichuan tight-gas push mandates duplex-stainless heads to manage 15% hydrogen-sulfide streams, creating openings for imported premium-connection technology.

Crude-Oil Price Volatility

Brent fluctuations between USD 55 and USD 85 per barrel through 2025-2026 triggered 15-20% project deferrals in West Africa and Southeast Asia when prices dipped below USD 60. Consolidation, such as the Devon-Coterra deal, concentrates buying power with fewer integrated players, pressuring suppliers to accept lower margins. Standardized, pre-engineered platforms like TechnipFMC's JXT-3 5 000-psi tree now enable projects to proceed economically even at USD 60 oil.

Other drivers and restraints analyzed in the detailed report include:

- Deep- & Ultra-Deepwater Project Sanctions

- Digital-Twin Predictive Maintenance Adoption

- Stringent Environmental & Methane-Leak Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Valve assemblies represented the fastest-growing slice of the wellhead components market, forecast to advance at 7.5% CAGR over 2026-2031. Expro's Solus single-valve shear-and-seal system, API 17G-qualified in 2026, halves installation time and fits smaller BOP stacks, reducing logistics costs by 20-30%. Casing heads accounted for 30.9% of the wellhead components market share in 2025, driven by their essential role in pressure control and maintaining well integrity. However, refurbishment programs and the adoption of digital monitoring technologies are extending their service life, thereby reducing replacement demand. Tubing heads, spools, and hangers are experiencing strong demand due to increased U.S. shale pad drilling activity and the transition to metal-seal interfaces to comply with methane-emission regulations. Adapter spools are also seeing increased adoption as operators upgrade legacy wells to ensure compatibility with advanced tree systems. Additionally, suppliers offering integrated packages that combine valves, seals, and sensing modules are enhancing their competitive position in the wellhead components market.

The push toward integrated component suites is strongest in deepwater tie-backs, where operators prefer single-source warranties. Plexus's 2025 licensing of POS-GRIP to Schlumberger and TechnipFMC expands metal-seal availability and positions the technology for 15-20% of U.S. retrofit demand by 2028. Meanwhile, Cactus Wellhead's 2026 purchase of 65% of Baker Hughes' surface pressure-control line boosts its ability to supply turnkey head-plus-valve kits throughout the Middle East and Latin America. As digital twins become standard, hardware differentiation will hinge on embedded sensor arrays that can feed predictive-maintenance platforms over a 20-year field life.

Ultra-high-pressure equipment (above 5 000 psi) is projected to grow at 7.9% CAGR, fueled by 20 000-psi Gulf of Mexico, Brazil pre-salt, and Nigeria deepwater fields. Chevron's Anchor pilot, which came onstream in 2024 using 20 000-psi heads, proved the technology's reliability at 7 000 ft water depth. Dril-Quip's BigBore II 20 000-psi mudline design subsequently secured 2025-award slots in West Africa. Low-pressure heads (≤3,000 psi) are projected to account for 41.5% of the wellhead components market size in 2025. This is attributed to their extensive use in mature onshore fields. However, growth is slowing as basin development nears saturation in several established production regions.

Mid-range 3 001-5 000 psi systems demand remains standard for Southeast Asian and Middle Eastern shelf gas, where water depth is 100-400 ft, and costs matter. TechnipFMC's JXT-3 tree, 5 000 psi-rated yet 40% lighter than conventional designs, secured Malaysia BIGST and Indonesia Mako gas awards in 2025. The Gulf of Mexico, Brazil, and Nigeria specify 15 000-20 000 psi heads, while onshore Middle East and North America continue to reorder ≤3 000 psi designs for infill wells.

Geography Analysis

North America controlled 40.1% of 2025 revenue, anchored by 4 500 Permian spuds and resurging Gulf of Mexico deepwater sanctions. Yet, regional growth is slowing due to the depletion of tier-1 shale inventory and a growing focus on capital investment in deepwater projects in Brazil and West Africa. Canada's Bay du Nord (first oil 2028) will add niche demand for cold-water-rated heads, whereas Mexico's shallow-water tenders languish under tight fiscal terms.

Asia-Pacific is the fastest-growing territory at a 7.3% CAGR thanks to Indonesia's Northern Hub (6.6 tcf), Malaysia's BIGST (800 MMcfd), and Vietnam's deepwater campaign that logged first oil at Lac Da Vang in Q4 2026. Papua LNG, Scarborough LNG, and China's South China Sea blocks collectively require 150-plus subsea heads by 2028, but local-content and alloy-forging gaps extend lead times to 18-24 months.

In Europe. Norway's Johan Sverdrup Phase 3 (FID 2025) and the U.K.'s Rosebank (first oil 2026) keep a residual flow of high-spec orders, while Plexus's 2025 North Sea framework exploits plug-and-abandonment demand.

In the Middle East and Africa, Saudi Aramco's Jafurah program alone necessitates thousands of 15 000-psi heads through 2030, and ADNOC's Hail & Ghasha sour-gas project, financed in 2025, requires corrosion-resistant alloy heads rated at 15 000 psi. Nigeria's Bonga North and Angola's new pre-salt probes add deepwater growth, although political and local-content hurdles stretch schedules. The

South America market is rising on the strength of Brazil's pre-salt complex, which delivered Buzios 9 and Mero 4 FPSOs in 2026, each tied to 8-12 subsea wells equipped with 15 000-psi systems. Argentina's YPF-Petronas LNG joint venture, targeting FID 2025, underpins 20 000 new shale wellheads by 2030, provided macro-economic stability holds.

- Schlumberger

- Halliburton

- Baker Hughes

- Weatherford

- NOV

- TechnipFMC

- Weir Oil & Gas

- Dril-Quip

- Aker Solutions

- Cameron (Schlumberger)

- Cactus Wellhead

- Forum Energy Technologies

- Plexus Holdings

- Vallourec

- Expro Group

- Welltec

- T3 Energy Services

- Jiangsu Sanyi Petroleum

- Jereh Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing global E&P activity

- 4.2.2 Higher investment in unconventional shale & tight plays

- 4.2.3 Deep- & ultra-deepwater project sanctions

- 4.2.4 Digital-twin predictive maintenance adoption

- 4.2.5 Modular compact wellhead systems for small LNG tie-backs

- 4.2.6 CCS well conversions needing retrofit wellheads

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility

- 4.3.2 Stringent environmental & methane-leak regulations

- 4.3.3 Supply-chain bottlenecks for high-spec alloy forgings

- 4.3.4 Cyber-security risks in smart wellhead controls

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component

- 5.1.1 Casing Heads

- 5.1.2 Casing Spools

- 5.1.3 Tubing Heads

- 5.1.4 Hangers

- 5.1.5 Valves

- 5.1.6 Seals and Gaskets

- 5.1.7 Adapter Spools

- 5.2 By Pressure Rating

- 5.2.1 Up to 3,000 psi

- 5.2.2 3,001 to 5,000 psi

- 5.2.3 Above 5,000 psi

- 5.3 By Installation Location

- 5.3.1 Surface (Land and Platform)

- 5.3.2 Subsea

- 5.4 By Application

- 5.4.1 Onshore

- 5.4.2 Offshore - Shallow

- 5.4.3 Offshore - Deep/Ultra-deep

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Schlumberger

- 6.4.2 Halliburton

- 6.4.3 Baker Hughes

- 6.4.4 Weatherford

- 6.4.5 NOV

- 6.4.6 TechnipFMC

- 6.4.7 Weir Oil & Gas

- 6.4.8 Dril-Quip

- 6.4.9 Aker Solutions

- 6.4.10 Cameron (Schlumberger)

- 6.4.11 Cactus Wellhead

- 6.4.12 Forum Energy Technologies

- 6.4.13 Plexus Holdings

- 6.4.14 Vallourec

- 6.4.15 Expro Group

- 6.4.16 Welltec

- 6.4.17 T3 Energy Services

- 6.4.18 Jiangsu Sanyi Petroleum

- 6.4.19 Jereh Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment