|

시장보고서

상품코드

2063257

풍력 터빈 발전기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Wind Turbine Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

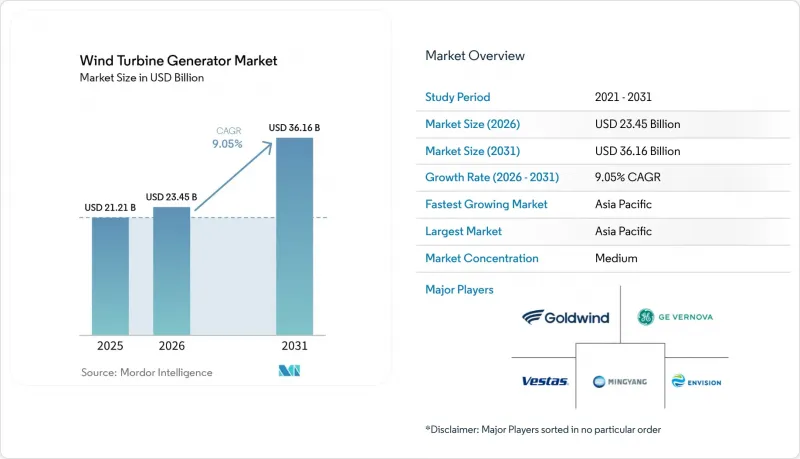

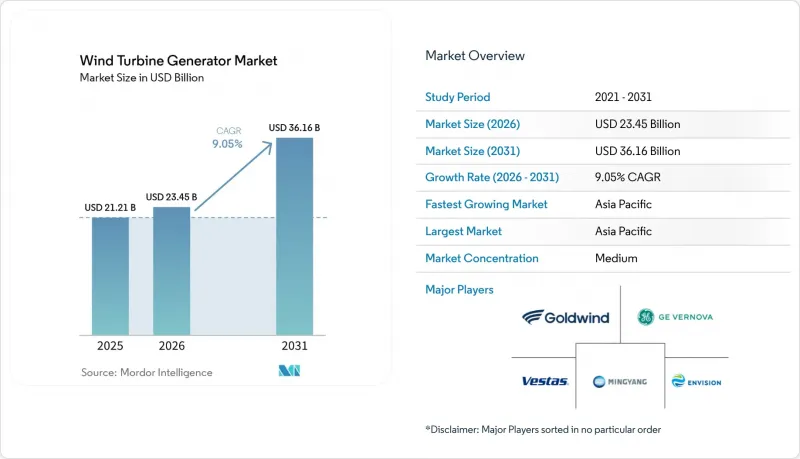

Mordor Intelligence에 의하면, 풍력 터빈 발전기 시장 규모는 2025년 212억 1,000만 달러로 평가되었습니다. 2026년 234억 5,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 9.05%를 나타내, 2031년까지 361억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 발전기 유형(PMSG, DFIG, 기존 동기 발전기 등), 정격 출력(2MW 미만, 2-5MW 등), 용도(육상, 기타), 최종 사용자(유틸리티·IPP, 산업용 자가소비, 상업·마이크로그리드), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 풍력 터빈 발전기 시장 동향 및 분석

PMSG 기술 분야의 급속한 비용 절감

중국 및 유럽 제조업체들이 자기 회로를 최적화하고 자동 권선 라인을 확대한 결과, 2024년부터 2026년 초까지 PMSG 시스템의 가격이 22% 하락했습니다. 재활용된 하드 디스크 드라이브에서 확보된 2차 희토류 공급으로 인해, 2025년에는 4,200톤의 네오디뮴이 추가로 공급되면서, 전년도 Kg당 160달러까지 급등했던 현물 가격이 하락세를 보였습니다. Goldwind와 Ming Yang은 자사가 소유한 자석 공장을 활용해 메가와트당 21만 달러에 PMSG 나셀을 공급했으며, 이는 유럽의 제시 가격보다 15% 낮은 수준이어서 2025년 아시아태평양 수주의 68%를 확보했습니다. 지멘스 가메사의 5.X 플랫폼에 채택된 모듈식 고정자 덕분에 조립 작업이 30% 감소하여, 중량물용 크레인이 부족한 시장에서도 직접 드라이브를 구현할 수 있게 되었습니다. 현재 18개월을 넘는 장기 해상 정비 주기가 정착되어 있어, 고비용이 드는 잭업 작업을 피할 수 있는 기어리스 PMSG 방식이 유리해지고 있습니다.

해상 풍력 발전 목표가 직접 드라이브 수요를 끌어올립니다.

유럽연합(EU)은 2025년에 22.5GW 규모의 해상 풍력 발전 설비를 설치했으며, 이 중 78%는 2년마다 실시되는 유지보수 기간에 대응하기 위해 정격 출력 12MW 이상의 직접 드라이브 PMSG를 채택했습니다. 중국은 해상 풍력 발전의 가동 중단 시간의 3분의 1을 차지하던 기어박스 고장 원인을 해결한 17MW 및 20MW 프로토타입을 현장 시험했습니다. 베스타스는 북해에서 진행한 시범 사업에서 94%의 설비 가동률을 달성한 V236-15MW 모델에 대한 4.2GW 규모의 수주를 확보했습니다. 이는 동급의 DFIG(이중 고정 자기장) 터빈군보다 8포인트 높은 수치입니다. 하이윈드 탄펜사는 나셀의 중량을 120톤으로 제한했으나, 이 기준은 부문화된 아이언리스 로터를 갖춘 소형 PMSG 유닛을 통해 충족되고 있습니다. 새로운 IEC 61400-3-2 부유식 규격은 회전 부품이 적고 비틀림 공진 위험이 낮은 직접 드라이브 방식을 권장하는 방향을 더욱 강화하고 있습니다.

희토류 공급 변동이 PMSG 비용을 끌어올리고 있습니다.

중국의 자석용 합금 수출 규제에 따라 2025년 초 네오디뮴 가격이 Kg당 160달러까지 상승했으며, PMSG의 부품 원가는 메가와트당 8만 달러 증가했습니다. 유럽과 북미는 희토류 수요의 90% 이상을 수입에 의존하고 있어, 이 프로젝트는 환율 변동과 정치적 위험에 노출되어 있습니다. 재활용이 일시적인 완충 역할을 했지만, 작년 전 세계 자석 수요 중 재활용 공급이 충당할 수 있었던 비중은 고작 12%에 불과했습니다. 경량 고온 초전도 발전기는 자석을 사용하지는 않지만, 극저온 시스템이기 때문에 여전히 비용이 많이 듭니다. 2028년 이후 호주, 캐나다, 탄자니아의 다양한 광산이 본격적으로 가동되기 전까지는 PMSG 가격의 불확실성이 입찰 예산에 부담을 줄 것입니다.

부문별 분석

고온 초전도(HTS) 유닛용 풍력 터빈 발전기 시장 규모는 현재 작지만, 부유식 개발 사업자들이 1메가와트당 8톤 미만의 나셀 중량을 추구함에 따라 2031년까지 연평균 성장률(CAGR) 15.6%를 나타낼 전망입니다. DFIG 시스템은 낮은 자본 비용과 광범위한 서비스 네트워크 덕분에 2025년 시점에서 54.9%의 시장 점유율을 유지했습니다. 영구자석 동기 발전기(PMSG)의 채택이 급속히 확대되고 있으며, 특히 12MW를 초과하는 용량의 해상 풍력 터빈에서 그 추세가 두드러집니다. 이 터빈들은 기어박스가 제거되어 있어 유지보수 필요성이 줄어들고 점검 주기가 연장됩니다. 기존의 동기 발전기는 틈새 전력계통 형성의 역할을 담당하고 있으며, 스위치드 릴랙턴스 방식의 개념은 여전히 실용화 전 단계에 있습니다.

3.6 MW급 EcoSwing 발전기와 같은 HTS 프로토타입은 1메가와트당 11톤의 중량비를 달성했으며, 희토류 자석을 배제함으로써 대당 6만 5,000달러의 재료비를 절감했습니다. 보다 엄격한 저전압 라이드스루 규격을 충족하기 위해서는 DFIG의 업그레이드가 필요해졌으며, 이에 따라 그 비용 경쟁력은 점차 약화되고 있습니다. 5-10MW급에서는 PMSG(영구자석 동기 발전기)의 직접 드라이브 방식이 주류를 이루고 있으며, 분할된 고정자 덕분에 일반 도로를 통한 운송 및 현장에서의 조립이 가능합니다. 블랙 스타트 기능이 필요한 마이크로그리드에는 여전히 기존의 동기 발전기가 채택되고 있지만, 축전지의 보급으로 인해 그 우위는 점차 줄어들고 있습니다. 80데시벨을 초과하는 스위치드 릴랙턴스 발전기의 소음 문제로 인해 주거지 인근에서의 도입이 제한되어, 보급 확대가 더딘 상황입니다.

2-5MW급은 2025년 설치 건수의 64.5%를 차지하며, 대부분의 육상 부지에서 적용되는 800톤급 이동식 크레인 제한 기준을 여전히 충족했습니다. 5-10MW 부문은 리파워링 계획을 통해 발전소 1기당 에너지 생산량을 3배로 늘리고 토목 공사를 절반으로 줄일 수 있는 소수의 발전 단위가 선호됨에 따라, 2026년 이후에는 연평균 성장률(CAGR) 12.0%를 나타낼 전망입니다. 개발 사업자들이 50% 이상의 설비 가동률을 추구하는 가운데, 10MW를 초과하는 기종은 작년 해상 수주량의 14%를 차지했습니다.

잭업식 시추선의 일당 비용이 27만 달러에 육박함에 따라, 소형 터빈 3기와 비교해 선박 가동 시간을 40% 단축할 수 있는 15MW급 유닛의 도입이 촉진되고 있습니다. 나셀의 모듈 분할 방식 덕분에, 7MW 육상형 모델은 6개의 고정자 섹션을 트럭으로 운송함으로써 도로 중량 규정을 충족할 수 있습니다. 태풍이 빈번하게 발생하는 지역의 보험 보상 한도는 터빈 1기당 1,800만 달러로 설정되어 있으며, 이로 인해 동아시아에서는 15MW를 초과하는 단일 유닛의 도입이 억제되고 있습니다. 배전 사업자의 규제로 인해 ‘계량기 뒤쪽’의 풍력 발전 용량이 2MW로 제한된 지역, 지역 경관 보전 차원에서 허브 높이가 낮은 기종이 요구되는 지역에서는 2MW 미만의 터빈이 여전히 주류를 이루고 있습니다.

지역별 분석

아시아태평양은 2025년 풍력 터빈 발전기 시장 매출의 42.8%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 9.7%로 확대될 것으로 전망됩니다. 중국의 연간 설치량이 100GW를 넘어섰다는 점과 17MW 규모의 부유식 발전 설비 시제품 개발이 이 지역의 선도적 지위를 뒷받침하고 있습니다. 인도는 9GW 규모의 송전망 현대화 작업을 신속히 추진한 결과, 2025년에 6.3GW를 추가했으나, 라자스탄주에서는 여전히 2단계 미수주 물량이 남아 있습니다. 일본과 한국에서는 태풍으로 인한 베어링 고장을 방지하고 보험사의 요건을 충족하기 위해 클래스 T 인증 터빈의 사용이 의무화되어 있습니다. 사이클론이 빈번하게 발생하는 지역인 베트남과 필리핀과 2.8GW 규모의 계약을 체결했는데, 모든 계약에서 실시간 상태 모니터링 기능을 갖춘 PMSG(영구자석 동기 발전기)가 지정되었습니다.

유럽에서는 2030년까지 120GW를 목표로 하는 REPowerEU 정책에 따라 22.5GW 규모의 해상 풍력 발전 설비가 설치되어 있습니다. 독일은 680MW 규모의 육상 풍력 발전 설비를 리파워링하여, 새로운 송전망 노드를 추가하지 않고도 부지당 메가와트 밀도를 3배로 높였습니다. 영국의 10GW 규모 부유식 해상 풍력 발전 임대 계약에서는 나셀의 질량을 1MW당 8톤 미만으로 규정하고 있으며, 이 기준이 HTS 발전기의 도입을 가속화하고 있습니다. 북유럽의 송전 계통 연계선을 통해 잉여 해상 전력을 수출할 수 있게 되었으며, 바람의 영향을 전적으로 받는 북해의 풍력 발전 단지에서 설비 가동률을 94% 가까이 유지하고 있습니다. 프랑스에서는 시각적 영향을 최소화하기 위해 15MW급 직접 드라이브 방식 발전기를 도입한 브르타뉴 및 노르망디 지역의 프로젝트(총 3.2GW)가 진행되고 있습니다.

북미에서는 미국이 2,600GW에 달하는 송전망 연결 대기 목록이 있음에도 불구하고 11.2GW를 증설했으며, 2028년까지 38GW를 확보하기 위해 FERC 지침 2023에 기대를 걸고 있습니다. 캐나다는 앨버타주와 서스캐처원주를 중심으로 2.4GW 규모의 계약을 체결했습니다. 이 지역들에서는 5MW 이상의 발전기가 유지보수 시간을 단축하고 있습니다. 브라질의 828MW 규모 돔 이노센시오 풍력발전소와 아르헨티나의 230MW 규모 에스키나 도 벤토는 40%의 설비 가동률을 무기로 장기 전력구매계약(PPA)을 체결했습니다. 중동 및 아프리카에서는 사우디아라비아의 3GW 규모 메가 팜이 1kWh당 1.33센트라는 기록적인 전력 판매 가격을 책정하고, 사막의 더위를 견딜 수 있는 7.7MW급 PMSG 터빈을 선정했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the wind turbine generator market size is expected to grow from USD 21.21 billion in 2025 to USD 23.45 billion in 2026 and is forecast to reach USD 36.16 billion by 2031 at 9.05% CAGR over 2026-2031.

This report is Segmented by Generator Type (PMSG, DFIG, Conventional Synchronous, and More), Capacity Rating (Below 2 MW, 2-5 MW, and More), Application (Onshore, and More), End-User (Utilities & IPPs, Industrial Captive, Commercial & Micro-Grids), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wind Turbine Generator Market Trends and Insights

Rapid Cost Reductions in PMSG Technology

PMSG system prices fell 22% between 2024 and early 2026 as Chinese and European manufacturers optimized magnet circuits and scaled automated winding lines. Secondary rare-earth supply from recycled hard-disk drives added 4,200 tonnes of neodymium in 2025, softening spot prices that had spiked to USD 160 per kilogram a year earlier . Goldwind and Ming Yang leveraged captive magnet plants to offer PMSG nacelles at USD 210,000 per megawatt, undercutting European quotes by 15% and winning 68% of Asia-Pacific orders in 2025. Modular stators on Siemens Gamesa's 5. X platform trimmed assembly labor 30%, making direct-drive viable in markets that lack heavy-lift cranes . Longer offshore service intervals now exceeding 18 months favor gearless PMSG machines that avoid costly jack-up interventions.

Offshore Wind Targets Boosting Direct-Drive Demand

The European Union installed 22.5 GW offshore in 2025, with 78% using direct-drive PMSGs rated above 12 MW to meet two-year maintenance windows . China field-tested 17 MW and 20 MW prototypes that retired gearbox failure modes responsible for one-third of offshore downtime. Vestas booked 4.2 GW of V236-15 MW orders that achieved 94% capacity factors in North Sea pilots, eight points above comparable DFIG fleets. Hywind Tampen capped nacelle mass at 120 tonnes, a threshold met by compact PMSG units with segmented ironless rotors. New IEC 61400-3-2 floating rules reinforce preference for direct-drive models with fewer rotating parts and lower torsional resonance risk.

Rare-Earth Supply Volatility Inflating PMSG Costs

Neodymium prices climbed to USD 160 per kilogram in early 2025 after export curbs on Chinese magnet alloys, boosting PMSG bills of material by USD 80,000 per megawatt. Europe and North America rely on imports for more than 90% of rare-earth needs, exposing projects to currency swings and political risk. Recycling added a temporary buffer, yet the secondary supply covered only 12% of global magnet demand last year. Lighter High-Temperature Superconducting generators avoid magnets but remain cost-intensive due to cryogenic systems. Until diversified mines in Australia, Canada, and Tanzania are fully commissioned after 2028, PMSG price uncertainty will pressure tender budgets.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Code Revisions Requiring Variable-Speed Operation

- Corporate PPAs Driving Utility-Scale Rollouts

- Transmission Interconnection Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The wind turbine generator market size for High-Temperature Superconducting (HTS) units is small today, yet it will expand at a 15.6% CAGR through 2031 as floating developers chase nacelle mass below 8 tonnes per megawatt. DFIG systems retained 54.9% market share in 2025 thanks to lower capital cost and extensive service networks. The adoption of Permanent Magnet Synchronous Generators (PMSG) is growing rapidly, especially in offshore turbines with capacities exceeding 12 MW. The removal of the gearbox in these turbines reduces maintenance needs and extends service intervals. Conventional synchronous units satisfy niche grid-forming roles, and switched-reluctance concepts remain pre-commercial.

HTS prototypes like the 3.6 MW EcoSwing generator achieved an 11-tonne-per-megawatt ratio and removed rare-earth magnets, cutting material exposure by USD 65,000 per machine. DFIG upgrades are now needed to meet stricter low-voltage ride-through codes, eroding their cost edge. PMSG direct-drive units dominate the 5-10 MW bracket, where segmented stators allow road-legal transport and on-site assembly. Conventional synchronous machines still equip micro-grids that need black-start capability, but batteries are narrowing that advantage. Switched-reluctance noise issues above 80 decibels limit deployment near communities, delaying broader uptake.

The 2 to 5 MW class represented 64.5% of 2025 installations and continues to align with 800-tonne mobile crane limits on most onshore sites. The 5 to 10 MW segment will grow at 12.0% CAGR after 2026 as repowering programs favor fewer units that triple energy output per foundation and cut civil works in half. Machines above 10 MW grabbed 14% of offshore orders last year as developers chase capacity factors beyond 50%.

Jack-up day rates near USD 270,000 incentivize 15 MW units that cut vessel time 40% compared with three smaller turbines. Modular nacelle splits let 7 MW onshore models meet road-weight regulations by trucking six stator sections. Insurance limits in typhoon zones cap coverage at USD 18 million per turbine, which discourages single-unit capacities above 15 MW in East Asia. Sub-2 MW turbines persist where distribution-utility rules cap behind-the-meter wind at 2 MW and where community aesthetics drive demand for lower hub heights.

Geography Analysis

Asia-Pacific held 42.8% of the 2025 wind turbine generator market revenue and is forecast to expand at 9.7% CAGR to 2031. China's >100 GW annual installation run rate and its prototype 17 MW floating units underpin regional leadership. India added 6.3 GW in 2025 after fast-tracking 9 GW of grid upgrades, though a second-tier backlog in Rajasthan persists. Japan and South Korea now mandate Class T certified turbines to satisfy insurers after typhoon-related bearing failures. Vietnam and the Philippines signed 2.8 GW of contracts in cyclone zones, all specifying PMSGs with real-time condition monitoring.

Europe is installing 22.5 GW offshore under the REPowerEU policy that targets 120 GW by 2030. Germany repowered 680 MW of onshore capacity, tripling megawatt density per site without adding new grid nodes. The United Kingdom's 10 GW floating offshore leases stipulate nacelle mass below 8 tonnes per megawatt, a criterion that accelerates HTS generator adoption. Nordic interconnectors enable export of surplus offshore power and sustain capacity factors near 94% on fully exposed North Sea arrays. France advanced 3.2 GW of Brittany and Normandy projects that adopt 15 MW direct-drive machines to minimize visual impact.

In North America, the U.S. added 11.2 GW despite the 2,600 GW interconnection queue and is banking on FERC Order 2023 to unlock 38 GW by 2028. Canada closed 2.4 GW of contracts centered in Alberta and Saskatchewan, where 5 MW-plus machines lower service person-hours. Brazil's 828 MW Dom Inocencio wind farm and Argentina's 230 MW Esquina do Vento leveraged 40% capacity factors to win long-dated PPAs. In the Middle East and Africa, Saudi Arabia's 3 GW mega-farm set a record 1.33 cents per kilowatt-hour tariff and selected 7.7 MW PMSG turbines that withstand desert heat.

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems A/S

- GE Vernova

- Nordex Group

- Mitsubishi Heavy Industries

- Suzlon Energy Ltd.

- Enercon GmbH

- Goldwind

- Envision Energy

- Ming Yang Smart Energy

- Dongfang Electric Corporation

- CSIC Haizhuang Wind Power

- Senvion GmbH

- Doosan Enerbility

- Hitachi Ltd.

- ABB Ltd.

- Siemens Energy AG

- Lagerwey (Enercon Group)

- Bergey WindPower Co.

- Inox Wind Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid cost reductions in PMSG technology

- 4.2.2 Offshore wind targets boosting high-capacity direct-drive demand

- 4.2.3 Grid-code revisions mandating advanced variable-speed generators

- 4.2.4 Corporate PPAs accelerating utility-scale installations

- 4.2.5 Repowering schemes creating retrofit demand

- 4.2.6 Floating offshore pilots driving lightweight generator designs

- 4.3 Market Restraints

- 4.3.1 Rare-earth supply volatility inflating PMSG costs

- 4.3.2 Transmission interconnection delays

- 4.3.3 Crane weight limits restricting large onshore units

- 4.3.4 Insurance premium hikes from bearing-failure risk in typhoon zones

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Generator Type

- 5.1.1 Permanent-Magnet Synchronous Generator (PMSG)

- 5.1.2 Doubly-Fed Induction Generator (DFIG)

- 5.1.3 Conventional Synchronous Generator

- 5.1.4 Conventional Induction Generator

- 5.1.5 Switched Reluctance Generator

- 5.2 By Capacity Rating

- 5.2.1 Below 2 MW

- 5.2.2 2 to 5 MW

- 5.2.3 5 to 10 MW

- 5.2.4 Above 10 MW

- 5.3 By Application

- 5.3.1 Onshore

- 5.3.2 Offshore (Fixed-bottom)

- 5.3.3 Floating Offshore

- 5.4 By End-user

- 5.4.1 Utilities and IPPs

- 5.4.2 Industrial Captive

- 5.4.3 Commercial and Micro-grids

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Siemens Gamesa Renewable Energy

- 6.4.2 Vestas Wind Systems A/S

- 6.4.3 GE Vernova

- 6.4.4 Nordex Group

- 6.4.5 Mitsubishi Heavy Industries

- 6.4.6 Suzlon Energy Ltd.

- 6.4.7 Enercon GmbH

- 6.4.8 Goldwind

- 6.4.9 Envision Energy

- 6.4.10 Ming Yang Smart Energy

- 6.4.11 Dongfang Electric Corporation

- 6.4.12 CSIC Haizhuang Wind Power

- 6.4.13 Senvion GmbH

- 6.4.14 Doosan Enerbility

- 6.4.15 Hitachi Ltd.

- 6.4.16 ABB Ltd.

- 6.4.17 Siemens Energy AG

- 6.4.18 Lagerwey (Enercon Group)

- 6.4.19 Bergey WindPower Co.

- 6.4.20 Inox Wind Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment