|

시장보고서

상품코드

2063263

풍력 터빈 기초 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Wind Turbine Foundation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

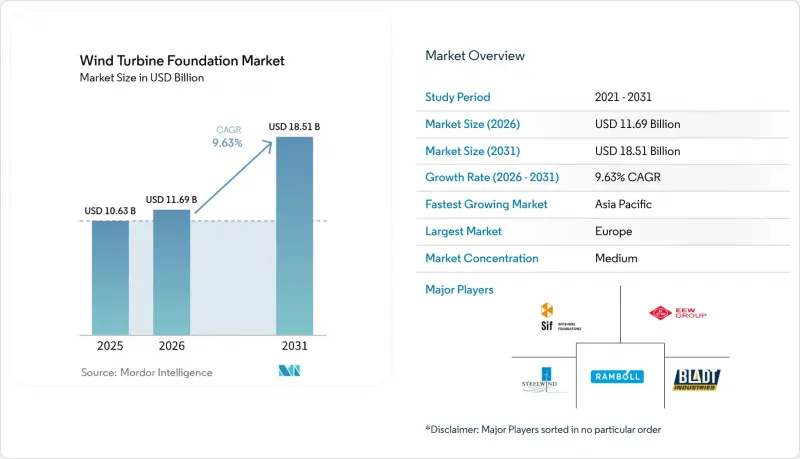

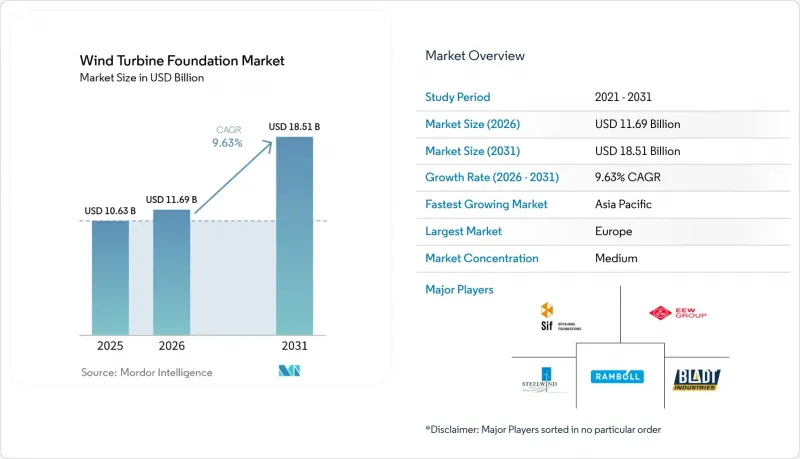

Mordor Intelligence에 의하면, 풍력 터빈 기초 시장 규모는 2025년에 106억 3,000만 달러로 평가되었습니다. 2026년 116억 9,000만 달러에서 2031년까지 185억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 9.63%를 나타낼 전망입니다.

본 보고서는 기초 유형(중력식 구조, 기타), 재질(콘크리트, 강철, 복합재/하이브리드), 설치 장소(육상, 기타), 터빈 정격(2MW 미만, 기타), 최종 용도(유틸리티 규모, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 풍력 터빈 기초 시장 동향 및 인사이트

세계의 탄소중립 목표에 따른 해상 풍력 발전소 건설의 급속한 확대

2025년부터 2026년에 걸쳐, 2024년 기준에서 이미 가동 중인 83GW에 더해, 2050년까지 탄소중립을 목표로 하는 각국 정부는 약 100GW 규모의 해상 풍력 발전 용량을 경매에 부쳤습니다. 유럽의 ‘REPowerEU’ 계획만 해도 2050년까지 300GW를 목표로 하고 있는 반면, 미국의 ‘인플레이션 감축법’에 따른 청정 에너지 인센티브는 프로젝트의 내부수익률(IRR)을 최대 3퍼센트 포인트 끌어올리고 있습니다. 중국의 ‘제14차 5개년 계획’에서는 2030년까지 50GW 규모의 해상 풍력 발전을 목표로 하고 있으며, 이는 제조 능력을 상회하는 국내 건설 프로그램을 뒷받침하고 있습니다. 이에 따라 XXL 모노파일의 리드타임이 24개월로 늘어났으며, 개발 사업자들은 2029년까지의 할당량을 확보할 수밖에 없는 상황입니다. Sif Group과 같이 자동화 생산 라인과 심수 부두를 갖춘 제조업체들은 2026년도 EBITDA 전망치가 전년 대비 181% 증가하는 등 프리미엄 가격을 확보하고 있습니다.

15MW 이상의 터빈에는 XXL 사이즈의 기초가 필요합니다.

차세대 터빈은 10MW 모델보다 40% 더 높은 추력 하중을 발생시키기 때문에 모노파일은 직경 10m, 길이 120m, 무게 2,400t 규모로 확대될 수밖에 없습니다. 항만의 수심이 병목 현상이 되고 있어, 현재 10m를 초과하는 모노파일을 처리할 수 있는 곳은 에스비알, 브레머하펜, 에이블 시튼, 마스프락테 II뿐입니다. EEW와 CS Wind는 Nordlicht 1 프로젝트의 초기 단계에 필요한 모노파일을 예정보다 빨리 납품했으며, 로봇 용접을 통해 전체 길이 100m에 걸쳐 치수 공차를 5mm 이내로 유지할 수 있음을 입증했습니다. 현재 이 부문의 경쟁력은 120mm를 초과하는 두께의 강판을 압연할 수 있는 제철소와 실시간 품질 관리를 통합한 제조업체에 달려 있습니다. RWE가 2028년까지 32만 톤의 두꺼운 강판을 확보하고 있다는 사실은 대규모 구매자들이 제한된 생산 능력을 빠르게 확보하고 있는 실태를 보여줍니다.

심해용 부유식 솔루션에 대한 막대한 설비 투자

부유식 기초의 비용은 1메가와트당 약 340만 유로이며, 이 중 플랫폼 제조 및 운송에 최대 140만 달러, 설치 및 계류에 최대 450만 유로가 소요됩니다. 선박의 용선료는 하루당 23만 4,000달러에서 35만 1,000달러 사이이며, 선박 1척당 10-15일이 소요되므로 설치 비용은 고정식 프로젝트보다 50-70% 더 비쌉니다. 현재 부유식 발전의 균등화 발전 비용은 1kW시당 0.20달러를 초과하고 있으며, DNV는 2050년까지 1메가와트시당 67달러로 서서히 하락할 뿐이라고 예측하고 있어, 단기적으로는 자금 조달의 어려움이 지속될 것으로 보입니다. 항만 개보수로 인해 비용은 더욱 늘어날 것입니다. 미국 서부 해안만 해도 대규모 조립 작업을 시작하기 전에 새로운 통합 부두와 크레인 설비에 최소 12억 달러가 필요합니다. 총 자본 비용이 1메가와트당 292만 달러 미만으로 떨어질 때까지, 대부분의 부유식 프로젝트는 일본, 스코틀랜드, 캘리포니아의 보조금 대상 시범 구역으로만 제한될 것입니다.

부문별 분석

2025년 기준으로 모노파일 부문은 풍력 터빈 기초 시장의 55.4%를 차지했으며, 수심 60m까지의 수역에서 높은 비용 효율성을 입증하고 있습니다. 그러나 수심 100m를 초과하는 해역에서의 부유식 풍력 발전 확대에 따라, 반잠수식 기초 시장은 연평균 성장률(CAGR) 27.8%를 나타낼 것으로 전망됩니다.

재킷식 기초는 아시아태평양에서 주목을 받고 있으며, 오르스테드(Orsted)의 ‘그레이터 창화’ 프로젝트에서는 공사 기간을 20% 단축하는 데 성공했습니다. 노르웨이에서는 이산화탄소 배출량을 80% 감축한다는 목표를 바탕으로 중력식 구조가 다시 주목받고 있습니다. 일본의 11.7기가와트 입찰과 스코틀랜드 BW Ideol사의 파이프라인에 힘입어, 부유식 기초의 가동 중인 용량은 234메가와트, 계획 중인 용량은 244기가와트에 달하고 있습니다. BW Ideol사의 ‘댐핑 풀’이나 Principle Power사의 ‘WindFloat’와 같은 혁신적인 기술은 효율성을 높이고 설치 시간을 최대 60% 단축함으로써 기초 기술 분야에서 큰 전환점을 보여주고 있습니다.

2025년 기준으로 풍력 터빈 기초 시장의 67.1%를 철강이 차지했으며, 이는 성숙한 공급망과 높은 강도 대 중량 비율을 반영한 것입니다. 그러나 2026년 3월 1쇼트톤당 1,115달러에 달했던 강판 가격의 급등과, 2027년까지 톤당 58-93달러의 추가 부담이 될 탄소국경조정세로 인해 개발 사업자들은 보다 친환경적인 자재 구성으로 전환하고 있습니다. 복합재 및 하이브리드 기초는 절대량으로는 적지만, 폐기 시 70%의 자재 회수를 의무화하는 EU의 순환형 경제 규정에 힘입어 2031년까지 연평균 성장률(CAGR) 14.4%를 나타낼 것으로 전망됩니다. BW Ideol사의 ‘Damping Pool’과 같은 하이브리드 철근 콘크리트 반잠수식 구조물은 매립량을 40% 줄이고, 사용 종료 시 해체 과정을 간소화합니다. REFRESH 시험을 통해, 신재와 동등한 특성을 지니며 2050년까지 발생할 것으로 예상되는 2,500만 톤의 블레이드 폐기물을 흡수할 수 있는 재활용 유리섬유 매트가 실증되었습니다.

콘크리트 중력식 기초가 다시 주목받고 있습니다. 모듈식 거푸집을 사용하면 내륙에서 콘크리트 타설이 가능해지며, 이후 바지선으로 예인하여 반출할 수 있으므로, XXL 모노파일의 물류에 지장을 주는 선저 깊이 제한을 피할 수 있기 때문입니다. Peikko사의 ‘Cage Rock’ 암반 고정 시스템은 플랫나하기(Flatnahagi)에서 콘크리트 사용량을 15%, 철근 사용량을 17% 줄여, 소규모 도서 지역의 송전망 경제성을 향상시켰습니다. 딜링거사가 2027년부터 2028년에 출시할 예정인 ‘PURE STEEL+’ 시리즈는 기존 강판에 비해 CO2 배출량을 55-60% 감축하는 것을 목표로 하고 있으며, 이는 기존 철강 제조업체들조차 저탄소 공급에 대응하고 있음을 보여줍니다. 탄소 가격 인상이 진행됨에 따라, 개발 사업자들은 초기 비용과 향후 회수 가능한 크레딧을 저울질하게 되며, 이에 따라 자금 조달 수단의 폭이 넓어지게 될 것입니다. 그 결과, 철강이 수량 면에서 우위를 유지하는 한편, 복합재와 하이브리드 솔루션이 풍력 터빈 기초 시장의 다음 성장 단계를 개척하게 될 것입니다.

지역별 분석

2025년, 유럽은 전 세계 풍력 터빈 기초 시장 점유율의 37.2%를 차지했습니다. 이는 북해에서의 건설 확대와 에스비알 및 브레머하펜의 항만 시설 확충에 힘입은 결과입니다. 에스비야르에서는 항로 수심을 12.8m로 깊게 하고, 복합 터미널을 확장함으로써 직경 10m를 초과하는 모노파일의 선적이 가능해졌습니다. 독일의 Gennaker 및 Windanker 프로젝트에는 총 80기 이상의 XXL 기초가 필요한 반면, 영국의 Dogger Bank 및 Hornsea 3 프로젝트에는 250기 이상이 필요한 것으로 알려져 있습니다. Sif Group의 Maasvlakte II 공장은 연간 200기의 모노파일을 생산하고 있으며, 이를 통해 유럽은 2030년까지 충분한 생산 여력을 확보하고 있습니다. 오스트에드(AustEd)사의 그레이터 창화(Greater Changhua) 현장에 도입된 흡입 버킷식 재킷은 현재 소음에 민감한 북해 해역에서의 도입이 검토되고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 13.6%를 기록하며 풍력 터빈 기초 시장 규모를 꾸준히 끌어올리고 있습니다. 중국에서는 이미 광둥성에서 23.5GW, 장쑤성에서 11.3GW가 가동 중이며, 모두 두께 120mm 이상의 플레이트가 필요한 15MW 이상의 대형 터빈으로 전환되고 있습니다. 대만은 2026년 1월, 그레이터 창화 2b 및 4 구역에서 66기의 흡입 버킷 재킷을 완공함으로써, 현지 조선소가 복잡한 격자 구조의 시공을 수행할 수 있음을 입증했습니다. 일본은 2025년까지 4개 구역에서 총 11.7GW의 발전 용량을 확정할 예정이며, 수심 100m를 초과하는 해역에서는 반잠수식 구조물에 기대를 걸고 있습니다. 한국의 GS 엔텍은 베트남과 필리핀으로의 수출 수주에 대응하기 위해 2026년 초까지 모노파일 생산 능력을 두 배로 늘릴 예정입니다.

북미는 설치 실적 면에서는 뒤처져 있지만, 미국 동부 해안을 따라 5.8GW에 달하는 탄탄한 파이프라인을 보유하고 있어, 이 지역은 풍력 터빈 기초 시장 점유율을 확대해 나가고 있습니다. 엠파이어 윈드와 코스트 버지니아 오프쇼어 윈드는 2025년을 목표로 총 230기의 XXL 모노파일을 설치했으나, 연방 정부의 공사 중단 명령으로 인해 건설이 일시 중단되면서 자금 조달 비용 스프레드가 확대되었습니다. 캘리포니아주의 4.6GW에 달하는 부유식 리스 프로젝트는 수요를 1MW당 약 397만 달러 규모의 반잠수식 플랫폼으로 전환시킬 것입니다. 캐나다는 2030년까지 5GW 규모의 해상 풍력 발전 설비 용량을 계획하고 있으며, 브라질과 모로코는 각각 1GW를 초과하는 환경 허가를 이미 취득했습니다. 이러한 신흥 파이프라인은 북미 및 일부 신흥 시장이 이미 확고히 자리 잡은 유럽 및 아시아 거점과의 격차를 꾸준히 좁혀가고 있음을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the wind turbine foundation market size was valued at USD 10.63 billion in 2025 and is estimated to grow from USD 11.69 billion in 2026 to reach USD 18.51 billion by 2031, at a CAGR of 9.63% during the forecast period (2026-2031).

This report is Segmented by Foundation Type (Gravity-Based Structure, Others), Material Type (Concrete, Steel, Composite/Hybrid), Installation Site (Onshore, Others), Turbine Rating (Below 2 MW, Others), End-Use Application (Utility-Scale, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wind Turbine Foundation Market Trends and Insights

Rapid Offshore Wind-Farm Build-Out Under Global Net-Zero Targets

Governments pursuing mid-century carbon neutrality auctioned roughly 100 GW of offshore wind capacity during 2025-2026 on top of the 83 GW already operating in 2024. Europe's REPowerEU blueprint alone eyes 300 GW by 2050, while the U.S. Inflation Reduction Act's clean-energy incentives lift project IRRs by up to three percentage points. China's 14th Five-Year Plan calls for 50 GW of offshore wind by 2030, fueling a domestic build programme that eclipses fabrication capacity. In response, lead times for XXL monopiles have stretched to 24 months, pushing developers to reserve slots through 2029. Fabricators with automated lines and deep-water quays, such as Sif Group, whose FY 2026 EBITDA guidance jumped 181% year on year, are securing premium pricing.

Turbine Ratings ≥15 MW Demanding XXL Foundations

Next-generation turbines generate thrust loads 40% above 10 MW models, forcing monopiles to 10 m diameters, 120 m lengths, and 2,400 t weights. Port depth is the chokepoint; only Esbjerg, Bremerhaven, Able Seaton, and Maasvlakte II currently handle >10 m monopiles. EEW and CS Wind delivered early Nordlicht 1 monopiles ahead of schedule, confirming that robotized welding keeps dimensional tolerances within 5 mm across 100 m lengths. The segment's competitive edge now rests on mills able to roll >120 mm plate and fabricators that integrate real-time QC. RWE's reservation of 320,000 t of plate through 2028 illustrates how large buyers are vacuuming up scarce capacity.

High CAPEX for Deep-Water Floating Solutions

Floating foundations cost about EUR 3.4 million per megawatt, of which platform fabrication and transport represent up to USD 1.4 million, and installation plus mooring add as much as EUR 4.5 million. Vessel charters range from USD 234,000 to USD 351,000 per day and can last 10-15 days per unit, so installation expenses run 50-70% above fixed-bottom projects. Current floating levelized energy prices exceed USD 0.20 per kilowatt-hour, and DNV foresees only a gradual fall to USD 67 per megawatt-hour by 2050, keeping bankability challenging in the near term. Port upgrades intensify the bill; the U.S. West Coast alone needs at least USD 1.2 billion for new integration quays and crane capacity before large-scale assembly can start. Until total capital costs drop below USD 2.92 million per megawatt, most floating projects will remain limited to subsidized pilot zones in Japan, Scotland, and California.

Other drivers and restraints analyzed in the detailed report include:

- Falling LCOE Boosting Developer ROI

- Mass-Produced Modular Concrete Bases Cutting Port Bottlenecks

- Limited Global Supply of Greater than 120 mm Steel Plate

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The monopile segment accounted for 55.4% of the wind turbine foundation market size in 2025, underscoring its cost efficiency in depths to 60 m. Semi-submersibles, however, are poised to register a 27.8% CAGR as floating wind scales in >100 m waters.

Jacket foundations are gaining traction in Asia-Pacific, with Orsted's Greater Changhua project achieving 20% faster schedules. Gravity-based structures are resurging in Norway, targeting an 80% carbon reduction. Floating foundations, driven by Japan's 11.7-gigawatt auction and Scotland's BW Ideol pipeline, represent 234 megawatts operationally, with a 244-gigawatt pipeline. Innovations like BW Ideol's Damping Pool and Principle Power's WindFloat enhance efficiency, reducing installation time by up to 60%, signaling a significant shift in foundation technologies.

Steel owned 67.1% of the wind turbine foundation market share in 2025, reflecting mature supply chains and high strength-to-weight performance. Yet escalating steel-plate prices that hit USD 1,115 per short ton in March 2026 and carbon-border levies that will add USD 58-93/t by 2027 are nudging developers toward greener mixes. Composite and hybrid foundations, though smaller in absolute volume, are forecast to grow at a 14.4% CAGR to 2031, driven by EU circular-economy rules that demand 70% material recovery at decommissioning. Hybrid steel-concrete semi-submersibles such as BW Ideol's Damping Pool offer 40% lower embodied emissions and simplified end-of-life dismantling. REFRESH trials showed recycled glass-fiber mats that match virgin properties and create a sink for the 25 Mt blade waste expected by 2050.

Concrete gravity bases are gaining a fresh lease because modular molds allow inland casting followed by barge tow-out, which bypasses draft limits that hamper XXL monopile logistics. Peikko's Cage Rock rock-anchored system cut concrete volume 15% and reinforcement 17% at Flatnahagi, improving economics for small island grids. Dillinger's PURE STEEL+ line, launching 2027-2028, targets 55-60% CO2 reduction relative to conventional plate, signaling that even incumbent steel players are hedging with low-carbon supply. As carbon pricing tightens, developers will weigh upfront cost against future salvage credits, leading to a broader procurement palette. Consequently, while steel keeps its numeric lead, composite and hybrid solutions will carve the next leg of growth in the wind turbine foundation market.

Geography Analysis

Europe commanded 37.2% of the global wind turbine foundation market share in 2025, underpinned by the North Sea build-out and upgraded ports in Esbjerg and Bremerhaven. Esbjerg deepened its fairway to 12.8 m and expanded the Combi-Terminal, enabling load-out of monopiles larger than 10 m in diameter. Germany's Gennaker and Windanker projects together need more than 80 XXL foundations, while the United Kingdom's Dogger Bank and Hornsea 3 require over 250 units. Sif Group's Maasvlakte II plant produces 200 monopiles a year, giving Europe ample fabrication headroom through 2030. Suction-bucket jackets deployed at Orsted's Greater Changhua site are now being evaluated for noise-sensitive North Sea zones.

Asia-Pacific is the fastest-growing region, advancing at a 13.6% CAGR to 2031 and steadily lifting the wind turbine foundation market size. China already operates 23.5 GW in Guangdong and 11.3 GW in Jiangsu, both shifting to 15 MW and larger turbines that need plates thicker than 120 mm. Taiwan completed 66 suction-bucket jackets at Greater Changhua 2b & 4 in January 2026, proving that local yards can handle complex lattice work. Japan awarded 11.7 GW of capacity across four zones in 2025 and is counting on semi-submersibles for depths beyond 100 m. South Korea's GS Entec is doubling monopile capacity by early 2026 to serve export orders to Vietnam and the Philippines.

North America trails in installations yet holds a robust 5.8 GW pipeline along the U.S. East Coast, giving the region a growing share of the wind turbine foundation market size. Empire Wind and Coastal Virginia Offshore Wind together installed 230 XXL monopiles in 2025, but federal stop-work orders briefly halted construction and raised financing spreads. California's 4.6 GW of floating leases will pivot demand toward semi-submersible platforms that cost about USD 3.97 million per megawatt. Canada plans 5 GW of offshore capacity by 2030, while Brazil and Morocco have each cleared over 1 GW in environmental permits. These emerging pipelines suggest that North America and selected frontier markets will steadily close the gap with established European and Asian hubs.

- Ramboll Group A/S

- Sif Group

- Bladt Industries A/S

- EEW Group

- BW Ideol

- Principle Power, Inc.

- DEME Offshore

- Boskalis

- Navantia-Windar

- Harland & Wolff

- Peikko Group

- Balltec Ltd.

- BFG International

- Steelwind Nordenham GmbH

- Seaway 7

- Van Oord

- Jan De Nul

- Lamprell

- Smulders

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid offshore wind-farm build-out under global net-zero targets

- 4.2.2 Turbine ratings Above 15 MW demanding XXL foundations

- 4.2.3 Falling LCOE boosting developer ROI

- 4.2.4 Mass-produced modular concrete bases cutting port bottlenecks

- 4.2.5 Digital-twin geotechnical modelling accelerating custom design

- 4.2.6 Demand for recyclable foundation materials

- 4.3 Market Restraints

- 4.3.1 High CAPEX for deep-water floating solutions

- 4.3.2 Limited global supply of greater than 120 mm steel plate

- 4.3.3 Shallow-draft ports delaying XXL monopile logistics

- 4.3.4 Unclear salvage liability inflating finance costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Foundation Type

- 5.1.1 Gravity-Based Structure

- 5.1.2 Monopile

- 5.1.3 Jacket

- 5.1.4 Tripod

- 5.1.5 Semi-submersible

- 5.1.6 Others

- 5.2 By Material Type

- 5.2.1 Concrete

- 5.2.2 Steel

- 5.2.3 Composite/Hybrid

- 5.3 By Installation Site

- 5.3.1 Onshore

- 5.3.2 Offshore

- 5.3.2.1 Fixed-Bottom Offshore

- 5.3.2.2 Floating Offshore

- 5.4 By Turbine Rating (Capacity)

- 5.4.1 Below 2 MW

- 5.4.2 2 to 5 MW

- 5.4.3 Above 5 MW

- 5.5 By End-Use Application

- 5.5.1 Utility-Scale

- 5.5.2 Commercial and Industrial

- 5.5.3 Residential and Micro-grid

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Russia

- 5.6.2.6 Finland

- 5.6.2.7 Sweden

- 5.6.2.8 Tukey

- 5.6.2.9 Netherlands

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Vietnam

- 5.6.3.7 Rest of Asia Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Egypt

- 5.6.5.4 Morocco

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Ramboll Group A/S

- 6.4.2 Sif Group

- 6.4.3 Bladt Industries A/S

- 6.4.4 EEW Group

- 6.4.5 BW Ideol

- 6.4.6 Principle Power, Inc.

- 6.4.7 DEME Offshore

- 6.4.8 Boskalis

- 6.4.9 Navantia-Windar

- 6.4.10 Harland & Wolff

- 6.4.11 Peikko Group

- 6.4.12 Balltec Ltd.

- 6.4.13 BFG International

- 6.4.14 Steelwind Nordenham GmbH

- 6.4.15 Seaway 7

- 6.4.16 Van Oord

- 6.4.17 Jan De Nul

- 6.4.18 Lamprell

- 6.4.19 Smulders

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment