|

시장보고서

상품코드

2063267

인도의 자동차용 조명 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Automotive Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

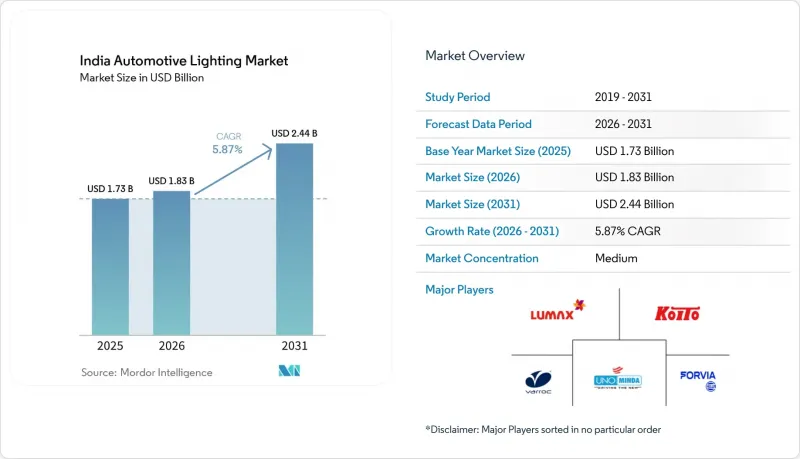

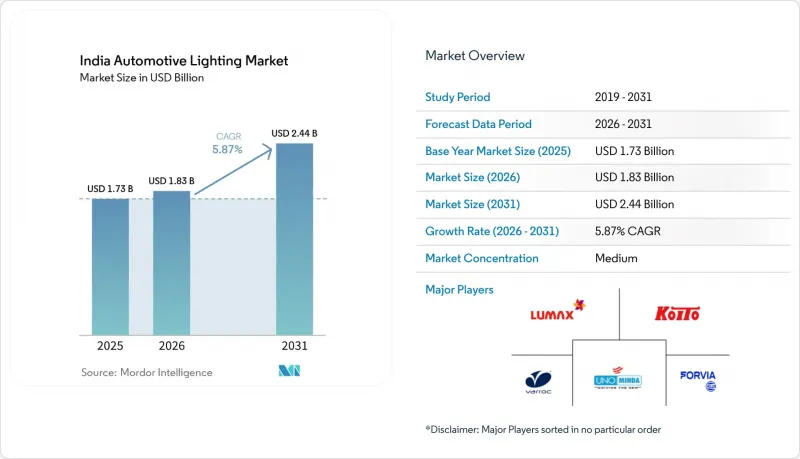

Mordor Intelligence에 의하면, 인도의 자동차용 조명 시장 규모는 2025년에 17억 3,000만 달러로 평가되었고, 2026년 18억 3,000만 달러로 추정되고, 2031년까지 24억 4,000만 달러에 이를 것으로 예상되고 있으며, 2026-2031년 CAGR 5.87%로 성장할 전망입니다.

본 보고서는 차종별(승용차, 소형 상용차, 중형 및 대형 상용차, 이륜차), 용도별(외장 및 내장), 기술별(할로겐, 크세논/HID, LED, 레이저, OLED), 판매 채널별(OEM 및 애프터마켓)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(대수)으로 제시되어 있습니다.

인도의 자동차 조명 시장 동향 및 인사이트

LED 가격 하락과 에너지 효율 규제

부품 비용의 하락과 에너지 효율국(BEE)의 기준치가 맞물리면서, LED는 모든 가격대에서 기본 사양으로 자리 잡았습니다. 현재 OEM 계약에서는 열적 손실 없이 칸델라 요건을 충족하기 위해, 보급형 스쿠터라도 LED가 지정되어 있습니다. PLI 제도의 틀 안에서 자동 표면 실장 라인에 투자한 국내 공급업체들은 이러한 변화를 포착하고 있는 반면, 할로겐 수요는 기존의 교체용 채널로 후퇴하고 있습니다. 선순환적인 비용-물량 사이클에 힘입어 LED 모듈의 가격은 할로겐 어셈블리와 동등한 수준으로 낮아지고 있으며, 이로 인해 할로겐 어셈블리의 도태가 불가피해지고 있습니다.

AIS-008/AIS-012 안전 규정 시행

2025년, 전조등 및 신호 장치의 형식 인증 심사가 더욱 엄격해졌습니다. 사내에 광도 측정 터널을 보유한 1차 공급업체는 기준을 쉽게 충족하고 있지만, 그레이 마켓의 조립 업체들은 제품 인증 획득에 어려움을 겪고 있습니다. 이미 법 집행 조치를 통해 도시 지역의 소매점에서 규격에 맞지 않는 여러 유형의 애프터마켓용 램프가 철수되었습니다. 앞으로 지속적인 감시를 통해 인증되지 않은 전구가 시장에서 퇴출됨에 따라, 인도 도로의 루멘 안정성과 색상 일관성이 향상될 것으로 예측됩니다.

고급 조명 모듈에 부과되는 높은 GST 세율과 수입 관세

레이저 및 매트릭스 LED 어셈블리의 완제품 수입에 대해 총 40%가 넘는 관세가 부과됨에 따라, 양산차 부문에서 이를 광범위하게 도입하려는 OEM 업체들의 의욕이 꺾이고 있습니다. 장거리 레이저 하이빔을 제공하기 위한 추가 비용을 부담하는 것은 고급 브랜드뿐이지만, 현지 합작 기업들은 부품 조립의 현지화를 서두르고 있습니다. 그들의 목표는 관세로 인한 비용 상승 부담 없이 프리미엄 기능을 더 합리적인 가격에 제공하는 것입니다.

부문별 분석

2025년, 인도 자동차 조명 시장에서 승용차가 48.41%라는 최대 점유율을 차지했으며, 해치백과 세단에 LED가 광범위하게 채택되고 있음을 반영하고 있습니다. 반면, 이륜차는 연평균 성장률(CAGR) 6.01%로 가장 빠르게 성장할 것으로 전망됩니다. 이는 신형 스쿠터나 오토바이에 자동 헤드라이트 점등 기능이 탑재되면서, 신뢰성이 높은 솔리드 스테이트 램프가 필수품이 되었기 때문입니다. 부문별 규제로 인해 조명 장비가 확대되고 있으며, 오토바이는 판매량 증가의 주요 동력이 되고 있습니다.

이러한 규제 측면의 호재에 힘입어, 공급업체들은 인도의 몬순 시즌 방수 기준도 충족하는 이륜차용 소형 LED 모듈의 맞춤형 개발을 추진하고 있습니다. 모듈식 램프 하우징 덕분에 각 브랜드는 매년 디자인을 새롭게 바꿀 수 있게 되었으며, 이에 따라 OEM의 설계 주기가 단축되었습니다. 승용차가 여전히 금액 기준으로는 시장을 독점하고 있는 반면, 스쿠터의 전기화가 가속화됨에 따라 이륜차는 장기적인 성장 스토리에 확고한 위치를 차지하고 있으며, 단위당 수익성을 훼손하지 않으면서 시장 부문 구성의 균형을 유지하고 있습니다.

2025년, 인도의 자동차 조명 시장에서 외장 기능이 63.21%를 차지했습니다. 이러한 우월성은 주간 주행등, 어댑티브 프론트 라이팅, 그리고 브랜드를 상징하는 특징적인 디자인으로도 기능하는 전폭 테일바를 통해 확고히 자리 잡고 있습니다. OEM 디자이너들은 헤드램프를 '눈'으로 간주하며, 엄격한 빔 컷오프 규정을 충족하면서도 조각 같은 프론트 페이스에 자연스럽게 통합해야 합니다. 이러한 두 가지 요건으로 인해, 설계 선택이 이루어질 때 파사드 시스템은 예산 배분의 최우선 순위가 되며, 기존 모델을 계승한 모델이라 하더라도 단계적인 업그레이드가 확실히 이루어집니다. 외부 조명 시장의 연평균 성장률(CAGR) 6.11% 전망치는 해질녘이나 몬순철의 폭우 시 가시성을 높여주는 연속 조명 기능을 갖춘 더 넓은 라이트바의 계획적인 도입도 반영하고 있습니다.

인테리어 조명은 규모는 작지만, 커넥티드카나 전기차의 실내 공간에서 현재 촉각적인 차별화 요소로 작용하고 있습니다. 멀티존 RGB 스트립을 통해 운전자는 무드 조명을 인포테인먼트 테마와 동기화하여, 실내 분위기를 소프트웨어를 통해 정의된 경험으로 바꿀 수 있습니다. 이에 대응하여 각 벤더사는 디퓨저와 CAN 버스 컨트롤러를 하나의 슬림한 케이스에 통합한 플러그 앤 플레이 방식의 LED 레일을 출시함으로써, 이를 통해 라인 조립 시간을 단축하고 있습니다. 외장 시스템이 여전히 전체 가치의 대부분을 차지하고 있지만, 실내 맞춤화 옵션이 확대됨에 따라 고급 트림의 보급률 상승과 발맞추어 내장 주문도 꾸준히 증가하고 있습니다. 각 공급업체들은 단일 LIN 버스 게이트웨이로 헤드램프의 밝기 조절과 풋웰의 분위기 조명을 모두 제어할 수 있기 때문에 이 두 가지 흐름을 경쟁 관계가 아닌 상호 보완적인 것으로 보고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the indian automotive lighting market size was valued at USD 1.73 billion in 2025 and is expected to increase from USD 1.83 billion in 2026 to reach USD 2.44 billion by 2031, growing at a CAGR of 5.87% over 2026-2031.

This report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium & Heavy Commercial Vehicles, and Two-Wheelers), Application (Exterior and Interior), Technology (Halogen, Xenon/HID, LED, Laser, and OLED), and Sales Channel (OEM and Aftermarket). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

India Automotive Lighting Market Trends and Insights

LED Price Erosion and Energy-Efficiency Mandates

Declining component costs coupled with Bureau of Energy Efficiency thresholds have made LEDs the default fitment across price bands. OEM contracts now specify LEDs even for entry-level scooters to meet candela requirements without thermal penalties. Domestic suppliers that invested in automated surface-mount lines under the PLI scheme are capturing this shift, while halogen demand retreats to legacy replacement channels. The virtuous cost-volume cycle is compressing LED module prices toward parity with halogen assemblies, sealing the latter's obsolescence.

AIS-008 / AIS-012 Safety Regulations Enforcement

Type-approval audits for headlamps and signaling devices became more stringent in 2025. Tier-one suppliers with in-house photometric tunnels readily comply, whereas gray-market assemblers struggle to certify their products. Enforcement actions have already removed several non-conforming aftermarket lamps from urban retail shelves. Over time, sustained surveillance is expected to marginalize uncertified bulbs, improving lumen stability and color consistency on Indian roads.

High GST Slab and Import Duty on Advanced Lighting Modules

Combined levies exceeding 40% on imported complete units of laser and matrix-LED assemblies are dampening OEM enthusiasm for widespread adoption in the mass segment. While only luxury brands are shouldering the extra costs to provide long-range laser high beams, local joint ventures are hurrying to localize sub-assemblies. Their goal is to make premium features more affordable without the burden of duty inflation.

Other drivers and restraints analyzed in the detailed report include:

- Electrification Push Under FAME-LI Boosting 2-W and 4-W LED Fitment

- Tier-1 Localisation Incentives (PLI-Auto and Specs)

- LED-Driver Semiconductor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars constituted the largest 48.41% share of the Indian automotive lighting market in 2025, reflecting broad LED adoption across hatchbacks and sedans. In contrast, two-wheelers will grow the fastest, at a 6.01% CAGR, as newer scooters and motorcycles now feature automatic headlamp-on functions that mandate reliable solid-state lamps. Segment-specific regulations continue to elevate lighting content, making motorcycles a critical volume driver.

The regulatory tailwind encourages suppliers to customize compact LED modules for motorcycles that also meet splash-resistance norms for Indian monsoons. OEM design cycles have therefore shortened, as modular lamp housings allow brands to refresh aesthetics annually. While passenger cars continue to dominate value terms, accelerating scooter electrification firmly embeds two-wheelers in long-term growth narratives, balancing the market's segment mix without diluting unit profitability.

Exterior functions captured 63.21% of the Indian automotive lighting market in 2025, a lead cemented by daytime running lamps, adaptive front-lighting, and full-width tail bars that double as unmistakable brand signatures. OEM designers treat headlamps as "eyes" that must meet strict beam cutoff regulations while still packaging seamlessly into sculpted fascias. That dual imperative keeps exterior systems at the top of budget lists when engineering choices are made, ensuring incremental upgrades even in carry-over models. The 6.11% CAGR projected for exterior lamps also reflects planned rollouts of wider light bars whose continuous illumination improves conspicuity at dusk and during monsoon downpours.

Interior illumination, although smaller, now serves as a tactile differentiator in connected vehicles and electric cab-ins. Multi-zone RGB strips enable drivers to sync mood lighting with infotainment themes, turning the cabin ambiance into a software-defined experience. Vendors respond by shipping plug-and-play LED rails that integrate diffusers and CAN bus controllers into a single, slim form factor, reducing line assembly time. While exterior systems still dominate total value, expanding cabin-personalization menus ensure that interior orders rise in lockstep with higher trim penetrations. Suppliers see the two streams as complementary rather than competitive, since a single LIN-bus gateway can orchestrate both headlamp leveling and foot-well ambiance.

List of Companies Covered in this Report:

- Koito Manufacturing Co. Ltd.

- Lumax Industries Limited

- Varroc Group

- HELLA GmbH & Co. KGaA

- UNO Minda Ltd.

- Valeo Lighting Systems India

- Marelli Automotive Lighting India

- Hyundai Mobis Co. Ltd.

- Osram India

- Philips Automotive Lighting India

- SL Corporation

- Motherson Sumi Systems (Samvardhana)

- J.W. Speaker

- Magneti Marelli Parts & Services India

- Bosch Limited - Lighting ECUs

- Texas Instruments India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED-Price Erosion & Energy-Efficiency Mandates

- 4.2.2 AIS-008 / AIS-012 Safety Regulations Enforcement

- 4.2.3 Electrification Push Under Fame-LI Boosting 2-W & 4-W Led Fitment

- 4.2.4 Tier-1 Localization Incentives (PLI-Auto & Specs)

- 4.2.5 ADAS-Ready Adaptive Lighting Demand From Premium Oems

- 4.2.6 Smart-Corridor Pilots Enabling V2I-Linked Lighting

- 4.3 Market Restraints

- 4.3.1 High GST Slab & Import Duty On Advanced Lighting Modules

- 4.3.2 Prevalence Of Counterfeit Aftermarket Bulbs

- 4.3.3 LED-Driver Semiconductor Shortages

- 4.3.4 Low Consumer Awareness In Tier-2/3 Cities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium & Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.2 By Application

- 5.2.1 Exterior

- 5.2.1.1 Headlamps

- 5.2.1.2 Taillights

- 5.2.1.3 Daytime Running Lights (DRLs)

- 5.2.1.4 Fog Lamps

- 5.2.2 Interior

- 5.2.2.1 Ambient / Footwell

- 5.2.2.2 Roof / Dome

- 5.2.1 Exterior

- 5.3 By Technology

- 5.3.1 Halogen

- 5.3.2 Xenon / HID

- 5.3.3 LED

- 5.3.4 Laser

- 5.3.5 OLED

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Koito Manufacturing Co. Ltd.

- 6.4.2 Lumax Industries Limited

- 6.4.3 Varroc Group

- 6.4.4 HELLA GmbH & Co. KGaA

- 6.4.5 UNO Minda Ltd.

- 6.4.6 Valeo Lighting Systems India

- 6.4.7 Marelli Automotive Lighting India

- 6.4.8 Hyundai Mobis Co. Ltd.

- 6.4.9 Osram India

- 6.4.10 Philips Automotive Lighting India

- 6.4.11 SL Corporation

- 6.4.12 Motherson Sumi Systems (Samvardhana)

- 6.4.13 J.W. Speaker

- 6.4.14 Magneti Marelli Parts & Services India

- 6.4.15 Bosch Limited - Lighting ECUs

- 6.4.16 Texas Instruments India

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment