|

시장보고서

상품코드

2063275

자동차 글레이징 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Glazing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

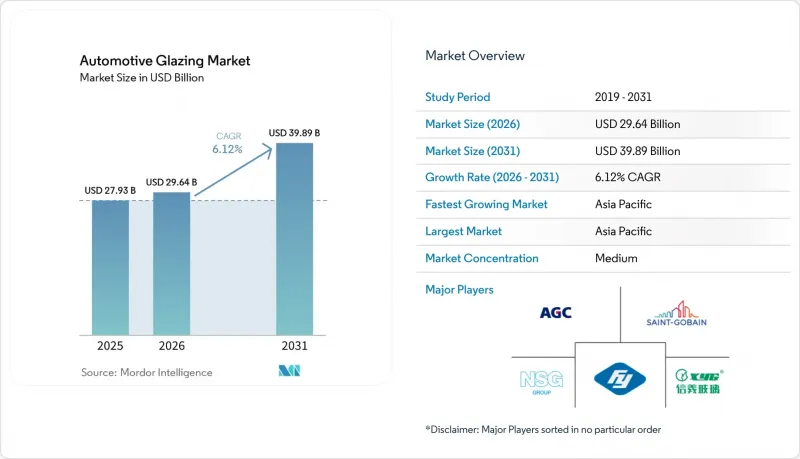

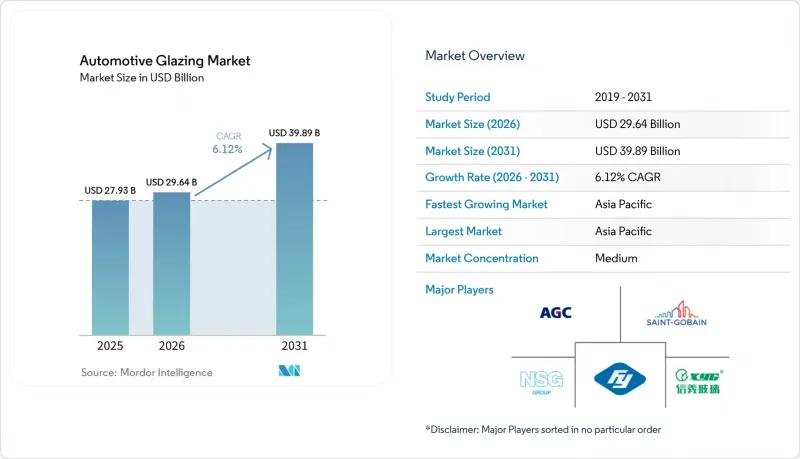

Mordor Intelligence에 의하면, 자동차 글레이징 시장 규모는 2025년 279억 3,000만 달러로 평가되었습니다. 2026년 296억 4,000만 달러로 확대되어 2031년까지 398억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 6.12%를 나타낼 전망입니다.

본 보고서는 제품 유형(복합 유리, 강화 유리 등), 용도 유형(전면 유리, 후면 유리 등), 차종(승용차, 소형 상용차 등), 구동 방식(내연기관(ICE) 등), 유통 채널 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자동차 글레이징 시장 동향 및 인사이트

신흥국에서의 자동차 생산 증가

인도 및 아세안 회랑 지역의 공장 생산량이 확대됨에 따라, 유리 공급망은 현지화된 플로트 라인으로 전환되고 있습니다. 푸야오(Fuyao)의 2개 공장 체제 구상, 즉 중국을 규모 확대의 원동력으로 삼고 헝가리를 유럽의 적시생산(JIT) 프로그램 거점으로 삼는 전략은 새로운 조립 거점에서 퍼스트핏(First Fit) 계약을 확보하는 데 필요한 대응 능력을 보여주고 있습니다. 자외선 차단 코팅이나 저방사율(Low-E) 코팅 등, 과거에는 고급차 전용으로 여겨졌던 기술들이 현지 1차 공급업체들의 생산 능력이 확대됨에 따라 양산 모델에도 도입되고 있습니다.

경량 유리가 전기차의 주행 거리와 연비 효율을 향상시킵니다.

전기차(EV) 플랫폼의 경우, 경량화를 통해 1Kg을 줄이면 주행 거리 연장으로 바로 이어집니다. 폴리카보네이트는 유리보다 무게가 약 절반 정도이며, 열전도율도 낮기 때문에 배터리용량을 소모시키는 공조(HVAC) 부하를 줄여줍니다. AGC와 생고뱅은 전방 충돌 안전 기준을 충족하면서도 경량화를 실현하는 하이브리드 적층 유리를 검증하고 있으며, 중국의 제조업체들은 BEV의 측면 창문에 얇은 중간막을 채택함으로써 경량화를 한층 더 추진하고 있습니다. 배터리 팩의 크기를 늘리지 않으면서도 경량화가 요구되는 엄격한 차량 함대 평균 CO₂ 배출 기준이 적용되는 지역에서는 전 세계 자동차 제조업체들의 도입이 가속화되고 있습니다.

첨단 유리 제품의 높은 원가와 복잡한 제조 공정

태양광 발전층, 일렉트로크로믹 층 또는 HUD용 중간막을 통합하려면 공급업체는 자본 집약적인 소성로 업그레이드, 더욱 엄격한 클린룸 관리, 그리고 새로운 인라인 검사 공정에 대한 투자를 감수해야 합니다. 층이 추가될 때마다 수율 위험이 커집니다. 왜냐하면, 시트 한 장에 결함이 있으면 라미네이트 전체가 불량품이 되기 때문에 규모의 경제가 실현되기 전에 학습 곡선에 따른 불량품 발생이 이익률을 압박할 우려가 있기 때문입니다. 이러한 비용 부담은 가격 탄력성이 낮고, OEM 업체가 원자재비 상승분을 소비자에게 전가하기 어려운 대량 생산 주요 브랜드에서 가장 심각하게 느껴집니다. 세계 안전 기준에 따라 의무화된 충격 시험이나 자외선 노화 시험 등의 인증 시험은 개발 주기를 더욱 길게 만들고, 운영 자금을 묶어두게 됩니다.

부문별 분석

2025년, 접합유리는 자동차 글레이징 시장에서 62.35%의 점유율을 유지하며, 전 세계 충격 흡수 기준을 충족함을 입증했습니다. 폴리카보네이트는 가장 빠르게 부상하고 있는 대체 소재로, 자동차 제조업체들이 사이드 윈도우와 루프 모듈에 이 소재의 경량성을 활용함에 따라 연평균 성장률(CAGR) 7.13%로 시장이 확대될 것으로 전망됩니다. 각 공급업체들은 접합 유리로 만든 전면 유리와 폴리카보네이트 재질의 사이드라이트를 결합한 하이브리드 구조를 모색하고 있으며, 이를 통해 플랫폼은 중량 목표를 희생하지 않고도 안전 기준을 충족할 수 있게 됩니다. 내스크래치성 및 장기적인 투명성과 관련된 기술적 과제는 여전히 남아 있지만, 코팅 기술이 지속적으로 발전하고 있는 만큼, 규제 당국이 결국 전면 유리 규제를 완화하여 수요가 더욱 확대될 가능성이 있습니다.

차세대 전기차 아키텍처의 설계가 확정됨에 따라, 조기에 다중 소재 솔루션 인증을 획득한 기업이 사양 채택에서 우위를 점하게 될 것입니다. 지속적인 연구 개발을 통해 얇은 적층 시트와 폴리머 코어를 결합함으로써 카테고리 간의 경계가 모호해지며, 기존 제조업체는 경량화 기준을 충족하면서도 기존의 생산 설비를 유지할 수 있게 됩니다. OEM 각사는 적층 구조의 음향 성능과 적외선 차단 효과를 중시하고 있기 때문에 단기적으로는 전면적인 전환이 이루어지지는 않을 것입니다. 대신, 비용, 중량, 규제 허용 범위를 최적화하기 위해 각 기판을 특정 차량 구역에 할당하는 공존 모델이 등장하고 있습니다.

전면 유리는 적층 구조의 법적 의무화와 부품 표면적의 넓음을 배경으로, 2025년 자동차 글레이징 시장 규모의 47.22%를 차지했습니다. 한편, 선루프는 파노라마 레이아웃이 프리미엄 브랜드에서 소형 크로스오버로 전환됨에 따라 연평균 성장률(CAGR) 7.96%를 기록하며 성장을 주도하고 있습니다. 디자이너는 개방감 있는 실내 공간을 조성하기 위해 루프 전체의 투명성을 중시하고 있으며, 공급업체는 현재 외장 판금 구조를 변경하지 않으면서도 기능적 가치를 더하기 위해 조광 기능이 있는 필름과 태양광 발전 필름을 통합하고 있습니다. 루프 유리는 플랫폼 재설계를 최소화하면서도 높은 고급스러움을 제공하기 때문에 이러한 업그레이드 방향은 OEM의 수익 전략과 부합합니다.

앞유리는 HUD 프로젝터와 증강현실(AR) 오버레이를 지원하는 쐐기형 중간막 덕분에, 수동적인 장벽에서 디지털 디스플레이로 동시에 진화하고 있습니다. 이러한 광학 시스템에는 매우 높은 표면 평탄도와 엄격한 굴절률 허용 오차가 요구되므로, 유리 제조업체가 준수해야 할 사양 범위는 점점 좁아지고 있습니다. 측면 유리나 후면 유리는 기능 도입 면에서 뒤처져 있지만, 전면 유리에서 검증된 코팅 기술을 점차 적용해 나가면서 트리클다운 수요를 창출하고 있습니다. 다양한 용도에 걸친 전환 속도는 공급업체가 다양한 곡률 및 두께 요건에 맞추어 새로운 적층 구조를 얼마나 신속하게 표준화할 수 있는지에 달려 있습니다.

지역별 분석

아시아태평양은 2025년에 자동차 글레이징 시장의 45.81% 점유율을 유지했으며, 7.31%라는 가장 높은 연평균 성장률(CAGR)을 나타냈습니다. 이러한 성장은 주로 중국 내 배터리 전기자동차(BEV)의 급증, 인도의 생산 확대, 그리고 일본 및 한국과의 기술 교류를 통해 주도되고 있습니다. 현지 공급업체들은 플로트 유리 생산 능력을 확대하고 있는 반면, 각국 정부는 특히 에너지 효율이 높은 용해로 및 재활용 의무화 등의 인센티브를 통해 투자를 유치하고 있습니다.

유럽과 북미는 생산량 면에서는 뒤처져 있지만, 자동차 부품으로서의 부가가치 면에서는 뛰어납니다. 유럽에서는 소음 및 사용 후 유리 재활용에 중점을 둔 지침이 OEM 사양을 결정하고 있습니다. 이러한 중시 덕분에 저소음 및 분해가 용이한 유리 등의 특성이 조달 과정에서 필수적인 요소가 되었습니다. 한편, 북미에서는 미국 중서부에 위치한 플로트 유리 생산 라인부터 멕시코의 조립 거점에 이르는 지역적 공급망을 활용함으로써, 환율 변동이나 운송 비용으로 인한 문제를 효과적으로 완화하고 있습니다.

남미, 중동 및 아프리카는 현재 자동차 글레이징 시장에서 비교적 작은 비중을 차지하고 있지만, 분명한 잠재력을 가지고 있습니다. 예를 들어, 걸프 연안 국가들의 프리미엄 SUV 수요 증가나 브라질에서 BEV(배터리 전기차) 도입을 위한 실험적인 노력은 이러한 성장 가능성을 시사하고 있습니다. 그러나 이러한 잠재력을 실현할 수 있을지는 경제의 안정성, 노동력의 기술 수준, 그리고 현지 플로트라인 생산에 대한 인센티브와 관련된 수입 관세에 대한 명확한 정책 등의 요인에 좌우될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the automotive glazing market size is expected to increase from USD 27.93 billion in 2025 to USD 29.64 billion in 2026 and reach USD 39.89 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

This report is Segmented by Product Type (Laminated Glass, Tempered Glass, and More), Application Type (Front Windshield, Rear Windshield, and More), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and More ), Propulsion Type (Internal Combustion Engine (ICE) and More), Distribution Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Glazing Market Trends and Insights

Rising Vehicle Production in Emerging Economies

Factory output in India and the ASEAN corridor is expanding, pulling glazing supply chains toward localized float lines. Fuyao's dual-plant blueprint, China as a scale engine, and Hungary for European just-in-time programs illustrate the responsiveness needed to win first-fit contracts in new assembly hubs. Technology once reserved for premium trims, such as UV-cut coatings and low-emissivity layers, is entering volume models as local tier-ones ramp capacity.

Lightweight Glazing Boosts EV Range and Fuel Efficiency

Electric-vehicle platforms treat every kilogram saved as extended driving range. Polycarbonate weighs roughly half as much as glass and shows lower thermal conductivity, easing HVAC demand that drains battery capacity. AGC and Saint-Gobain validated hybrid laminates that meet frontal-impact rules while trimming mass, and Chinese producers deploy thinner interlayers on BEV side windows to compound savings. Global OEM adoption quickens wherever stringent fleet-average CO2 standards compel weight reduction without increasing battery pack size.

High Cost and Process Complexity of Advanced Glazing

Embedding photovoltaic layers, electrochromic stacks, or HUD interlayers forces suppliers to invest in capital-intensive furnace upgrades, tighter clean-room controls, and new inline inspection steps. Each additional layer multiplies yield risk because an imperfection in any sheet can condemn the entire laminate, so learning-curve scrap can erode profit margins before scale efficiencies arrive. The expense is felt most acutely in high-volume nameplates, where price elasticity is low, making it harder for OEMs to pass on material premiums to consumers. Certification testing, such as impact and UV-aging trials required under global safety codes, further lengthens development cycles and ties up working capital.

Other drivers and restraints analyzed in the detailed report include:

- Surging Adoption of Panoramic Sunroofs

- OEM Push for HUD-Ready "Display" Glass

- Soda-Ash Supply Shocks Inflating Glass Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laminated glass maintained 62.35% of the automotive glazing market share in 2025, underlining its compliance with global impact-retention rules. Polycarbonate is the fastest-rising alternative, projected to expand at a 7.13% CAGR as automakers leverage its weight advantage for side windows and roof modules. Suppliers explore hybrid assemblies that pair laminated windshields with polycarbonate sidelites, enabling platforms to meet safety codes without sacrificing mass targets. Technical hurdles remain around scratch resistance and long-term clarity, yet ongoing coating advances suggest regulatory bodies could eventually relax front-glazing restrictions, opening additional volume.

Firms able to qualify multi-material solutions early will capture specification wins as next-generation electric architectures freeze designs. Continued R&D blurs categorical lines by marrying thin laminated sheets with polymer cores, helping incumbents defend their installed furnace base while meeting lightweight benchmarks. OEMs value the acoustics and infrared attenuation of laminated constructions, so a wholesale switch is unlikely in the near term. Instead, a coexistence model emerges in which each substrate is matched to specific vehicle zones to optimize cost, mass, and regulatory headroom.

Front windshields held 47.22% share of the automotive glazing market size in 2025, anchored by legal mandates for laminated construction and the sheer surface area of the part. Sunroofs, however, lead growth with a 7.96% CAGR as panoramic layouts migrate from premium badges into compact crossovers. Designers champion full-roof transparency to create an airy cabin feel, and suppliers now integrate dimmable or photovoltaic films to add functional value without altering exterior sheet metal. The upgrade path aligns with OEM revenue strategies because roof glass offers high perceived luxury while requiring minimal platform re-engineering.

Windshields are simultaneously evolving from passive barriers into digital displays, thanks to wedge interlayers that support HUD projectors and augmented-reality overlays. These optics demand pristine surface flatness and strict refractive-index tolerances, tightening specification windows for glass makers. Side and rear lights lag in feature adoption but gradually inherit coatings first proven on windshields, creating trickle-down demand. The pace of cross-application migration will hinge on how quickly suppliers standardize new stacks across varied curvature and thickness requirements.

Geography Analysis

Asia-Pacific retained 45.81% of the automotive glazing market share in 2025 and shows the quickest 7.31% CAGR outlook. This growth is largely driven by a surge in Battery Electric Vehicles (BEVs) in China, increasing production in India, and a technological exchange from Japan and South Korea. Local suppliers are expanding their float-glass capacities, while governments are enticing investment through incentives, notably energy-efficient furnaces and recycling mandates.

While Europe and North America lag in volume, they excel in the value derived from vehicle content. In Europe, directives focused on acoustic emissions and end-of-life recycling are shaping Original Equipment Manufacturer (OEM) specifications. This emphasis has made features such as low-noise, easily dismantled glass essential in procurement. Meanwhile, North America is capitalizing on its regional supply chains, which span from float lines in the United States Midwest to assembly corridors in Mexico, effectively mitigating the challenges posed by currency fluctuations and freight costs.

Though South America, the Middle East, and Africa currently represent smaller segments of the automotive glazing market, there's evident potential. For instance, the rising demand for premium SUVs in Gulf states and experimental BEV initiatives in Brazil hint at this upside. However, realizing this potential will depend on factors such as economic stability, the skill level of the workforce, and clear policies on import duties in relation to incentives for local float-line production.

- AGC Inc.

- Saint-Gobain S.A.

- Nippon Sheet Glass Co., Ltd.

- Fuyao Glass Industry Group Co., Ltd.

- Xinyi Glass Holdings Ltd.

- Guardian Industries

- Vitro SAB de CV

- Central Glass Co., Ltd.

- Teijin Limited

- Webasto SE

- Magna International Inc.

- Gentex Corporation

- AGP eGlass

- Corning Incorporated

- Sisecam

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Vehicle Production in Emerging Economies

- 4.2.2 Lightweight Glazing Boosts EV Range and Fuel Efficiency

- 4.2.3 Surging Adoption of Panoramic Sunroofs

- 4.2.4 OEM Push for HUD-Ready "Display" Glass

- 4.2.5 Mandatory Urban-Noise Rules Driving Acoustic Glazing

- 4.2.6 Photovoltaic Glazing to Harvest Solar Energy for EVs

- 4.3 Market Restraints

- 4.3.1 High Cost and Process Complexity of Advanced Glazing

- 4.3.2 Soda-Ash Supply Shocks Inflating Glass Costs

- 4.3.3 Regulations Limiting Polycarbonate in Windscreens

- 4.3.4 Recycling Mandates Add Reverse-Logistics Burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Laminated Glass

- 5.1.2 Tempered Glass

- 5.1.3 Polycarbonate Glass

- 5.2 By Application Type

- 5.2.1 Front Windshield

- 5.2.2 Rear Windshield

- 5.2.3 Sidelites (Side Windows)

- 5.2.4 Sunroof

- 5.2.5 Quarter Glass

- 5.3 By Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine (ICE)

- 5.4.2 Battery Electric Vehicle (BEV)

- 5.4.3 Hybrid Electric Vehicle (HEV)

- 5.4.4 Plug-In Hybrid Electric Vehicle (PHEV)

- 5.4.5 Fuel-Cell Electric Vehicle (FCEV)

- 5.5 By Distribution Channel

- 5.5.1 Original Equipment Manufacturer (OEM)

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 Spain

- 5.6.3.4 Italy

- 5.6.3.5 France

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Saint-Gobain S.A.

- 6.4.3 Nippon Sheet Glass Co., Ltd.

- 6.4.4 Fuyao Glass Industry Group Co., Ltd.

- 6.4.5 Xinyi Glass Holdings Ltd.

- 6.4.6 Guardian Industries

- 6.4.7 Vitro SAB de CV

- 6.4.8 Central Glass Co., Ltd.

- 6.4.9 Teijin Limited

- 6.4.10 Webasto SE

- 6.4.11 Magna International Inc.

- 6.4.12 Gentex Corporation

- 6.4.13 AGP eGlass

- 6.4.14 Corning Incorporated

- 6.4.15 Sisecam

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment