|

시장보고서

상품코드

2063282

제로 트러스트 네트워크 액세스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Zero Trust Network Access - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

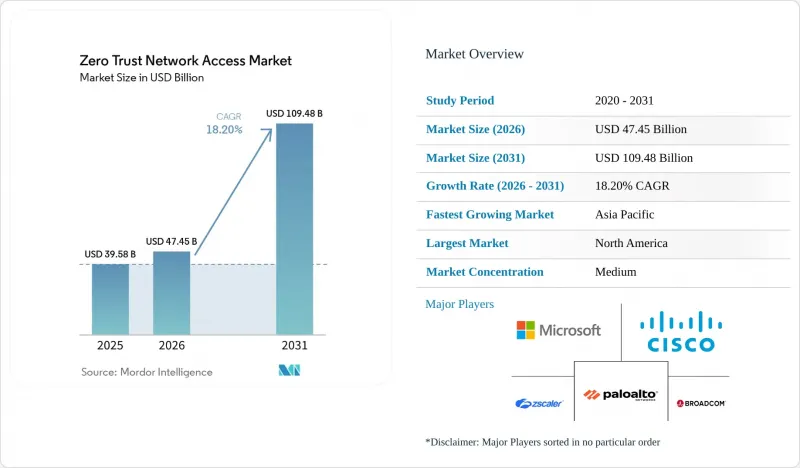

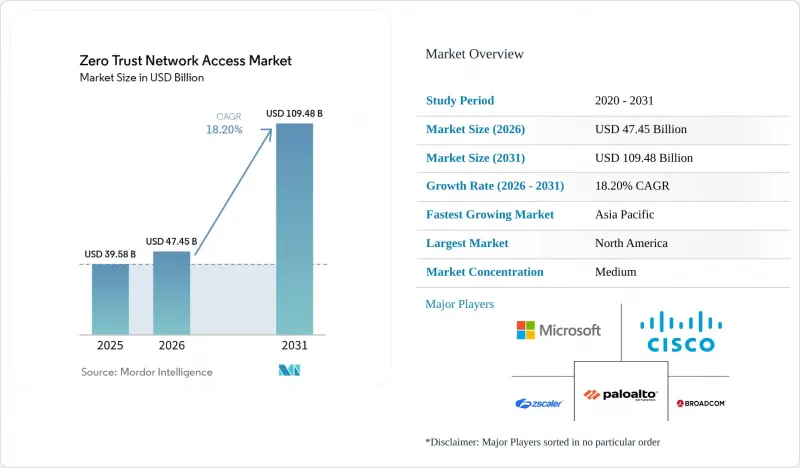

Mordor Intelligence에 의하면, 제로 트러스트 네트워크 액세스(ZTNA) 시장 규모는 2025년에 395억 8,000만 달러로 평가되었습니다. 2026년에 474억 5,000만 달러에 달하고, 2031년까지 1,094억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 18.20%를 나타낼 것으로 전망됩니다.

본 보고서는 구성 요소별(플랫폼 수준의 ZTNA, 데이터 중심형 보안 플랫폼 등), 도입 형태별(클라우드 기반, 하이브리드형, On-Premise형), 조직 규모별(대기업 등), 산업별(은행, 금융서비스 및 보험(BFSI), 헬스케어, 정부 기관 등), 지역별(북미, 아시아태평양, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 제로 트러스트 네트워크 액세스 시장 동향 및 인사이트

이사회 차원에서의 사이버 위험 책임의 급속한 강화

2023년 12월에 시행된 미국 증권거래위원회(SEC)의 규정에 따라, 상장 기업은 중대한 사고를 4영업일 이내에 공시해야 할 의무가 부과되었으며, 이사의 책임이 보안 대책과 연계되었습니다. 현재 이사회는 최소 권한 적용을 입증하고 침해 조사 기간을 단축할 수 있는 감사 가능한 제로 트러스트 로그를 요구하고 있습니다. 미국 법무부의 2027년도 예산 요청안에는 제로 트러스트에 1억 1,030만 달러가 배정되어 있으며, 이는 공공 조달을 통해 민간 부문의 기준이 설정될 것임을 시사하고 있습니다. 법무 담당자는 ZTNA(제로 트러스트 네트워크 액세스)를 ‘합리적인 안전 조치의 증거’로 규정하고 있으며, 이러한 표현은 사이버 리스크를 거버넌스 지표로 재정의하는 것입니다. 그 결과, 제로 트러스트 네트워크 액세스 시장은 단순한 IT 지출에서 규정 준수를 위한 필수 요건으로 전환되고 있습니다. 제품의 기능을 공개 요건에 직접 부합시킬 수 있는 공급업체는 이사회로부터 더 신속하게 승인을 받을 수 있습니다.

미국 및 EU 공공 부문 IT 지출에서 제로 트러스트 의무화

OMB 각서 M-22-09는 미국의 민간 기관에 대해 2026년 12월까지 5가지 제로 트러스트 핵심 요소를 충족할 것을 요구하고 있습니다. 한편, CISA의 피싱에 강한 다단계 인증(MFA)에 관한 지침에서는 SMS 토큰의 사용이 부적합한 것으로 규정되어 있습니다. 이와 병행하여, 2024년 10월까지 국내법에 반영될 예정인 EU의 NIS2 지침은 18개 주요 부문에 걸쳐 의무를 확대하고, 경영진에 대한 개인적 책임을 도입하고 있습니다. FedRAMP High 또는 EU 인증을 취득한 공급업체는 우선 입찰자 지위를 획득하여 조달 측면에서 우위를 확보합니다. 이러한 의무는 민간 기업이 준수해야 할 세계 규정 준수 최저 기준을 확립하고, 제로 트러스트 네트워크 액세스 시장의 지속적인 성장을 이끌어 낼 것입니다. 지출은 우선 북미와 유럽에서 가속화될 것이며, 아시아·태평양 지역의 정부들도 공급망 계약의 적격성을 유지하기 위해 신속하게 대응해 나갈 것입니다.

분산된 레거시 IAM 스택이 정책 통합을 저해하고 있습니다.

기업에서는 Active Directory, Okta, Ping Identity 및 맞춤형 LDAP 시스템을 함께 사용하는 경우가 많으며, 각각의 스키마와 세션 유효 기간이 다릅니다. CISA의 ‘알려진 악용된 취약점 목록’에는 2025년 3월 기준으로 1,143건의 ID 관련 결함이 등록되었으며, 공격자가 이러한 사일로 간의 간극을 연쇄적으로 이용해 공격을 감행하는 실태가 드러났습니다. 통합 프로세스 중에 병행하여 인증을 수행하면 제로 트러스트의 적용 범위가 약화됩니다. 2023년 10월 발생한 Okta 침해 사건에서는 지원 포털의 토큰이 도난당했으며, 단 하나의 취약한 링크만으로도 페더레이션의 신뢰가 훼손될 수 있음이 밝혀졌습니다. ID 통합이 가속화되기 전까지는 ZTNA 프로젝트에 더 오랜 시간과 더 많은 비용이 소요될 것입니다.

부문별 분석

보안 서비스 엣지(SSE) 솔루션은 연평균 성장률(CAGR) 18.96%를 나타낼 것으로 예측되며, 2025년에는 38.18%의 시장 점유율을 차지했던 기존 플랫폼 제품을 추월할 전망입니다. 이러한 변화는 통합 스택이 보안 웹 게이트웨이, CASB, ZTNA를 단일 클라우드 정책으로 통합하여 통합에 따른 오버헤드를 줄이기 위함입니다. Dell'Oro는 SASE와 SSE에 대한 총 지출이 2030년까지 970억 달러에 육박할 것으로 예측하고 있으며, 이는 이러한 통합이 현재 주류 구매 패턴임을 뒷받침하고 있습니다. 독립형 플랫폼은 하이브리드 환경에서 여전히 중요하지만, 하이퍼스케일러들이 대규모 계약에 액세스 제어를 도입함에 따라 가격 면에서 압박을 받고 있습니다. 데이터 중심 보안 플랫폼은 기밀 컴퓨팅 엔클레이브 내의 워크로드를 토큰화함으로써 규제 대상 데이터 흐름에 대응합니다. IAM 제품군은 여전히 신원 관리의 기반이 되지만, 멀티 클라우드 환경 전체에서 속성을 동기화해야 하기 때문에 이 작업으로 인해 프로젝트 진행이 지연되고 있습니다.

플랫폼 수준의 ZTNA는 On-Premise 데이터센터가 계속 운영되는 환경에서 전략적 가치를 유지합니다. 시스코의 Armorblox 인수를 통해 협업 도구 내 피싱을 감지하기 위한 자연어 분석 기능이 추가되었습니다. 틈새 시장 전문 공급업체들은 OT 세분화을 목표로 삼고 있으며, SSE 벤더가 제공하지 않는 프로토콜 인식형 제어 기능을 제공합니다. 예측 기간 동안, 구성 요소 범주별 제로 트러스트 네트워크 액세스(ZTNA) 시장 규모는 구매자가 포인트 도구를 통합형 클라우드에 얼마나 신속하게 통합할 수 있는지에 따라 달라질 것입니다.

2025년에는 클라우드 기반 도입이 지출의 63.71%를 차지하며, 연평균 성장률(CAGR) 18.57%를 나타냈습니다. 사용자 단위로 요금이 부과되는 SaaS 이용 모델은 어플라이언스의 교체 주기에 따른 자본적 장벽을 해소합니다. Zscaler의 클라우드는 150개의 노드에 걸쳐 하루 5,000억 건 이상의 트랜잭션을 처리하고 있으며, 이는 규모의 경제를 여실히 보여주고 있습니다. 하이브리드 모델은 데이터 소재지에 관한 법률의 제약을 받는 업계에 매력적입니다. 왜냐하면 공급업체는 정책 노드를 자국 영토 내에 배치할 수 있기 때문입니다. On-Premise 구축은 에어갭 환경이나 기밀 네트워크에서 여전히 이루어지고 있지만, 인력 부족 문제에 직면해 있습니다. CISA(미국 사이버보안·인프라보안청)는 보안 엔클레이브 분야의 제로 트러스트 전문 인력이 50만 명 부족할 것으로 추산하고 있습니다.

운영 비용 측면에서는 클라우드가 유리합니다. 사용자당 월 5-15달러의 이용료는 수십만 달러 규모의 하드웨어 구매보다 승인받기 쉽기 때문입니다. 하이브리드 솔루션에서는 클라우드 엔진과 로컬 게이트웨이 간에 정책을 지속적으로 동기화해야 하며, 파로알토 네트웍스와 같은 벤더들은 자동 복제를 통해 이러한 복잡성을 해소하고자 하고 있습니다. 프로토콜 변환이 필요한 산업 현장에서는 On-Premise형 게이트웨이가 여전히 유용하지만, 설비 투자(CAPEX)의 제약으로 인해 도입 속도는 둔화되고 있습니다.

지역별 분석

북미는 미국 연방 정부의 의무 규정, SEC의 공시 규정, 그리고 성숙한 통합업체 생태계의 뒷받침을 받아 41.24%의 점유율로 계속해서 주도적인 위치를 유지하고 있습니다. 미국 법무부의 예산안에는 2027 회계연도에 제로 트러스트 대책으로 1억 1,030만 달러가 편성되어 있어, 이에 대한 수요가 지속될 것임을 시사하고 있습니다. 캐나다에서 제안된 ‘중요 사이버 시스템 보호법’은 적용 범위를 통신 및 에너지 분야로 확대함으로써 국내 공급업체를 지원하고 있습니다. 멕시코는 예산 면에서 뒤처져 있지만, 미국 제조업의 니어쇼어링이 데이터 흐름을 보호하기 위한 국경을 초월한 ZTNA를 촉진하고 있습니다.

아시아태평양은 각국 정부가 사이버 규제를 디지털 경제의 목표와 조화시켜 나감에 따라 연평균 성장률(CAGR) 18.91%로 가장 높은 성장세를 보일 것으로 전망됩니다. 일본은 2024년, 112억 달러 규모의 디지털 예산 중 3,000억 엔(20억 달러)을 사이버 보안에 배정했습니다. 인도의 CERT-In 지침에 따르면, 침해 사실을 6시간 이내에 보고하고, 로그를 180일간 보관해야 할 의무가 있습니다. 싱가포르의 ‘스마트 네이션’ 프로그램에서는 시민 서비스에 있어 신원 확인 기능을 갖춘 접근이 요구되고 있으며, 한국에서는 생체 인증 데이터 처리 업체에 대해 제로 트러스트가 의무화되어 있습니다. 중국의 보안 심사는 국내 공급업체를 우대하고 있으며, 세계 시장을 개별 정책 영역으로 분할하고 있습니다.

유럽에서는 NIS2 도입 현황에 차이가 있지만 시장은 확대되고 있으며, 독일은 2024년에 법안을 통과시켰으나 이탈리아와 스페인은 2025년까지 시행을 연기했습니다. 영국 NCSC의 지침에 따르면, 고가치 자산부터 단계적으로 제로 트러스트를 도입하는 것이 권장됩니다. 중동에서는 주권 클라우드에 대한 투자가 진행되고 있으며, 사우디아라비아는 국내 데이터 저장을 의무화하고 있고, UAE는 유엔의 전자정부 순위에 부합하는 국가 기준을 발표했습니다. 남미와 아프리카는 여전히 초기 단계에 있습니다. 브라질의 LGPD나 남아프리카공화국의 POPIA에 따라 규정 준수를 촉진하는 요인은 존재하지만, 예산 및 기술 부족으로 인해 도입이 지연되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the zero trust network access market size is projected to be USD 39.58 billion in 2025, USD 47.45 billion in 2026, and reach USD 109.48 billion by 2031, growing at an 18.20% CAGR from 2026 to 2031.

This report is Segmented by Component (Platform-Level ZTNA, Data-Centric Security Platforms, and More), Deployment Mode (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and More), Industry Vertical (BFSI, Healthcare, Government, and More), and Geography (North America, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Zero Trust Network Access Market Trends and Insights

Rapid Board-Level Cyber-Risk Accountability

The U.S. Securities and Exchange Commission rule that came into force in December 2023 forces listed companies to disclose material incidents within four business days, linking director liability to security controls. Boards now demand auditable zero-trust logs that prove least-privilege enforcement and shorten breach investigations. U.S. Department of Justice budget requests for fiscal 2027 earmark USD 110.3 million for zero-trust, signaling that public procurement will set the private-sector baseline. Legal counsel describes ZTNA as evidence of reasonable safeguards, a phrase that redefines cyber-risk as a governance metric. As a result, the Zero Trust Network Access market is moving from discretionary IT spending to compliance-driven obligations. Vendors able to map product features directly to disclosure requirements win faster board approval.

Mandates for Zero-Trust by U.S. and EU Public-Sector IT Spending

OMB memorandum M-22-09 sets a December 2026 deadline for U.S. civilian agencies to satisfy five zero-trust pillars, while CISA's directive on phishing-resistant MFA disqualifies SMS tokens. In parallel, the EU NIS2 Directive, transposed into national law by October 2024, expands obligations across 18 critical sectors and introduces personal liability for management. Vendors with FedRAMP High or EU certification gain preferred-bidder status, creating a procurement edge. These mandates establish a global compliance floor that private firms must match, driving sustained growth in the Zero Trust Network Access market. Spending accelerates first in North America and Europe, with Asia-Pacific governments quickly aligning to remain eligible for supply-chain contracts.

Fragmented Legacy IAM Stacks Slowing Policy Unification

Enterprises often juggle Active Directory, Okta, Ping Identity, and bespoke LDAP systems, each with different schemas and session lifetimes. CISA's Known Exploited Vulnerabilities list registered 1,143 identity-related flaws by March 2025, illustrating how attackers chain gaps across these silos. Running parallel authentication during consolidation dilutes zero-trust coverage. The October 2023 Okta breach, where support-portal tokens were stolen, showed that a single weak link undermines federated trust. Until identity harmonization accelerates, ZTNA projects face longer timelines and higher costs.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native Data Fabrics Needing Identity-Aware Micro-Segmentation

- Generative-AI Threat Surface Expansion

- High Transition CAPEX for Brown-Field OT Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security Service Edge solutions are forecast to expand at an 18.96% CAGR, eclipsing traditional platform offerings that held a 38.18% share in 2025. The shift arises because converged stacks bundle secure web gateway, CASB, and ZTNA into a single cloud policy, cutting integration overhead. Dell'Oro projects combined SASE and SSE spending to approach USD 97 billion by 2030, reinforcing that convergence is now the mainstream buying pattern. Standalone platforms remain relevant for hybrid estates, but face price pressure as hyperscalers embed access control into larger deals. Data-centric security platforms address regulated data flows by wrapping tokenization around workloads in confidential-computing enclaves. IAM suites continue as the identity backbone, yet must synchronize attributes across multicloud deployments, a task that slows projects.

Platform-level ZTNA keeps strategic value where on-premises data centers persist. Cisco's Armorblox buy added natural-language analytics to detect phishing in collaboration tools. Niche providers target OT segmentation, offering protocol-aware controls that SSE vendors do not. Over the forecast horizon, the Zero Trust Network Access market size for component categories will hinge on how quickly buyers collapse point tools into unified clouds.

Cloud-based deployments accounted for 63.71% of spending in 2025 and are projected to grow at a 18.57% CAGR. SaaS consumption models priced per user remove the capital hurdle of appliance refresh cycles. Zscaler's cloud processes more than 500 billion daily transactions across 150 nodes, illustrating the scale advantage. Hybrid models appeal to sectors bound by data-residency laws because vendors can place policy nodes within national borders. On-premises deployments persist in air-gapped or classified networks but face staffing shortages; CISA counts a 500,000-person gap in zero-trust talent for secure enclaves.

Operational economics favor cloud because monthly fees of USD 5-15 per user are easier to approve than six-figure hardware buys. Hybrid solutions must constantly sync policies between cloud engines and local gateways, a complexity that vendors like Palo Alto Networks attempt to mask through automated replication. On industrial sites that require protocol translation, on-premises gateways remain relevant, though uptake is slower due to CAPEX constraints.

Geography Analysis

North America continues to lead with 41.24% share, supported by U.S. federal mandates, SEC disclosure rules, and a mature ecosystem of integrators. The U.S. justice budget seeks USD 110.3 million for zero-trust in fiscal 2027, signaling sustained demand. Canada's proposed Critical Cyber Systems Protection Act extends requirements to telecom and energy, boosting homegrown suppliers. Mexico lags on budgets, yet near-shoring of U.S. manufacturing drives cross-border ZTNA to secure data flows.

Asia-Pacific is forecast to have the fastest 18.91% CAGR as governments align cyber rules with digital-economy goals. Japan earmarked JPY 300 billion (USD 2 billion) of its USD 11.2 billion digital budget to cybersecurity in 2024. India's CERT-In directive mandates breach reporting within 6 hours and 180-day log retention. Singapore's Smart Nation program requires identity-aware access for citizen services, and South Korea mandates zero-trust for biometric data processors. China's security reviews favor domestic vendors, fragmenting the global market into separate policy domains.

Europe grows despite uneven NIS2 adoption, with Germany passing its law in 2024, while Italy and Spain delayed into 2025. The UK's NCSC principles recommend phased zero-trust rollouts starting with high-value assets. The Middle East invests in sovereign clouds: Saudi Arabia mandates in-country data storage, and the UAE published national standards aligned to UN e-government rankings. South America and Africa remain early-stage; compliance drivers exist under Brazil's LGPD and South Africa's POPIA, but budgets and skill shortages slow uptake.

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Zscaler, Inc.

- Broadcom Inc.

- Okta, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings, Inc.

- IBM Corporation

- Google LLC

- Cloudflare, Inc.

- Akamai Technologies, Inc.

- Illumio, Inc.

- Forcepoint LLC

- Tenable Holdings, Inc.

- Trend Micro Incorporated

- Ping Identity Holding Corp.

- SailPoint Technologies Holdings, Inc.

- Cyxtera Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Board-Level Cyber-Risk Accountability (Post-SEC Rule)

- 4.2.2 Mandates For Zero-Trust By U.S. And EU Public-Sector IT Spending

- 4.2.3 Cloud-Native Data Fabrics Needing Identity-Aware Micro-Segmentation

- 4.2.4 Generative-AI Threat Surface Expansion

- 4.2.5 Tokenisation And Confidential-Computing Adoption

- 4.2.6 Quantum-Resistant Encryption Pilots

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy IAM Stacks Slowing Policy Unification

- 4.3.2 High Transition CAPEX For Brown-Field OT Networks

- 4.3.3 Shortage Of Zero-Trust Architects And ZTMM Skillsets

- 4.3.4 Vendor Lock-In Concerns Around Proprietary Policy Engines

- 4.4 Impact Of Macroeconomic Factors On The Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat Of New Entrants

- 4.8.2 Bargaining Power Of Buyers

- 4.8.3 Bargaining Power Of Suppliers

- 4.8.4 Threat Of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform-Level Zero Trust Network Access (ZTNA)

- 5.1.2 Data-Centric Security Platforms

- 5.1.3 Identity And Access Management (IAM) Suites

- 5.1.4 Security Service Edge (SSE) Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 Hybrid

- 5.2.3 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small And Mid-Sized Enterprises (SME)

- 5.4 By Industry Vertical

- 5.4.1 Banking, Financial Services And Insurance (BFSI)

- 5.4.2 Healthcare And Life Sciences

- 5.4.3 Government And Public Sector

- 5.4.4 IT And Telecom

- 5.4.5 Manufacturing And Critical Infrastructure

- 5.4.6 Retail And E-Commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products And Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 Palo Alto Networks, Inc.

- 6.4.4 Zscaler, Inc.

- 6.4.5 Broadcom Inc.

- 6.4.6 Okta, Inc.

- 6.4.7 Fortinet, Inc.

- 6.4.8 Check Point Software Technologies Ltd.

- 6.4.9 CrowdStrike Holdings, Inc.

- 6.4.10 IBM Corporation

- 6.4.11 Google LLC

- 6.4.12 Cloudflare, Inc.

- 6.4.13 Akamai Technologies, Inc.

- 6.4.14 Illumio, Inc.

- 6.4.15 Forcepoint LLC

- 6.4.16 Tenable Holdings, Inc.

- 6.4.17 Trend Micro Incorporated

- 6.4.18 Ping Identity Holding Corp.

- 6.4.19 SailPoint Technologies Holdings, Inc.

- 6.4.20 Cyxtera Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment