|

시장보고서

상품코드

2063284

광업 TIC : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mining TIC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

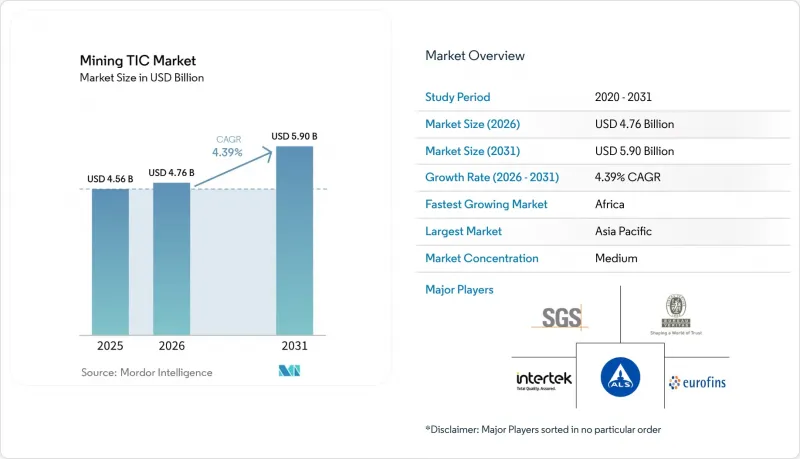

Mordor Intelligence에 의하면, 광업 TIC 시장 규모는 2025년에 45억 6,000만 달러로 평가되었습니다. 2026년 47억 6,000만 달러에서 2031년까지 59억 달러로 확대되고 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.39%를 나타낼 전망입니다.

본 보고서는 서비스 유형(시험, 검사, 인증), 조달 방식(사내 수행, 외부 위탁), 서비스 제공 방식(온사이트, 오프사이트/실험실, 원격/디지털) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 광업 TIC 시장 동향과 인사이트

배터리용 광물 탐사 자본의 급증

2025년, 아프리카 전역의 배터리용 광물 예산은 11% 증가했습니다. 이는 자동차 제조업체와 배터리 제조업체가 오프테이크 계약을 체결함으로써 중소 탐사 기업의 자금 조달 위험을 완화한 결과, 3년 동안 이어져 온 비철금속 지출 감소 추세가 주춤해졌음을 보여줍니다. 벤처 투자자와 전략적 투자자들은 짐바브웨의 리튬 및 콩고민주공화국의 코발트 프로젝트에 28억 달러를 투자했으며, 이에 따라 분석 기관들은 기존의 화성 분석법에 비해 20%에서 30%의 가격 프리미엄이 붙는 유도 결합 플라즈마 질량 분석법(ICP-MS)이나 X선 회절(XRD) 워크플로우를 도입하기 시작했습니다. 2026년 4월, 서지 배터리 메탈즈(Sarge Battery Metals)는 ALS 리미티드(ALS Limited)에 수산화리튬 침출 시험 프로그램을 의뢰했습니다. 이로 인해 처리 기간이 연장되면서, 복잡한 습식 야금 분석에서 만성적인 처리 능력의 한계가 부각되었습니다. 센추리 리튬사는 2026년 2월 실시된 타당성 조사에서 1만 2,000미터의 시추를 수행하고, 4,500건의 분석 시료를 제출했습니다. 이는 프로젝트가 탐사 단계에서 예비 타당성 조사 단계로 넘어갈 때 분석량이 급격히 증가함을 보여줍니다. 하류 부문 수요도 두드러지며, 일렉트라 배터리 머티리얼즈는 2025년 7월 자동차 규격용 황산코발트의 순도 검증을 실시함으로써, 마이닝 TIC 시장의 참여 기업들을 화학 공학 분야로 더욱 깊이 끌어들이고 있습니다.

ESG 규정 준수 요건의 강화

2026년 1월에 발효된 유럽연합(EU)의 기업 지속가능성 보고 지침 및 국제 지속가능성 기준 위원회(ISSB)의 규정에 따라, 광산 기업은 위탁 연구소 및 시료 물류 등을 포함한 스코프 3 배출량을 공개해야 할 의무가 있습니다. 앵글로-아메리칸사는 2026년 1월부터 3월에 걸쳐 3개 사업장에서 ‘책임 있는 광업 보증 이니셔티브(IRMA)’에 대한 모니터링 감사를 완료하고, ISO 14064 온실가스 인벤토리 및 ISO 50001 에너지 관리 요건을 시험·검사·인증(TIC) 제공업체에 적용했습니다. 알베마르사는 2026년 4월, 아타카마 소금호(Salar de Atacama) 시설에서 이와 같은 기준을 충족함으로써, 배터리용 광물 공급망과 검증 가능한 ESG 성과 간의 연계가 점점 더 강화되고 있음을 여실히 보여주었습니다. 2026년 1월에 시작된 TUV NORD의 CERA 4in1 제도는 환경, 사회, 추적성, 순환성에 대한 감사를 단일 계약으로 통합하여 중견 생산업체의 규정 준수 비용을 절감하는 동시에, 광업 TIC 시장에 진출하는 기업들에게 새로운 지속적인 수익원을 창출했습니다. 이에 대해 뷰로베리타스는 ‘Towards Sustainable Mining’ 프로토콜과 ISO 26000의 사회적 지침을 통합한 ‘Mine ESG Audit’ 서비스를 도입하여 인증 기회를 더욱 확대했습니다.

상품 가격 변동이 탐사 예산을 압박하고 있습니다.

2024년 초부터 2025년 말까지 탄산리튬 가격은 46% 하락했고, 니켈은 37%, 코발트는 41% 하락했습니다. 이로 인해 배터리용 광물을 전문으로 하는 검사 기관의 분석량은 15%에서 20% 감소했습니다. BHP는 야금용 석탄 가격이 27% 하락함에 따라 설비 투자를 축소하고, 신규 개발(그린필드)에서 광산 주변의 작업으로 전환하여 분석 비용이 더 적게 드는 저가치 광산으로 중점을 옮겼습니다. 외부 위탁 수요의 80% 이상을 차지하는 중소 탐사 기업들은 2025년 하반기에 12억 달러 규모의 자금 조달을 보류할 수밖에 없게 되었고, 그 결과 시추 거리를 25%에서 30%까지 줄여야 했으며, 검사 기관들은 지급 기한 연장을 어쩔 수 없이 받아들여야 했습니다. 위험이 낮은 프로그램으로의 전환으로 인해, 일반 업무보다 3배 높은 수익성을 지닌 프리미엄 희토류 및 백금족 금속의 분석 수요가 감소하면서, 광업용 TIC 시장의 이익률이 압박받고 있습니다.

부문별 분석

2025년, 광업 TIC 시장 점유율의 48.31%를 분석이 차지했으며, 이는 자원 추정에서 지구화학 분석 및 야금 시험이 중심적인 역할을 하고 있음을 반영합니다. 인증 규모는 작지만, ESG 압력으로 인해 광산 기업들이 제3자에 의한 관리 이력(체인 오브 카스투디) 인증을 요구하는 경향이 강해지고 있어, 연평균 성장률(CAGR) 4.48%로 확대되고 있습니다. 검사는 이 두 가지 사이에 위치하며, 자동화를 통해 검사 건당 비용이 감소하고 기술적 범위가 확대됨에 따라 꾸준히 성장하고 있습니다. 시험 처리량은 여전히 높은 수준을 유지하고 있습니다. 중규모 금광 프로젝트의 경우, 시료 1개당 30-80달러의 비용으로 2만 개의 시료가 생성될 가능성이 있으며, 이는 검사 기관에 있어 예측 가능한 현금 흐름의 기반이 되고 있습니다. 앵글로-아메리칸과 알베마르 등이 ‘책임 있는 광업 보증 이니셔티브(IRMA)’를 연례 감사 주기에 포함시킨 데 따라 인증 수요가 가속화되고 있으며, 이는 인증 기관에게 일시적인 것이 아닌 구조적인 수익원이 될 것임을 시사합니다.

각 검사 기관은 리튬, 코발트, 희토류 분석 워크플로우에 대응하는 고처리량 유도 결합 플라즈마 질량 분석기로의 교체를 추진하고 있으며, 급증하는 배터리용 광물 예산에 걸맞은 처리 능력을 확보하고 있습니다. TUV NORD가 발표한 ‘CERA 4in1’은 ESG 인증을 원스톱으로 제공하여, 중복되는 여러 차례의 감사를 피하고자 하는 중견 제조 기업들의 관심을 모으고 있습니다. SGS의 MsMin 인수를 통해 확보한 드론 기반 노천 채굴 검사 및 로버를 활용한 스톡파일 조사는 인력을 증원하지 않고도 검사 주기를 확대하여 기여 이익률을 향상시키고 있습니다. ISO IWA 45 : 2024의 도입에 따라 인증 신청이 밀려 있는 상황이며, 각 광산 기업들은 1년 전부터 감사 인력을 확보하고 있습니다. 이러한 추세는 광업 TIC 시장에 진출한 기업들에게 견조한 수주 전망을 뒷받침하는 요인이 되고 있습니다.

지역별 분석

2025년, 아시아태평양은 광업 TIC 시장 매출의 38.28%를 차지했습니다. 이는 중국의 희토류 정제 감사, 호주의 철광석 품위 관리 프로토콜, 그리고 인도의 석탄 수출 검사에 힘입은 결과입니다. 유로핀즈와 SGS는 하류 자석 제조업체들이 요구하는 순도 및 추적성 검사에 대응하기 위해 중국에 촘촘한 검사 네트워크를 구축하고 있습니다. 또한 SGS는 2025년 1월 필바라에 시설을 가동하여 하루 최대 1,000건의 철광석 시료를 처리하며, 주요 생산업체에 4시간 이내에 결과를 제공한다고 보장하고 있습니다. 호주의 금광 사업에서 휴대용 형광 X선 분석 장비를 도입함에 따라, 외부 분석에 대한 의존도가 낮아지고 있으며, 이는 실시간 의사 결정으로의 전환을 반영하고 있습니다. 인도에서 철광석 화물에 대한 제3자 검증 움직임이 코텍나사의 2025년 항만 계약에도 반영되어 있으며, 이는 해당 지역에서 중립적인 검증이 점점 더 중요시되고 있음을 보여줍니다.

아프리카는 가장 빠르게 성장하고 있는 지역으로, 짐바브웨에서의 리튬 발견과 콩고민주공화국의 코발트 생산 능력 확대에 힘입어 2031년까지 연평균 성장률(CAGR) 5.22%를 나타낼 것으로 전망됩니다. 세계적인 가격 변동에도 불구하고, 전략적 투자자들이 새로운 자본을 투입함에 따라 2025년 탐사 예산은 11% 증가했습니다. SGS는 2025년 9월 나미비아에 연구소를 개설하고, 희토류 분석 수요에 부응하기 위해 유도 결합 플라즈마 질량 분석법을 도입함으로써 신흥 시장에서 선구자로서의 우위를 강조하고 있습니다. 자동차 제조업체들이 더욱 엄격한 사양을 요구함에 따라 코발트 황산염의 순도 시험이 활발해지고 있으며, 이는 구리 벨트 지역 내 프리미엄 분석 수요를 견인하고 있습니다. 물류 분야의 과제는 여전히 심각합니다. 시료의 항공 운송비는 편당 2,000달러에 달하기도 하며, 환율 변동을 고려하여 업체의 이익을 확보하기 위해 달러 표시 계약이 주류를 이루고 있습니다.

북미와 유럽은 광업 TIC 시장에서 성숙 단계에 접어들었음에도 여전히 성장을 이어가고 있는 지역입니다. 미국에서는 2029년까지 지질과학 분야에서 13만 명의 인력 부족이 예상되고 있으며, 이로 인해 검사 기관들의 자동화 투자 속도가 빨라지고 있습니다. SGS는 2026년 4월, 퀘벡주의 이해관계자들과 협력하여 리튬 및 니켈 검사 역량을 확대했습니다. 이는 캐나다의 배터리 공급망에 대한 야망과 맥을 같이하는 것입니다. 2026년 1월에 발효된 유럽의 ‘기업 지속가능성 보고 지침’은 스코프 3 배출량 인벤토리에 대한 수요를 촉진하고 있는 반면, TUV NORD의 CERA 4in1 도입은 유럽연합(EU) 시장 진출을 목표로 하는 생산자들에게 통일된 인증 절차를 제공합니다. 중동은 틈새 성장 분야로 부상하고 있으며, SGS가 2025년 10월 사우디아라비아에 개설한 거점은 ‘비전 2030’에 기반한 광업 투자를 유치하는 것을 목적으로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the mining testing, inspection, and certification (TIC) market size was valued at USD 4.56 billion in 2025 and is estimated to grow from USD 4.76 billion in 2026 to USD 5.90 billion by 2031, at a CAGR of 4.39% from 2026 to 2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

Global Mining TIC Market Trends and Insights

Surge in Battery-Mineral Exploration Capital

Battery-mineral budgets climbed 11% across Africa in 2025, reversing a three-year slide in base-metal spending as automakers and battery manufacturers locked in offtake agreements that reduced funding risk for junior explorers. Venture and strategic investors directed USD 2.8 billion into Zimbabwe lithium and Democratic Republic of the Congo cobalt projects, prompting laboratories to add inductively coupled plasma mass spectrometry and X-ray diffraction workflows that command 20% to 30% price premiums over conventional fire assays. Surge Battery Metals awarded ALS Limited a lithium-hydroxide leach-testing program in April 2026, extending turnaround times and highlighting chronic capacity constraints for complex hydrometallurgical analysis. Century Lithium drilled 12,000 meters and submitted 4,500 assay samples during its February 2026 feasibility study, illustrating the step change in assay volume when projects advance from exploration to pre-feasibility. Downstream pull is also visible, with Electra Battery Materials validating cobalt sulfate purity for automotive specifications in July 2025, drawing Mining TIC market participants deeper into chemical-engineering domains.

Heightened ESG Compliance Requirements

The European Union Corporate Sustainability Reporting Directive and International Sustainability Standards Board rules, effective January 2026, require miners to disclose Scope 3 emissions that encompass contracted laboratories and sample logistics. Anglo American completed Initiative for Responsible Mining Assurance surveillance audits at three operations between January and March 2026, cascading ISO 14064 greenhouse-gas inventories and ISO 50001 energy management requirements to testing, inspection and certification (TIC) providers. Albemarle met the same standard at its Salar de Atacama facility in April 2026, highlighting the tightening link between battery-mineral supply chains and verifiable ESG credentials. TUV NORD's CERA 4in1 scheme, launched in January 2026, bundles environmental, social, traceability, and circularity audits into a single engagement, trimming compliance costs for mid-tier producers and creating a new avenue of recurring revenue for Mining TIC market participants. Bureau Veritas responded by introducing an integrated Mine ESG Audit service that merges Towards Sustainable Mining protocols with ISO 26000 social guidance, further widening the certification opportunity set.

Volatile Commodity Price Cycles Curtailing Exploration Budgets

Lithium carbonate prices dropped 46% between early 2024 and late 2025, while nickel slid 37% and cobalt 41%, leading to a 15% to 20% fall in assay volumes at laboratories focused on battery minerals. BHP pared capital spending after a 27% decline in metallurgical coal prices, shifting from greenfield to near-mine work that needs fewer, lower-value assays. Junior explorers, which drive more than 80% of outsourced demand, lost USD 1.2 billion in committed financing during 2H 2025, forcing drilling meterage cuts of 25% to 30% and pushing laboratories toward extended payment terms. The pivot to lower-risk programs reduces the need for premium rare-earth or platinum-group-metal assays, which can be 3 times as lucrative as routine work, compressing Mining TIC market margins.

Other drivers and restraints analyzed in the detailed report include:

- Digital Core Sampling and Automation Adoption

- Rapid Uptake of Remote and Autonomous Inspections

- Shortage of Qualified Geochemists and Inspectors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing controlled 48.31% of the Mining TIC market share in 2025, reflecting the centrality of geochemical assays and metallurgical testwork to resource estimation. Certification, although smaller, is expanding at a 4.48% CAGR as ESG pressures draw miners toward third-party chain-of-custody credentials. Inspection sits between the two, growing steadily as automation lowers per-inspection cost and expands technical scope. Testing volume intensity remains high; a mid-tier gold campaign can generate 20,000 samples at USD 30 to USD 80 each, underpinning predictable cash flow for laboratories. Certification demand accelerated after Anglo American, Albemarle, and others embedded the Initiative for Responsible Mining Assurance into annual audit cycles, signaling a structural, not episodic, revenue stream for accredited bodies.

Laboratory operators are upgrading to high-throughput inductively coupled plasma mass spectrometry rigs that accommodate lithium, cobalt, and rare-earth workflows, aligning capacity with surging battery-mineral budgets. TUV NORD's CERA 4in1 launch offers a one-stop ESG credential, attracting mid-tier producers that wish to avoid multiple overlapping audits. Drone-assisted pit inspections and rover-based stockpile surveys, gained via SGS's MsMin acquisition, are extending inspection cycles without adding headcount, boosting contribution margins. As ISO IWA 45:2024 rolls out, certification backlogs are forming, prompting miners to reserve auditor slots a year in advance, a pattern that underpins robust order visibility for Mining TIC market participants.

Geography Analysis

Asia-Pacific generated 38.28% of Mining TIC market revenue in 2025, anchored by China's rare-earth refining audits, Australia's iron-ore grade-control protocols, and India's coal export inspections. Eurofins and SGS operate dense laboratory networks in China to meet purity and traceability checks demanded by downstream magnet manufacturers. SGS also commissioned a Pilbara facility in January 2025 to process up to 1,000 iron-ore samples daily, ensuring a four-hour turnaround for major producers. Portable X-ray fluorescence adoption across Australian gold campaigns is reducing reliance on off-site assays, reflecting a shift toward real-time decision-making. India's move toward third-party verification of iron-ore cargo, evident in Cotecna's 2025 port contracts, reflects the region's growing preference for neutral validation.

Africa is the fastest-expanding region, projected to grow at 5.22% CAGR through 2031, driven by lithium finds in Zimbabwe and cobalt capacity in the Democratic Republic of the Congo. Exploration budgets rose 11% in 2025 as strategic investors committed fresh capital despite global price volatility. SGS opened a Namibia laboratory in September 2025 and is adding inductively coupled plasma mass spectrometry to meet demand for rare-earth assays, underscoring its first-mover advantage in nascent jurisdictions. Cobalt sulfate purity testing is intensifying as automakers impose stricter specs, driving premium assay demand in the Copperbelt. Logistics hurdles remain acute; sample flights can cost USD 2,000 per shipment, and currency swings prompt USD-denominated contracts to protect provider margins.

North America and Europe represent mature yet still-growing pockets of the Mining TIC market. The United States faces a 130,000-position gap in geoscience by 2029, motivating labs to accelerate automation investments. SGS partnered with Quebec stakeholders in April 2026 to expand lithium and nickel testing capacity, aligning with Canada's ambitions for the battery supply chain. Europe's Corporate Sustainability Reporting Directive, effective January 2026, is pushing demand for Scope 3 emission inventories, while TUV NORD's CERA 4in1 rollout offers a harmonized certification path for producers seeking European Union market access. The Middle East is emerging as a niche growth pocket, and SGS's October 2025 Saudi Arabia opening is designed to capture Vision 2030 mining investments.

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- ALS Limited

- Eurofins Scientific SE

- TUV SUD AG

- Applus Services S.A.

- Element Materials Technology Group Limited

- DNV AS

- TUV Rheinland AG

- Kiwa N.V.

- Mistras Group, Inc.

- Cotecna Inspection SA

- Core Laboratories N.V.

- China Certification and Inspection Group CCIC

- PetroCanada Laboratories Ltd.

- Alex Stewart International Corporation

- Inspectorate Griffith Australia Pty Ltd.

- Mitra SK Private Limited

- Poni International Inspection Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened ESG Compliance Requirements

- 4.2.2 Increasing Depth and Complexity of Ore Bodies

- 4.2.3 Digital Core Sampling and Automation Adoption

- 4.2.4 Surge in Battery-Mineral Exploration Capital

- 4.2.5 Rapid Uptake of Remote and Autonomous Inspections

- 4.2.6 Growing Demand for Outsourced TIC in Junior Mining Firms

- 4.3 Market Restraints

- 4.3.1 Volatile Commodity Price Cycles Curtailing Exploration Budgets

- 4.3.2 Shortage of Qualified Geochemists and Inspectors

- 4.3.3 Fragmented Global Regulatory Regimes

- 4.3.4 Rising Cost of On-site Sample Logistics in Remote Regions

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Mode of Service Delivery

- 5.3.1 On-site

- 5.3.2 Off-site / Laboratory

- 5.3.3 Remote / Digital

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas SA

- 6.4.3 Intertek Group plc

- 6.4.4 ALS Limited

- 6.4.5 Eurofins Scientific SE

- 6.4.6 TUV SUD AG

- 6.4.7 Applus Services S.A.

- 6.4.8 Element Materials Technology Group Limited

- 6.4.9 DNV AS

- 6.4.10 TUV Rheinland AG

- 6.4.11 Kiwa N.V.

- 6.4.12 Mistras Group, Inc.

- 6.4.13 Cotecna Inspection SA

- 6.4.14 Core Laboratories N.V.

- 6.4.15 China Certification and Inspection Group CCIC

- 6.4.16 PetroCanada Laboratories Ltd.

- 6.4.17 Alex Stewart International Corporation

- 6.4.18 Inspectorate Griffith Australia Pty Ltd.

- 6.4.19 Mitra SK Private Limited

- 6.4.20 Poni International Inspection Group Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment