|

시장보고서

상품코드

2063285

의약품 TIC 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pharmaceutical TIC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

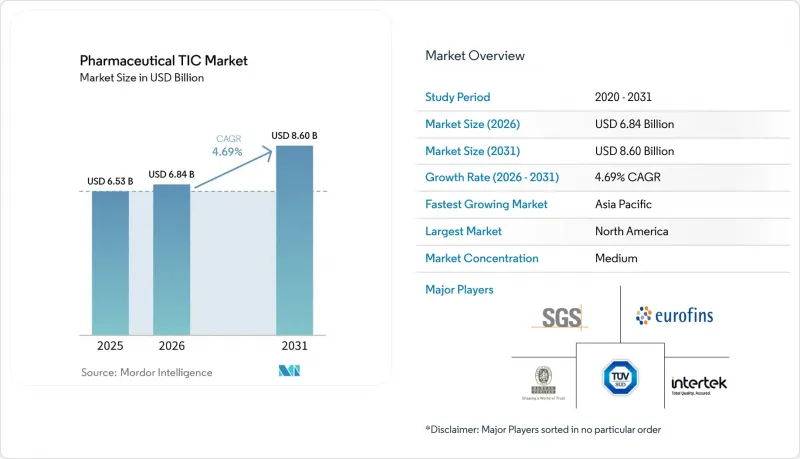

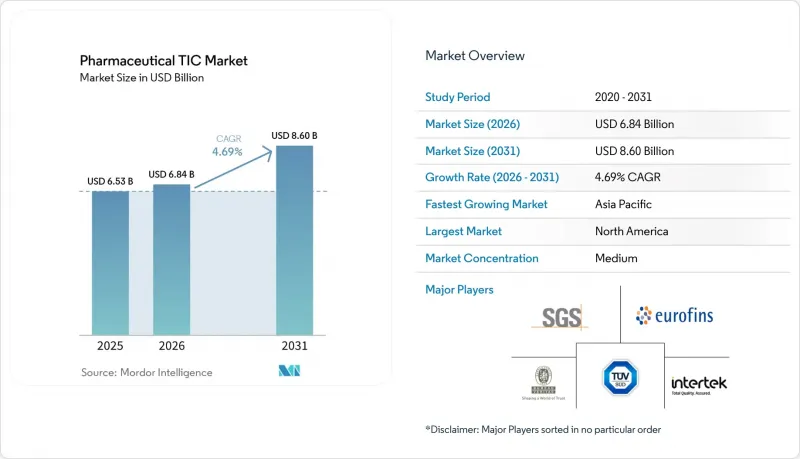

Mordor Intelligence에 의하면, 의약품 TIC 시장은 2025년에 65억 3,000만 달러로 평가되었고, 2026년 68억 4,000만 달러로 추정되고, 2031년까지 86억 달러로 성장할 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 4.69%가 될 것으로 추정되고 있습니다.

본 보고서는 서비스 유형별(시험, 검사, 인증), 조달 유형별(사내, 외부 위탁), 서비스 제공 형태별(온사이트, 오프사이트 및 실험실, 원격 및 디지털) 및 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의약품 TIC 시장 동향 및 인사이트

전 세계 GMP 규제의 강화

FDA는 2025년, 지난 20년 동안 가장 많은 수의 경고장을 발부했습니다. 그 주된 원인은 데이터 무결성의 결여와 무균성 관리의 미비였으며, 이로 인해 제조업체들은 무균 충전 라인과 전자 기록에 대한 제3자의 검증을 요구하게 되었습니다. 유럽의약품청(EMA)이 2022년에 부속서 1을 개정함에 따라 엄격한 오염 관리 규정이 도입되었으며, 현재 해당 지역 전체에서 클린룸의 정기적인 인증에 대한 수요가 증가하고 있습니다. WHO는 2025년 말까지 사전 인증 대상지를 87곳으로 확대하고, 각 시설에 대해 승인된 시험·검사·인증(TIC) 기관의 2년마다 실시하는 감사를 의무화했습니다. FDA의 PreCheck 시범 프로그램 초기 결과에 따르면, 인증된 TIC 기관의 보증이 갖춰진 경우 검사 소요 기간이 60일로 단축되었습니다. 이러한 움직임은 전반적으로 외부 기관에 의한 시험 및 인증을 제약 업무의 기반으로 정착시키는 것입니다.

복잡한 시험이 필요한 바이오의약품 파이프라인의 가속화

FDA는 2024년에 16개의 생물학적 제제를 승인했으며, 그 대부분은 단일클론 항체였지만, EMA는 같은 해에 11개의 바이오시밀러를 추가로 승인했습니다. 생물학적 제제의 경우, 당사슬 프로파일링이나 숙주 세포 단백질의 정량과 같은 고도의 분석법이 필요하지만, 이를 자사 연구소에서 보유하고 있는 기업은 거의 없습니다. 2024년 ICH Q5E 개정으로 인해, 많은 제조업체들은 ISO/IEC 17025 인증을 받은 파트너를 통해 측정법의 재검증을 수행할 수밖에 없게 되었습니다. 세포 및 유전자 치료 파이프라인의 확대에 따라, 벡터 효능 시험 및 복제 능력을 가진 바이러스에 대한 시험이 서비스 라인업에 추가되었습니다. 제품 포트폴리오가 틈새 의약품 및 맞춤형 의료 분야로 세분화되는 가운데, 바이오의약품에 대한 깊은 전문 지식을 갖춘 위탁 검사 기관은 필수적인 파트너가 되고 있습니다.

신흥 시장의 숙련된 감사 인력 부족

인도의 CDSCO는 2025년 검사관 결원율이 40%에 달했다고 보고했으며, 아시아태평양 실험실의 62%가 고도의 생물학적 제제 분석 담당자 채용에 어려움을 겪고 있다고 지적하고 있습니다. 교육 체계의 미비 및 고임금을 제공하는 제약 업계로의 인재 유출로 인해 감사 지연이 4-6주 정도 길어지고 있습니다. 주요 TIC 기업들은 지역 아카데미 및 대학과의 제휴를 통해 대응하고 있지만, 인력이 꾸준히 늘어나기까지는 아직 몇 년이 더 걸릴 것으로 예상되어, 성장세가 두드러지는 지역에서의 서비스 확장이 제약을 받고 있습니다.

부문별 분석

2025년 매출의 43.19%를 검사 업무가 차지하며, 서비스 유형 중 의약품 TIC 시장에서 가장 높은 점유율을 기록했습니다. 이러한 수요는 단일클론 항체나 세포 및 유전자 치료제를 위한 복잡한 분석법에서 비롯된 것으로, 이를 위해서는 고가의 전문 장비가 필요하지만 많은 사내 연구실에서는 이러한 장비를 보유하고 있지 않습니다. 인증 분야는 규모는 작지만, 기업들이 수출의 길을 열기 위해 ISO 13485나 WHO의 사전 승인을 취득하려 하고 있어 연평균 성장률(CAGR) 4.71%로 가장 빠르게 성장하고 있습니다. 인증과 관련된 의약품 TIC 시장 규모는 전 세계적인 상호인정협정의 진전에 따라 꾸준히 확대될 것으로 예측됩니다.

검사 서비스 분야에서는 원격 플랫폼의 보급으로 현장 작업 시간이 단축되면서 이익률에 대한 압박이 커지고 있지만, 연속 생산 및 데이터 무결성에 관한 전문적인 감사는 가격 결정력을 유지하고 있습니다. ISO 13485, ISO 9001 및 GDP 감사를 결합한 다년 계약 인증 패키지는 TIC 제공업체에 지속적인 수익을 가져다줍니다. 또한, 풍부한 데이터를 기반으로 한 시험 워크플로는 분석 분야에서 장기적인 비즈니스 기회를 창출하며, 검사 기관이 규정 준수 지원뿐만 아니라 프로세스 최적화에 관한 조언을 제공할 수 있도록 합니다.

지역별 분석

매사추세츠주, 뉴저지주, 노스캐롤라이나주의 바이오의약품 클러스터가 제3자 검증에 크게 의존한 결과, 2025년 매출의 34.41%를 북미가 차지했습니다. 2025년에 112건의 경고장이 발부되면서 강화된 해당 지역의 엄격한 감독 체제에 따라, 무균 충전 라인 및 전자 기록 분야에서 인증 시험 도입이 거의 전면적으로 진행되었습니다. 2026년 PreCheck 시범 프로그램은 디지털 트윈과 실시간 데이터 스트림을 통해 외부 감사를 더욱 정착시키는 것입니다. 캐나다와 멕시코는 지역 공급을 위한 생산 규모를 확대하고 있으며, WHO 사전 승인 및 수출 증명서와 관련된 새로운 입찰 기회를 창출함으로써 수요를 점차 끌어올리고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 인도의 1,500억 루피(1,200만 달러)에 달하는 생산 연계형 인센티브와, 2024년 중국의 48건의 생물학적 제제 승인을 바탕으로 2031년까지 연평균 성장률(CAGR) 5.54%로 확대될 전망입니다. 인도의 시설에서는 2025년에 87건의 FDA 사전 승인 검사가 실시되었으며, 이는 2020년에 비해 크게 증가한 수치인 만큼, 준비 현황을 확인하기 위해 TIC 기업을 활용하는 사례가 늘고 있습니다. 중국의 트라스투주맙 및 아달리무맙 바이오시밀러 시장 진출은 분석 수요를 더욱 부추기고 있는 반면, 일본의 리스크 기반 GMP 체제에서는 지속적인 제조 감사가 우선시되고 있습니다. 한국과 호주는 수출 지향적인 바이오의약품 및 백신 공장을 통해 틈새 시장을 담당하고 있습니다.

유럽에서는 2022년 EMA 부속서 1(오염 관리 규정)을 배경으로 여전히 큰 수요가 유지되고 있습니다. 독일, 프랑스, 영국은 광범위한 충전 변이체 시험 및 효능 시험이 필요한 바이오의약품 생산을 뒷받침하고 있습니다. EU와 미국의 상호 인정을 통해 규제상의 중복은 완화되었지만, 제조업체들은 여전히 국경을 넘는 보증을 위해 현지 TIC 파트너를 유지하고 있습니다. 중동은 여전히 분열된 상태가 지속되고 있습니다. 사우디아라비아는 ‘비전 2030’에 따른 노력을 추진하는 한편, UAE와 튀르키예는 독자적인 체계를 채택하고 있어, 이로 인해 여러 관할 구역에 걸친 컨설팅 수요가 증가하고 있습니다. 남미와 아프리카는 현재로서는 수익 기여도가 미미하지만, 수입 의존도를 낮추기 위한 생산 능력 투자를 추진하고 있어, 2028년 이후 TIC의 보급이 더욱 확대될 기반이 마련되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the pharmaceutical TIC market was valued at USD 6.53 billion in 2025 and is estimated to grow from USD 6.84 billion in 2026 to USD 8.60 billion by 2031, at a CAGR of 4.69% from 2026 to 2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Pharmaceutical TIC Market Trends and Insights

Stringent Global GMP Enforcement

The FDA, in 2025, issued its highest number of warning letters in two decades, largely for data-integrity lapses and aseptic errors, prompting manufacturers to seek third-party validation of sterile-fill lines and electronic records. The European Medicines Agency's 2022 Annex 1 update imposed prescriptive contamination-control rules that now drive demand for routine clean-room certification across the region. WHO expanded prequalification to 87 sites by end-2025, each requiring biennial audits by approved testing, inspection, and certification (TIC) bodies. Early results from the FDA PreCheck pilot indicate inspection lead times are shrinking to 60 days when accredited TIC assurances are in place. Collectively, these moves embed external testing and certification into baseline pharmaceutical operations.

Accelerating Biologics Pipeline Requiring Complex Testing

The FDA cleared 16 biologics in 2024, with monoclonal antibodies dominating approvals, while the EMA authorized an additional 11 biosimilars the same year. Biologics demand advanced assays such as glycosylation profiling and host-cell protein quantification that few in-house labs possess. The 2024 revision of ICH Q5E pushed many manufacturers to revalidate methods via ISO/IEC 17025-accredited partners. Growing cell-and-gene therapy pipelines add vector potency and replication-competent virus testing to the services mix. As product portfolios fragment into niche and personalized medicines, contract laboratories with deep biologics expertise become indispensable allies.

Scarcity of Skilled Auditors in Emerging Markets

India's CDSCO reported a 40% vacancy rate among inspectors in 2025, and 62% of Asia-Pacific labs cited hiring challenges for advanced biologics analysts. Limited training pipelines and talent migration into higher-paying pharma roles lengthen audit backlogs by 4 to 6 weeks. Leading TIC firms have responded with regional academies and university partnerships, yet tangible workforce growth is several years off, constraining rapid service expansion in high-growth geographies.

Other drivers and restraints analyzed in the detailed report include:

- Rising Pre-approval Inspection Frequency by US FDA and EMA

- Shift Toward Continuous Manufacturing in Pharma Plants

- High Cost of Advanced Analytical Instrumentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing generated 43.19% of 2025 revenue, marking the largest pharmaceutical TIC market share among service types. Demand stems from complex assays for monoclonal antibodies and cell-and-gene therapies that require costly, specialized instrumentation, which is unavailable in many in-house labs. Certification, though smaller, is rising fastest at a 4.71% CAGR as firms pursue ISO 13485 and WHO prequalification to unlock exports. The pharmaceutical TIC market size linked to certification is expected to widen steadily alongside global mutual recognition agreements.

Margin pressure is sharper in inspection services as remote platforms shorten on-site work, yet specialized audits for continuous manufacturing and data integrity retain pricing power. Bundled multi-year certification contracts that combine ISO 13485, ISO 9001, and GDP audits position TIC providers for recurring revenue. Data-rich testing workflows also generate long-tail opportunities in analytics, enabling laboratories to advise on process optimization alongside compliance.

Geography Analysis

North America accounted for 34.41% of 2025 revenue as biologics clusters in Massachusetts, New Jersey, and North Carolina relied heavily on third-party validations. The region's strict oversight, reinforced by 112 warning letters in 2025, has driven near-universal adoption of accredited testing across sterile-fill lines and electronic records. The 2026 PreCheck pilot further entrenches external audits through digital twins and real-time data streams. Canada and Mexico add incremental volume as both scale production for regional supply, creating new bids for WHO prequalification and export certificates.

Asia-Pacific is the fastest-growing area, advancing at a 5.54% CAGR through 2031, buoyed by India's INR 150 billion (USD 12 million) production-linked incentives and China's 48 biologic approvals in 2024. Indian facilities faced 87 FDA pre-approval inspections in 2025, up sharply from 2020, prompting widespread engagement of TIC firms for readiness checks. China's push into trastuzumab and adalimumab biosimilars further lifts analytical demand, while Japan's risk-based GMP regime prioritizes continuous-manufacturing audits. South Korea and Australia contribute niche volumes through export-oriented biologics and vaccine plants.

Europe maintains a sizable demand on the back of its 2022 EMA Annex 1 contamination-control rules. Germany, France, and the United Kingdom anchor biologics output that necessitates extensive charge-variant and potency testing. Although EU-US mutual recognition eases regulatory duplication, manufacturers still retain local TIC partners for cross-border assurance. The Middle East remains fragmented; Saudi Arabia aligns toward Vision 2030, while the UAE and Turkey operate distinct frameworks, boosting multi-jurisdiction consulting. South America and Africa presently contribute modest revenue but are investing in capacity to cut import reliance, setting the stage for greater TIC penetration after 2028.

- SGS SA

- Eurofins Scientific SE

- Bureau Veritas SA

- TUV SUD AG

- Intertek Group plc

- Applus Services, S.A.

- UL Solutions Inc.

- DNV AS

- TUV Rheinland AG

- ALS Limited

- Pace Analytical Services LLC

- NSF International

- Charles River Laboratories International, Inc.

- Element Materials Technology Group Limited

- Microbac Laboratories, Inc.

- Labstat International Inc.

- AmSpec LLC

- BSI Group (The British Standards Institution)

- Labcorp Drug Development, Inc.

- Pharmaron Beijing Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global GMP Enforcement

- 4.2.2 Accelerating Biologics Pipeline Requiring Complex Testing

- 4.2.3 Shift Toward Continuous Manufacturing in Pharma Plants

- 4.2.4 Rising Pre-approval Inspection Frequency by US FDA and EMA

- 4.2.5 Digital Twin Adoption for Remote Inspection

- 4.2.6 Green Chemistry Validation Mandates

- 4.3 Market Restraints

- 4.3.1 Scarcity of Skilled Auditors in Emerging Markets

- 4.3.2 High Cost of Advanced Analytical Instrumentation

- 4.3.3 Fragmented Regulatory Frameworks Across Middle East

- 4.3.4 Cybersecurity Risks in Connected Lab Equipment

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Mode of Service Delivery

- 5.3.1 On-site

- 5.3.2 Off-site / Laboratory

- 5.3.3 Remote / Digital

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Eurofins Scientific SE

- 6.4.3 Bureau Veritas SA

- 6.4.4 TUV SUD AG

- 6.4.5 Intertek Group plc

- 6.4.6 Applus Services, S.A.

- 6.4.7 UL Solutions Inc.

- 6.4.8 DNV AS

- 6.4.9 TUV Rheinland AG

- 6.4.10 ALS Limited

- 6.4.11 Pace Analytical Services LLC

- 6.4.12 NSF International

- 6.4.13 Charles River Laboratories International, Inc.

- 6.4.14 Element Materials Technology Group Limited

- 6.4.15 Microbac Laboratories, Inc.

- 6.4.16 Labstat International Inc.

- 6.4.17 AmSpec LLC

- 6.4.18 BSI Group (The British Standards Institution)

- 6.4.19 Labcorp Drug Development, Inc.

- 6.4.20 Pharmaron Beijing Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment