|

시장보고서

상품코드

2063290

인도의 TIC(시험, 검사 및 인증) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Testing, Inspection, And Certification (TIC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

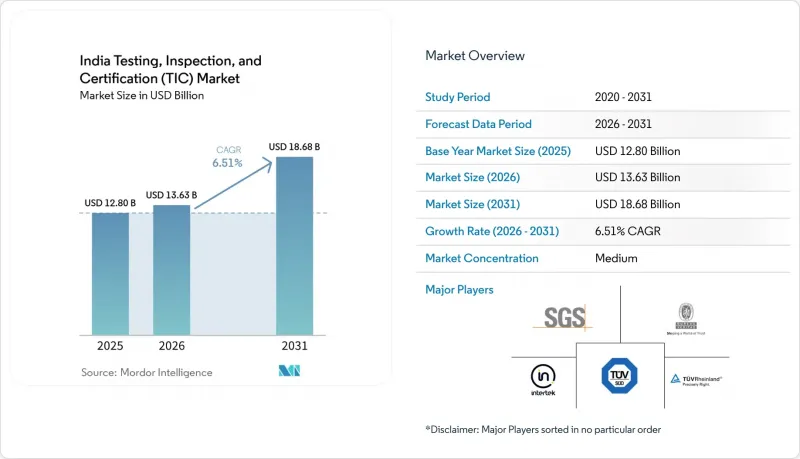

Mordor Intelligence에 의하면, 인도의 TIC(시험, 검사 및 인증) 시장 규모는 2025년 128억 달러로 평가되었습니다. 2026년 136억 3,000만 달러로 확대되어 2031년까지 186억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 6.51%를 나타낼 전망입니다.

본 보고서는 서비스 유형(시험, 검사 및 인증), 조달 형태(사내 실시, 외부 위탁), 업종(소비재 및 소매, ICT·통신, 자동차 및 운송, 기타) 및 서비스 제공 형태(온사이트, 오프사이트·실험실, 원격·디지털)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 TIC(시험, 검사 및 인증) 시장 동향과 인사이트

인도 각 산업 분야의 규제 집행 강화

BIS(인도 표준국)의 검사 결과, 주요 전자상거래 사이트에서 142건의 부적합 제품이 발견되어 각 플랫폼에 경고가 발령된 한편, 제3자에 의한 검증에 대한 수요가 확대되었습니다. 2025년 3월의 품질 관리 명령에 따라 769개 제품이 의무 인증 대상에 추가되었으며, 수공구, 알루미늄 제품, 가전제품 제조업체들이 즉시 규정 준수 대상이 되었습니다. 2025년에 개정된 태양전지 모듈 지침은 국내 생산 능력이 확대되는 바로 그 시점에 성능 시험 기준을 강화하여, 모듈 출하 전에 새로운 적합성 평가를 의무화했습니다. 수출 시장에 대한 병행 감시로 인해 기업들은 국내 기준에 더해 해외 기준까지 준수해야만 하는 상황에 놓이게 되었으며, 확보해야 할 시험 보고서 양이 두 배로 늘어났습니다. 국내외에서 이와 같이 동시에 진행되고 있는 규제 강화로 인해, BIS, IEC 및 수출 대상 시장의 기준을 모두 충족할 수 있는 인증 시험소에게는 지속적인 수주 파이프라인이 확보되고 있습니다.

수출업체 및 OEM 업체에 의한 TIC 아웃소싱 확대

정부의 인증 비용 지원으로 인해, 외부 위탁을 통한 보증은 사실상 보조금을 받는 서비스가 되었으며, 대부분의 중소·영세 기업(MSME)에게 사내 실험실을 유지하는 것은 경제적으로 비합리적이 되었습니다. 자동차 OEM 제조업체들은 이러한 변화를 상징하고 있으며, 배터리 안전성 및 형식 인증 업무를 ARAI에 위탁한 결과, ARAI의 수익은 19% 증가했습니다. 세계 주요 TIC 기업들도 이러한 흐름에 동참하고 있습니다. TUV SUD가 방갈로르에 건설한 1,500만 유로(1,600만 달러) 규모의 복합 시설에서는 EMC 및 의료기기 시험을 일원화하고 있으며, 한편, 인터텍이 아메다바드의 태양광(PV) 시험소를 인수함에 따라, BIS 및 IECEE 인증을 원스톱으로 제공할 수 있게 되었습니다. 각 제조업체는 외부 시험소를 생산량에 따라 유연하게 조정할 수 있는 변동비로 간주하는 경향이 점점 더 강해지고 있습니다. 이를 통해 시장 출시까지 걸리는 시간을 단축하고, 원하는 국제 인증을 즉시 확보할 수 있습니다.

자격을 갖춘 검사원 및 실험실 분석원의 부족

인증 규정의 개정에 따라 수요가 급증한 바로 그 시점에 자격 요건이 상향 조정되면서, 국내에서는 약 1만 명의 자격 보유자가 부족한 상황이 발생했습니다. TUV SUD의 7만 평방피트 규모의 시설과 같은 대규모 확장 프로젝트에서는 전문 EMC 직책을 충원하기 위해 무려 9개월이나 걸리는 채용 기간이 소요되었습니다. CPRI 나시크와 같은 신규 지역 연구소는 다른 거점에서 엔지니어를 차용해야 하기 때문에 내부 자원을 둘러싼 경쟁이 벌어지고 있습니다. 비파괴 검사 분야에서는 인력 부족이 심각하며, 레벨 III 기술자들은 대도시에 집중되어 있고 고액의 급여를 받고 있기 때문에 성수기에는 인증 신청 대기 줄이 길어지고 있습니다. 인력 공급과 업계 수요 간의 불일치로 인해 처리 기간이 길어질 뿐만 아니라, 위험이 있음에도 불구하고 의뢰인이 인증을 받지 않은 대안을 선택할 수밖에 없는 상황도 발생하고 있습니다.

부문별 분석

수출 시장이 ESG 및 제품 안전 기준과 연계된 제3자 인증을 요구함에 따라, 인증의 중요성이 커지고 있습니다. 2025년도 시험 업무는 인도의 TIC 시장의 57.31%를 차지했지만, 서베이런스 감사 및 경영 시스템 갱신이 안정적인 지속 수익을 가져다주기 때문에 인증 수익의 성장률은 더욱 가파릅니다. TRACE 제도에 따른 보조금 덕분에 인증은 단순한 선택적 지출에서 전략적 우위로 그 위상이 변화하고 있으며, 특히 유럽이나 북미로부터의 수주를 목표로 하는 MSME(중소·영세기업)의 경우 이러한 경향이 두드러집니다. 건설, 에너지, 기계 분야에서는 여전히 검사가 필수적이지만, 드론과 AI의 활용이 확대됨에 따라 근로 시간이 단축되고 이익률이 향상되고 있습니다.

인증의 확산세는 금융기관이 의무화하는 ESG 감사나 GRIHA의 ‘Decarbonizing Habitat’ 티어와 같은 프로그램에 힘입어 가속화되고 있습니다. 인터텍(Intertek)의 ‘CarbonClear’ 및 ‘CarbonZero’ 서비스는 구매자의 평가 기준을 충족하기 위해 검증된 저탄소 라벨이 필요한 수출업체를 지원합니다. 제품이 매장에 진열되기 전에 실험실 분석을 의무화하는 QCO(품질 관리 기준)의 적용 범위가 계속 확대되는 가운데, 시험 업무는 여전히 주도적인 위치를 유지하고 있지만, 현재는 인증 업무가 더 가파른 성장 곡선을 그리고 있어, 다양한 인증 규격을 아우르는 제공업체에게 장기적인 수주 기반을 확고히 다져주고 있습니다.

2025년에는 아웃소싱 계약이 65.21%의 점유율을 차지하고 연평균 성장률(CAGR) 7.11%로 증가했으며, 이는 기업들이 변동 비용과 인증에 대한 즉각적인 접근을 중요시하고 있음을 여실히 보여주었습니다. 자동차, 재생에너지, 소비재 수출 기업들은 EMC 시험실, 진동 시험 장비 또는 생물학적 분석 시설에 수백만 달러 규모의 지출을 피하기 위해 규정 준수 프로세스 전반을 외부에 위탁하고 있습니다. TRACE 보조금과 같은 정책으로 인해 경제성이 사내 설비 구축에서 외부 위탁으로 결정적으로 기울고 있기 때문에 외부 위탁 업무와 연계된 인도의 TIC 시장 규모는 계속해서 확대되고 있습니다.

대기업들은 여전히 연구개발(R&D)을 위한 시범 단계의 실험실을 운영하고 있지만, 최종 적합성 평가는 대개 규제 당국이나 해외 구매자가 인정하는 인증을 발급하는 외부 기관에 위탁하고 있습니다. 전국에 25곳 이상의 거점을 갖춘 세계적인 대기업에서는 네트워크 효과가 발생하여, 원스톱 보증과 균일한 품질을 실현하고 있습니다. 개정된 NABL 규정은 중소기업 실험실에 더욱 큰 부담을 주고 있으며, 보수적인 기업조차도 단일 계약을 통해 여러 관할 구역에서 제품 승인을 획득할 수 있는 인증된 아웃소싱 업체를 찾게 만들고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the india testing, inspection, and certification (TIC) market size is expected to increase from USD 12.8 billion in 2025 to USD 13.63 billion in 2026 and reach USD 18.68 billion by 2031, growing at a CAGR of 6.51% over 2026-2031.

This report is Segmented by Service Type (Testing, Inspection, Certification), Sourcing Type (In-House, Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Automotive and Transportation, and More), and Mode of Service Delivery (On-Site, Off-Site Laboratory, Remote Digital). The Market Forecasts are Provided in Terms of Value (USD).

India Testing, Inspection, And Certification (TIC) Market Trends and Insights

Increasing Regulatory Enforcement Across Indian Industries

BIS inspections uncovered 142 non-compliant items on major e-commerce sites, putting platforms on notice and widening demand for third-party verification. The March 2025 Quality Control Orders added 769 products to mandatory certification, instantly pulling manufacturers of hand tools, aluminum goods, and household appliances into the compliance net. Revised 2025 solar-module guidelines toughened performance tests just as domestic capacity scaled, requiring fresh rounds of conformity assessments before modules could ship. Parallel scrutiny from export markets forces firms to layer foreign standards atop domestic ones, multiplying the volume of test reports they must secure. This synchronized enforcement at home and abroad ensures a durable pipeline for accredited laboratories able to cover BIS, IEC, and destination-market norms.

Growing Outsourcing of TIC by Exporters and OEMs

Government reimbursement of certification fees turns outsourced assurance into a subsidized service, making it financially irrational for most MSMEs to maintain internal labs. Automotive OEMs exemplify the shift, funneling battery-safety and homologation work to ARAI, which logged a 19% revenue jump as a result. Global TIC majors keep pace: a EUR 15 million (USD 16 million) Bengaluru complex by TUV SUD centralizes EMC and medical-device testing, while Intertek's purchase of a solar PV lab in Ahmedabad offers one-stop BIS and IECEE approvals. Manufacturers increasingly view external labs as an elastic cost that flexes with output, grants faster time-to-market, and instantly opens access to coveted international accreditations.

Shortage of Qualified Inspectors and Lab Analysts

Revised accreditation rules heightened the skill bar just as demand spiked, leaving the country short by around 10,000 qualified professionals. Large expansions, such as TUV SUD's 70,000-square-foot site, required nine-month hiring cycles to fill specialized EMC roles. New regional labs like CPRI Nashik had to borrow engineers from other sites, illustrating internal cannibalization. Scarcity is acute in non-destructive testing, where Level III technicians cluster in metros and command premium wages, swelling certification queues during seasonal peaks. The mismatch between talent supply and industry need stretches turnaround times and occasionally forces clients toward unaccredited alternatives despite the risks.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Life Sciences and Healthcare Sector

- Expansion of Consumer Goods and Retail Requiring Compliance

- Fragmented Lab Infrastructure and Inconsistent Quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Certification captured growing relevance as export markets insisted on third-party attestations tied to ESG and product-safety norms. While testing still represented 57.31% of the India TIC market in 2025, certification revenue is rising faster because surveillance audits and management-system renewals generate steady annuities. Subsidies under the TRACE scheme reposition certification from discretionary spend to strategic advantage, especially for MSMEs chasing European and North American orders. Inspection remains critical in construction, energy, and machinery, yet rising drone and AI use trims labor hours and lifts margins.

Certification momentum draws strength from lender-mandated ESG audits and programs such as GRIHA's Decarbonizing Habitat tiers. Intertek's CarbonClear and CarbonZero offerings cater to exporters needing verified low-carbon labels to pass buyer scorecards. Testing keeps its primacy through ever-widening QCO coverage that mandates laboratory analysis before goods hit shelves, but certification now delivers the sharper growth slope, anchoring long-term order books for providers with deep multi-standard portfolios.

Outsourced contracts owned 65.21% share in 2025 and are forecast to rise at 7.11% CAGR, underscoring how firms favor variable costs and instant access to accreditations. Automotive, renewable energy, and consumer-goods exporters outsource whole compliance cycles to avoid multimillion-dollar outlays on EMC chambers, vibration rigs, or bioanalytical suites. The India TIC market size attached to outsourced work keeps expanding as policies like the TRACE subsidy tilt the economics decisively away from in-house builds.

Large manufacturers still keep pilot-phase labs for R&D, yet final conformity is usually entrusted to external bodies whose certificates regulators and overseas buyers recognize. Network effects accrue to global majors running 25-plus sites nationwide, enabling one-stop assurance and uniform quality. Revised NABL rules further hobble smaller corporate labs, steering even conservative firms toward accredited outsourcers that can clear products for multiple jurisdictions in a single engagement.

List of Companies Covered in this Report:

- SGS India Pvt. Ltd.

- Bureau Veritas (India) Pvt. Ltd.

- Intertek India Pvt. Ltd.

- TUV SUD South Asia Pvt. Ltd.

- TUV Rheinland India Pvt. Ltd.

- UL India Pvt. Ltd.

- DNV Business Assurance India Pvt. Ltd.

- DEKRA Certification India Pvt. Ltd.

- Lloyd's Register Quality Assurance India Pvt. Ltd.

- IRClass Systems and Solutions Pvt. Ltd.

- Applus+ India Inspection Services Pvt. Ltd.

- Eurofins Analytical Services India Pvt. Ltd.

- ALS Testing Services India Pvt. Ltd.

- Mistras Group (India) Pvt. Ltd.

- Element Materials Technology India Pvt. Ltd.

- Kiwa Certification India Pvt. Ltd.

- QIMA Technical Services India Pvt. Ltd.

- TCR Engineering Services Pvt. Ltd.

- RINA India Pvt. Ltd.

- PONY Testing International Group India Pvt. Ltd.

- Velosi Certification Services India Pvt. Ltd.

- Vexil BPS Pvt. Ltd.

- ITS Testing Services (India) Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Regulatory Enforcement Across Indian Industries

- 4.2.2 Growing Outsourcing of TIC by Exporters and OEMs

- 4.2.3 Expansion of Consumer Goods and Retail Requiring Compliance

- 4.2.4 Rapid Growth of Life Sciences and Healthcare Sector

- 4.2.5 Digital Bharat Push Enabling Remote/AI-Driven Inspections

- 4.2.6 Surge in ESG-Linked Audits from Lenders and PE Investors

- 4.3 Market Restraints

- 4.3.1 Fragmented Lab Infrastructure and Inconsistent Quality

- 4.3.2 Shortage of Qualified Inspectors and Lab Analysts

- 4.3.3 Slow NABL/BIS Accreditation Turnaround Times

- 4.3.4 Price-Cutting by Unaccredited Local Labs Eroding Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Industry Vertical

- 5.3.1 Consumer Goods and Retail

- 5.3.2 ICT and Telecom

- 5.3.3 Automotive and Transportation

- 5.3.4 Aerospace and Defense

- 5.3.5 Oil, Gas and Petrochemicals

- 5.3.6 Energy and Utilities

- 5.3.7 Industrial Manufacturing and Machinery

- 5.3.8 Chemicals and Materials

- 5.3.9 Construction and Infrastructure

- 5.3.10 Life Sciences and Healthcare

- 5.3.11 Food, Agriculture and Beverage

- 5.3.12 Others Industry Verticals

- 5.4 By Mode of Service Delivery

- 5.4.1 On-site

- 5.4.2 Off-site / Laboratory

- 5.4.3 Remote / Digital

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SGS India Pvt. Ltd.

- 6.4.2 Bureau Veritas (India) Pvt. Ltd.

- 6.4.3 Intertek India Pvt. Ltd.

- 6.4.4 TUV SUD South Asia Pvt. Ltd.

- 6.4.5 TUV Rheinland India Pvt. Ltd.

- 6.4.6 UL India Pvt. Ltd.

- 6.4.7 DNV Business Assurance India Pvt. Ltd.

- 6.4.8 DEKRA Certification India Pvt. Ltd.

- 6.4.9 Lloyd's Register Quality Assurance India Pvt. Ltd.

- 6.4.10 IRClass Systems and Solutions Pvt. Ltd.

- 6.4.11 Applus+ India Inspection Services Pvt. Ltd.

- 6.4.12 Eurofins Analytical Services India Pvt. Ltd.

- 6.4.13 ALS Testing Services India Pvt. Ltd.

- 6.4.14 Mistras Group (India) Pvt. Ltd.

- 6.4.15 Element Materials Technology India Pvt. Ltd.

- 6.4.16 Kiwa Certification India Pvt. Ltd.

- 6.4.17 QIMA Technical Services India Pvt. Ltd.

- 6.4.18 TCR Engineering Services Pvt. Ltd.

- 6.4.19 RINA India Pvt. Ltd.

- 6.4.20 PONY Testing International Group India Pvt. Ltd.

- 6.4.21 Velosi Certification Services India Pvt. Ltd.

- 6.4.22 Vexil BPS Pvt. Ltd.

- 6.4.23 ITS Testing Services (India) Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment