|

시장보고서

상품코드

2063295

조광기 및 색변환 조명 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dimmer And Color Tunable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

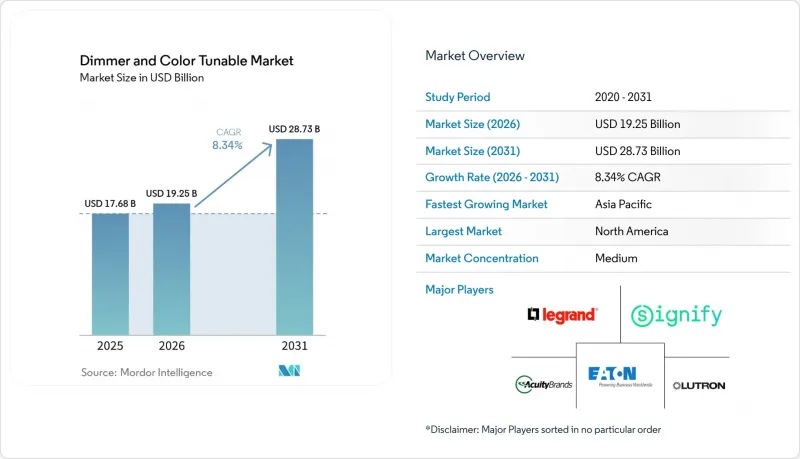

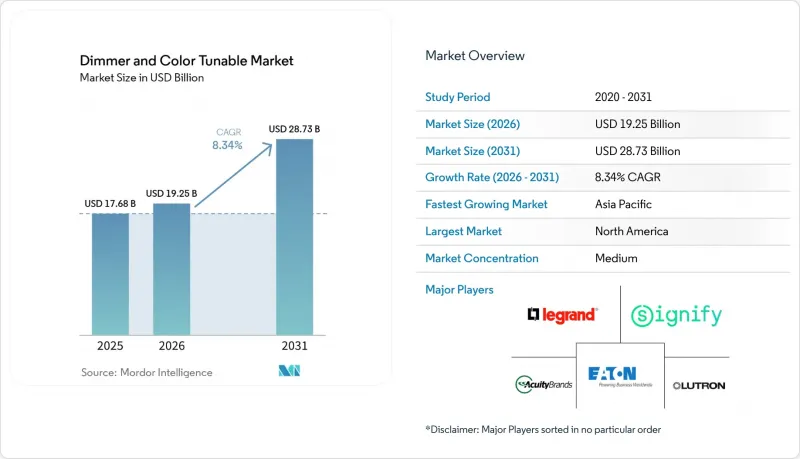

Mordor Intelligence에 의하면, 조광기 및 색변환 조명 시장 규모는 2025년에 176억 8,000만 달러로 평가되었습니다. 2026년에 192억 5,000만 달러에 달하고, 2031년까지 287억 3,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 8.34%를 나타낼 것으로 전망됩니다.

본 보고서는 제품 유형(로터리식, 슬라이드식, 비접촉식 등), 통신 기술(유선, 무선), 용도(주거, 상업용 사무실, 호텔·리조트, 소매, 실외·건축용 등), 판매 채널(신축 OEM, 리모델링, 온라인 소매, 전문 유통), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 조광기 및 색변환 조명 시장 동향과 인사이트

주택 개보수 프로젝트에서 LED의 급속한 보급

2024년, 미국 가정의 주거용 LED 소켓 보급률은 90%에 달했으나, 모든 조명 기구를 LED로 교체한 비율은 고작 37%에 그쳤으며, LED와 TRIAC 간의 플리커 문제를 해결하는 스마트 조광기에는 여전히 큰 개선 여지가 남아 있습니다. 음성 비서 스피커를 도입한 가정에서는 해당 기기를 사용하지 않는 가구에 비해 조광기 도입 속도가 2.3배 더 빠른 것으로 나타났으며, 생태계 간 호환성이 구매의 가장 큰 요인임이 확인되었습니다. 제조업체가 최소 부하에 대한 표시를 추가한 결과, 호환되지 않는 조광기와 관련된 보증 청구 건수가 2025년에 22% 감소했으며, 소비자의 신뢰도도 높아졌습니다. 2000년 이전에 지어진 오래된 주택에 리모델링 수요가 집중되고 있습니다. 이는 신축 주택에는 이미 최신 조광기에 대응하는 중성선이 설치되어 있기 때문입니다. 그 결과, 업그레이드 주기가 길어지면서 조광기 및 색조 조절이 가능한 조명 시장은 얼리 어답터층을 넘어 일반 DIY 채널로까지 확대되고 있습니다.

조명 제어 기능을 의무화하는 엄격한 건축 에너지 절약 기준 개정

2024년판 국제 에너지 절약 기준(IECC)은 5,000제곱피트를 초과하는 상업 공간에 대해 자동 조명 제어를 의무화하고 있으며, 이에 따라 미국 내 신규 사무실 건설의 5분의 4에 가까운 곳에서 실질적으로 연속 조광이 요구될 것입니다. 캘리포니아주 타이틀 24 파트 6은 주 전역에서 수요 반응형 조광을 의무화하고 있는 반면, 유럽연합(EU)의 최신 ‘건축물 에너지 성능에 관한 지침’은 자연광 활용 기준을 규정하고 있어, 프로젝트를 DALI-2 또는 0-10V 조광기 방식으로 이끌고 있습니다. 2028년에 제안된 개정안에 따르면, 수요 반응 제도의 적용 대상이 공동주택으로 확대되어, 조도 및 색조 조절이 가능한 시장에 연간 수천 세대가 추가될 전망입니다. ASHRAE 90.1 및 IEC 표준과의 규정 조화를 통해 전 세계 공급업체의 제품 개발에 대한 장벽이 완화됩니다. 장기적으로는 연속 조광이 건축의 표준 사양으로 자리 잡음에 따라, 규제에 따른 수요가 자발적인 개조 수요를 상회할 것으로 예측됩니다.

기존 TRIAC 인프라와 조광 가능 드라이버 간의 비호환성

2010년 이전의 위상 절단식 조광기는 조광이 가능한 백색 LED 드라이버와 결합할 경우, 귀에 들리는 윙윙거리는 소음이나 눈에 보이는 깜빡임을 발생시킵니다. 따라서 주택 소유자는 스위치와 조명 기구를 동시에 교체할 수밖에 없어, 방별 업그레이드 비용이 두 배로 늘어납니다. 미국의 오래된 건축물에서는 중성선이 없는 경우가 많아, 조명 기구 1대당 150-300달러의 배선 공사비가 추가로 발생하여 개보수 공사의 진행을 늦추고 있습니다. 배터리로 구동되는 하베스터는 배선 부족 문제를 해결해 주지만, 조광 범위에 제한이 있어 색조 조절이 가능한 대기 부하에는 대응할 수 없습니다. 호환성 데이터베이스에 따르면, 기존 TRIAC 모델 중 40% 미만만이 색상 조절이 가능한 LED에 적합하며, 이로 인해 소비자들의 혼란이 야기되고 있습니다. 이 문제는 신축 주택 증가에 따라 점차 해소될 것이지만, 당분간은 조광·조색기 시장에 중기적인 걸림돌이 될 것입니다.

부문별 분석

스마트 조광 스위치는 2025년 매출의 33.11%를 차지했습니다. 이는 주택 소유자들이 벽면에 설치할 공간을 확보할 수 있는 리모델링에 적합한 기기를 선호했기 때문입니다. 풀 컬러 RGB 모듈은 역동적인 색상 변화와 쇼핑객의 체류 시간을 연계하는 소매점에서의 도입에 힘입어 연평균 성장률(CAGR) 8.88%를 나타낼 것으로 전망됩니다. WELL 인증 획득을 목표로 하는 호텔 및 사무실 프로젝트에서는 조광이 가능한 백색 모듈이 2025년 시장 가치의 18.02%를 차지한 반면, 비용 효율을 중시하는 주택 건설 분야에서는 여전히 회전식 및 슬라이드식 조광기가 주류를 이루고 있습니다. 배터리 전원 방식의 제품이 중성선의 제약을 해소함에 따라, 스마트 스위치용 조광 및 색조 조절 시장 규모는 확대될 전망입니다. 한편, 허드슨 야즈와 같은 건축적 랜드마크는 RGB를 활용한 스토리텔링이 고가의 예산을 정당화할 수 있음을 입증하고 있으며, 조광기 및 색상 조절기 시장의 범위를 기능적인 조명을 넘어 확장시키고 있습니다.

다중 채널 LED 드라이버의 비용은 2023년 이후 25% 하락했으며, 이에 따라 조광이 가능한 백색 모듈과 RGB 모듈 간의 가격 차이가 줄어들면서 중규모 상업 프로젝트에서도 풀컬러 제어가 점차 보급되고 있습니다. 엄격한 위생 기준이 요구되는 의료 및 외식 산업에서는 비접촉식 조광기가 점차 보급되고 있지만, 이 틈새 시장 규모는 여전히 전체 시장 규모의 5% 미만에 그치고 있습니다. 플러그인식 램프 조광기나 인라인 코드 유닛은 특수한 장식 용도로 계속해서 사용되고 있습니다. 프리미엄 RGB 시스템이 주류 예산 범위에 포함됨에 따라, 원활한 설치 설정과 사전 설정된 색상 장면을 제공하는 업체들이 조광·색상 조절기 시장에서 점유율을 확대해 나갈 것입니다.

무선 기술은 2025년 예상 매출의 41.09%를 차지했으며, 이는 허브가 필요 없는 설치 솔루션에 대한 소비자의 선호도가 높아지고 있음을 보여줍니다. 이러한 추세는 원활하고 사용자 친화적인 스마트 홈 시스템에 대한 수요가 증가하고 있음을 반영하고 있습니다. Thread 및 Matter 솔루션은 주로 네이티브 IPv6의 이점에 힘입어 연평균 성장률(CAGR) 8.91%를 달성할 것으로 전망됩니다. 이는 싱글 허브 시스템으로 인해 발생하는 병목 현상을 효과적으로 해소하는 것입니다. Zigbee는 Philips Hue나 SmartThings 등의 생태계에서 초기 도입이 크게 뒷받침된 덕분에, 계속해서 도입 기반 측면에서 우위를 유지하고 있습니다. 그러나 플랫폼이 구형 무선 표준에 대한 지원을 단계적으로 중단함에 따라, 해당 시장 점유율은 서서히 감소하고 있으며, 이는 보다 진보된 기술로의 전환을 시사하고 있습니다. 유선 DALI-2는 상호 운용성과 비상 조명 규격 준수를 보장하는 IEC 62386-207 및 -209 규격을 충족한 점을 바탕으로, 상업용 매출의 22%를 차지했습니다.

위상 절단식 조광기는 오래된 주택에서는 여전히 널리 보급되어 있지만, 2011년 이후 건설된 미국 주택에서는 중성선이 표준으로 장착되기 때문에 그 시장 점유율은 감소할 것으로 예측됩니다. 블루투스 메시 기술은 특히 펌웨어 업데이트를 통해 게이트웨이 없이도 200노드 규모의 네트워크를 지원할 수 있게 된 이후, 부티크 호텔에서 큰 호응을 얻고 있습니다. 이러한 발전 덕분에 도입 시 부담이 대폭 줄어들어, 상업용 분야에서 더욱 매력적인 선택지가 되고 있습니다. Wi-Fi 지원 조광기는 설치가 용이하지만, 대기 시 전력 소비량이 많다는 점과 인구 밀도가 높은 공동주택에서 발생하는 네트워크 혼잡과 같은 과제에 직면해 있습니다. 인증 비용의 감소와 스마트폰 생태계에서 Matter 상태 표시기의 채택 확대에 따라, 조광 기능 및 색조 조절 기능을 갖춘 무선 제품 시장은 더욱 성장할 것으로 예측됩니다. 이러한 발전으로 인해 소비자의 구매 과정이 간소화되고, 무선 조명 솔루션의 보급이 전반적으로 촉진될 것으로 예측됩니다.

지역별 분석

북미는 캘리포니아주의 ‘Title 24’ 규제와 90%에 달하는 LED 보급률 덕분에 2025년 세계 시장 규모의 39.02%를 차지했습니다. 미국은 스마트 스피커를 도입한 1,400만 가구가 전국 평균의 2.3배에 달하는 비율로 조광기를 채택하고 있는 점에 힘입어, 해당 지역의 매출의 78%를 차지했습니다. 캐나다 수요는 온타리오주와 브리티시컬럼비아주에 집중되어 있으며, 이 지역에서는 스마트 조광기 비용의 최대 절반이 보조금으로 환급됩니다. 멕시코에서는 LED 보급률이 낮고, 스페인어로 제공되는 설치 관련 자료가 제한적이기 때문에 도입은 여전히 초기 단계에 머물러 있습니다.

아시아태평양은 사무실과 학교의 조도 조절 비율을 의무화하는 중국의 GB 50034-2024 규격에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.73%를 기록하며 성장할 것으로 전망됩니다. 지역별 매출 점유율에서는 중국이 압도적인 1위를 차지하고 있으며, 그 뒤를 일본이 따르고 있습니다. 일본에서는 고령화가 진행되고 있어, 상당수의 고령자 가구에서 음성 제어 조명의 도입이 확대되고 있습니다. 인도의 에너지 효율국은 조광이 가능한 LED에도 별점 평가 제도를 적용하여, 수백만 가구에 달하는 잠재 시장을 확대했습니다. 한국과 호주는 합쳐서 매출의 상당 부분을 차지하고 있으며, 특히 공공주택 개보수 공사에서 조광이 가능한 백색 LED 모듈이 채택되고 있다는 점이 주목됩니다.

유럽은 2025년 시장 규모에서 큰 점유율을 차지했으며, 이는 여러 공급업체 간의 상호 운용성을 보장하는 DALI-2 인증의 급격한 증가에 힘입은 결과입니다. 독일에서는 2025년에 주거용 조광기의 대대적인 교체를 촉진하기 위한 보조금 지원 대출 제도가 활용되었습니다. 영국의 ‘퓨처 홈스 스탠다드’는 향후 몇년내에 스마트 대응 배선을 의무화하게 될 것이며, 이는 브렉시트로 인한 관세 마찰의 영향을 상쇄하는 데 기여할 것입니다. 러시아는 부품 수입 규제로 인해 시장이 위축되었으나, 중동 및 아프리카는 NEOM과 같은 스마트시티 구상에 힘입어 전 세계 매출에 기여했습니다. 남미에서는 브라질과 아르헨티나가 주도적인 역할을 했으나, 통화 변동에 제약을 받아 2025년 시장 규모에서 차지하는 비중은 줄어들었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the dimmer and color tunable market size is expected to be USD 17.68 billion in 2025, USD 19.25 billion in 2026, and reach USD 28.73 billion by 2031, growing at a CAGR of 8.34% from 2026 to 2031.

This report is Segmented by Product Type (Rotary, Slide, Touchless, and More), Communication Technology (Wired, and Wireless), Application (Residential, Commercial Offices, Hospitality, Retail, Outdoor and Architectural, and More), Sales Channel (New Construction OEM, Retrofit, Online Retail, and Professional Distribution), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Dimmer And Color Tunable Market Trends and Insights

Rapid LED Penetration in Residential Retrofit Projects

Residential LED socket penetration hit 90% across United States households in 2024, yet just 37% of homes had converted every fixture, leaving a large upgrade pool for smart dimmers that solve LED-to-TRIAC flicker issues. Homes with voice-assistant speakers adopt dimmers 2.3 times faster than non-connected households, confirming that ecosystem compatibility is a first-order purchase trigger. Warranty claims tied to incompatible dimmers declined 22% in 2025 after manufacturers added minimum-load disclosures, improving consumer confidence. Older housing stock built before 2000 concentrates retrofit demand because newer homes already contain neutral wires that support modern dimmers. The resulting upgrade cycle expands the dimmer and color-tunable market beyond early adopters and into mainstream do-it-yourself channels.

Stringent Building Energy-Code Updates Mandating Controllable Lighting

The 2024 International Energy Conservation Code mandates automatic lighting controls for commercial spaces larger than 5,000 square feet, effectively requiring continuous dimming in nearly four-fifths of new U.S. office construction. California Title 24 Part 6 enforces demand-responsive dimming statewide, while the European Union's latest Energy Performance of Buildings Directive sets daylight-harvesting baselines that steer projects toward DALI-2 or 0-10 V dimmers. Proposed 2028 amendments will extend demand response to multifamily properties, adding thousands of units per year to the dimmer and color tunable market. Code harmonization with ASHRAE 90.1 and IEC standards reduces friction in product development for global suppliers. Over the long term, regulatory pull is expected to outpace voluntary retrofits as continuous dimming becomes a construction default.

Legacy TRIAC Infrastructure Incompatibility with Tunable Drivers

Pre-2010 phase-cut dimmers generate audible hum and visible flicker when paired with tunable-white LED drivers, forcing homeowners to replace switches and luminaires in tandem and doubling the cost of room-level upgrades. Neutral-wire absences in older U.S. construction add USD 150-300 per fixture to rewiring costs, slowing retrofits. Battery-powered harvesters mitigate wiring gaps but cap dimming range and cannot support color-tunable standby loads. Compatibility databases show that fewer than 40% of legacy TRIAC models are suitable for tunable LEDs, which increases consumer confusion. The issue will fade as new housing stock grows, yet it remains a medium-term drag on the dimmer and color-tunable market.

Other drivers and restraints analyzed in the detailed report include:

- Declining ASPs of Smart Dimmer ICs and Modules

- Pro-Lumen-Tunable Guidelines from WELL and LEED v4 Standards

- Fragmentation of Wireless Protocols Delaying Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart dimmer switches accounted for 33.11% of 2025 revenue, as homeowners favored retrofit-friendly devices that preserve wall-box footprints. Full-color RGB modules are forecast to grow at an 8.88% CAGR, supported by retail rollouts that link dynamic color shifts to shopper dwell times. Tunable-white modules accounted for 18.02% of the 2025 value in WELL-targeted hospitality and office projects, while rotary and slide dimmers remain prevalent in cost-sensitive residential construction. The dimmer and color-tunable market size for smart switches is poised to widen as battery-harvesting variants remove neutral-wire hurdles. Meanwhile, architectural landmarks such as Hudson Yards prove that RGB storytelling justifies premium budgets, expanding the dimmer-and-color-tunable market beyond functional lighting.

Cost declines for multi-channel LED drivers, down 25% since 2023, are compressing the price gap between tunable-white and RGB modules, democratizing full-color control for mid-tier commercial projects. Touchless dimmers gained traction in healthcare and food service under strict hygiene codes, although this niche remains below 5% of total value. Plug-in lamp dimmers and in-line cord units continue to serve specialty decor uses. As premium RGB systems migrate into mainstream budgets, vendors that offer seamless commissioning and pre-loaded color scenes will capture incremental market share in the dimmer- and color-tunable markets.

Wireless technologies accounted for 41.09% of the projected 2025 revenue, highlighting the growing consumer preference for hub-free installation solutions. This trend reflects the growing demand for seamless, user-friendly smart home systems. Thread and Matter solutions are forecast to achieve a compound annual growth rate (CAGR) of 8.91%, primarily driven by the advantages of native IPv6, which effectively eliminates the bottleneck caused by single-hub systems. Zigbee continues to dominate the installed base, largely driven by early adoption in ecosystems such as Philips Hue and SmartThings. However, its market share is gradually declining as platforms phase out support for legacy radios, signaling a shift toward more advanced technologies. Wired DALI-2 secured 22% of commercial revenue, benefiting from its compliance with IEC 62386-207 and -209 standards, which ensure interoperability and adherence to emergency-lighting codes.

Phase-cut dimmers remain prevalent in older homes; however, their market share is expected to decrease as neutral wires become a standard feature in U.S. housing constructed after 2011. Bluetooth Mesh technology has gained traction in boutique hotels, particularly after firmware updates enabled the support of 200-node networks without the need for gateways. This advancement has significantly reduced commissioning overhead, making it a more attractive option for commercial applications. Wi-Fi dimmers, while easy to install, face challenges such as higher standby power consumption and network congestion in densely populated apartment complexes. The market for dimmer and color-tunable wireless products is anticipated to grow further as certification costs decrease and smartphone ecosystems increasingly adopt Matter status indicators. These developments are expected to streamline the consumer purchase journey, enhancing the overall adoption of wireless lighting solutions.

Geography Analysis

North America controlled 39.02% of the 2025 global value, owing to California Title 24 and 90% LED penetration. The United States accounted for 78% of the region's revenue, aided by 14 million smart-speaker households adopting dimmers at 2.3 times the national rate. Canadian demand concentrates in Ontario and British Columbia, where incentives rebate up to half of smart-dimmer costs. Mexico's uptake remains nascent amid lower LED penetration and limited Spanish-language installation resources.

Asia-Pacific is projected to grow at an 8.73% CAGR through 2031, on the heels of China's GB 50034-2024 standard, which mandates dimming ratios in offices and schools. China dominates the regional revenue share, followed by Japan, where aging demographics are driving the adoption of voice-controlled lighting in a significant portion of senior households. India's Bureau of Energy Efficiency has extended star ratings to dimmable LEDs, expanding the addressable base across millions of households. South Korea and Australia collectively contribute a notable share of revenue, highlighted by public-housing retrofits that incorporate tunable-white modules.

Europe accounted for a significant share of the 2025 value, driven by a notable increase in DALI-2 certifications that guarantee multi-vendor interoperability. Germany leveraged subsidized loans that facilitated widespread residential dimmer upgrades during 2025. The United Kingdom's Future Homes Standard will mandate smart-ready wiring in the coming years, helping to offset Brexit-era tariff friction. Russia experienced a contraction due to component import curbs, while the Middle East and Africa contributed to global revenue, supported by smart-city blueprints like NEOM. South America, led by Brazil and Argentina, contributed a smaller share of the 2025 value, constrained by currency volatility.

- Lutron Electronics Co., Inc.

- Signify N.V.

- Legrand SA

- Leviton Manufacturing Co., Inc.

- Acuity Brands, Inc.

- Eaton Corporation plc

- Hubbell Incorporated

- Zumtobel Group AG

- ams-OSRAM AG

- Cree Lighting, A Company Of IDEAL INDUSTRIES, Inc.

- Savant Systems, Inc.

- Helvar Oy Ab

- Insteon Technologies LLC

- Jasco Products Company LLC

- Futronix Limited

- Casambi Technologies Oy

- RAB Lighting Inc.

- TCP International Holdings Ltd.

- MOSO Power Supply Technology Co., Ltd.

- LUTEC Lighting Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED Penetration in Residential Retrofit Projects

- 4.2.2 Stringent Building Energy-Code Updates Mandating Controllable Lighting

- 4.2.3 Declining ASPs of Smart Dimmer ICs and Modules

- 4.2.4 Pro-Lumen-Tunable Guidelines From WELL and LEED v4 Standards

- 4.2.5 Advances in Low-Voltage PoE Lighting Ecosystems

- 4.2.6 Hospitality Chains Pivot to Circadian-Lighting Guest Experiences

- 4.3 Market Restraints

- 4.3.1 Legacy TRIAC Infrastructure Incompatibility With Tunable Drivers

- 4.3.2 Fragmentation of Wireless Protocols Delaying Interoperability

- 4.3.3 Skilled-Installer Shortage in Emerging Economies

- 4.3.4 Supply-Chain Exposure to Silicon Carbide MOSFET Shortages

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors On The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Rotary Dimmer Switches

- 5.1.2 Slide Dimmer Switches

- 5.1.3 Touchless Dimmer Switches

- 5.1.4 Smart Dimmer Switches

- 5.1.5 Tunable White Modules

- 5.1.6 Full-Color RGB Tunable Modules

- 5.1.7 Other Product Type

- 5.2 By Communication Technology

- 5.2.1 Wired (0-10 V, DALI, Phase-Cut)

- 5.2.2 Wireless (Zigbee, Bluetooth Mesh, Wi-Fi, Thread And Matter)

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial Offices

- 5.3.3 Hospitality

- 5.3.4 Retail

- 5.3.5 Industrial

- 5.3.6 Outdoor And Architectural

- 5.3.7 Other Applications

- 5.4 By Sales Channel

- 5.4.1 New Construction OEM

- 5.4.2 Retrofit And Renovation

- 5.4.3 Online Retail

- 5.4.4 Professional Distribution / Wholesale

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East And Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products And Services, Recent Developments)

- 6.4.1 Lutron Electronics Co., Inc.

- 6.4.2 Signify N.V.

- 6.4.3 Legrand SA

- 6.4.4 Leviton Manufacturing Co., Inc.

- 6.4.5 Acuity Brands, Inc.

- 6.4.6 Eaton Corporation plc

- 6.4.7 Hubbell Incorporated

- 6.4.8 Zumtobel Group AG

- 6.4.9 ams-OSRAM AG

- 6.4.10 Cree Lighting, A Company Of IDEAL INDUSTRIES, Inc.

- 6.4.11 Savant Systems, Inc.

- 6.4.12 Helvar Oy Ab

- 6.4.13 Insteon Technologies LLC

- 6.4.14 Jasco Products Company LLC

- 6.4.15 Futronix Limited

- 6.4.16 Casambi Technologies Oy

- 6.4.17 RAB Lighting Inc.

- 6.4.18 TCP International Holdings Ltd.

- 6.4.19 MOSO Power Supply Technology Co., Ltd.

- 6.4.20 LUTEC Lighting Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment