|

시장보고서

상품코드

2063298

스마트 표면 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Smart Surfaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

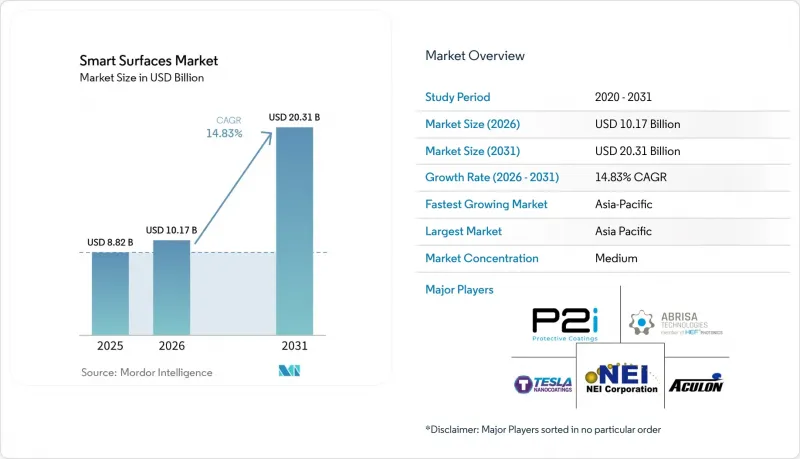

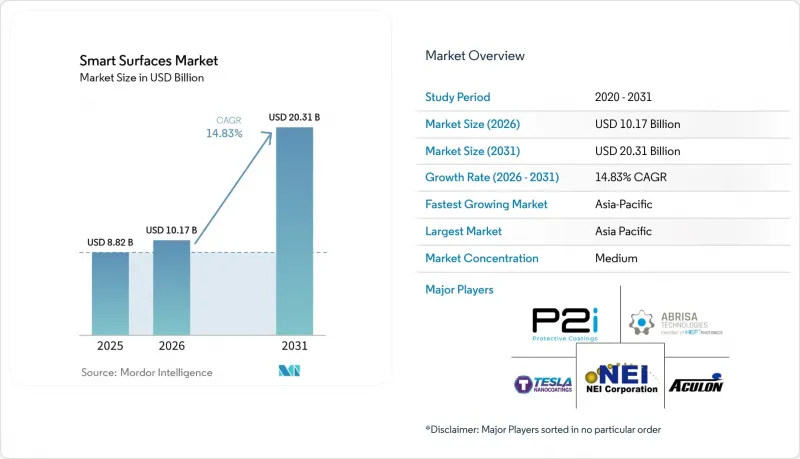

Mordor Intelligence에 의하면, 스마트 표면 시장 규모는 2025년에 88억 2,000만 달러로 평가되었습니다. 2026년 101억 7,000만 달러에서 2031년까지 203억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 14.83%를 나타낼 전망입니다.

본 보고서는 기능별(자가 세정, 자가 복원, 결빙 방지, 오염 방지 등), 소재별(폴리머, 금속 및 합금, 유리 및 세라믹 등), 기술별(물리 기상 증착(PVD), 화학 기상 증착(CVD), 졸-겔법 등), 최종 이용 산업(건축 및 건설, 에너지, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 스마트 표면 시장 동향과 인사이트

코로나19 이후 병원용 항균 표면에 대한 수요 급증

병원에서는 기존에 입원 환자의 7%에게 영향을 미치던 감염률을 낮추기 위해, 문손잡이, 침대 난간, 수술실 비품에 항균 코팅을 적용하고 있습니다. 클로르헥시딘이 결합된 스테인리스 스틸은 ISO 22196 프로토콜에 따라 2시간 이내에 메티실린 내성 황색포도상구균(MRSA)의 99.9%를 제거하며, 표면 열화 없이 병원체를 신속하게 사멸시키는 것을 우선으로 하는 조달 기준을 충족합니다. 물리 기상 증착법(PVD)을 통해 형성된 투명한 구리 필름은 디자인성을 해치지 않으면서도 덩어리 형태의 구리와 동등한 효과를 발휘하기 때문에 소아과 및 종양과 병동에서 채택이 확대되고 있습니다. 아연 기반 스프레이 코팅은 기존 설비에서 공구를 교체할 필요 없이 시공할 수 있기 때문에 외래 진료소에서 보급이 확대되고 있습니다. 유럽연합(EU)의 의료기기 규정에 따르면, 현재 소독용 물티슈로 1만 회 세척 주기를 거친 후에도 항균 효과가 지속되어야 하며, 가혹한 세척 조건에서도 효능을 유지하는 고성능 배합에 대한 수요가 높아지고 있습니다. 항균성 하이드로겔 인터페이스를 갖춘 무선 모니터링형 압력 센서는 2025년 12월에 임상시험을 시작했으며, 디지털 헬스와 표면 과학이 협력하여 감염 관리 프로토콜을 어떻게 재구축할 수 있는지 입증하고 있습니다.

자가 세정형 건축용 코팅의 보급 가속화

이산화티타늄(TiO2) 광촉매 코팅은 외벽 청소 빈도를 연간 1회에서 3년에 1회로 줄여주며, 상업용 부동산 소유주의 수명 주기 비용을 최대 40% 절감합니다. 2025년에 출시된 가시광선 활성화형은 그늘이 많은 도시 지역의 고층 빌딩군에서도 광촉매 작용을 발휘하여 대규모 개보수 시장을 개척하고 있습니다. 독일의 에너지 효율 기준인 ‘KfW 40 Plus’는 외단열 시스템에 자가 세정형 탑코트의 사용을 의무화하고 있어, 노후된 주택 재고를 개보수하는 건설업체들에게 규제 측면에서 큰 도움이 되고 있습니다. 유리 커튼월 표면에 코팅된 소수성 실리카 나노 입자는 150°가 넘는 물 접촉각을 구현하여, 경수로 인한 물때 부착이 우려되는 중동 도시에서 미네랄로 인한 얼룩 발생을 방지합니다. 태양광 발전 분야에서는 자가 세정층이 먼지 축적을 억제하여 패널 출력을 2-5% 향상시키고, 대규모 지상 설치형 어레이의 투자 회수 기간을 단축합니다. 계약 조항도 변화하고 있어, 건물 소유주가 정량화된 성능 보증을 요구하게 되었습니다. 이러한 변화로 인해 내구성과 세척 비용 절감을 입증할 수 있는 풍부한 데이터를 보유한 공급업체가 우대받고 있습니다.

엄격한 VOC 및 PFAS 규제가 불소계 화학물질의 사용을 제한하고 있습니다.

캘리포니아 주 의회 법안 제1817호에 따라, 2025년 1월부터 대부분의 코팅에서 퍼플루오로알킬 물질(PFAS) 및 폴리플루오로알킬 물질이 배제됨에 따라, 공급업체들은 지난 20년 동안 소수성 및 소유성 성능을 제공해 온 배합을 폐지할 수밖에 없게 되었습니다. 유럽화학물질청(ECHA)이 검토 중인 PFAS 금지 조치로 인해, 2027년까지 현재 스마트 표면용 화학물질의 15-20%가 시장에서 퇴출될 가능성이 있어, 긴급한 배합 변경이 시급합니다. 동시에, 미국 및 유럽의 휘발성 유기 화합물(VOC) 규제로 인해 용제 함유량이 1리터당 250그램으로 제한됨에 따라, 용제를 이용한 점도 조절에 의존하는 다기능 스택의 가공 조건이 더욱 까다로워지고 있습니다. 대형 OEM 제조업체들은 현재 구매 계약에 PFAS 회피 조항을 포함시키고 있어, 법적 기한보다 훨씬 앞서 기준을 충족하지 못하는 제품 시장 진입을 차단하고 있습니다. 불소 프리 시스템으로의 전환에는 제품 라인당 200만-500만 달러의 연구개발비가 추가로 소요되고, 상품화가 최대 2년 지연됨에 따라 단기적인 수익이 압박을 받고 있으며, 스마트 표면 시장 전체의 성장세가 둔화되고 있습니다.

부문별 분석

자가복구 코팅 시장은 2031년까지 연평균 성장률(CAGR) 15.63%로 확대되고 있으며, 자동차 및 항공우주 제조업체들이 미세한 균열을 자율적으로 봉합하는 마이크로캡슐 시스템을 도입함에 따라 스마트 표면 시장 전체보다 더 높은 성장세를 보이고 있습니다. 이러한 배합과 관련된 스마트 표면 시장 규모는 보증 기간이 표면의 무결성에 좌우되는 전기차 배터리 케이스나 항공기 복합재 패널 분야에서 가장 빠르게 확대되고 있습니다. 2025년 매출액에서 자가 세정층은 여전히 42.54%를 차지했으며, 유리 및 태양전지 모듈 위의 TiO₂ 광촉매 스택이 주류를 이루고 있습니다. 이를 통해 10년 동안 인건비를 30-40% 절감할 수 있습니다.

현재 의료 기관에서는 중환자실 전체에 항균 코팅 도입이 요구되고 있으며, ISO 22196 기준에 따라 99.9%의 병원체 살균 효과를 보이는 클로르헥시딘 결합 합금이나 투명 구리 필름이 활용되고 있습니다. 방빙 PDMS 층은 북유럽 풍력 터빈의 가동 중단 시간을 최대 50%까지 줄여주며, 방오 실리콘 시스템은 전 세계 선박에서 선체 저항을 5-10% 감소시키고 있습니다. 부식 방지 폴리아미드 나노 복합재는 연안 지역의 전기차 충전 설비의 수명을 약 3배로 연장하는 한편, 항공우주 프로그램에서는 우박 피해 복구를 목적으로 형상 기억 고분자의 평가가 진행되고 있습니다. 이러한 기능성 소재의 발전은 수익원의 다각화를 가져왔으며, 단일 용도에 의존하는 시장의 변동 위험으로부터 스마트 표면 시장을 안정화시키고 있습니다.

산화 그래핀이나 탄소나노튜브를 배합한 나노 복합재는 순수 수지에 비해 인장 강도를 최대 200% 향상시키고 열전도율을 5배 높이기 때문에 15.71%의 성장률을 보이고 있습니다. 2025년 수요의 34.11%는 폴리머가 차지했지만, 비용보다 임무 내구성이 우선시되는 의료용 임플란트나 방위용 항공기 구조물의 경우, 고성능 나노복합재가 폴리머를 대체해 가고 있습니다.

실리카 강화 폴리머는 150°가 넘는 물 접촉각을 실현하여, 경수 환경에서도 중동의 커튼월 표면에 오염이 달라붙지 않도록 합니다. 아연-니켈 합금판은 충전 커넥터를 갈바닉 부식으로부터 보호하며, 유리와 세라믹은 저반사 태양광 커버를 지지하여 모듈 효율을 2-5% 향상시킵니다. 클레이-플레이트렛 하이브리드는 산소 침투를 최대 60%까지 억제하여, 전 세계로 출하되는 전자 센서의 보관 기간을 연장합니다. 가격을 중시하는 건설업체들은 여전히 범용 아크릴 수지를 선호하고 있지만, 성능을 중시하는 구매자들은 나노 복합 소재 솔루션으로의 전환을 지속하고 있으며, 스마트 표면 시장에서 두 자릿수 성장을 유지하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 33.42%를 차지하며 가장 규모가 큰 지역 점유율을 기록했으며, 2031년까지 연평균 15.99%의 성장률을 보일 것으로 전망됩니다. 중국의 IMR Technology는 2025년부터 자동차 및 전자기기용 주문을 처리할 스프레이식 LbL 라인 구축을 위해 광둥성에 5억 5,100만 위안(7,600만 달러)을 투자했습니다. 인도는 의료기기용 코팅 시장 확대를 도모하기 위해 ‘생산 연계형 인센티브(PLI)’ 제도에 따라 3,420카롤 루피(4억 1,000만 달러)를 배정하여 국내 공급을 촉진하고 있습니다. 일본의 주요 전자 기업들은 증강현실(AR) 제품에 액정 엘라스토머 광학 소자를 도입하고 있으며, 이는 해당 지역의 혁신 수준을 여실히 보여주고 있습니다. 한국의 조선소들은 국제해사기구(IMO)의 트리부틸주석 금지 조치에 대응하기 위해 실리콘 방오 코팅을 도입하고 있으며, 호주의 광산 기업들은 해안 지역의 운송 트럭에 대해 부식 방지 처리를 의무화하고 있습니다.

북미와 유럽에서는 PFAS의 단계적 폐지를 염두에 두고 제품 포트폴리오 재검토가 진행되고 있습니다. 캘리포니아주의 2025년 금지 조치로 인해 제품의 즉각적인 전환이 시급한 상황이며, 유럽화학물질청(ECHA)의 규제안에 따라 그 일정은 더욱 엄격해지고 있습니다. Horizon Europe의 400만 유로(440만 달러) 규모의 SafeTouch 보조금은 대중교통 수단 표면용 항균 기술 개발을 가속화하고 있는 반면, 독일의 KfW 40 Plus 기준에 따르면, 현재 건설 활동의 60%를 차지하는 리모델링 공사에서 자가 세정 기능을 갖춘 탑코트의 사용이 의무화되어 있습니다. 미국 에너지부의 50억 달러 규모의 충전소 예산에는 15년간의 염수 분무 시험 요건이 포함되어 있어, 부식 방지 스택에 대한 예측 가능한 수요를 창출하고 있습니다.

중동 및 아프리카와 남미에서는 관련 시장의 확대가 예상됩니다. 사우디아라비아와 아랍에미리트에서는 먼지로 인한 월간 5-10%의 효율 저하를 막기 위해 자가 세척형 태양광 모듈이 요구되고 있습니다. 남아프리카의 광산 운영사는 내마모성 코팅을 통해 설비의 가동 시간을 3배로 연장한 반면, 브라질의 해상 플랫폼에서는 혹독한 대서양 해수로 인해 연간 0.5-1.5mm씩 발생하는 강재 부식을 견디기 위해 방식·방오 패키지가 채택되고 있습니다. 아르헨티나의 농업 기계 제조업체는 수확기에 자가 세척 코팅을 적용함으로써, 성수기의 처리 능력을 10-15% 향상시키고 있습니다. 이러한 노력들이 어우러져 전 세계 스마트 표면 시장의 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the smart surfaces market size was valued at USD 8.82 billion in 2025 and estimated to grow from USD 10.17 billion in 2026 to reach USD 20.31 billion by 2031, at a CAGR of 14.83% during the forecast period (2026-2031).

This report is Segmented by Functionality (Self-Cleaning, Self-Healing, Anti-Icing, Anti-Fouling, and More), Material (Polymers, Metals and Alloys, Glass and Ceramics, and More), Technology (Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), Sol-Gel, and More), End-Use Industry (Building and Construction, Energy, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Surfaces Market Trends and Insights

Surge In Demand for Anti-Microbial Hospital Surfaces Post-COVID-19

Hospitals are embedding anti-microbial layers into door handles, bed rails, and operating room fixtures to cut infection rates that historically affected 7% of in-patients. Chlorhexidine-bonded stainless steel removes 99.9% of methicillin-resistant Staphylococcus aureus under ISO 22196 protocols within two hours, meeting procurement criteria that prioritize rapid pathogen kill without surface degradation. Transparent copper films deposited by physical vapor deposition (PVD) preserve design aesthetics while matching the efficacy of bulk copper, widening adoption in pediatric and oncology wards. Zinc-based spray coatings are scaling in outpatient clinics because existing architectural equipment can apply them without retooling. The European Union's Medical Device Regulation now requires anti-microbial durability after 10,000 disinfectant wipe cycles, funneling demand toward high-end formulations that maintain efficacy under harsh cleaning. Wirelessly monitored pressure sensors with anti-microbial hydrogel interfaces entered clinical trials in December 2025, demonstrating how digital health and surface science together reshape infection-control protocols.

Accelerating Adoption of Self-Cleaning Architectural Coatings

Titanium-dioxide (TiO2) photocatalytic coatings reduce facade-cleaning frequency from yearly to once every three years, trimming lifecycle costs by up to 40% for commercial real-estate owners. Visible-light activated variants launched in 2025 extend photocatalysis into shaded urban canyons, unlocking dense retrofit markets. Germany's KfW 40 Plus energy-efficiency standard mandates self-cleaning topcoats on external insulation systems, securing a regulatory pull for builders renovating aging housing stock. Hydrophobic silica nanoparticles on glass curtain walls reach water-contact angles above 150°, preventing mineral spotting in Middle Eastern cities prone to hard-water deposits. In the solar sector, self-cleaning layers curb dust build-up, elevating panel output by 2-5% and shortening payback periods on large ground-mount arrays. Contract language is evolving, with building owners requesting quantified performance guarantees, a shift that rewards data-rich suppliers able to certify durability and cleaning cost reductions.

Stringent VOC And PFAS Regulations Constraining Fluorinated Chemistries

California's Assembly Bill 1817 removed per- and polyfluoroalkyl substances from most coatings beginning January 2025, compelling suppliers to retire formulations that delivered hydrophobic and oleophobic performance for two decades. The European Chemicals Agency's pending PFAS ban could eliminate 15-20% of current smart-surface chemistries by 2027, triggering emergency reformulation. At the same time, United States and European volatile-organic-compound caps restrict solvent content to 250 grams per liter, tightening the processing window for multi-functional stacks that depend on solvent-borne viscosity control. Large original-equipment manufacturers now embed PFAS-avoidance clauses into purchase contracts, blocking market entry for non-compliant products well ahead of legal deadlines. Transitioning to fluorine-free systems adds USD 2-5 million of R&D per product line and delays commercialization by up to two years, constraining near-term revenue and slowing the overall smart surfaces market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of EV Charging Infrastructure Requiring Anti-Corrosion Surfaces

- Government Incentives for Ice-Phobic Coatings in Wind Turbines

- High Fabrication Costs of Multi-Functional Nano-Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-healing coatings are advancing at a 15.63% CAGR through 2031, outperforming the overall smart surfaces market as automotive and aerospace builders integrate microcapsule systems that autonomously seal micro-cracks. The smart surfaces market size tied to these formulations is rising fastest in electric-vehicle battery enclosures and aircraft composite panels, were warranty cycles hinge on surface integrity. Self-cleaning layers still commanded 42.54% of 2025 revenue, dominated by TiO2 photocatalytic stacks on glass and solar modules that reduce labor costs 30-40% over a decade.

Healthcare operators now specify anti-microbial coatings across intensive-care units, leveraging chlorhexidine-bonded alloys and transparent copper films that demonstrate 99.9% pathogen kill under ISO 22196. Anti-icing PDMS layers cut Nordic wind-turbine downtime by up to 50%, and anti-fouling silicone systems lower hull drag 5-10% for global shipping fleets. Anti-corrosion polyamide nanocomposites nearly triple the service life of coastal EV charging gear, while aerospace programs evaluate shape-memory polymers for hail-damage recovery. Collectively, these functional pathways diversify revenue and stabilize the smart surfaces market against single-application volatility.

Nanocomposites built with graphene oxide or carbon nanotubes are growing at 15.71% because they amplify tensile strength by up to 200% and boost thermal conductivity fivefold relative to neat resins. Although polymers retained 34.11% of 2025 demand, high-performance nanocomposites are displacing them in medical implants and defense aerostructures, where cost is secondary to mission durability.

Silica-reinforced polymers achieve water-contact angles above 150°, keeping Middle Eastern curtain walls free of staining despite hard-water conditions. Zinc-nickel metal plates seal charging connectors against galvanic attack, while glass and ceramics underpin low-reflection solar covers that lift module efficiency by 2-5%. Clay-platelet hybrids slow oxygen ingress by up to 60%, extending shelf life for electronic sensors shipped worldwide. Price-sensitive builders still default to commodity acrylics, but performance-driven buyers continue migrating toward nanocomposite solutions, sustaining double-digit growth within the smart surfaces market.

Geography Analysis

Asia-Pacific posted the largest regional footprint at 33.42% of 2025 revenue and is forecast to grow at 15.99% through 2031. China's IMR Technology invested CNY 551 million (USD 76 million) in Guangdong for spray-based LbL lines that support automotive and electronics orders beginning 2025. India earmarked INR 3,420 crore (USD 410 million) under its Production Linked Incentive scheme to scale medical-device coatings, catalyzing domestic supply. Japan's electronics leaders deploy liquid-crystal elastomer optics in augmented-reality products, highlighting the region's innovation depth. South Korean shipyards implement silicone foul-release layers to meet International Maritime Organization bans on tributyltin, and Australia's miners specify anti-corrosion treatments for coastal haul trucks.

North America and Europe are recalibrating portfolios around PFAS phase-outs. California's 2025 ban forces immediate product changeovers, and the European Chemicals Agency's restriction proposal tightens timelines further. Horizon Europe's EUR 4 million (USD 4.4 million) SafeTouch grant accelerates anti-microbial transit surfaces, while Germany's KfW 40 Plus standard mandates self-cleaning topcoats on retrofits that make up 60% of current construction activity. The United States Department of Energy's USD 5 billion charging-station budget embeds 15-year salt-spray requirements, creating predictable pull for anti-corrosion stacks.

The Middle East, Africa, and South America present rising adjacencies. Saudi Arabia and the United Arab Emirates demand self-cleaning solar modules to stem 5-10% monthly efficiency loss from dust. South African mining operators extend equipment uptime threefold with wear-resistant coatings, while Brazil's offshore platforms adopt anti-corrosion and anti-fouling packages to withstand 0.5-1.5 mm annual steel loss in aggressive Atlantic waters. Argentina's farm machinery makers spray self-cleaning layers on harvesters, raising throughput 10-15% during peak season. Collectively, these initiatives sustain the global spread of the smart surfaces market.

- P2i Limited

- Aculon, Inc.

- NEI Corporation

- Tesla NanoCoatings, Inc.

- DryWired Defense Technologies, LLC

- Abrisa Technologies

- NanoSonic, Inc.

- Surfactis Technologies SAS

- Nanofilm Technologies International Limited

- Hydromer, Inc.

- Plasmatreat GmbH

- XPEL, Inc.

- Ultratech International, Inc.

- PermaShield Surface Solutions, Inc.

- Nano-Care Deutschland AG

- Bio-Gate AG

- ACTnano, Inc.

- Imagine Intelligent Materials Pty Ltd

- Nano4Life Europe L.P.

- Hexis S.A.S.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Adoption of Self-Cleaning Architectural Coatings

- 4.2.2 Surge in Demand for Anti-Microbial Hospital Surfaces Post-COVID-19

- 4.2.3 Government Incentives for Ice-Phobic Coatings in Wind Turbines

- 4.2.4 Rapid Expansion of EV Charging Infrastructure Requiring Anti-Corrosion Surfaces

- 4.2.5 Emergence of Smart-Surface Enabled Adaptive Optics in AR/VR Headsets

- 4.2.6 Defense Funding for Radar-Stealth Nano-Textured Skins

- 4.3 Market Restraints

- 4.3.1 High Fabrication Costs of Multi-Functional Nano-Coatings

- 4.3.2 Limited Long-Term Durability Data Under Real-World Conditions

- 4.3.3 Stringent VOC and PFAS Regulations Constraining Fluorinated Chemistries

- 4.3.4 Scale-Up Bottlenecks for Layer-by-Layer Assembly Processes

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Functionality

- 5.1.1 Self-Cleaning

- 5.1.2 Self-Healing

- 5.1.3 Anti-Icing

- 5.1.4 Anti-Fouling

- 5.1.5 Anti-Corrosion

- 5.1.6 Anti-Microbial

- 5.1.7 Other Functionality

- 5.2 By Material

- 5.2.1 Polymers

- 5.2.2 Metals and Alloys

- 5.2.3 Glass and Ceramics

- 5.2.4 Nanocomposites

- 5.2.5 Other Material

- 5.3 By Technology

- 5.3.1 Physical Vapor Deposition (PVD)

- 5.3.2 Chemical Vapor Deposition (CVD)

- 5.3.3 Sol-Gel

- 5.3.4 Layer-by-Layer Assembly

- 5.3.5 Spray Coating

- 5.3.6 Micro/Nano-Texturing

- 5.3.7 Other Technology

- 5.4 By End-Use Industry

- 5.4.1 Building and Construction

- 5.4.2 Automotive and Transportation

- 5.4.3 Medical and Healthcare

- 5.4.4 Electronics and Consumer Devices

- 5.4.5 Energy (Solar and Wind)

- 5.4.6 Maritime and Aerospace

- 5.4.7 Industrial Machinery

- 5.4.8 Other End-Use Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 P2i Limited

- 6.4.2 Aculon, Inc.

- 6.4.3 NEI Corporation

- 6.4.4 Tesla NanoCoatings, Inc.

- 6.4.5 DryWired Defense Technologies, LLC

- 6.4.6 Abrisa Technologies

- 6.4.7 NanoSonic, Inc.

- 6.4.8 Surfactis Technologies SAS

- 6.4.9 Nanofilm Technologies International Limited

- 6.4.10 Hydromer, Inc.

- 6.4.11 Plasmatreat GmbH

- 6.4.12 XPEL, Inc.

- 6.4.13 Ultratech International, Inc.

- 6.4.14 PermaShield Surface Solutions, Inc.

- 6.4.15 Nano-Care Deutschland AG

- 6.4.16 Bio-Gate AG

- 6.4.17 ACTnano, Inc.

- 6.4.18 Imagine Intelligent Materials Pty Ltd

- 6.4.19 Nano4Life Europe L.P.

- 6.4.20 Hexis S.A.S.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment