|

시장보고서

상품코드

2063328

센싱 케이블 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Sensing Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

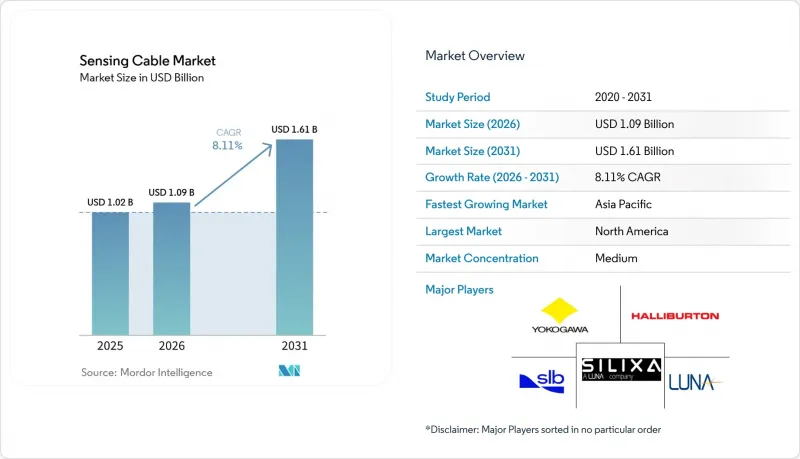

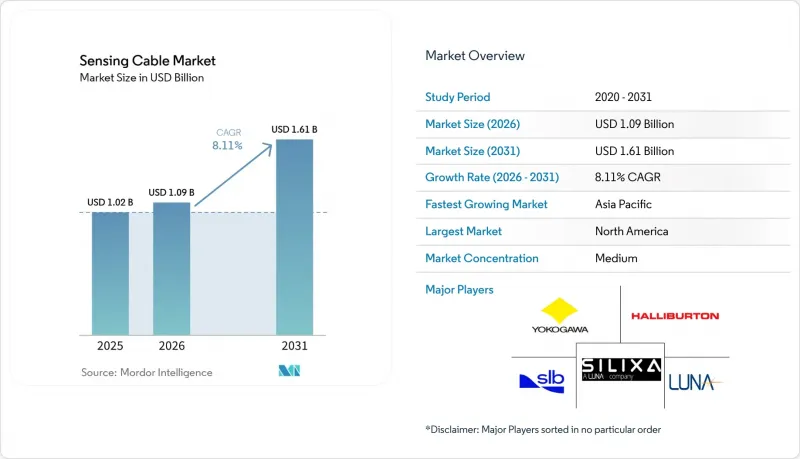

Mordor Intelligence에 의하면, 센싱 케이블 시장 규모는 2025년에 10억 2,000만 달러로 평가되었습니다. 2026년 10억 9,000만 달러에서 2031년까지 16억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.11%를 나타낼 전망입니다.

본 보고서는 케이블 유형(광섬유 센싱 케이블, 전기/동축 센싱 케이블, 기타), 센싱 기술(분산형 변형/압력 센싱, 기타), 용도(구조물 건전성 및 지반 모니터링, 기타), 최종 사용자 산업(석유 및 가스, 전력 및 유틸리티, 국방·보안, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 센싱 케이블 시장 동향 및 분석

비전통적 자원 분야에서 분산형 광섬유 센싱 기술의 도입 확대

영구적인 광섬유 스트링을 통해 셰일 시추 업체는 파쇄 단계의 성능과 저류층의 유량을 실시간으로 파악할 수 있어, 비생산 시간을 줄이고 회수율을 높일 수 있습니다. 할리버튼사의 베어 파이버 개입 기술에 관한 2025년 라이선스는 사업자가 펌프 작동을 중단하지 않고도 자극 처리 중에 파이버를 스풀링할 수 있음을 입증했습니다. 주기적인 굴절률 변조를 가하는 증산란 광섬유는 신호 대 잡음비를 15dB 개선하고, 단일 인터로게이터를 사용한 도달 거리를 50km 이상으로 연장하며, 하드웨어의 수를 줄여줍니다. 중동의 국영 석유 회사들은 탄산염암의 불균일성으로 인해 유체가 가려지는 장거리 유정에 대해서도 유사한 모니터링을 요구하고 있으며, 이를 통해 센싱 케이블 시장을 확대할 다년 계약을 체결했습니다.

위험물 파이프라인에 대한 누출 감지 의무화 규정

미국 파이프라인 위험물 안전국(PHMSA)은 현재 액체 수송 라인 운영 사업자에게 엄격한 시간 및 유량 범위 내에서 누출을 감지할 것을 의무화하고 있으며, API RP 1130에서는 분산형 광섬유 감지 기술이 적합 기술로 지정되어 있습니다. 유럽에서는 세베소 III 지침에 따라 적용 범위가 화학물질 운송 경로까지 확대됨에 따라 노후화된 운송 노선의 개보수가 촉진되고 있습니다. 2025년에 AP Sensing이 수행한 1,300km에 달하는 BRUA 프로젝트에서는 규제 요건을 충족하는 1km 이하의 정확도로 누출 위치를 특정하는 것이 입증되었으며, 동시에 사고 보고용 상세 데이터도 제공되었습니다. 연속적인 광섬유 커버리지로 인해 사각지대가 제거됨에 따라, 사업자들은 정기적인 항공 조사를 대체하는 속도를 높이고 있으며, 이에 따라 센싱 케이블 시장은 일반적인 예산 주기에 점차 임베디드되고 있습니다.

장거리 운용 시 높은 인터로게이터 단가

대당 5만-20만 달러에 달하는 인터로게이터의 가격대는 자금 사정에 어려움을 겪고 있는 유틸리티체나 중견 기업들에게 수백 킬로미터에 걸친 광범위한 설치를 주저하게 만드는 요인이 되고 있습니다. AP Sensing은 2025년에 300km의 해저 커버리지를 달성했으나, 이러한 성과를 뒷받침한 코히런트 레이리 레이저와 저잡음 검출기는 설비 투자 예산을 부풀리고 있습니다. 매니지드 서비스 모델은 사용자 간에 비용을 분담하는 것을 목표로 하고 있지만, 이를 실현하기 위해서는 대부분의 지역이 보유하고 있지 않은 고밀도 자산 회랑이 필요합니다. 실리콘 포토닉스의 시제품은 웨이퍼 단위 가격 하락을 시사하고 있지만, 상용화까지는 아직 2년이 더 걸릴 전망입니다. 그 전까지는 고액의 초기 비용이 신흥 시장에서의 도입을 저해하여, 전 세계 센싱 케이블 시장의 성장 궤도를 제한하게 될 것입니다.

부문별 분석

2025년 기준으로 광섬유 부문에 대한 지출은 센싱 케이블 시장 점유율의 51.78%를 차지했으나, 160°C를 넘어도 투명성을 유지하는 퍼플루오로화 그라데이션 인덱스 코어의 성장에 힘입어 폴리머 광섬유 시장은 연평균 성장률(CAGR) 9.06%를 나타낼 것으로 전망됩니다. 정유시설 및 화학 플랜트가 전자기 간섭의 영향을 받지 않는 솔루션을 모색하는 가운데, 폴리머계 센싱 케이블 시장은 새로운 전성기를 맞이하려 하고 있습니다. 실리카계 케이블은 0.2dB/km의 감쇠로 인해 100km를 초과하는 단일 인터로게이터 스팬이 가능하기 때문에 장거리 자산 분야에서 여전히 주류를 이루고 있습니다.

원격 노드에 전력망으로부터의 전력 공급이 없는 해상 풍력 발전소에서는 전력과 광섬유를 결합한 하이브리드 구조가 등장하고 있습니다. 기존 화재 감지 루프의 개보수 공사에서는 여전히 전기 케이블이나 동축 케이블이 주류를 이루고 있지만, 비용 격차가 줄어들고 할로겐계 피복이 금지됨에 따라 구매자들은 광섬유로 대체해 나가고 있습니다. TOPAS 및 CYTOP 코어를 실험적으로 도입하는 제조업체들은 효율을 점진적으로 향상시키고 있는 반면, PFAS가 포함되지 않은 클래드는 유럽에서 다가오고 있는 화학물질 규제에 대응하고 있습니다. 재료 과학이 발전함에 따라, 센싱 케이블 시장에서는 열적, 화학적, 기계적 내구성을 용도별 요구 사항에 맞춘 더욱 폭넓은 제품군이 받아들여지고 있습니다.

분산형 온도 감지 기술은 2025년 매출의 43.12%를 차지하며, 파이프라인 및 전력 케이블의 상태 관리 프로그램에서 이 기술의 중요성을 부각시킨 반면, 분산형 음향 감지 기술은 연평균 성장률(CAGR) 9.09%를 기록하며 모든 경쟁 제품을 능가하는 성장이 예상됩니다. 이 음향 시스템은 코히런트 레이리 후방 산란을 분석하여 킬로헤르츠 단위의 진동 정보를 제공함으로써, 침입, 누출, 지진 진동을 실시간으로 감지합니다. 엣지 AI가 원시 데이터의 대역폭을 줄이고 네트워크 통합 비용을 절감함에 따라, 음향 플랫폼용 센싱 케이블 시장은 확대되고 있습니다.

다중 파라미터 측정 장치는 라만, 브릴루앙, 레이리 채널을 결합하여 중요 인프라의 종합적인 가시화를 실현하지만, 그 가격은 30만 달러를 초과합니다. 해양 관측소에서는 이미 해저 지진 지도를 작성하기 위해 900km가 넘는 음향 케이블을 활용하고 있습니다. 예측 기간 동안 통합형 온도·진동 센서가 중규모 파이프라인에도 보급됨에 따라, 센싱 케이블 시장 점유율 구성은 범용성이 높은 음향 주도형 번들 쪽으로 유리하게 기울어질 것으로 보입니다.

지역별 분석

아시아태평양은 일본의 지진 모니터링, 중국의 파이프라인 안전 대책 강화, 인도의 인재 양성 프로그램에 힘입어 2025년 매출의 31.73%를 차지했습니다. 이 지역의 센싱 케이블 시장은 실시간 열 모니터링이 필요한 고압(HV) 및 통신 회선을 대도시권에서 점점 더 많이 지하화함에 따라 성장하고 있습니다. 일본의 관련 기관들은 쓰가루·난카이 해저 케이블에 감지기를 설치하여, 국가적 재난 대책으로서 광섬유 센싱의 유효성을 입증하는 고밀도 지진 경보 네트워크를 구축하고 있습니다.

북미는 PHMSA(미국 파이프라인 위험물 안전국)의 규제에 따라 액체 수송 라인에서 분산형 감지 방식이 표준 관행으로 자리 잡으면서 약 28%의 점유율을 차지했습니다. 버지니아주와 텍사스주에서 진행 중인 하이퍼스케일 시설 건설로 인해 화재 감지 루프 업그레이드에 필요한 수주가 증가하는 한편, ‘Digital 395’ 프로젝트에서는 통신용 광섬유를 지진 모니터링과 네트워크 서비스 양쪽에 활용하는 사례가 제시되었습니다. 캐나다의 오일샌드에서는 열 모니터링이 계속되고 있지만, 자본 규율로 인해 그 속도는 둔화되고 있습니다. 멕시코에서는 예산 제약으로 인해 자본 리스크를 흡수하는 ‘센싱-어-서비스(Sensing-as-a-Service)’ 제공업체들이 주목을 받고 있으며, 이는 센싱 케이블 시장에서 서비스 주도형으로의 전환을 시사하고 있습니다.

유럽은 매출의 약 24%를 차지했으며, 연속 온도 감지 기능이 탑재된 해저 HVDC 링크가 이를 뒷받침하고 있습니다. NKT의 20억 유로(21억 6,000만 달러) 규모의 SSEN 송전 계약에서는 광섬유가 내장된 525kV 케이블이 채택되었으며, 이는 북해의 전기화에 활용된 해당 지역의 노력을 여실히 보여주고 있습니다. 중동은 연평균 성장률(CAGR) 9.21%를 기록하며 가장 빠르게 성장하고 있으며, Ducab의 고전압용 광섬유 제품과 국영 석유 회사의 도입 의무화가 보급을 주도하고 있습니다. 한편, 정책상의 미비점이나 자금 부족으로 인해 남미와 아프리카의 대부분 지역에서는 보급률이 5% 이하에 그치고 있지만, 브라질 연안 유전에서의 도입 프로그램은 센서 비용이 낮아지면 잠재적인 가능성이 있음을 시사하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the sensing cable market size was valued at USD 1.02 billion in 2025 and estimated to grow from USD 1.09 billion in 2026 to reach USD 1.61 billion by 2031, at a CAGR of 8.11% during the forecast period (2026-2031).

This report is Segmented by Cable Type (Fiber-Optic Sensing Cables, Electrical/Coaxial Sensing Cables, and More), Sensing Technology (Distributed Strain/Pressure Sensing, and More), Application (Structural Health and Geotechnical Monitoring, and More), End-User Industry (Oil and Gas, Power and Utilities, Defense and Security, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Sensing Cable Market Trends and Insights

Rising Deployment of Distributed Fiber-Optic Sensing in Unconventionals

Permanent fiber strings let shale drillers visualize frac-stage performance and reservoir flow in real time, trimming non-productive time and boosting recovery factors. Halliburton's 2025 license for bare-fiber intervention technology demonstrated that operators could spool fibers during stimulation without halting pumping operations. Enhanced-scattering fibers that add periodic refractive-index modulation improve signal-to-noise by 15 dB, extend single-interrogator reach beyond 50 km, and reduce hardware count. National oil companies in the Middle East demand similar surveillance for extended-reach wells, where carbonate heterogeneity masks flow, locking in multi-year orders that expand the sensing cable market.

Mandatory Leak-Detection Regulations for Hazardous Pipelines

The U.S. Pipeline and Hazardous Materials Safety Administration now compels liquid-line operators to spot leaks within tight time and volume windows, and API RP 1130 names distributed fiber sensing as a compliant method. In Europe, the Seveso III Directive widens the net to chemical corridors, prodding retrofits of aging transmission lines. AP Sensing's 1,300 km BRUA project in 2025 demonstrated sub-kilometer localization that meets regulatory requirements while providing forensic data for incident reporting. Because continuous fiber coverage removes blind spots, operators accelerate replacement of periodic flyovers, nudging the sensing cable market into routine budget cycles.

High Interrogator-Unit Cost for Long-Reach Deployments

Price tags between USD 50,000 and USD 200,000 per interrogator deter cash-strapped utilities and midstream firms from blanketing hundreds of kilometers. AP Sensing delivered 300 km submarine coverage in 2025, but the coherent Rayleigh lasers and low-noise detectors behind that feat inflate capital budgets. Managed service models aim to amortize costs across users but require dense asset corridors that few regions possess. Silicon-photonics prototypes hint at wafer-scale price breaks, though commercial launches remain two years away. Until then, high upfront costs temper emerging-market adoption and cap the global sensing cable market's trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI Analytics Lowers OPEX and False Alarms

- Adoption of Passive Fire-Detection Cables in Hyperscale Data Centers

- Scarcity of Trained Fiber-Optic Installation Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spending on fiber-optic formats accounted for 51.78% of the sensing cable market share in 2025, yet polymer optical fibers are forecast to grow at a 9.06% CAGR, driven by perfluorinated graded-index cores that remain transparent beyond 160 °C. The sensing cable market for polymer lines is poised to reach new heights as refiners and chemical plants seek solutions immune to electromagnetic interference. Silica-based cables still dominate long-haul assets because 0.2 dB/km attenuation enables single-interrogator spans over 100 km.

Hybrid power-plus-fiber constructions emerge for offshore wind farms where remote nodes lack grid feeds. Electrical and coaxial forms persist in legacy fire-loop retrofits, but shrinking cost differentials and the ban on halogenated jackets are pushing buyers toward fiber alternatives. Manufacturers experimenting with TOPAS and CYTOP cores drive incremental efficiency gains, while PFAS-free claddings address looming European chemical restrictions. As material science evolves, the sensing cable market welcomes a broader portfolio that aligns thermal, chemical, and mechanical resilience with application-specific needs.

Distributed temperature sensing accounted for 43.12% of 2025 revenue, underscoring its role in pipeline and power-cable health programs, yet distributed acoustic sensing is projected to outgrow all rivals at a 9.09% CAGR. Acoustic systems parse coherent Rayleigh backscatter to deliver kilohertz-rate vibration insights that spot intrusions, leaks, and seismic tremors in real time. The sensing cable market for acoustic platforms grows as edge AI reduces raw-data bandwidth, easing network integration costs.

Multi-parameter interrogators combine Raman, Brillouin, and Rayleigh channels, yielding holistic visibility for critical infrastructure but ringing in at price points above USD 300,000. Ocean observatories already harness acoustic spans longer than 900 km for subsea quake mapping. Over the forecast window, integrated temperature-vibration packages will filter down to mid-tier pipelines, tilting the sensing cable market share mix in favor of versatile acoustic-led bundles.

Geography Analysis

Asia-Pacific anchored 31.73% of 2025 revenue, underpinned by seismic monitoring in Japan, pipeline safety upgrades in China, and workforce acceleration programs in India. The sensing cable market in the region is growing as megacities bury more HV and telecom lines that require real-time thermal supervision. Japanese agencies mount interrogators on the Tsugaru and Nankai submarine cables, weaving a dense quake-alert net that validates fiber sensing for national disaster readiness.

North America held a roughly 28% share as PHMSA mandates made distributed sensing standard practice for liquids transmission lines. Hyperscale construction in Virginia and Texas is channeling orders toward fire-loop upgrades, while the Digital 395 project showcased the dual use of telecom fibers for seismic and network services. Canada's oil sands continue thermal monitoring, but the pace slows with capital discipline. Mexico's constrained budgets are attracting sensing-as-a-service providers that absorb capital risk, signaling a service-driven shift in the sensing cable market.

Europe represented about 24% of turnover, buoyed by subsea HVDC links that embed continuous temperature sensing. NKT's EUR 2 billion (USD 2.16 billion) SSEN Transmission contract packages 525 kV cable with embedded fibers, underscoring the region's push to electrify the North Sea. The Middle East is growing fastest at a 9.21% CAGR, with Ducab's high-voltage fiber offerings and national oil company mandates driving adoption. Meanwhile, policy gaps and capital scarcity leave most of South America and Africa below 5% penwith penetration etrationot programs in Brazil's offshore fields hint at latent potential once interrogator costs fall.

- AP Sensing GmbH

- Bandweaver Technology Ltd.

- Omnisens SA

- Luna Innovations Incorporated

- Silixa Ltd.

- Fotech Solutions Ltd.

- Schlumberger Limited

- Halliburton Company

- Yokogawa Electric Corporation

- OFS Fitel, LLC

- Brugg Kabel AG

- AFL Telecommunications LLC

- NKT Photonics A/S

- Micron Optics, Inc.

- OptaSense Ltd.

- FISO Technologies Inc.

- Ziebel AS

- Future Fibre Technologies Limited

- Sensornet Limited

- LIOS Technology GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Deployment of Distributed Fiber-Optic Sensing in Unconventionals

- 4.2.2 Mandatory Leak-Detection Regulations for Hazardous Pipelines

- 4.2.3 Integration of AI Analytics Lowers OPEX and False Alarms

- 4.2.4 Adoption of Passive Fire-Detection Cables in Hyperscale Data Centers

- 4.2.5 Monetization of Dark Fiber for Dual Telecom-Sensing Use

- 4.2.6 Sub-Sea HVDC Growth Demanding Continuous Thermal Monitoring

- 4.3 Market Restraints

- 4.3.1 Scarcity of Trained Fiber-Optic Installation Workforce

- 4.3.2 High Interrogator-Unit Cost for Long-Reach Deployments

- 4.3.3 Cyber-Hardening Requirements Delaying Approvals

- 4.3.4 Polymer Sensing-Cable Degradation in High-Temperature Wells

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cable Type

- 5.1.1 Fiber-Optic Sensing Cables

- 5.1.2 Electrical/Coaxial Sensing Cables

- 5.1.3 Polymer Optical Fiber (POF) Sensing Cables

- 5.1.4 Hybrid (Power + Fiber) Sensing Cables

- 5.2 By Sensing Technology

- 5.2.1 Distributed Temperature Sensing (DTS)

- 5.2.2 Distributed Acoustic Sensing (DAS)

- 5.2.3 Distributed Strain/Pressure Sensing

- 5.2.4 Hybrid Multi-Parameter Sensing

- 5.3 By Application

- 5.3.1 Leak and Spill Detection

- 5.3.2 Structural Health and Geotechnical Monitoring

- 5.3.3 Power Cable and Grid Asset Monitoring

- 5.3.4 Perimeter and Security Intrusion Detection

- 5.3.5 Fire Detection and Safety Systems

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Power and Utilities

- 5.4.3 Civil Infrastructure and Construction

- 5.4.4 Industrial Manufacturing and Process

- 5.4.5 Defense and Security

- 5.4.6 Data Centers and Commercial Buildings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AP Sensing GmbH

- 6.4.2 Bandweaver Technology Ltd.

- 6.4.3 Omnisens SA

- 6.4.4 Luna Innovations Incorporated

- 6.4.5 Silixa Ltd.

- 6.4.6 Fotech Solutions Ltd.

- 6.4.7 Schlumberger Limited

- 6.4.8 Halliburton Company

- 6.4.9 Yokogawa Electric Corporation

- 6.4.10 OFS Fitel, LLC

- 6.4.11 Brugg Kabel AG

- 6.4.12 AFL Telecommunications LLC

- 6.4.13 NKT Photonics A/S

- 6.4.14 Micron Optics, Inc.

- 6.4.15 OptaSense Ltd.

- 6.4.16 FISO Technologies Inc.

- 6.4.17 Ziebel AS

- 6.4.18 Future Fibre Technologies Limited

- 6.4.19 Sensornet Limited

- 6.4.20 LIOS Technology GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment