|

시장보고서

상품코드

2063332

트랜스포머리스 UPS 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Transformerless UPS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

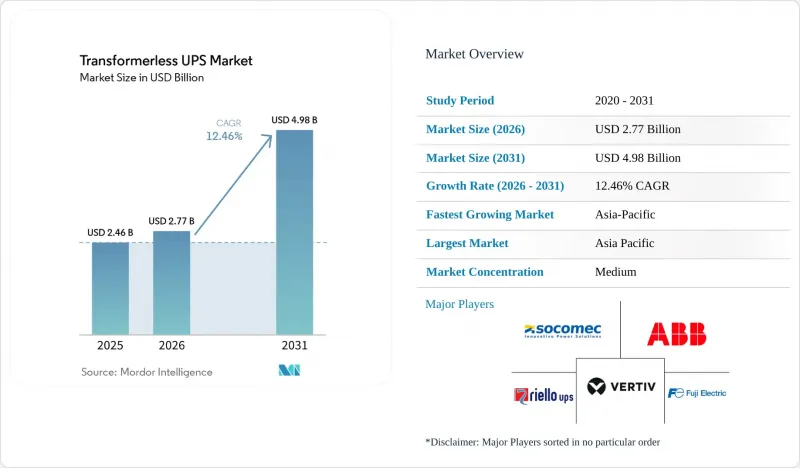

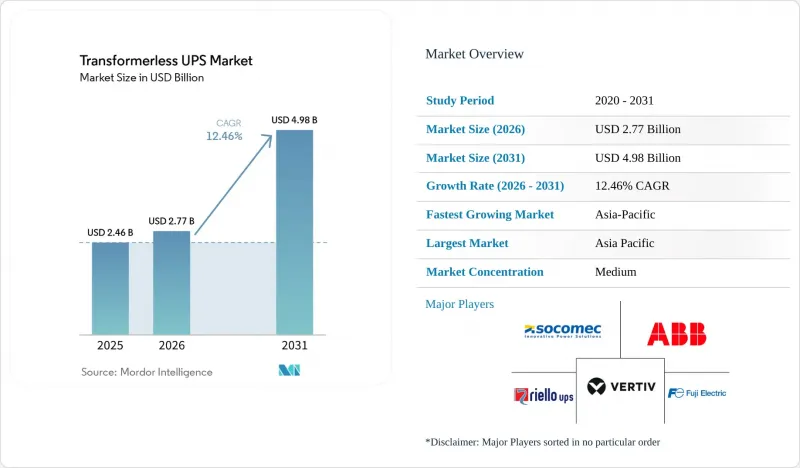

Mordor Intelligence에 의하면, 트랜스포머리스 UPS 시장 규모는 2025년에 24억 6,000만 달러로 평가되었고, 2026년 27억 7,000만 달러로 추정되고, 2031년까지 49억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 예측 기간 CAGR은 12.46%를 나타낼 전망입니다.

본 보고서는 정격 출력별(10KVA 미만, 10-100KVA, 100KVA 초과), 상수별(단상, 3상), 최종 사용자 산업별(데이터센터, 산업 제조, 상업용 건물, 의료시설, 통신 등), 폼 팩터별(랙 마운트형, 타워형, 모듈형), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 트랜스리스 UPS 시장 동향 및 인사이트

하이퍼스케일 데이터센터의 용량 확대

트랜스포머리스 UPS 시장은 현재의 데이터센터 건설 주기와 밀접한 관련이 있습니다. 이는 새로운 AI 캠퍼스가 기존 기업 시설보다 랙 밀도가 높고, 전력 변동이 더 빠르며, 전압 불안정성에 대한 허용 범위가 훨씬 좁다는 전제 하에 계획되었기 때문입니다. 아마존은 2026년 4월, 미시시피주 데이터센터에 250억 달러를 투자할 것이라고 발표했습니다. 이는 여전히 막대한 규모의 인프라 투자가 새로운 디지털 인프라 구축에 투입되고 있음을 보여줍니다. 이는 UPS 공급업체에게 중요한 의미를 지닙니다. 왜냐하면 고밀도 AI 룸에는 신속하게 대응할 수 있고, 높은 부하 상태에서도 효율을 유지하며, 냉각 및 개폐 장치의 요구 사항으로 인해 이미 공간이 부족한 전원실에 설치할 수 있는 보호 시스템이 필요하기 때문입니다. Vertiv가 2024년 12월, 250kW에서 1,250kW의 정격 용량을 갖춘 대규모 데이터센터용 소형 고전력 밀도 UPS 플랫폼을 출시한 것은 공급업체들의 로드맵이 이미 더 적은 수의 캐비닛으로 더 큰 보호 부하를 처리하는 방향으로 전환되고 있음을 보여줍니다. 또한, Piller사는 핀란드에서 진행 중인 Nebius Group의 확장 프로젝트를 위해 200대 이상의 UPS 장비를 공급했습니다. 해당 사이트는 75MW까지 확장될 예정이며, 목표 PUE는 1.1이라는 낮은 수준으로 설정되어 있는데, 이는 현재 도입 규모에 따라 조달 결정이 좌우되고 있는 현실을 반영한 것입니다. 하이퍼스케일, 코로케이션, AI 중심 캠퍼스를 지향하는 프로젝트가 늘어남에 따라, 트랜스리스 UPS 시장은 고밀도이며 극도로 역동적인 컴퓨팅 환경을 지원할 수 있는 고속 응답·고주파 전력 아키텍처와의 호환성을 점점 더 강화하고 있습니다.

에너지 효율과 총소유비용(TCO)에 대한 관심 증가

무변압기 UPS 시장이 확대되고 있는 배경에는 에너지 손실이 설치 후 시설 팀이 해결해야 할 이차적인 기술적 과제가 아니라, 복원력과 마찬가지로 재무적 과제로 대두되고 있다는 점도 있습니다. Vertiv는 자사의 PowerUPS 9000 플랫폼에서 최대 97.5%의 이중 변환 효율을 달성했다고 보고했으며, 이는 전력 비용과 열 부하를 모두 고려해야 하는 대규모의 중요한 환경에서 현재 기대되는 성능 기준을 반영한 것입니다. Centiel사는 PremiumTower S2가 VFI 모드에서 최대 97.1%의 효율을 달성하고, 설계 수명인 15년을 초과하는 기간 동안 정기적인 부품 교체가 필요 없도록 함으로써, 초기 비용만을 기준으로 한 결정이 아닌 라이프사이클 기반의 조달로 전환하는 것을 지원하고 있다고 밝혔습니다. 미국 에너지부의 광대역 갭 전력 전자 장치에 관한 프레임워크 역시, 첨단 전력 전자 기술이 산업용 및 계통 연계 용도 전반에 걸쳐 효율, 전력 밀도, 시스템 성능을 어떻게 향상시킬 수 있는지를 명확히 보여주며, 이는 새로운 트랜스리스 설계의 기술적 타당성을 뒷받침합니다. 실용적인 관점에서 볼 때, 이는 트랜스리스 UPS 시장의 구매자들이 이전의 조달 주기보다 더 엄격하게 전력 손실, 냉각 수요, 유지보수 주기 및 운영 프로파일을 비교 검토하고 있음을 의미합니다. 유럽에서는 EU의 에코디자인 지침이 10kVA를 초과하는 많은 설비에 대해 실질적인 조달 기준치를 설정함으로써 이러한 방향성을 더욱 강화하고 있습니다.

높은 초기 시스템 및 배터리 투자 비용

초기 비용은 여전히 트랜스리스 UPS 시장의 큰 걸림돌로 작용하고 있으며, 특히 리튬 이온 배터리 캐비닛이 추가되는 프로젝트의 경우 장기적인 운영 경제성보다 여전히 구매 가격이 주요 판단 기준이 되고 있어 이러한 경향이 두드러집니다. 중소기업, 분산형 통신 사업자 및 예산이 제한된 기관의 경우, 자산의 전체 수명 주기 동안 더 효율적인 시스템이 더 우수한 성능을 발휘하더라도, 초기 투자 비용이 가장 낮은 제안을 우선시하는 승인 절차를 거치는 경우가 많습니다. 이 문제는 의료 분야에서 더욱 심각해집니다. NFPA 99 및 NFPA 110이 주요 전기 시스템과 비상 전원의 성능에 대해 엄격한 요건을 규정하고 있기 때문에 프로젝트의 총 예산은 UPS 하드웨어 자체의 비용을 넘어 증가하게 되며, 소규모 병원 네트워크의 경우 자본 승인을 얻기가 더욱 어려워집니다. 즉, 리튬 이온 배터리의 장점인 교체 빈도 감소, 급속 충전, 냉각 수요 감소, 유지보수 작업 경감과 같은 이점이라 할지라도, 예산 제약이나 분산된 조달 권한 앞에서는 여전히 설득력이 떨어지는 결과가 될 수 있습니다. 이러한 장벽은 남미, 아프리카 및 동남아시아 일부 지역에서 가장 두드러집니다. 이러한 지역에서는 성숙한 시장에 비해 배터리 공급 체계, 자금 조달 수단, 장기적인 시설 계획이 충분히 갖춰져 있지 않은 경우가 많기 때문입니다. 사업자가 수명 주기 관점을 수용하더라도, 초기 도입 패키지 비용이 시설의 승인 가능한 자본 예산 상한선을 초과할 경우, 트랜스리스 UPS 시장은 단기적인 수주 기회를 놓칠 가능성이 있습니다.

부문별 분석

2025년 기준으로 10-100kVA 부문은 트랜스리스 UPS 시장의 44.02%를 차지했으며, 상업용 빌딩, 엣지 노드, 중규모 기업 데이터센터, 통신 기지국, 그리고 광범위한 교체 수요에서 수요의 중심을 이루고 있습니다. 이 범위는 훨씬 더 대규모 설비에 따르는 공간 확보, 설계상의 복잡성, 자본 부담 없이도 충분한 내결함성이 필요한 프로젝트에 적합합니다. 따라서, 성숙한 도입 환경과 신흥 도입 환경 모두에서 여전히 중요한 위치를 차지하고 있습니다. 또한, 많은 기업 및 통신 사업자의 웹사이트에서 실제로 적용되는 운영 방식과도 잘 부합합니다. 이러한 사이트에서는 시스템이 최대 부하보다 낮은 수준에서 장시간 가동되므로, 뛰어난 부분 부하 효율과 관리가 용이한 설치 조건의 이점을 누릴 수 있습니다. 10kVA 미만의 제품군은 여전히 분산된 지점이나 소규모 시설에서 사용되고 있지만, 그 소규모 특성과 낮은 효율성으로 인해 트랜스포머리스 UPS 시장 전체에서 조달 우선순위가 수명 주기 비용, 밀도, 성능으로 전환되는 가운데 그 영향력은 제한적입니다.

100kVA를 초과하는 부문은 AI 데이터센터 건설, 대규모 코로케이션 시설, 그리고 메가와트급 보호 요구 사항으로 전환되는 산업용 중요 부하의 성장에 힘입어 2031년까지 연평균 성장률(CAGR) 12.68%를 나타낼 것으로 전망됩니다. Vertiv사의 PowerUPS 9000은 1대당 250-1,250kW를 지원하며, 최대 5MW까지 확장할 수 있습니다. 이는 공급업체가 더 높은 캐비닛 밀도와 대규모 디지털 캠퍼스와의 호환성을 갖추고, 더 대규모의 보호 부하 블록을 목표로 하고 있음을 보여줍니다. 500kW SiC 기반 3상 UPS에 대한 동료 심사 논문을 통해서도, 최적화된 필터 및 방열 설계를 통해 실용적인 상업적 가치를 지닌 대용량 운전이 가능함이 입증되었으며, 이는 더 대규모의 트랜스리스 플랫폼으로 나아가는 기술적 로드맵을 뒷받침하는 데 일조했습니다. 이 상용 제품 시장 출시 준비와 기술적 검증이 결합됨에 따라, 트랜스리스 UPS 시장이 고밀도 컴퓨팅, 대규모 산업 자동화 및 더 큰 규모의 중요 시설로 전환됨에 따라 고출력 부문의 중요성이 더욱 커질 것으로 보입니다.

2025년에는 3상 시스템이 매출 점유율의 66.23%를 차지했으며, 대규모 데이터센터, 산업 플랜트, 주요 상업시설에서의 도입에서 여전히 중심적인 위치를 차지하고 있습니다. 이러한 시설에서는 균형 잡힌 전력 분배와 고밀도 부하에 대한 대응이 표준적인 설계 전제가 되고 있습니다. 이러한 우위는 중요 인프라의 기존 아키텍처를 반영한 것입니다. 왜냐하면 대규모 시설에서는 이미 효율성, 안정성, 그리고 업스트림 및 하류 장비와의 손쉬운 통합을 중시하는 3상 토폴로지를 우선시하는 전기 배선 레이아웃에 의존하고 있기 때문입니다. 또한, 이 부문은 유럽 및 기타 성숙 시장에서 더욱 효율적인 전력 인프라를 높이 평가하는 규제 및 보고 환경의 혜택도 누리고 있습니다. 이로 인해 신규 프로젝트나 교체 주기에서 구형이고 비효율적인 장비의 도입을 정당화하기가 어려워지고 있습니다. 실제로, 트랜스리스 UPS 시장에서 프로젝트 규모가 소규모 룸 레벨, 브랜치 레벨 또는 단일 캐비닛 백업 요구 사항을 초과하는 경우, 3상 플랫폼이 여전히 기본 선택지로 자리 잡고 있습니다.

단상 시스템은 2031년까지 연평균 성장률(CAGR) 12.91%를 나타낼 것으로 예측되며, 이는 단상 부문에서 가장 높은 성장률을 나타내는 것으로, 주요 용도에서의 철수가 아닌 분산형 디지털 인프라에서의 활용 확대를 시사합니다. 이러한 성장은 5G 스몰 셀, 엣지 컴퓨팅 노드, 지점 시설, 그리고 3상 전원을 사용할 수 없거나 설치 장소의 실제 수요 프로파일에 비해 규모가 과도한 소형 기업 거점에서 비롯되고 있습니다. 최신 단상 설계는 출력 역률 향상, 깨끗한 전력 공급 및 고효율화를 통해 기존 성능 격차를 좁히고 있으며, 규모는 작지만 여전히 정밀한 응용 분야에서 신뢰성을 높이고 있습니다. 소수의 초대형 사이트가 아닌 수많은 소규모 사이트나 외딴 지역으로 도입이 확대됨에 따라, 단상 제품은 3상 시스템의 기존 인프라를 대체하는 것이 아니라 무변압기 UPS 시장을 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년에 43.54%의 점유율을 차지한 것으로 평가되었으며, 이 지역의 트랜스리스 UPS 시장은 2031년까지 연평균 성장률(CAGR) 12.55%로 성장할 것으로 전망됩니다. 현재 전망에 따르면, 이 지역은 가장 규모가 크고 가장 빠르게 성장하는 지역으로 자리매김할 것으로 보입니다. 이러한 위상은 중국의 디지털 인프라 계획, 일본의 반도체 팹 부활, 그리고 인도의 디지털 공공 인프라 구상이 맞물려 만들어낸 효과를 반영한 것으로, 이 모든 요소는 데이터센터, 통신 및 산업 분야에서 효율적이고 소형화된 전원 보호 솔루션에 대한 새로운 수요를 뒷받침하고 있습니다. 또한, 해당 지역은 SiC 및 관련 파워 일렉트로닉스 밸류체인에 쉽게 접근할 수 있다는 이점도 누리고 있으며, 이를 통해 제조 비용 효율이 향상되고 조달 주기 단축에 따라 리드 타임 압박을 완화할 수 있습니다. 이 밸류체인상의 우위는 중요한 의미를 지닙니다. 왜냐하면 대규모 데이터센터나 통신 프로젝트의 구매 담당자들은 프로젝트 규모가 커짐에 따라 납기 준수, 유연한 구성, 그리고 비용 관리를 더욱 중요하게 여기게 되었기 때문입니다. 이러한 이유로, 아시아태평양의 트랜스리스 UPS 시장은 예측 기간 동안 주요 성장 동력으로 남아 있을 가능성이 높습니다.

북미는 하이퍼스케일 사업의 확대, 송전망에 대한 투자, 그리고 대규모 데이터센터 단지에 대한 지속적인 설비 투자를 바탕으로 트랜스리스 UPS 시장의 두 번째 주요 수요 거점으로 자리매김하고 있습니다. 아마존은 2026년 4월, 미시시피주 데이터센터에 250억 달러를 투자하겠다고 발표하며, 해당 지역에 여전히 대규모의 새로운 핵심 전력 인프라가 계획되고 있음을 시사했습니다. 이튼(Eaton)사의 보고서에 따르면, 미국의 민간 전력 회사들은 데이터센터의 전력 수요 증가에 대응하기 위해 향후 5년간 약 4,000억 달러 규모의 송전망 업그레이드 계획을 세우고 있으며, 이는 디지털 인프라의 성장이 광범위한 시스템에 미치는 영향을 여실히 보여주고 있습니다. 유럽은 특히 운영 손실이나 보고 의무가 더욱 엄격하게 적용되는 데이터센터 및 산업 분야에서 효율성에 관한 규제와 업데이트 주기가 여전히 현대적이고 고효율적인 시스템을 뒷받침하고 있기 때문에 상업적으로 중요한 시장으로 남아 있습니다. 따라서 아시아태평양의 규모에는 미치지 못하지만, 유럽은 여전히 프리미엄 수요의 중심적인 위치를 차지하고 있습니다.

남미, 중동 및 아프리카는 절대적인 규모 면에서는 여전히 작지만, 5G 구축, 코로케이션 시설 확충, 그리고 전력망의 불안정성으로 인해 성숙한 지역과는 다른 수요 패턴이 나타나고 있으며, 대부분의 경우 소형이고 효율적인 백업 아키텍처가 선호되기 때문에 전략적으로 중요합니다. 브라질과 아르헨티나는 여전히 남미의 주요 수요 거점으로 자리 잡고 있는 반면, 아랍에미리트(UAE)와 사우디아라비아에서는 국가 주도의 디지털 인프라 프로그램 및 AI 관련 시설 개발을 통해 3상 전원에 대한 수요가 확대되고 있습니다. 아프리카에서는 통신 사업자들이 제한된 캐비닛 공간 내에서 더 긴 시간 동안 백업 기능을 필요로 하기 때문에 통신 용도가 여전히 중심적인 위치를 차지하고 있습니다. UPTECH는 컴팩트한 크기, 효율성, 통신 등급의 신뢰성을 겸비한 트랜스리스 UPS 제품을 판매하고 있습니다. 이러한 개척 지역들은 현재로서는 매출을 주도파관는 않지만, 트랜스리스 UPS 시장의 잠재 고객 기반을 확대하고, 예측 기간 동안 더 폭넓은 제품 포트폴리오의 필요성을 높이는 요인이 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the transformerless UPS market size was valued at USD 2.46 billion in 2025 and is estimated to grow from USD 2.77 billion in 2026 to reach USD 4.98 billion by 2031, at a CAGR of 12.46% during the forecast period 2026-2031.

This report is Segmented by Power Rating (Less Than 10 KVA, 10-100 KVA, and Greater Than 100 KVA), Phase (Single-Phase, and Three-Phase), End-User Industry (Data Centers, Industrial Manufacturing, Commercial Buildings, Healthcare Facilities, Telecom, and More), Form Factor (Rack-Mounted, Tower, and Modular), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Transformerless UPS Market Trends and Insights

Hyperscale Data Center Capacity Expansion

The transformerless UPS market is closely tied to the current data center build cycle, because new AI campuses are being planned around higher rack density, faster power swings, and much lower tolerance for voltage instability than earlier enterprise facilities. Amazon announced in April 2026 that it will invest USD 25 billion in Mississippi data centers, which shows that very large-scale infrastructure commitments are still flowing into new digital capacity. This matters for UPS vendors because dense AI rooms require protection systems that can respond quickly, remain efficient under heavy load, and fit into power rooms already under pressure from cooling and switchgear requirements. Vertiv's December 2024 launch of a compact, high-power-density UPS platform for large data centers, with ratings from 250 kW to 1,250 kW, demonstrated that supplier roadmaps are already shifting toward larger protected loads in fewer cabinets. Piller also supplied more than 200 UPS units for Nebius Group's expansion in Finland, where the site is being expanded to 75 MW with a target PUE as low as 1.1, which reflects the deployment scale now shaping procurement decisions. As more projects move toward hyperscale, colocation, and AI-focused campuses, the transformerless UPS market is increasingly aligning with fast-response, high-frequency power architectures that can support dense, highly dynamic compute environments.

Rising Energy Efficiency And Total Cost Of Ownership Focus

The transformerless UPS market is also expanding because energy loss is now a financial issue alongside resilience, rather than a secondary technical consideration left for facility teams to solve after installation. Vertiv reported up to 97.5% double-conversion efficiency for its PowerUPS 9000 platform, which reflects the performance threshold now expected in large, critical environments where power costs and thermal loads are both under review. Centiel stated that PremiumTower S2 achieves up to 97.1% efficiency in VFI mode and avoids scheduled component replacements over a design life exceeding 15 years, supporting the move toward lifecycle-based procurement rather than first-cost decisions alone. The U.S. Department of Energy's wide-bandgap power electronics framework also highlighted how advanced power electronics can improve efficiency, power density, and system performance across industrial and grid-connected applications, which supports the technology case for newer transformerless designs. In practical terms, this means buyers in the transformerless UPS market are now weighing power loss, cooling demand, maintenance cycles, and operating profile with greater discipline than in earlier procurement cycles. In Europe, the EU Ecodesign Directive has reinforced that direction by setting a practical procurement floor for many installations above 10 kVA.

High Upfront System And Battery Capex

Upfront costs remain a real brake on the transformerless UPS market, especially when lithium-ion battery cabinets are added to projects that are still being judged mainly on acquisition price rather than long-term operating economics. Smaller enterprises, distributed telecom operators, and budget-constrained institutions often face approval processes that reward the lowest initial capital request, even when a more efficient system would perform better across the asset life. The issue becomes sharper in healthcare, where NFPA 99 and NFPA 110 set strict requirements for essential electrical systems and emergency power performance, raising the total project budget beyond UPS hardware alone and making capital approval more difficult for smaller hospital networks. That means the case for lithium-ion, lower replacement frequency, faster recharge, reduced cooling demand, and less maintenance labor, can still lose against short-budget planning and fragmented procurement authority. The barrier is most visible in South America, Africa, and parts of Southeast Asia, where battery supply depth, financing options, and long-horizon facility planning are often less developed than in mature markets. Even when operators accept the lifecycle argument, the transformerless UPS market can still lose near-term orders if the initial package exceeds the capital threshold a site can approve.

Other drivers and restraints analyzed in the detailed report include:

- Growing Preference For High Power Density And Reduced Footprint

- Modular UPS Adoption For Staged Capacity Expansion

- Load Compatibility Limits In High-Inrush And Legacy Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 10-100 kVA segment accounted for 44.02% of the transformerless UPS market in 2025, making it the volume center of demand across commercial buildings, edge nodes, mid-size enterprise data centers, telecom base stations, and a wide base of repeat replacement activity. This range fits projects that need meaningful resilience without the space commitment, engineering complexity, and capital burden associated with much larger installations, which is why it remains relevant across both mature and emerging deployment settings. It also aligns well with the practical operating profile of many enterprise and telecom sites, where systems spend long periods below peak load, thereby benefiting from strong partial-load efficiency and manageable installation requirements. The less than 10 kVA range still serves distributed branch offices and small facilities, but its smaller scale and lower efficiency limit its influence as procurement priorities shift toward lifecycle cost, density, and performance across the broader transformerless UPS market.

The more than 100 kVA segment is projected to grow at a 12.68% CAGR through 2031, supported by AI data center buildouts, large colocation halls, and industrial critical loads moving into megawatt-scale protection requirements. Vertiv's PowerUPS 9000 supports 250-1,250 kW per unit and scales to 5 MW, which shows how suppliers are targeting larger protected load blocks with higher cabinet density and a stronger fit for large digital campuses. Peer-reviewed research on a 500 kW SiC-based three-phase UPS also showed that an optimized filter and heat-dissipation design can support large-capacity operation with credible commercial relevance, helping validate the technical path for larger transformerless platforms. That combination of commercial product readiness and technical validation suggests that the upper power tier will continue to gain weight as the transformerless UPS market shifts toward high-density compute, large industrial automation, and larger critical facilities.

Three-phase systems held 66.23% of the revenue share in 2025, keeping them at the center of deployment in large data centers, industrial plants, and major commercial facilities, where balanced power distribution and higher-density load support are standard design assumptions. That lead reflects the installed architecture of critical infrastructure, because large facilities already depend on electrical layouts that favor three-phase topology for efficiency, stability, and straightforward integration with upstream and downstream equipment. The segment also benefits from a regulatory and reporting environment that increasingly rewards more efficient power infrastructure in Europe and other mature markets, making older, low-efficiency equipment harder to justify in new projects and replacement cycles. In practice, this keeps three-phase platforms as the default choice whenever projects move beyond smaller room-level, branch-level, or single-cabinet backup requirements in the transformerless UPS market.

Single-phase systems are projected to grow at a 12.91% CAGR through 2031, making them the fastest-growing phase segment and signaling wider use in distributed digital infrastructure rather than a retreat from critical applications. Growth comes from 5G small cells, edge computing nodes, branch facilities, and compact enterprise sites where three-phase supply is either unavailable or oversized relative to the installation's actual demand profile. Modern single-phase designs have narrowed earlier performance gaps through better output power factor, cleaner power delivery, and higher efficiency, thereby improving their credibility in smaller yet still sensitive applications. As deployment expands across many compact or remote sites instead of a few very large ones, single-phase products are broadening the transformerless UPS market rather than displacing the installed base of three-phase systems.

Geography Analysis

Asia-Pacific held a 43.54% share in 2025, and the regional transformerless UPS market is forecast to grow at a 12.55% CAGR through 2031, keeping the region as both the largest and the fastest-growing geography in the current outlook. This position reflects the combined effect of China's digital infrastructure programs, Japan's semiconductor-fab revival, and India's Digital Public Infrastructure agenda, all of which support new demand for efficient, compact power protection across data center, telecom, and industrial settings. The region also benefits from closer access to SiC and related power-electronics supply chains, which improves manufacturing economics and can reduce lead-time pressure as procurement cycles tighten. That supply chain advantage matters because buyers in large data center and telecom programs are placing more value on delivery reliability, flexible configuration, and cost discipline as project size continues to increase. For these reasons, the transformerless UPS market in Asia-Pacific is likely to remain the main growth engine through the forecast period.

North America forms the second major demand center in the transformerless UPS market, supported by hyperscale expansion, grid investment, and continued capital spending on large data center campuses. Amazon said in April 2026 that it would invest USD 25 billion in Mississippi data centers, signaling that significant new critical power infrastructure is still being planned in the region. Eaton reported that U.S. investor-owned utilities plan around USD 400 billion in grid upgrades over 5 years in response to rising data center power demand, underscoring the broader system impacts now surrounding digital infrastructure growth. Europe remains commercially important because efficiency regulations and replacement cycles continue to favor modern, high-efficiency systems, especially in data center and industrial settings, where operating losses and reporting obligations are taken more seriously. That keeps Europe central to premium demand, even if it does not match Asia-Pacific's scale.

South America, the Middle East, and Africa remain smaller in absolute terms, but they are strategically important because 5G rollout, colocation buildout, and grid instability are creating demand patterns that differ from mature regions and often favor compact, efficient backup architectures. Brazil and Argentina remain the main South American demand centers, while the United Arab Emirates and Saudi Arabia are generating larger three-phase requirements through state-backed digital infrastructure programs and AI-linked facility development. In Africa, telecom applications remain central because operators need longer backup capability within constrained cabinets, and UPTECH markets transformerless UPS products that combine compact size, efficiency, and telecom-grade reliability. These frontier regions will not define current revenue leadership, but they do widen the addressable base of the transformerless UPS market and strengthen the case for broader product portfolios across the forecast period.

- Socomec Group S.A.

- ABB Ltd.

- Riello Elettronica S.p.A.

- Vertiv Group Corporation

- Fuji Electric Co., Ltd.

- Kehua Data Co., Ltd.

- Cyber Power Systems (USA), Inc.

- Centiel AG

- Borri S.p.A.

- AEG Power Solutions B.V.

- Piller Group GmbH

- East Group Co., Ltd.

- INVT Power System (Shenzhen) Co., Ltd.

- Salicru S.A.

- BlueWalker GmbH

- BPC Energy Limited

- N1 Critical Technologies, Inc.

- Shenzhen EverExceed Industrial Co., Ltd.

- Kohler Uninterruptible Power Ltd.

- Santak Electronic (Shenzhen) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale Data Center Capacity Expansion

- 4.2.2 Rising Energy Efficiency and Total Cost of Ownership Focus

- 4.2.3 Growing Preference for High Power Density and Reduced Footprint

- 4.2.4 Modular UPS Adoption for Staged Capacity Expansion

- 4.2.5 Silicon Carbide Power Stage Efficiency Gains

- 4.2.6 Grid-Interactive Ups Use for Tariff Optimization

- 4.3 Market Restraints

- 4.3.1 High Upfront System and Battery Capex

- 4.3.2 Load Compatibility Limits in High-Inrush and Legacy Environments

- 4.3.3 Cybersecurity Exposure of Network-Connected Power Controls

- 4.3.4 Wide-Bandgap Semiconductor Supply Concentration

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Rating

- 5.1.1 Less than 10 kVA

- 5.1.2 10-100 kVA

- 5.1.3 Greater than 100 kVA

- 5.2 By Phase Type

- 5.2.1 Single-Phase

- 5.2.2 Three-Phase

- 5.3 By End-user Industry

- 5.3.1 Data Centers

- 5.3.2 Industrial Manufacturing

- 5.3.3 Commercial Buildings

- 5.3.4 Healthcare Facilities

- 5.3.5 Telecom

- 5.3.6 Other End-user Industries

- 5.4 By Form Factor

- 5.4.1 Rack-mounted

- 5.4.2 Tower

- 5.4.3 Modular

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Socomec Group S.A.

- 6.4.2 ABB Ltd.

- 6.4.3 Riello Elettronica S.p.A.

- 6.4.4 Vertiv Group Corporation

- 6.4.5 Fuji Electric Co., Ltd.

- 6.4.6 Kehua Data Co., Ltd.

- 6.4.7 Cyber Power Systems (USA), Inc.

- 6.4.8 Centiel AG

- 6.4.9 Borri S.p.A.

- 6.4.10 AEG Power Solutions B.V.

- 6.4.11 Piller Group GmbH

- 6.4.12 East Group Co., Ltd.

- 6.4.13 INVT Power System (Shenzhen) Co., Ltd.

- 6.4.14 Salicru S.A.

- 6.4.15 BlueWalker GmbH

- 6.4.16 BPC Energy Limited

- 6.4.17 N1 Critical Technologies, Inc.

- 6.4.18 Shenzhen EverExceed Industrial Co., Ltd.

- 6.4.19 Kohler Uninterruptible Power Ltd.

- 6.4.20 Santak Electronic (Shenzhen) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment