|

시장보고서

상품코드

2063334

드론 데이터 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Drone Data Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

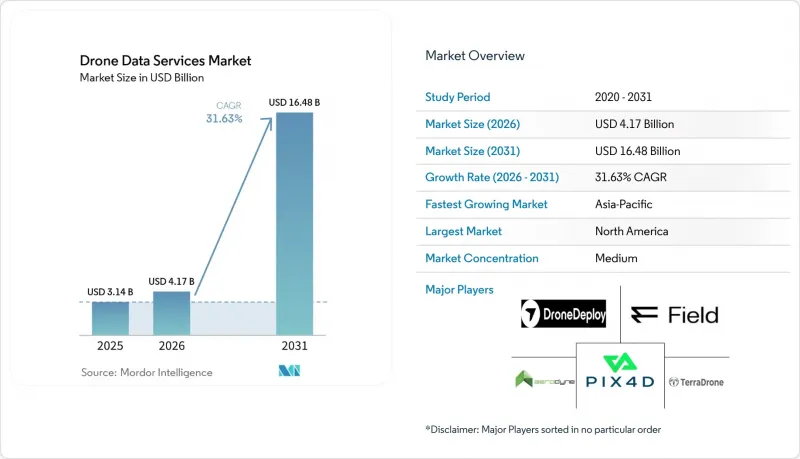

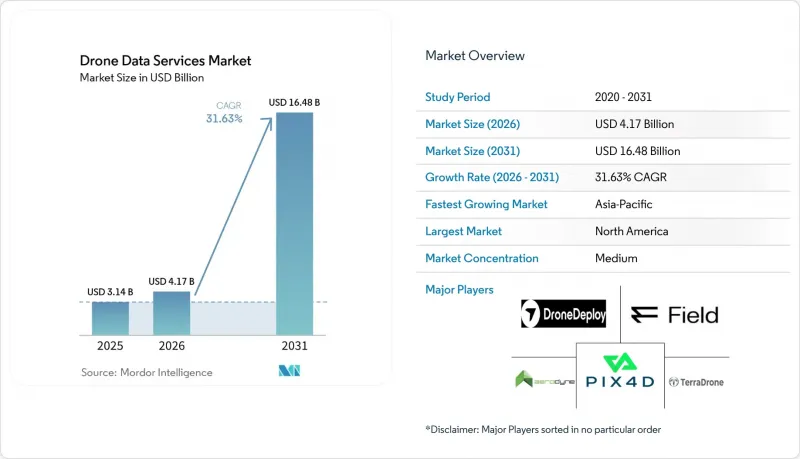

Mordor Intelligence에 의하면, 드론 데이터 서비스 시장 규모는 2025년에 31억 4,000만 달러로 평가되었고, 2026년에 41억 7,000만 달러로 추정되고, 2031년까지 164억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 31.63%로 성장할 전망입니다.

본 보고서는 서비스 유형별(매핑 및 측량, 사진 측량 및 3D 모델링 등), 플랫폼 유형별(멀티로터형 무인 항공기 등), 최종 사용자 산업별(농업, 에너지 및 유틸리티, 건설 및 광업, 석유 및 가스, 보험 등), 도입 모델별(클라우드, 온프레미스, 하이브리드), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 드론 데이터 서비스 시장 동향 및 인사이트

주요 시장의 BVLOS 규제 완화

시야 외(BVLOS) 비행 허가로 인해 현장 감시원이 필요 없어지며, 통로 매핑 및 작물 모니터링 시 에이커당 검사 비용이 40-60% 절감됩니다. 2025년에 발표된 미국의 Part 108 초안에서는 인증된 운영자가 별도의 면제 조치 없이 50km를 초과하는 비행 임무를 수행할 수 있도록 하는 성능 기반 기준이 마련되었습니다. 2025년 1월에 발효될 유럽의 U-Space 구상은 전자 식별 및 지오펜싱을 통한 안전 대책이 마련되면 자동 비행 계획을 가능하게 합니다. 이 지역들에서 조기에 규제가 명확해짐에 따라 에너지 및 건설 분야의 고객들은 사업 규모 확대를 가속화할 수 있게 되었으나, 아시아 일부 지역에서는 도입 상황이 고르지 않아 중국이나 인도 이외의 지역에서는 이와 같은 혜택을 누리지 못하고 있습니다.

LiDAR 및 사진측량 센서의 급격한 가격 하락

2만 달러 미만의 LiDAR 모듈은 과거에는 수십만 달러 규모의 항공기 탑재 시스템에서만 구현할 수 있었던 수직 정밀도에 필적하게 되었으며, 이에 따라 중견 계약업체들도 지형 측량 프로젝트에 경쟁력 있는 가격으로 입찰할 수 있게 되었습니다. DJI의 L3 유닛은 기존 Velodyne 제품보다 가격이 60%나 저렴하여, 측량 업체와 유틸리티체에게 3cm의 정밀도를 실현할 수 있게 되었습니다. 42메가픽셀 RGB 페이로드의 가격도 마찬가지로 하락하고 있어, 고해상도 사진 측량의 활용 기회가 확대되고 있습니다. 이로 인해 경쟁 우위는 하드웨어 소유에서 정사모자이크상의 이상을 자동으로 감지하는 클라우드 기반 분석으로 확실히 이동하고 있습니다.

분열된 세계의 공역 관리 기준

193개 규제를 아우르며 규정 준수를 관리하는 운영사는 매뉴얼, 보험 계약, 항공기 원격 측정 시스템 등의 운영 측면을 현지화해야 하므로 큰 과제에 직면해 있습니다. 이러한 요건으로 인해 규정 준수 비용이 25-40% 증가하고, 서비스 개시까지의 기간이 최대 18개월 연장될 수 있습니다. 국제민간항공기구(ICAO)는 일반적인 지침만을 제공하고 있기 때문에 국가에 따라 승인 절차에 큰 차이가 발생하고 있습니다. 예를 들어, 파키스탄에서는 여전히 시야 외 비행(BVLOS)이 금지되어 있는 반면, 인도에서는 이러한 운용에 대응하기 위해 디지털 스카이 회랑의 확장을 적극적으로 추진하고 있습니다. 이러한 규제의 복잡성은 해당 지역에서 강력한 입지를 확보한 대형 서비스 제공업체에게 유리한 환경을 조성하고 있습니다. 왜냐하면, 그들은 이러한 과제에 대처할 수 있는 체제가 갖춰져 있기 때문입니다. 그러나 한편으로는 다자간 회랑 프로젝트의 진전을 늦추고, 국경을 넘는 드론 운용의 시행을 더욱 지연시키는 결과로 이어지고 있습니다.

부문별 분석

측량 및 조사 분야는 2025년 매출의 38.21%를 차지했으며, 이는 드론 데이터 서비스 시장이 여전히 핵심적인 지리공간 산출물에 기반을 두고 있음을 보여줍니다. 그러나 배송 및 물류 데이터 서비스는 경로 최적화 엔진이나 배송 증명 시스템에 정보를 제공하는 실시간 텔레메트리 기술의 견인 아래 연평균 성장률(CAGR) 32.63%로 성장할 전망입니다. 알파벳 산하의 윙(Wing)은 2025년 말까지 35만 건의 배송을 완료했다고 보고했으며, 정확한 GPS 좌표와 중량 변동 데이터를 수집하여 실제 도착 시각으로부터 90초 이내에 예상 도착 시각(ETA)을 정밀하게 산출하고 있습니다. 환경 모니터링의 응용 분야에서는 탄소 크레딧의 MRV(측정·보고·검증) 워크플로우가 지원되고 있으며, Pachama와 같은 플랫폼은 2025년에 1,800만 톤의 CO2를 검증했습니다. 이는 자동화된 검증 도구에 대한 산업 전반 수요가 증가하고 있음을 보여줍니다.

2020년대 후반에는 유틸리티 및 제조업 고객들이 비행 운용, 포인트 클라우드 처리, 결함 분류를 외부에 위탁함에 따라, 점검 및 유지보수 서비스가 수익 다각화를 더욱 촉진할 것입니다. Skyspecs사만 해도 2025년에는 240만 장의 풍력 발전 블레이드 이미지를 처리하여 94%의 감지 정확도를 달성하는 동시에 오감지를 40% 줄였습니다. 2만 달러짜리 LiDAR 시스템의 가격이 더욱 하락함에 따라, 사진 측량 및 3D 모델링 워크플로가 중규모 계약업체들에게도 이용 가능해졌으며, 비록 눈부신 성장률은 아니더라도 이러한 결과물을 대상으로 하는 드론 데이터 서비스 시장을 견인하고 있습니다.

멀티로터 기체는 좁은 도시 지역이나 산업 단지에서 수직 이착륙이 가능하다는 장점 덕분에, 2025년 드론 데이터 서비스 시장 점유율의 61.72%를 차지했습니다. 그러나 배터리용량 제한으로 인해 비행 시간이 35분 미만으로 제한되어, 회랑 프로젝트의 실행에 제약이 발생하고 있습니다. Quantum-Systems사의 Trinity F90+와 같은 하이브리드 VTOL 시스템은 한 번의 출동으로 400헥타르를 커버할 수 있을 뿐만 아니라 4제곱미터의 빈 공간에도 착륙할 수 있어, 예측 기간 동안 연평균 성장률(CAGR) 32.43%에 기여할 것으로 전망됩니다. 고정익 플랫폼은 광역 농업 및 지적 측량 분야에서 틈새 시장을 유지하고 있는 반면, 250g 미만의 나노 크래프트는 부동산 및 보험 업계의 지붕 조사 분야에서 완화된 등록 규제를 지속적으로 활용하고 있습니다.

추진 효율이 향상되어 1kg당 250와트시에 가까워짐에 따라, 최신 하이브리드 기체는 시속 70km로 최대 2시간 동안 비행할 수 있게 됩니다. 또한, 이 기체들은 로터 호버링으로 원활하게 전환할 수 있어, 대상 지역에서 정밀한 데이터 수집이 가능해집니다. 이러한 장시간 비행 능력과 정밀한 표적 지정 기능을 결합함으로써, 이 하이브리드 모델들은 철도, 파이프라인, 송전선로 회랑 감시 등의 용도에 특히 적합합니다. 기존에는 이러한 업무에 더 고가의 유인 항공기를 사용하거나, 동일한 지역을 커버하기 위해 여러 대의 드론을 연계해야 했습니다. 이러한 첨단 하이브리드 기체의 도입은 상세하고 신뢰할 수 있는 데이터 수집이 필요한 업계에 비용 대비 효과가 높고 효율적인 솔루션을 제공함으로써, 드론 데이터 서비스 시장에서 놀라운 성장과 혁신을 주도하고 있습니다.

지역별 분석

북미는 2025년 드론 데이터 서비스 시장 매출의 41.48%를 차지했습니다. 이는 보험 업계에서 청구 처리 기간을 40% 단축한 FAA(연방항공청)의 조기 면제 조치가 주도한 결과입니다. 이러한 면제 조치 덕분에 50km 거리의 BVLOS(시야 외 비행)를 통한 파이프라인 모니터링 임무도 가능해졌으며, 길게 이어지는 면제 신청 절차의 필요성도 사라졌습니다. 건설 및 유틸리티 인프라 확장의 둔화를 주된 요인으로 삼아, 성장률은 20%대 후반에 머물 것으로 예상되지만, 시장은 여전히 견조한 모습을 보이고 있습니다. AI 지원 페이로드에 대한 교체 수요가 여전히 높은 지출 수준을 뒷받침하고 있으며, 이는 해당 지역의 드론 데이터 서비스 시장의 꾸준한 성장을 보장하고 있습니다.

아시아태평양은 모든 지역 중 가장 높은 연평균 성장률(CAGR) 32.63%를 달성할 것으로 전망됩니다. 이러한 성장은 주로, 드론을 활용해 농촌 지역의 토지 구획을 매핑하는 것을 목표로 하는 인도의 'SVAMITVA' 농촌 조사 이니셔티브와, 효율적인 감시를 위해 드론 기술을 활용하는 중국의 대규모 송전선 점검 계약에 힘입어 이루어지고 있습니다. 인도에서는 드론 친화적인 세제 혜택 등 정부 정책이 업계의 성장을 뒷받침하고 있습니다. 또한, 인증 드론 조종사 수가 4만 명에 육박하는 등 증가세를 보이고 있으며, 이는 현지 서비스 제공업체의 확장을 견인하여 해당 지역에서 견고한 드론 운영 생태계를 구축하고 있습니다. 일본에서는 고령화와 방재 대책의 중요성이 부각되면서, 최근 체결된 ANA와 Wingtra의 제휴를 통해 하이브리드 VTOL 도입을 위한 새로운 가능성이 더욱 확대되고 있습니다.

유럽에서는 지역 전체의 드론 운용을 효율화하기 위한 U-Space의 도입으로 큰 혜택을 보고 있습니다. 그러나 회원국 간 공역 분류에 차이가 있어, 사업자는 여러 가지 규정 준수 요건을 동시에 충족해야 하므로 운영이 복잡해지고 있습니다. 중동 및 아프리카에서는 태양광 발전소의 열화상 촬영이나 장거리 파이프라인 점검에 드론이 점점 더 많이 활용되며, 중요 인프라의 감시 수요에 대응하고 있습니다. 한편, 남미에서는 다중 스펙트럼 분석 기능을 갖춘 드론을 활용해 농업 기법을 최적화하는 작업이 진행되고 있으며, 특히 사탕수수와 대두 농장에서는 비료 사용량을 최대 25%까지 줄이는 데 성공했습니다. 이러한 지역별 다양한 우선순위와 용도가 결합되어, 사람이 거주하는 모든 대륙에서 드론 데이터 서비스 시장의 견실한 성장을 견인하고 있으며, 이 분야의 적응력과 지속적인 확장 가능성을 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the drone data services market size is expected to be USD 3.14 billion in 2025, USD 4.17 billion in 2026, and reach USD 16.48 billion by 2031, growing at a CAGR of 31.63% from 2026 to 2031.

This report is Segmented by Service Type (Mapping and Surveying, Photogrammetry and 3D Modeling, and More), Platform Type (Multirotor Unmanned Aerial Vehicle, and More), End-User Industry (Agriculture, Energy and Utilities, Construction and Mining, Oil and Gas, Insurance, and More), Deployment Model (Cloud, On-Premise, and Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Drone Data Services Market Trends and Insights

Favorable BVLOS Regulations in Key Markets

Beyond-visual-line-of-sight allowances eliminate the need for on-site observers, cutting per-acre inspection costs by 40-60% for corridor mapping and crop monitoring. The United States Part 108 proposal, published in 2025, established performance-based criteria that allow certified operators to fly missions exceeding 50 kilometers without individual waivers. Europe's U-Space construct, effective January 2025, enables automated flight planning once electronic identification and geofencing safeguards are in place. Early regulatory clarity in these regions accelerates scale for energy and construction clients, while patchier implementation in parts of Asia delays similar benefits outside China and India.

Rapid Cost Decline in LiDAR and Photogrammetry Sensors

LiDAR modules priced below USD 20,000 now match the vertical accuracy once reserved for six-figure airborne systems, enabling mid-tier contractors to bid competitively on topographic projects. DJI's L3 unit undercut earlier Velodyne offerings by 60%, bringing three-centimeter precision within reach for survey firms and utilities. Parallel drops in 42-megapixel RGB payload prices are widening access to high-resolution photogrammetry, shifting competitive advantage firmly from hardware ownership toward cloud-based analytics that automatically surface anomalies in orthomosaics.

Fragmented Global Airspace Management Standards

Operators managing compliance across 193 regulatory regimes face significant challenges, as they must localize operational aspects such as manuals, insurance policies, and fleet telemetry systems. These requirements increase compliance costs by 25-40% and can extend launch timelines by up to 18 months. The International Civil Aviation Organization (ICAO) provides only general guidance, resulting in significant variations in approval processes across countries. For instance, Pakistan continues to prohibit Beyond Visual Line of Sight (BVLOS) flights, while India is actively expanding its digital-sky corridors to accommodate such operations. This regulatory complexity creates an environment that favors large service providers with strong regional presence, as they are better equipped to navigate these challenges. However, it also slows the progress of multi-country corridor projects, further delaying the implementation of cross-border drone operations.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Real-Time Asset Inspection in Energy and Utilities

- Growth of Digital Twins in Brownfield Industrial Sites

- Data-Privacy and Cybersecurity Concerns Among Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mapping and surveying produced 38.21% of 2025 revenue, demonstrating that the drone data services market remains rooted in core geospatial deliverables. However, delivery and logistics data services will expand at a 32.63% CAGR, driven by live telemetry that feeds route-optimization engines and proof-of-delivery systems. Alphabet's Wing reported 350,000 completed drops by late-2025, capturing precise GPS coordinates and weight variance data that refine predictive ETAs within 90 seconds of actual arrival. Environmental monitoring applications support carbon-credit MRV workflows, where platforms such as Pachama verified 18 million metric tons of CO2 in 2025, underscoring cross-industry appetite for automated validation tools.

In the second half of the decade, inspection and maintenance services will deepen revenue diversity as utilities and manufacturing clients outsource flight operations, point-cloud processing, and defect classification. Skyspecs alone processed 2.4 million wind-blade images in 2025, achieving 94% detection accuracy and reducing false positives by 40%. As pricing for USD 20,000 LiDAR systems compresses further, photogrammetry and 3D modeling workflows become accessible to mid-size contractors, pushing the drone data services market for these deliverables higher, even without headline-grabbing growth rates.

Multirotor craft held 61.72% of the 2025 drone data services market share thanks to their vertical takeoff and landing capability in tight urban or industrial areas. Yet battery limits cap flight times under 35 minutes, constraining corridor projects. Hybrid VTOL systems such as Quantum-Systems' Trinity F90+ can cover 400 hectares per sortie and still land inside a four-square-meter clearing, contributing to a 32.43% CAGR over the forecast horizon. Fixed-wing platforms maintain their niche in wide-area agriculture and cadastral work, while sub-250-gram nano craft continue to capitalize on lenient registration rules for real estate and insurance roof surveys.

As propulsion efficiencies improve and approach 250 watt-hours per kilogram, the latest hybrid airframes can cruise at 70 kilometers per hour for up to 2 hours. Additionally, these airframes can transition seamlessly to rotor hover, enabling precise data collection in targeted areas. This combination of extended endurance and precision targeting makes these hybrid models particularly well-suited for applications such as monitoring railways, pipelines, and power-line corridors. Previously, these tasks relied on more expensive manned aircraft or required coordinating multiple drones to cover the same areas. The adoption of these advanced hybrid airframes is driving significant growth and innovation in the drone data services market, as they offer a cost-effective, efficient solution for industries that require detailed, reliable data collection.

Geography Analysis

North America accounted for 41.48% of 2025 revenue in the drone data services market, driven by early FAA exemptions that reduced claim-cycle times by 40% in the insurance sector. These exemptions also facilitated 50-kilometer BVLOS (Beyond Visual Line of Sight) pipeline missions, eliminating the need for lengthy waiver processes. While growth is expected to moderate to the high twenties, primarily due to a slowdown in construction and utility build-outs, the market remains robust. Replacement demand for AI-ready payloads continues to sustain elevated spending levels, ensuring steady growth in the region's drone data services market.

Asia-Pacific is projected to achieve a compound annual growth rate (CAGR) of 32.63%, the highest among all regions. This growth is primarily driven by India's SVAMITVA rural survey initiative, which aims to map rural land parcels using drones, and China's large-scale power-line inspection contracts that leverage drone technology for efficient monitoring. In India, government policies, such as drone-friendly tax incentives, are fostering the industry's growth. Additionally, the growing number of certified drone pilots, which has reached nearly 40,000, is driving the expansion of local service providers, creating a robust ecosystem for drone operations in the region. Japan's aging population and disaster-preparedness priorities further extend runway for hybrid VTOL adoption under the newly inked ANA-Wingtra alliance.

Europe benefits significantly from the U-Space rollout, which aims to streamline drone operations across the region. However, variations in airspace classifications among member states compel operators to maintain parallel compliance channels, adding complexity to operations. In the Middle East and Africa, drones are increasingly used for solar park thermography and long-distance pipeline inspections, addressing critical infrastructure monitoring needs. Meanwhile, South America leverages drones equipped with multispectral analytics to optimize agricultural practices, particularly in sugarcane and soybean estates, where fertilizer usage has been reduced by up to 25%. These diverse regional priorities and applications collectively drive robust growth in the drone data services market across all inhabited continents, highlighting the sector's adaptability and potential for sustained expansion.

- Field Group

- DroneDeploy, Inc.

- Pix4D S.A.

- Skycatch, Inc.

- Kespry, Inc.

- senseFly S.A.

- Delair S.A.S.

- Aerodyne Group Sdn Bhd

- Terra Drone Corporation

- Measure UAS, Inc.

- Flyability SA

- AgEagle Aerial Systems Inc.

- AirMap, Inc.

- Altavian, Inc.

- DroneBase, Inc.

- Quantum-Systems GmbH

- HUVRdata, Inc.

- Wingtra AG

- Precision XYZ, LLC

- Skyspecs, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Favorable BVLOS Regulations in Key Markets

- 4.2.2 Rapid Cost Decline in LiDAR and Photogrammetry Sensors

- 4.2.3 Rising Demand for Real-Time Asset Inspection in Energy and Utilities

- 4.2.4 Growth of Digital Twins in Brown-Field Industrial Sites

- 4.2.5 Integration of Drone Data with Carbon-Credit MRV Platforms

- 4.2.6 Edge-AI-Powered Precision Spraying Data Feedback Loops

- 4.3 Market Restraints

- 4.3.1 Fragmented Global Airspace Management Standards

- 4.3.2 Data-Privacy and Cybersecurity Concerns Among Enterprises

- 4.3.3 Shortage of Certified Drone-Data Analysts

- 4.3.4 Volatility in Cloud-Processing Costs for High-Resolution Imagery

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Mapping and Surveying

- 5.1.2 Inspection and Maintenance

- 5.1.3 Photogrammetry and 3D Modeling

- 5.1.4 Environmental Monitoring and Research

- 5.1.5 Delivery and Logistics Data Services

- 5.2 By Platform Type

- 5.2.1 Multirotor Unmanned Aerial Vehicle

- 5.2.2 Fixed-Wing Unmanned Aerial Vehicle

- 5.2.3 Hybrid VTOL Unmanned Aerial Vehicle

- 5.2.4 Nano/Micro Unmanned Aerial Vehicle

- 5.3 By End-user Industry

- 5.3.1 Agriculture

- 5.3.2 Energy and Utilities

- 5.3.3 Construction and Mining

- 5.3.4 Oil and Gas

- 5.3.5 Transport and Logistics

- 5.3.6 Public Safety and Emergency Services

- 5.3.7 Insurance

- 5.3.8 Media and Entertainment

- 5.4 By Deployment Model

- 5.4.1 Cloud

- 5.4.2 On-Premise

- 5.4.3 Hybrid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Field Group

- 6.4.2 DroneDeploy, Inc.

- 6.4.3 Pix4D S.A.

- 6.4.4 Skycatch, Inc.

- 6.4.5 Kespry, Inc.

- 6.4.6 senseFly S.A.

- 6.4.7 Delair S.A.S.

- 6.4.8 Aerodyne Group Sdn Bhd

- 6.4.9 Terra Drone Corporation

- 6.4.10 Measure UAS, Inc.

- 6.4.11 Flyability SA

- 6.4.12 AgEagle Aerial Systems Inc.

- 6.4.13 AirMap, Inc.

- 6.4.14 Altavian, Inc.

- 6.4.15 DroneBase, Inc.

- 6.4.16 Quantum-Systems GmbH

- 6.4.17 HUVRdata, Inc.

- 6.4.18 Wingtra AG

- 6.4.19 Precision XYZ, LLC

- 6.4.20 Skyspecs, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment