|

시장보고서

상품코드

2063341

압전 액추에이터 및 모터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Piezoelectric Actuators And Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

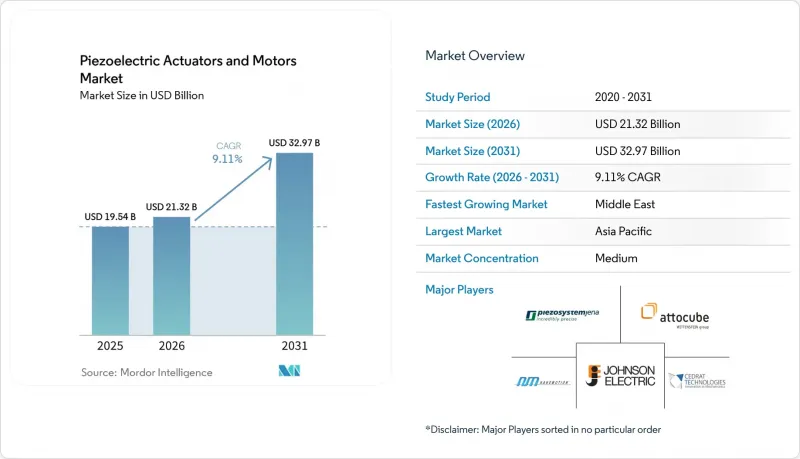

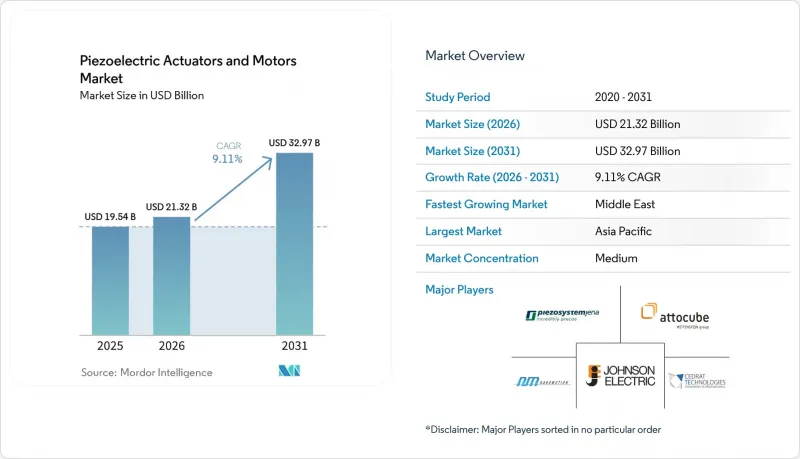

Mordor Intelligence에 의하면, 압전 액추에이터 및 모터 시장 규모는 2025년 195억 4,000만 달러로 평가되었습니다. 2026년 213억 2,000만 달러에서 확대해, 2031년까지 329억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR은 9.11%를 나타낼 전망입니다.

본 보고서는 제품 유형(스택형, 벤더/유니모프형, 기타), 작동 원리(준정적, 공진/초음파, 하이브리드 모드), 최종 사용자 산업(산업 및 제조, 자동차, 기타), 용도(정밀·나노 포지셔닝, 진동·모션 제어, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 압전 액추에이터 및 모터 시장 동향 및 인사이트

반도체 리소그래피 및 첨단 패키징 분야의 고정밀도 수요

3nm 이하의 디바이스 아키텍처로의 전환에 따라, 압전 액추에이터 및 모터 시장에서 특히 EUV 및 고NA EUV 리소그래피 장비 내에서의 압전 위치 제어의 중요성이 점점 더 커지고 있습니다. SPIE Advanced Lithography and Patterning 2026에 참석한 연구진은 EUV 오버레이 보정을 위해 필러 지지 기판에 통합된 3자유도(3-DOF) 박막 PZT 액추에이터를 발표했습니다. 이 액추에이터는 30 nm를 초과하는 변위와 서브 nm 수준의 반복 정밀도를 실현하고 있습니다. SPIE Advanced Packaging에서는 이러한 수요 추세가 더욱 뚜렷해지고 있습니다. 왜냐하면 웨이퍼 레벨 팬아웃이나 치플렛 본딩에는 10-9hPa까지의 클린룸 환경에서도 작동하며, 고출력이면서 저전압인 다층 적층 액추에이터가 필요하기 때문입니다. PI Ceramic GmbH는 2025년 3월, PICMA Stack의 리드 타임을 12주에서 4주로 단축하고, 공급업체가 장비 생산 확대를 신속하게 지원할 수 있도록 재고 및 생산 모델을 어떻게 재구축하고 있는지 보여주었습니다. 압전 액추에이터 및 모터 시장에서는 공급업체의 대응 시간이 단축됨에 따라 부품 제조업체들이 OEM 인증 과정에 깊이 관여하게 되며, 플랫폼이 승인되면 더 장기적인 상업적 락인 현상이 발생하게 됩니다.

의료용 외과 로봇에서 비자성 및 저소음 작동의 필요성

MRI 유도 로봇 공학은 압전 액추에이터 및 모터 시장이 비자성, 저소음, 소형 모션 시스템의 이점을 누리는 가장 대표적인 분야 중 하나로 자리 잡고 있습니다. Tekceleo는 2025년 7월, Wavelling 시리즈 초음파 모터를 탑재한 유니버시티 칼리지 런던(UCL)의 심장 카테터 검사용 로봇이, 팬텀 검사에서 100%의 시술 성공률을 달성했으며, 수동 기술에 비해 궤도 편차를 33.9% 감소시켰다고 보고했습니다. 이 결과는 형광 투시법을 대체하는 기법을 사용할 경우 방사선 피폭이 증가하는 MRI 보어 내에서 저소음 압전 구동 기술을 임상적 실용성과 직접적으로 연결한다는 점에서 중요합니다. 이와 유사한 요건은 로봇 보조 복강경 수술 및 하이컨텐츠 이미징 분야로도 확대되고 있으며, 이러한 분야에서는 전자기 구동으로 인해 열이나 전자기 간섭이 발생하여 인근 센서가 이를 견디지 못하는 상황이 발생합니다. 압전 액추에이터 및 모터 시장 전반에서 FDA 510(k) 및 CE 인증 요건 역시 적격 공급업체의 선택 폭을 좁히고 있으며, 의료 현장에서 성능이 입증된 플랫폼의 높은 가격 책정을 부추기고 있습니다.

고비용 시스템 대 전자기식 및 보이스 코일식 대체품

압전 액추에이터 및 모터 시장에서 시스템 가격은 여전히 가장 큰 상업적 장벽으로 남아 있습니다. 이는 액추에이터, 고전압 증폭기, 센서, 컨트롤러가 포장물에 포함되어 있기 때문입니다. 많은 산업용 사례에서 동등한 힘 및 변위 사양을 갖춘 전자기 서보 옵션과 비교하더라도 시스템 전체 비용은 여전히 3배에서 10배 더 높습니다. 이러한 격차는 특수 세라믹 제조, 전용 고전압 전자기기, 브러쉬리스 DC 모터 플랫폼에 비해 생산량이 훨씬 적기 때문입니다. 2025년 9월, PI는 OEM 구매 고객을 위해 납기 단축과 양산을 통한 비용 절감을 실현하는 ‘Nanopositioning and Micropositioning Essentials’ 시리즈를 발표했습니다. 이는 공급업체들이 이미 규모를 중시하는 포장을 통해 가격 장벽을 완화하려 하고 있음을 보여줍니다. 이러한 노력이 있음에도 불구하고, mm 단위의 정밀도로 충분하고 저비용 보이스 코일이나 서보 시스템이 여전히 허용되는 용도의 경우, 압전 액추에이터 및 모터 시장의 보급은 여전히 완만한 수준에 그치고 있습니다.

부문별 분석

2025년, 스택 액추에이터는 압전 액추에이터 및 모터 시장의 31.80%를 차지했으며, 소형 어셈블리에서 힘 밀도와 위치 결정 분해능을 동시에 달성하는 것이 여전히 어렵기 때문에 그 우위를 유지하고 있습니다. 압전 액추에이터 및 모터 시장에서 이러한 장치들은 웨이퍼 스테이지의 위치 결정, 마이크로플루이딕스공학 분야의 정밀 밸브 제어, 빔 핸들링 시스템의 고속 스티어링 미러 구동에서 핵심적인 역할을 수행하고 있습니다. 이러한 장치가 지원하는 용도에서는 힘, 속도, 정밀도 중 어느 하나뿐만 아니라 이 세 가지가 동시에 요구되므로, 그 역할은 앞으로도 흔들림 없이 지속될 것으로 보입니다. 벤더 액추에이터와 유니모프 액추에이터는 저비용 초음파 세척 및 이미징용 트랜스듀서 용도에서 여전히 중요한 역할을 하고 있는 반면, 증폭형 및 플렉처형은 벌크 세라믹의 기본적인 변형 한계를 초과하는 가동 범위를 지원합니다.

전단형 및 비틀림형 장치는 주사형 프로브 현미경이나 원자력 현미경 분야에서 규모는 작지만 고부가가치의 틈새 시장을 계속해서 차지하고 있습니다. 이러한 부문에서는 출하량보다는 기술적 적합성에 따라 단가가 결정됩니다. 초음파 모터, 특히 리니어 유형은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.28%를 나타낼 것으로 예측되며, 압전 액추에이터 및 모터 시장 전반에서 제품 혁신이 활발하게 이어질 전망입니다. Xeryon이 2026년에 XLA-10용으로 출시할 예정인 통합 컨트롤러는 폭 11.5mm에 10N의 힘을 발휘하며, 소형 디자인이 휴대용 진단 기기 및 소형 영상 시스템에서의 활용 범위를 넓히고 있음을 보여줍니다. 관성 모터와 피에조 워크 시스템은 특히 전자현미경 스테이지나 빔라인 광학계에서 긴 스트로크와 매우 높은 해상도를 동시에 확보해야 하는 상황에서 여전히 중요한 역할을 하고 있습니다. SmarAct의 SLC-1720은 22×17×8.5mm 크기에 서브 나노미터 해상도와 12mm 스트로크를 갖춘 폐쇄 루프 압전 스테이지로 발표되었으며, 이는 공간 제약이 있는 OEM 플랫폼에서 이러한 아키텍처의 적용 범위가 확대되고 있음을 보여줍니다.

2025년 압전 액추에이터 및 모터 시장 규모에서 공진형 및 초음파 시스템은 46.47%의 점유율을 차지했으며, 이는 자동 초점 구동 장치, 외과용 핸드피스, 광학 스티어링 어셈블리 등에서의 폭넓은 활용을 반영하고 있습니다. 이러한 장점은 휴대용 기기나 의료기기에 가장 적합한 소형 모터 구조, 저소음 작동, 전원이 꺼진 상태에서도 유지되는 성능에서 비롯됩니다. 준정적 동작은 고출력과 극히 짧은 스트로크가 허용되는 상황, 특히 나노 포지셔닝 스테이지나 정밀 밸브 구동 분야에서 여전히 중요합니다. 압전 액추에이터 및 모터 시장에서 준정적 모드와 공진 모드의 구분은 서로 대체되는 것보다는 서로 다른 작동 범위에 적합하도록 하는 측면이 더 강하다고 할 수 있습니다.

하이브리드 모드 시스템은 2031년까지 연평균 성장률(CAGR) 9.35%를 나타낼 것으로 예측되며, 이러한 성장세는 동일한 플랫폼에서 더 긴 스트로크와 nm 수준의 정상 응답을 모두 원하는 고객의 요구를 반영하고 있습니다. 압전 액추에이터 및 모터 산업은 시스템 설계 초기 단계에서 OEM에 특정 작동 모드를 강요하는 대신, 소프트웨어 제어 하에 공진 작동과 준정적 작동을 융합함으로써 이러한 요구에 부응하고 있습니다. 2026년 1월에 출시된 Physik Instrumente의 ‘6D NanoCube’는 폐쇄 루프형 피에조 플렉처 드라이브와 머신러닝으로 강화된 정렬 루틴을 탑재하여, 1초 이내에 커플링 작업을 완료함으로써 이러한 방향성을 보여주고 있습니다. SmarAct의 ISO 9001 : 2015 인증을 획득한 생산 체계는 전용 모션, 계측 및 자동화 유닛과 결합되어, 공급업체가 시스템 통합사업자의 인증 절차를 간소화하기 위해 모듈형 플랫폼을 어떻게 패키지화하고 있는지를 보여줍니다. 그 결과, 압전 액추에이터 및 모터 시장은 더 이상 하드웨어로 엄격하게 정의된 제품 범주가 아니라, 소프트웨어로 정의된 동작 양상으로 전환되고 있습니다.

지역별 분석

2025년, 아시아태평양은 압전 액추에이터 및 모터 시장 점유율의 40.75%를 차지했으며, 이러한 우위는 해당 지역의 반도체 팹, 가전 OEM, 정밀 제조 공급망의 집적에 기인합니다. 중국, 일본, 한국, 대만은 전 세계 첨단 로직 및 메모리 생산 능력의 상당 부분을 차지하고 있으며, 리소그래피 및 검사에 사용되는 스택 액추에이터, 초음파 모터, 나노 포지셔닝 시스템에 대한 안정적인 수요를 창출하고 있습니다. 이러한 확고한 산업 기반은 개별 하류 부문의 상황이 위축되더라도 아시아태평양의 압전 액추에이터 및 모터 시장에 강력한 수요 기반을 제공합니다. 일본에서는 Murata Manufacturing, 교세라, TDK와 같은 기업들이 소재, 부품, 완제품 시스템 등 각 부문에서 사업을 전개하고 있어, 공급망의 깊이가 특히 두드러집니다. 교세라가 2025년 2월 TactoTek에 500만 유로(540만 달러)를 투자한 것은 지역 공급업체들이 피에조 기술의 적용 분야를 자동차용 햅틱스 및 커넥티드 기기의 인터페이스로 확대하고 있음을 보여줍니다.

북미와 유럽은 정밀 기기 OEM 기업, 방위 관련 기업, 생명과학 기기 제조업체가 집중되어 있는 점을 배경으로, 2025년에는 매출 규모 2위를 기록했습니다. 독일은 Physik Instrumente, PI Ceramic, SmarAct, Piezosystem Jena, Attocube와 같은 기업들이 긴밀한 엔지니어링 클러스터를 형성하고 있어, 압전 액추에이터 및 모터 시장의 핵심 설계 거점으로 자리매김하고 있습니다. PI가 2025년 가을, 매사추세츠주 슈루즈베리에 14만 제곱피트 규모의 새로운 생산 시설을 확장한 것은 북미의 반도체 및 포토닉스 고객사와 가까운 곳으로의 리쇼어링을 추진하려는 더 광범위한 추세를 반영한 것입니다. PI(미국), 프랑스의 CEA-Leti, 독일의 프라운호퍼 IKTS는 상용 VLSI 공정과 호환되는 KNN 기반 기술 및 관련 소재의 연구 개발을 추진함으로써, 무연 압전 기술 개발 분야에서 유럽의 위상을 강화하고 있습니다.

중동의 압전 액추에이터 및 모터 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.44%로 확대될 것으로 전망됩니다. 이러한 성장 속도는 장기적인 국가 개발 프로그램의 일환으로 진행되는 정밀 제조, 국방 현대화, 의료 인프라에 대한 공공 투자와 관련이 있습니다. 이스라엘은 이 지역에서 두드러진 존재로 자리매김하고 있습니다. 이는 2025년에 나노모션사가 반도체 계측용으로 0.25nm의 분해능과 1nm 이하의 안정성을 갖춘 프로토타입 위치 결정 스테이지를 납품했기 때문입니다. 아프리카와 남미는 여전히 초기 단계 시장이지만, 조립 및 사후 서비스 지원의 현지화가 진전되면 예측 기간 동안 압전 액추에이터 및 모터의 도입이 점차 확대될 것으로 전망됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the piezoelectric actuators and motors market size is expected to increase from USD 19.54 billion in 2025 and USD 21.32 billion in 2026 and reach USD 32.97 billion by 2031, growing at a CAGR of 9.11% over 2026-2031.

This report is Segmented by Product Type (Stack, Bender/Unimorph, and More), Operation Principle (Quasi-Static, Resonant/Ultrasonic, and Hybrid-Mode), End-User Industry (Industrial and Manufacturing, Automotive, and More), Application (Precision and Nanopositioning, Vibration and Motion Control, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Piezoelectric Actuators And Motors Market Trends and Insights

Semiconductor Lithography And Advanced Packaging Precision Demand

The move toward sub-3 nm device architectures has made piezoelectric positioning increasingly central to the piezoelectric actuators and motors market, especially inside EUV and high-NA EUV lithography tools. Researchers at SPIE Advanced Lithography and Patterning 2026 presented a 3-DOF thin-film PZT actuator integrated into pillar-supported substrates for EUV overlay correction, with displacement above 30 nm and sub-nanometer repeatability. SPIE Advanced Packaging is reinforcing this demand pattern because wafer-level fan-out and chiplet bonding require high-force, low-voltage multilayer stack actuators that also operate in cleanroom-compatible environments down to 10-9 hPa. PI Ceramic GmbH reduced PICMA Stack lead times from 12 weeks to 4 weeks in March 2025, showing how suppliers are reshaping inventory and production models to support faster equipment ramp-ups. In the piezoelectric actuators and motors market, tighter supplier response times are pushing component makers deeper into OEM qualification cycles and creating longer commercial lock-in once a platform is approved.

Medical And Surgical Robotics Need For Non-Magnetic Silent Motion

MRI-guided robotics remains one of the clearest areas where the piezoelectric actuators and motors market benefits from non-magnetic, quiet, and compact motion systems. Tekceleo reported in July 2025 that a University College London cardiac catheterization robot powered by Wavelling series ultrasonic motors achieved a 100% procedural success rate in phantom testing and reduced trajectory deviation by 33.9% compared with the manual technique. That result matters because it ties silent piezo motion directly to clinical usability inside the MRI bore, where fluoroscopy alternatives raise radiation exposure. The same requirement is extending into robotic-assisted laparoscopy and high-content imaging, where electromagnetic drives introduce heat and electromagnetic interference that nearby sensors cannot tolerate. Across the piezoelectric actuators and motors market, FDA 510(k) and CE qualification steps also narrow the field of acceptable suppliers, which supports premium pricing for platforms with verified performance in medical settings.

High System Cost Versus Electromagnetic And Voice-Coil Alternatives

System pricing remains the largest commercial barrier in the piezoelectric actuators and motors market because the total package includes the actuator, high-voltage amplifier, sensor, and controller. In many industrial use cases, the full system cost still runs 3 to 10 times above comparable electromagnetic servo options for similar force and displacement requirements. The gap is tied to specialized ceramic production, dedicated high-voltage electronics, and far lower manufacturing volumes than brushless DC motor platforms. In September 2025, PI introduced its Nanopositioning and Micropositioning Essentials range to offer shorter delivery times and volume savings for OEM buyers, which shows that suppliers are already trying to soften the price barrier through scale-oriented packaging. Even with those efforts, the piezoelectric actuators and motors market continues to see slower penetration in applications where millimeter-level accuracy is sufficient and lower-cost voice-coil or servo systems remain acceptable.

Other drivers and restraints analyzed in the detailed report include:

- Optical Alignment And Photonics Proliferation In Datacom And Imaging

- Miniaturized Consumer Camera And Sensing Modules

- Control Electronics And Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stack actuators held 31.80% of the piezoelectric actuators and motors market share in 2025, and they kept that lead because force density and positioning resolution remain difficult to match in compact assemblies. Within the piezoelectric actuators and motors market, these devices are at the center of wafer-stage positioning, precision valve control in microfluidics, and fast-steering mirror actuation in beam-handling systems. Their role remains durable because the applications they support require force, speed, and accuracy simultaneously, not just one of those characteristics. Bender and unimorph actuators remain important in lower-cost ultrasonic cleaning and imaging transducer uses, while amplified and flexure types serve motion ranges that exceed the basic strain limit of bulk ceramics.

Shear and torsional devices continue to occupy smaller but high-value niches in scanning probe microscopy and atomic force microscopy, where unit pricing is supported by technical fit rather than shipment volume. Ultrasonic motors, specifically linear variants, are projected to grow at a 9.28% CAGR from 2026 to 2031, keeping product innovation active across the piezoelectric actuators and motors market. Xeryon's planned 2026 integrated-controller release for the XLA-10, offering 10 N force in an 11.5 mm width, shows how smaller formats are widening use in portable diagnostics and compact imaging systems. Inertia motors and piezo-walk systems still matter where long travel and very high resolution have to coexist, especially in electron microscopy stages and beamline optics. SmarAct's SLC-1720, described as a closed-loop piezo stage at 22 X 17 X 8.5 mm with sub-nanometer resolution and 12 mm stroke, shows how space-limited OEM platforms are expanding the addressable range of these architectures.

Resonant and ultrasonic systems accounted for 46.47% share of the piezoelectric actuators and motors market size in 2025, reflecting their broad use in autofocus drives, surgical handpieces, and optical steering assemblies. Their lead comes from compact motor formats, silent operation, and power-off holding behavior that are well-suited to portable and medical devices. Quasi-static operation remains important where high force and very short travel are acceptable, especially in nanopositioning stages and precision valve actuation. In the piezoelectric actuators and motors market, the split between quasi-static and resonant modes is less about replacing one another and more about matching different motion envelopes.

Hybrid-mode systems are projected to grow at a 9.35% CAGR through 2031, and that pace reflects customers' desire for both longer travel and nanometer-level settling on the same platform. The piezoelectric actuators and motors industry is responding to that need by blending resonant and quasi-static behavior under software control, rather than forcing OEMs to choose one operating mode early in system design. Physik Instrumente's 6D NanoCube, launched in January 2026, illustrates this direction with closed-loop piezo flexure drives and machine-learning-enhanced alignment routines that complete coupling tasks in under 1 second. SmarAct's ISO 9001:2015-certified production setup, along with its dedicated motion, metrology, and automation units, demonstrates how suppliers are packaging modular platforms to simplify qualification for integrators. As a result, the piezoelectric actuators and motors market is moving toward software-defined motion behavior rather than strictly hardware-defined product categories.

Geography Analysis

Asia-Pacific held 40.75% of the piezoelectric actuators and motors market share in 2025, and that lead came from the region's concentration of semiconductor fabs, consumer electronics OEMs, and precision manufacturing supply chains. China, Japan, South Korea, and Taiwan host much of the world's advanced logic and memory capacity, creating a steady demand for stack actuators, ultrasonic motors, and nanopositioning systems used in lithography and inspection. That installed industrial base provides the piezoelectric actuators and motors market with a strong demand anchor in Asia-Pacific, even when conditions soften in individual downstream sectors. Japan's supply chain remains especially deep because companies such as Murata, Kyocera, and TDK operate across materials, components, and finished systems. Kyocera's February 2025 investment of EUR 5 million (USD 5.4 million), in TactoTek showed how regional suppliers are also extending piezo use into automotive haptics and connected-device interfaces.

North America and Europe formed the second-largest revenue bloc in 2025, supported by the concentration of precision instrument OEMs, defense contractors, and life science equipment makers. Germany remains a core design center for the piezoelectric actuators and motors market because it hosts Physik Instrumente, PI Ceramic, SmarAct, Piezosystem Jena, and Attocube within a tight engineering cluster. PI's planned expansion into a new 140,000 sq ft production facility in Shrewsbury, Massachusetts, with a Fall 2025 target, reflected the broader reshoring push closer to semiconductor and photonics customers in North America. PI-USA France's CEA-Leti and Germany's Fraunhofer IKTS strengthen Europe's position in lead-free piezo development by advancing KNN-based and related material work compatible with commercial VLSI processes.

The piezoelectric actuators and motors market in the Middle East is projected to expand at a 9.44% CAGR between 2026 and 2031. That pace is linked to public investment in precision manufacturing, defense modernization, and healthcare infrastructure under long-horizon national development programs. Israel stands out in this region because Nanomotion delivered a prototype positioning stage with 0.25 nm resolution and sub-1 nm stability for semiconductor metrology in 2025. Africa and South America remain early-stage markets, but wider localization of assembly and after-sales support should still support the gradual uptake of piezoelectric actuators and motors over the forecast period.

- Piezosystem Jena GmbH

- Attocube Systems GmbH

- Nanomotion Ltd.

- Johnson Electric Holding Ltd.

- Cedrat Technologies SA

- Piezomotor Uppsala AB

- New Scale Technologies, Inc.

- Mad City Labs, Inc.

- PiezoDrive Pty Ltd

- APC International, Ltd.

- CoreMorrow Ltd.

- Xeryon Inc.

- Dynamic Structures and Materials, LLC

- Kinetic Ceramics, LLC

- TDK Corporation

- Kyocera Corporation

- NGK Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Semiconductor Lithography and Advanced Packaging Precision Demand

- 4.2.2 Medical and Surgical Robotics Need for Non-Magnetic Silent Motion

- 4.2.3 Optical Alignment and Photonics Proliferation in Datacom and Imaging

- 4.2.4 Miniaturized Consumer Camera and Sensing Modules

- 4.2.5 RoHS-Driven Shift to Lead-Free Piezo Platforms

- 4.2.6 Closed-Loop Smart Motion Architectures With AI Compensation

- 4.3 Market Restraints

- 4.3.1 High System Cost Versus Electromagnetic and Voice-Coil Alternatives

- 4.3.2 Control Electronics and Integration Complexity

- 4.3.3 Lead-Free Material Performance Gap and Requalification Burden

- 4.3.4 Wear, Drift, and Lifetime Validation in High-Duty Ultrasonic and Stick-Slip System

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Stack Actuators

- 5.1.2 Bender/Unimorph Actuators

- 5.1.3 Amplified/Flexure Actuators

- 5.1.4 Shear/Torsional Actuators

- 5.1.5 Ultrasonic Motors - Rotary

- 5.1.6 Ultrasonic Motors - Linear

- 5.1.7 Inertia (Stick-Slip) Motors

- 5.1.8 Piezo-Walk / Step Motors

- 5.2 By Operation Principle

- 5.2.1 Quasi-Static (Direct)

- 5.2.2 Resonant / Ultrasonic

- 5.2.3 Hybrid-Mode

- 5.3 By End-user Industry

- 5.3.1 Industrial and Manufacturing

- 5.3.2 Automotive

- 5.3.3 Medical and Life Sciences

- 5.3.4 Aerospace and Defense

- 5.3.5 Consumer Electronics

- 5.3.6 Energy and Power

- 5.3.7 Research and Academia

- 5.4 By Application

- 5.4.1 Precision and Nanopositioning

- 5.4.2 Vibration and Motion Control

- 5.4.3 Fluid Handling and Valves

- 5.4.4 Imaging and Optics Focus

- 5.4.5 Robotics and Micromanipulation

- 5.4.6 Energy-Harvesting Systems

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Piezosystem Jena GmbH

- 6.4.2 Attocube Systems GmbH

- 6.4.3 Nanomotion Ltd.

- 6.4.4 Johnson Electric Holding Ltd.

- 6.4.5 Cedrat Technologies SA

- 6.4.6 Piezomotor Uppsala AB

- 6.4.7 New Scale Technologies, Inc.

- 6.4.8 Mad City Labs, Inc.

- 6.4.9 PiezoDrive Pty Ltd

- 6.4.10 APC International, Ltd.

- 6.4.11 CoreMorrow Ltd.

- 6.4.12 Xeryon Inc.

- 6.4.13 Dynamic Structures and Materials, LLC

- 6.4.14 Kinetic Ceramics, LLC

- 6.4.15 TDK Corporation

- 6.4.16 Kyocera Corporation

- 6.4.17 NGK Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment