|

시장보고서

상품코드

2063342

자재관리 장비 텔레매틱스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Material Handling Equipment Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

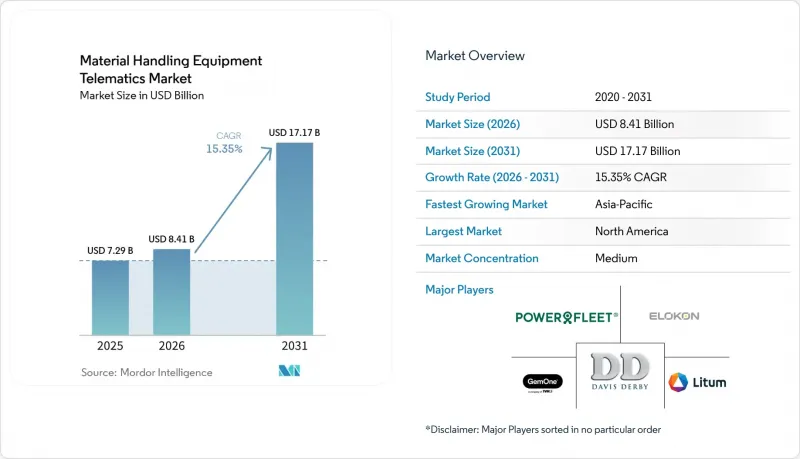

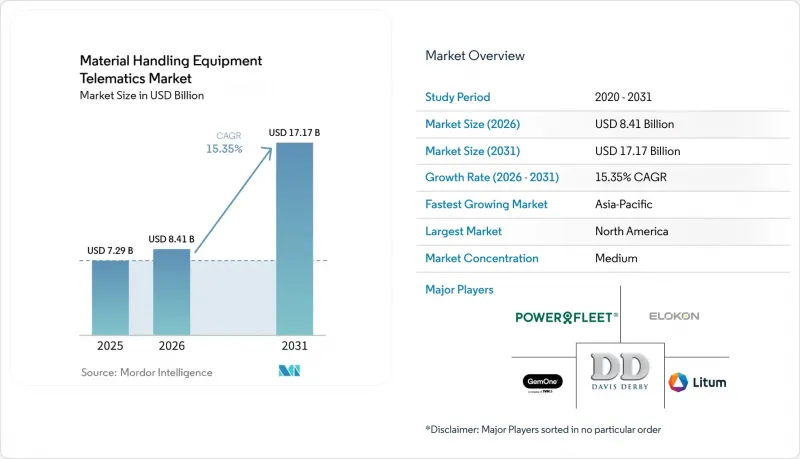

Mordor Intelligence에 의하면, 자재관리 장비 텔레매틱스 시장 규모는 2025년 72억 9,000만 달러로 평가되었습니다. 2026년에는 84억 1,000만 달러로 확대되어 2031년까지 171억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR은 15.35%를 나타낼 전망입니다.

본 보고서는 장비 유형(지게차, 크레인, 무인 운반차(AGV), 기타), 솔루션 유형(자산 추적, 차량 관리, 기타), 최종 사용자 산업(제조, 물류 및 창고, 기타), 기술(GPS, IoT 센서, AI 기반 예측 시스템, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자재관리 장비 텔레매틱스 시장 동향 및 인사이트

창고 자동화와 전자상거래 주문 처리 밀도 증가

자재관리 장비 텔레매틱스 시장은 더욱 엄격해진 처리 능력 목표와 높은 장비 밀도 하에서 운영되는 창고 환경에서 그 성장세가 가속화되고 있습니다. 시설의 자동화가 진행됨에 따라, 관리자가 가동률, 혼잡 구역, 안전 관련 상황을 실시간으로 파악할 수 있도록 더 많은 자산을 지속적으로 모니터링해야 합니다. 이러한 수요에 따라 텔레매틱스는 위치 추적의 범위를 넘어 지게차, 로봇, 부두 작업 전반에 걸친 보다 광범위한 제어 역할로 그 영역을 확장하고 있습니다. OneTrack에 따르면, AI를 활용한 차량 관리 인텔리전스는 잉여 용량이나 가동률이 낮은 장비를 파악함으로써 차량 운영 비용을 15-25% 절감할 수 있다고 합니다. 이는 함대의 적정 규모화를 목표로 하는 현재의 추세와 부합합니다. 고밀도 물류 처리 환경에서 모니터링되지 않는 장비는 더 큰 운영 위험을 초래하기 때문에 자재관리 장비 텔레매틱스 시장은 이러한 변화에 효과적으로 대응하고 있습니다. 그 결과, 텔레매틱스는 단순한 모니터링 도구가 아니라 자동 창고 운영 로직의 일부로 자리 잡고 있습니다.

함대 가동률 향상 및 가동 중단 시간 단축에 대한 수요 증가

신속한 대응이 요구되는 창고 및 공장 업무에서 피할 수 있는 가동 중단으로 인한 비용 증가 역시 자재관리 장비 텔레매틱스 시장을 견인하고 있습니다. 사업자들은 어떤 차량이 유휴 상태인지, 어떤 유닛이 과부하 상태인지, 고장으로 인해 근무가 중단되기 전에 유지보수 위험이 어디에 누적되고 있는지를 보여주는 시스템을 점점 더 요구하고 있습니다. 이에 따라 구매 우선순위가 단순한 시각화에서 가동률 관리 및 예방 조치로 전환되고 있습니다. MHS Lift는 지게차 차량군의 예측 유지보수가 기계의 건전성 지표를 지속적으로 모니터링하는 데 달려 있으며, 이를 통해 팀이 문제가 고장으로 발전하기 전에 대처할 수 있다고 지적하고 있습니다. 실용적인 관점에서 볼 때, 자재관리 장비 텔레매틱스 시장이 성장세를 보이고 있는 이유는 적절한 규모 선정과 유지보수 계획이 광범위한 자동화 프로젝트보다 더 신속하게 가치를 창출하는 경우가 많기 때문입니다. 이러한 짧은 투자 회수 주기로 인해, 신속한 업무 효율화가 필요한 시설에서 텔레매틱스 도입의 타당성을 입증하기가 더 쉬워졌습니다.

높은 개조·통합·변경 관리 비용

높은 개조 및 통합 비용은 특히 구형 장비나 여러 브랜드의 장비를 운영하는 사업자에게 있어 자재관리 장비 텔레매틱스 시장의 실질적인 장벽이 되고 있습니다. 공장 출하 시에 내장된 시스템은 도입이 용이하지만, 많은 차량 소유주들은 여전히 구형 장비에 의존하고 있어 데이터를 표준화하려면 추가 하드웨어, 맞춤형 배선 및 프로토콜 브리지가 필요합니다. 텔레매틱스를 창고 관리 시스템, ERP 도구, 현장 고유의 워크플로우 규칙과 연동해야 하는 경우, 통합은 더욱 어려워집니다. 과제는 설비 투자뿐만이 아닙니다. 감독자, 기술자, 사업자가 동시에 새로운 디지털 프로세스를 도입해야 하는 경우, 변경 관리의 부담도 커집니다. 소규모 사업자의 경우, 사내에 IT 및 OT 지원 체계가 갖춰져 있지 않은 경우가 많아 이러한 압박을 더욱 크게 느끼고 있습니다. 이러한 비용이나 도입의 장벽으로 인해, 텔레매틱스의 장기적인 이점이 분명하더라도 의사결정이 지연될 가능성이 있습니다.

부문별 분석

지게차는 2025년 자재관리 장비 텔레매틱스 시장 점유율의 41.28%를 차지하며, 물류, 제조, 소매, 콜드체인 업무에서 핵심적인 역할을 계속 수행해 가장 큰 장비 카테고리로 자리매김했습니다. 이러한 우위는 임베디드형 연결 기능, 사업자 관리 도구, 서비스 연동 데이터 레이어에 대한 OEM 각사의 오랜 기간에 걸친 투자도 반영하고 있습니다. 레이먼드 코퍼레이션은 자사의 ‘iWAREHOUSE Enterprise’ 시스템이 차량 인증 관리, 충돌 알림, 배터리 분석을 단일 차량 관리 인텔리전스 플랫폼에 통합하고 있다고 밝혔습니다. 토요타 자재관리 역시 MyInsights를 연결된 지게차의 규정 준수, 사용 현황 가시화, 배터리 관련 모니터링을 지원하는 네이티브 텔레매틱스 계층으로 자리매김하고 있습니다. 자재관리 장비 텔레매틱스 시장에서 크레인, 텔레핸들러, 야드용 차량에도 텔레매틱스 기능을 도입하는 추세가 강해지고 있지만, 그 도입 기반은 지게차만큼 표준화되어 있지 않습니다. 이러한 차이점 때문에 지게차는 여전히 대부분의 차량 디지털화 프로그램에서 핵심적인 위치를 차지하고 있습니다.

AGV(무인 운반차)는 2031년까지 연평균 성장률(CAGR) 15.41%를 기록하며 성장할 것으로 예상되며, 자재관리 장비 텔레매틱스 시장에서 가장 빠르게 성장하는 장비 부문으로 자리매김하고 있습니다. AGV 시스템은 채널 설정, 배터리 상태, 교통 로직, 작업 할당에 대한 지속적인 조정에 의존하기 때문에 그 텔레매틱스 요구 사항은 구조적으로 다릅니다. KINEXON은 자사의 AMR 및 AGV 환경용 플릿 매니저가 통합된 오케스트레이션과 VDA 5050 표준 준수를 지원하며, 이는 소프트웨어 주도형 플릿 제어로의 전환을 반영한다고 밝혔습니다. 이 점은 중요합니다. 왜냐하면 AGV의 성장은 단순히 연결된 차량의 수를 늘리는 데 그치지 않고, 텔레매틱스의 역할을 능동적인 내부 물류 제어 영역으로 확대하기 때문입니다. 따라서 자재관리 장비 텔레매틱스 산업은 사업자 중심의 지게차 모니터링에서 자율 주행 차량 전체에 걸친 머신-투-시스템(M2S) 오케스트레이션으로 확대되고 있습니다. 실내 또는 반실내 환경에서 사용되는 고소 작업차 및 토목 건설 기계는 규모는 작지만 신흥 시장 부문으로, 각 업체들은 더욱 복잡해지는 위치 정보 요구 사항에 맞추어 텔레매틱스를 적용하고 있습니다.

2025년 기준으로, 차량 관리는 자재관리 장비 텔레매틱스 시장의 34.36%를 차지했으며, 대부분의 도입 사례에서 기반이 되는 솔루션 계층으로서의 역할이 확인되었습니다. 구매자들은 여전히, 보다 심층적인 분석으로 확대하기 전에 자산 시각화, 사업자 인증, 디지털 점검, 사용 현황 대시보드부터 도입을 시작하는 경향이 있습니다. 이 순서가 중요한 이유는 이러한 기본 기능들이 이후의 안전, 유지보수, 생산성 향상을 위한 용도의 기반이 되기 때문입니다. 도요타와 레이몬드는 모두 규정 준수 기록, 접근 제어, 이용 현황의 가시화가 단일 운영 화면 내에 통합된, 이 종합적인 차량 관리 모델을 기반으로 한 텔레매틱스 서비스를 제공합니다. 자재관리 장비 텔레매틱스 시장에서 자산 추적 및 안전 모니터링은 긴급한 운영 요구 사항을 충족시키고 투자 회수 경로가 명확하기 때문에 여전히 초기 단계 지출의 대부분을 차지하고 있습니다. 또한, 전기차 차량군이 확대되고 교대 근무를 넘나들며 배터리 사용을 보다 신중하게 관리해야 할 필요성이 커짐에 따라, 에너지 최적화의 중요성도 커지고 있습니다.

예지 보전은 2031년까지 연평균 성장률(CAGR) 15.56%를 나타낼 것으로 예측되며, 자재관리 장비 텔레매틱스 시장에서 가치 창출 구조가 재편되기 시작한 부문입니다. MHS Lift는 예측 유지보수를 엔진 온도, 배터리 상태, 유압 성능 및 기타 장비의 상태와 관련된 센서 데이터를 바탕으로 구축된 모델로 정의하며, 이를 통해 고장이 발생하기 전에 문제를 해결할 수 있습니다. 이러한 접근 방식을 통해 텔레매틱스는 단순한 모니터링 도구에서 비용 관리 도구로 변모하게 됩니다. 왜냐하면 가장 가치 있는 성과는 과거의 보고가 아니라, 업무의 혼란을 미연에 방지하는 것이기 때문입니다. 또한, 원시 데이터를 기술자나 관리자가 실행 가능한 명확한 유지보수 조치로 변환해 줄 수 있는 공급업체의 중요성도 커지고 있습니다. 따라서 자재관리 장비 텔레매틱스 산업은 단순히 무슨 일이 발생했는지를 보여줄 뿐만 아니라, 다음에 무엇을 해야 할지를 지시하는 시스템으로 전환되고 있습니다. 장비의 안전성과 관련된 규정 준수 요건 또한 설계 선택에 영향을 미치고 있으며, 이를 통해 보다 체계적이고 감사 가능한 예측 유지보수 워크플로우가 지원되고 있습니다.

지역별 분석

2025년, 북미는 자재관리 장비 텔레매틱스 시장 점유율의 38.54%를 차지했습니다. 이 지역은 첨단 창고 인프라, OEM 텔레매틱스의 높은 보급률, 안전 문서화 및 사업자 관리에 중점을 둔 규제 환경의 혜택을 누리고 있습니다. OSHA(미국 산업안전보건청)의 동력 구동 산업용 트럭에 관한 기준은 창고 및 산업 현장에서의 교육, 운용, 기록 관리와 관련된 사업자의 의무를 계속해서 규정하고 있습니다. 미국은 보유 차량 수가 많고, 자동화에 할당된 예산이 풍부하며, 여러 거점에 걸친 운영 관리가 일반적이기 때문에 여전히 주요 수요 거점으로 자리 잡고 있습니다. 또한, 텔레매틱스가 안전성, 가시성, 국경을 넘는 차량 운영 분야로 확대되는 가운데, 캐나다와 멕시코도 이 지역 전체의 성장세를 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.83%를 기록하며 성장할 것으로 예상되며, 자재관리 장비 텔레매틱스 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이 지역은 제조업의 다각화, 전자상거래 물류 네트워크의 확대, 자동화 물류 인프라에 대한 광범위한 투자의 혜택을 누리고 있습니다. 인도, 한국, 동남아시아, 동아시아 일부 지역에서는 신규 시설이 기존 부지 배치를 개조하는 대신 처음부터 연결형 시스템을 도입할 수 있기 때문에 텔레매틱스 분야에 새로운 기회가 생겨나고 있습니다. 이는 새로운 창고나 산업용 건물에서 기존 시설보다 차량 관리 소프트웨어, 센서, 디지털 워크플로를 보다 원활하게 통합할 수 있다는 점에서 중요합니다. 그 결과, 자재관리 장비 텔레매틱스 시장은 아시아태평양 전체에서 성장세를 보이고 있으며, 그 요인은 물량 증가뿐만 아니라 소프트웨어 도입에 적합한 운영 기반의 구축에도 있습니다.

유럽은 자재관리 장비 텔레매틱스 시장에서 여전히 3위의 규모를 자랑하며, 엄격한 규제와 성숙한 공급업체 생태계가 두드러집니다. 해당 지역의 조달 기준에서는 정보 보안, 상호 운용성, 문서화된 운영 관리가 특히 중시되고 있습니다. SYNAOS는 자사의 인트라로지스틱스 플랫폼에 대한 ISO 27001 인증을 강조하고 있으며, 이는 유럽 구매자들 사이에서 제품 인증에 있어 보안 조치의 중요성이 점점 더 커지고 있음을 반영하고 있습니다. 또한 Trackunit은 2025년 하반기에 Sunbelt Rentals UK 및 아일랜드와의 제휴를 확대하여, IrisX 플랫폼을 통해 오프로드 부문에서 연결된 자산의 커버리지를 넓혔습니다. 남미, 중동 및 아프리카는 소규모 기반에서 발전하고 있으며, 건설, 광업, 물류 프로젝트가 도입의 여지를 마련하고 있지만, 개조 및 설치 비용과 거버넌스 체계의 정비 상황이 여전히 급속한 확장을 제한하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the material handling equipment telematics market size is expected to increase from USD 7.29 billion in 2025 to USD 8.41 billion in 2026 and reach USD 17.17 billion by 2031, growing at a CAGR of 15.35% over 2026 to 2031.

This report is Segmented by Equipment Type (Forklifts, Cranes, Automated Guided Vehicles (AGVs), and More), Solution Type (Asset Tracking, Fleet Management, and More), End-User Industry (Manufacturing, Logistics and Warehousing, and More), Technology (GPS, Iot Sensors, AI-Based Predictive Systems, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Material Handling Equipment Telematics Market Trends and Insights

Rising Warehouse Automation And E-Commerce Fulfillment Density

The material handling equipment telematics market is gaining traction in warehouse environments that now operate under tighter throughput targets and higher equipment density. As facilities add more automation, more assets must be continuously monitored so managers can see utilization, congestion points, and safety events in real time. That need is pushing telematics beyond location tracking and into a wider control role across forklift, robot, and dock activity. OneTrack states that AI-driven fleet intelligence can reduce fleet costs by 15-25% by identifying excess capacity and underused equipment, which fits the current drive toward tighter fleet sizing. The material handling equipment telematics market is responding well to this shift because unmonitored equipment now creates a larger operational risk in high-density fulfillment settings. As a result, telematics is becoming part of the operating logic of automated warehouses rather than a separate monitoring tool.

Growing Need For Fleet Utilization And Downtime Reduction

The rising cost of avoidable downtime in fast-moving warehouse and plant operations is also lifting the material handling equipment telematics market. Operators increasingly want systems that show which vehicles are idle, which units are overworked, and where maintenance risk is building before a failure interrupts a shift. This is changing buying priorities from simple visibility toward utilization management and preventive action. MHS Lift notes that predictive maintenance in forklift fleets relies on continuous monitoring of machine health indicators so teams can address issues before they become breakdowns. In practical terms, the material handling equipment telematics market is gaining strength because right-sizing and maintenance planning often deliver value faster than broader automation projects. That shorter payback cycle makes telematics easier to justify in facilities that need quick operational gains.

High Retrofit, Integration, And Change-Management Costs

High retrofit and integration costs remain a real brake on the material handling equipment telematics market, especially for operators running older equipment or mixed-brand fleets. Factory-fitted systems are easier to deploy, but many fleet owners still depend on legacy units that need additional hardware, custom wiring, and protocol bridging before data can be standardized. Integration becomes even more challenging when telematics must connect with warehouse management systems, ERP tools, and site-specific workflow rules. The challenge is not only capital spending; change management demands also rise when supervisors, technicians, and operators have to adopt new digital processes simultaneously. Smaller operators feel this pressure more sharply because they often lack in-house IT and OT support. These cost and implementation hurdles can delay decisions even when the long-term case for telematics is clear.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Cloud, IoT, And AI-Enabled Remote Diagnostics

- Tightening Safety And Compliance Requirements For Powered Industrial Trucks

- Cybersecurity And Data Governance Risks In Multi-Site Fleets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Forklifts held 41.28% of the material handling equipment telematics market share in 2025, making them the largest equipment category, as they remain central to logistics, manufacturing, retail, and cold-chain operations. Their lead also reflects long-standing OEM investment in embedded connectivity, operator management tools, and service-linked data layers. The Raymond Corporation states that its iWAREHOUSE Enterprise system combines vehicle certification management, impact notifications, and battery analytics into a single fleet intelligence platform. Toyota Material Handling also positions MyInsights as a native telematics layer that supports compliance, usage visibility, and battery-related monitoring on connected forklifts. In the material handling equipment telematics market, cranes, telehandlers, and yard-oriented vehicles are increasingly adopting telematics features, but their adoption base is less standardized than forklifts. That difference keeps forklifts at the center of most fleet digitization programs.

AGVs are projected to grow at a 15.41% CAGR through 2031, making them the fastest-growing equipment category in the material handling equipment telematics market. Their telematics needs are structurally different because AGV systems depend on continuous coordination of routing, battery status, traffic logic, and task assignment. KINEXON states that its fleet manager for AMR and AGV environments supports centralized orchestration and VDA 5050 compatibility, reflecting the shift toward software-led fleet control. This is important because growth in AGVs does not simply add more connected vehicles; it expands the role of telematics into active intralogistics control. The material handling equipment telematics industry is therefore widening from operator-focused forklift monitoring toward machine-to-system orchestration across autonomous fleets. Aerial work platforms and earth-moving equipment in indoor or semi-indoor environments remain a smaller but emerging area where vendors are adapting telematics to more complex positioning needs.

Fleet management accounted for 34.36% of the material handling equipment telematics market in 2025, confirming its role as the base solution layer for most deployments. Buyers still tend to start with asset visibility, operator authentication, digital inspections, and usage dashboards before expanding into deeper analytics. That sequence matters because these basic functions lay the foundation for later safety, maintenance, and productivity applications. Toyota and Raymond both present telematics around this broader fleet management model, where compliance records, access control, and utilization visibility sit within a single operating view. In the material handling equipment telematics market, asset tracking and safety monitoring still absorb a large share of first-stage spending because they address urgent operational needs with a familiar payback path. Energy optimization is also becoming more visible as electric fleets expand and battery use has to be managed more carefully across shifts.

Predictive maintenance is expected to grow at a 15.56% CAGR through 2031, and this is where the material handling equipment telematics market is starting to reshape value capture. MHS Lift describes predictive maintenance as a model built on sensor data from engine temperature, battery condition, hydraulic performance, and other equipment health signals, enabling faults to be addressed before failure. That approach changes telematics from a monitoring tool into a cost-control tool because the most valuable outcome becomes avoided disruption rather than historical reporting. It also raises the importance of vendors that can turn raw readings into clear maintenance actions for technicians and managers. The material handling equipment telematics industry is therefore moving toward systems that prescribe what to do next rather than simply showing what has happened. Compliance requirements around equipment safety are also influencing design choices, which supports more structured and auditable predictive workflows.

Geography Analysis

North America held 38.54% of the material handling equipment telematics market share in 2025. The region benefits from advanced warehouse infrastructure, strong OEM telematics penetration, and a regulatory environment that keeps safety documentation and operator control in focus. OSHA's powered industrial truck standard continues to shape employer obligations around training, operation, and recordkeeping across warehouses and industrial sites. The United States remains the core demand center because fleets are larger, automation budgets are deeper, and multi-site operational oversight is more common. Canada and Mexico also add regional momentum as telematics expands across safety, visibility, and cross-border fleet operations.

Asia-Pacific is projected to grow at a 15.83% CAGR through 2031, making it the fastest-growing geography in the material handling equipment telematics market. The region is benefiting from manufacturing diversification, expanding e-commerce fulfillment networks, and broader investment in automated logistics infrastructure. India, South Korea, Southeast Asia, and parts of East Asia are creating new telematics opportunities, as greenfield facilities can adopt connected systems from the start rather than retrofitting older site layouts. That matters because new warehouses and industrial buildings can integrate fleet software, sensors, and digital workflows more cleanly than legacy operations. As a result, the material handling equipment telematics market is gaining traction across Asia-Pacific, not only from volume growth, but also from a more software-ready operating base.

Europe remains the third-largest region in the material handling equipment telematics market and stands out for its regulatory discipline and a mature provider ecosystem. Procurement standards in the region place significant emphasis on information security, interoperability, and documented operational controls. SYNAOS highlights its ISO 27001 certification for its intralogistics platform, reflecting the growing importance of security readiness in product qualification among buyers in Europe. Trackunit also expanded its partnership with Sunbelt Rentals UK and Ireland in late 2025, extending connected asset coverage through the IrisX platform in the off-highway sector. South America, the Middle East, and Africa are developing from a smaller base, where construction, mining, and logistics projects are creating space for adoption, but retrofit costs and governance readiness still limit faster scaling.

- PowerFleet, Inc.

- ELOKON GmbH

- GemOne NV

- Davis Derby Limited

- Litum Technologies, Inc.

- Kiwitron S.r.l.

- Ubiquicom S.r.l.

- WISER Systems, Inc.

- The Collective Intelligence Group Pty Ltd

- Rombit NV

- Stocked Robotics, Inc. d/b/a SIERA.AI

- Trio Mobil Teknoloji A.?.

- Troax Active Safety Spain S.L.U.

- FTC Safety Solutions Ltd.

- Trackunit A/S

- Teletrac Navman US Ltd.

- Samsara Inc.

- Geotab Inc.

- ORBCOMM Inc.

- CombiQ AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Warehouse Automation and E-Commerce Fulfillment Density

- 4.2.2 Tightening Safety and Compliance Requirements for Powered Industrial Trucks

- 4.2.3 Growing Need for Fleet Utilization and Downtime Reduction

- 4.2.4 Expansion of Cloud, IoT, and AI-Enabled Remote Diagnostics

- 4.2.5 Lithium-Ion Battery Analytics Becoming a Fleet Control Layer

- 4.2.6 Telematics Integration With WMS and Intralogistics Orchestration Platforms

- 4.3 Market Restraints

- 4.3.1 High Retrofit, Integration, and Change-Management Costs

- 4.3.2 Cybersecurity and Data Governance Risks in Multi-Site Fleets

- 4.3.3 Mixed-Fleet Interoperability Gaps Across OEM and Aftermarket Systems

- 4.3.4 Signal Degradation in Dense Metal-Rack and High-Interference Indoor Environments

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Forklifts

- 5.1.2 Cranes

- 5.1.3 Automated Guided Vehicles (AGVs)

- 5.1.4 Earth-moving Equipment

- 5.1.5 Telehandlers

- 5.1.6 Trucks

- 5.1.7 Tractors

- 5.1.8 Aerial Work Platforms

- 5.2 By Solution Type

- 5.2.1 Asset Tracking

- 5.2.2 Fleet Management

- 5.2.3 Predictive Maintenance

- 5.2.4 Safety and Compliance Monitoring

- 5.2.5 Energy Optimization

- 5.2.6 Operational Analytics

- 5.2.7 Other Solution Types

- 5.3 By End-User Industry

- 5.3.1 Manufacturing

- 5.3.2 Logistics and Warehousing

- 5.3.3 Automotive

- 5.3.4 Construction

- 5.3.5 Mining

- 5.3.6 Transportation

- 5.3.7 Other End-User Industries

- 5.4 By Technology

- 5.4.1 GPS

- 5.4.2 IoT Sensors

- 5.4.3 AI-based Predictive Systems

- 5.4.4 Edge Computing

- 5.4.5 5G-enabled Telematics

- 5.5 By Distribution Channel

- 5.5.1 OEM (Original Equipment Manufacturer)

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Israel

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 PowerFleet, Inc.

- 6.4.2 ELOKON GmbH

- 6.4.3 GemOne NV

- 6.4.4 Davis Derby Limited

- 6.4.5 Litum Technologies, Inc.

- 6.4.6 Kiwitron S.r.l.

- 6.4.7 Ubiquicom S.r.l.

- 6.4.8 WISER Systems, Inc.

- 6.4.9 The Collective Intelligence Group Pty Ltd

- 6.4.10 Rombit NV

- 6.4.11 Stocked Robotics, Inc. d/b/a SIERA.AI

- 6.4.12 Trio Mobil Teknoloji A.?.

- 6.4.13 Troax Active Safety Spain S.L.U.

- 6.4.14 FTC Safety Solutions Ltd.

- 6.4.15 Trackunit A/S

- 6.4.16 Teletrac Navman US Ltd.

- 6.4.17 Samsara Inc.

- 6.4.18 Geotab Inc.

- 6.4.19 ORBCOMM Inc.

- 6.4.20 CombiQ AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment