|

시장보고서

상품코드

2063351

프랑스의 시험, 검사 및 인증(TIC) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)France Testing, Inspection, And Certification (TIC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

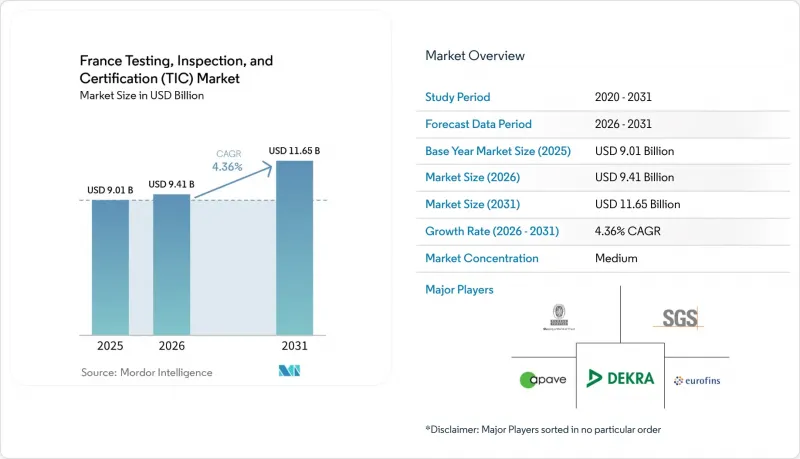

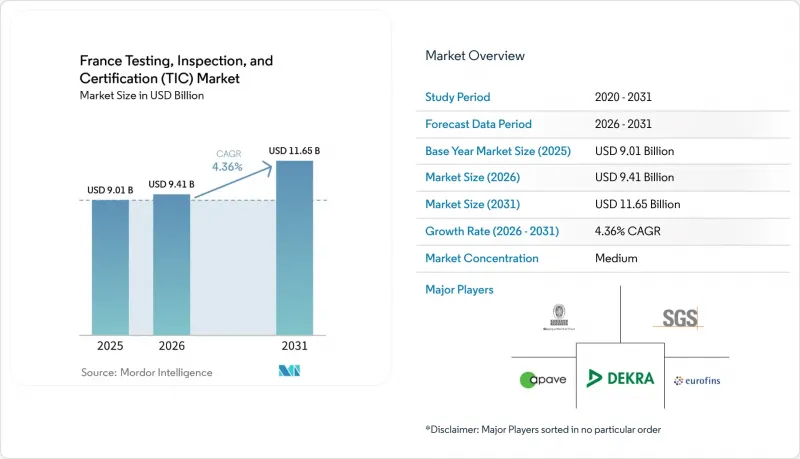

Mordor Intelligence에 의하면, 프랑스의 시험, 검사 및 인증(TIC) 시장 규모는 2025년 90억 1,000만 달러로 평가되었습니다. 2026년에는 94억 1,000만 달러로 확대되어 2031년까지 116억 5,000만 달러에 이르고 2026-2031년에 걸쳐 CAGR은 4.36%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(시험, 검사 및 인증), 조달 형태별(사내 수행 및 외부 위탁), 산업별(소비재 및 소매, ICT·통신, 에너지 및 유틸리티, 화학·소재, 기타), 서비스 제공 형태별(온사이트, 오프사이트/검사실, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

프랑스의 시험, 검사 및 인증(TIC) 시장 동향 및 인사이트

EU와 프랑스의 규제 준수 의무 급증

2024년 10월에 발효된 ‘네트워크 및 정보 보안 지침 2’에 따라, 1만 개가 넘는 프랑스 기관은 정기적인 사이버 보안 감사를 실시해야 할 의무가 있으며, 이를 위반할 경우 전 세계 매출액에 따라 벌금이 부과됩니다. '사이버 복원력법'은 2026년 9월부터 연결 제품에 대한 제3자 CE 마크 평가를 확대하고, 검사 기관에 2년간의 체계 정비 기간을 부여하고 있습니다. ANSSI의 ReCyF 프레임워크 등 국내 조정 노력을 통해 감사 체크리스트가 표준화되고, 검사 기관의 인증이 가속화되고 있습니다. 기업 지속가능성 보고 지침에 따른 병행 의무에 따라, 대기업의 경우 2026년까지는 제한적 보증, 2028년까지는 합리적 보증이 요구되고 있으며, 제품 안전, 사이버 보안, ESG 검증을 통합한 감사 계약이 추진되고 있습니다. 이러한 규칙들이 복합적으로 작용하여, 여러 부문에 걸친 프로그램을 제공할 수 있는 사업자에게는 높은 지속적인 수익이 유지되고 있습니다.

수소 배터리 기가팩토리 건설에 따른 수요

2025년 12월에 가동을 시작한 Verkor의 15억 유로(17억 3,000만 달러) 규모 덩케르크 배터리 공장은 전극 품질, 전해액 순도, 열폭주 검사에 따른 지속적인 실험실 업무의 부담을 여실히 보여주고 있습니다. 2025년 5월 Lhyfe가 취득한 RFNBO 인증은 제3자 인증이 어떻게 수년에 걸친 생산 보조금 확보를 가능하게 하는지 보여주고 있습니다. 유럽 집행위원회가 2026년 3월에 수립한 그린 수소 계획에 따르면, 200메가와트급 전해조가 여러 대 도입될 전망이며, 각 전해조에 대해 수소 순도, 압력 용기의 건전성, 계통 연계 안전성에 관한 ISO 17025 인증 분석이 요구됩니다. EU의 기술 기준이 강화됨에 따라 배터리와 수소 시설 모두에 대해 정기적인 재인증이 필요하게 되어, 적합성 평가 서비스에 대한 지속적인 수요가 보장될 것입니다.

인증된 실험실과 숙련된 감사관의 부족

COFRAC이 2024년 12월에 LAB REF 08을 개정함에 따라 인증 주기가 최대 24개월로 연장되었는데, 이는 수소 순도, 배터리 안전성, 사이버 보안 침투 테스트에 대한 수요가 급증한 시기와 맞물려 있습니다. 노동력 공급은 연평균 3% 증가에 그치는 반면, 수요는 5-6%의 속도로 증가하고 있습니다. 데크라(Dekra)가 프랑스에서 검사원 1,000명을 채용할 계획인 것은 인력 부족 문제를 여실히 드러내고 있습니다. 또한, 2026년 바이오뱅크 인증과 같은 새로운 프로그램으로 인해 모니터링 팀의 부담은 더욱 커지고 있습니다. 대학에서는 ESG 보증 및 IoT 보안에 관한 교육 과정이 아직 충분히 마련되어 있지 않아, 서비스 제공업체들은 타사에서 인재를 영입하거나, 역량 강화가 지연되는 수년에 걸친 수습 제도에 자금을 투입할 수밖에 없는 상황입니다.

부문별 분석

2025년, 프랑스의 시험, 검사 및 인증(TIC) 시장에서는 의약품 및 식품 안전 등 실험실 활용이 많은 부문에 힘입어 검사 부문이 매출의 58.94%를 차지하며 시장을 주도했습니다. 그러나 인증 부문은 5.12%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이는 ‘사이버 복원력법’, NIS2, ‘기업 지속가능성 보고 지침’이 모두 사내 연구소에서는 제공할 수 없는 제3자 인증을 규정하고 있기 때문입니다. 따라서 프랑스 TIC 시장의 인증 부문 규모는 2031년까지 꾸준히 확대될 전망입니다. 시장 출시 전 검사와 출시 후 모니터링을 단일 감사 패키지로 통합할 수 있는 공급업체들이 다년 계약을 수주하고 있으며, 이는 규제로 인해 인증이 비용 센터에서 수익원으로 전환되고 있음을 보여줍니다.

고빈도 샘플링이나 파괴 검사가 의무화되어 있는 부문에서는 검사 서비스가 여전히 필수적이지만, 그 성장세는 다소 완만해지고 있습니다. 검사 서비스는 에너지, 엘리베이터, 건설 부문의 자산 유지 관리 프로그램을 지원함으로써 그 중간 영역을 담당하고 있습니다. 이 세 가지 서비스를 융합한 하이브리드 솔루션이 프랑스 TIC 시장에서 점유율을 확대함에 따라, 이 부문의 장기적인 안정성이 뒷받침되고 있습니다.

아웃소싱 계약은 2025년에 64.31%의 점유율을 차지했으며, 연평균 성장률(CAGR) 4.93%로 증가할 것으로 전망되어, 이 부문에서 가장 높은 성장률을 보이고 있습니다. COFRAC의 범위 관리 규정이 강화됨에 따라, 사내 ISO 17025 인증을 유지하기 위한 고정비가 증가하여, 대형 제조업체조차도 정기 감사를 외부에 위탁하고 있습니다. 그 결과, 인증을 받은 대기업들이 컴플라이언스 관련 비용을 수백 개의 고객사에 분산함에 따라, 프랑스의 시험, 검사 및 인증(TIC) 시장에서 외부 공급업체가 차지하는 비중은 해마다 확대되고 있습니다.

사내 팀이 남아 있는 분야는 항공우주 부문의 고장 분석이나 의약품 제제 연구 등, 독자적인 기술이나 기밀성이 높은 업무로 한정되어 있습니다. 그러나 이러한 기업들조차 인건비를 절감하기 위해 정기적인 법정 감사를 외부에 위탁하고 있습니다. 5세대 사설 네트워크 덕분에 원격 검증이 가능해지면서, 과거 상주 검사관이 가졌던 우위는 줄어들고 있습니다. 예측 기간 동안 프랑스 TIC 시장에서 사내 서비스의 점유율은 점차 축소될 것으로 예측됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the france testing, inspection, and certification (TIC) market size is expected to increase from USD 9.01 billion in 2025 to USD 9.41 billion in 2026 and reach USD 11.65 billion by 2031, growing at a CAGR of 4.36% over 2026-2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Energy and Utilities, Chemicals and Materials, and More ), and Mode of Service Delivery (On-Site, Off-Site Laboratory, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Testing, Inspection, And Certification (TIC) Market Trends and Insights

Mandatory EU And French Regulatory Compliance Surge

The Network and Information Security Directive 2, which took effect in October 2024, obliges more than 10,000 French organizations to commission periodic cybersecurity audits, with fines tied to global turnover for non-compliance. The Cyber Resilience Act extends third-party CE-mark assessments to connected products from September 2026, creating a two-year capacity-build window for laboratories. National alignment efforts, such as ANSSI's ReCyF framework, have standardized audit checklists, accelerating accreditation of inspection bodies. Parallel obligations under the Corporate Sustainability Reporting Directive require limited assurance for large firms by 2026 and reasonable assurance by 2028, driving integrated audit contracts that bundle product safety, cybersecurity, and ESG verification. Together, these rules sustain high recurring revenue for providers able to deliver multidisciplinary programs.

Hydrogen and Battery Gigafactory Build-Out Needs

Verkor's EUR 1.5 billion (USD 1.73 billion) Dunkirk battery plant, inaugurated in December 2025, illustrates the recurring laboratory workload attached to electrode quality, electrolyte purity, and thermal-runaway testing. Lhyfe's RFNBO certification in May 2025 shows how third-party attestations unlock multi-year production subsidies. The European Commission's March 2026 green-hydrogen scheme foresees several 200 megawatt electrolyzers, each demanding ISO 17025-accredited analyses of hydrogen purity, pressure-vessel integrity, and grid-connection safety. Both battery and hydrogen facilities require periodic re-certification as EU technical standards tighten, guaranteeing a durable pipeline for conformity services.

Shortage of Accredited Labs and Skilled Auditors

COFRAC's December 2024 LAB REF 08 revision lengthened accreditation cycles to as much as 24 months, coinciding with surging demand for hydrogen purity, battery safety, and cybersecurity penetration tests. Labor supply grows only 3% annually, versus 5-6% demand growth. Dekra's plan to recruit 1,000 inspectors in France highlights the talent gap, while new programs such as the 2026 biobank accreditation stretch surveillance teams thinner. Universities have yet to scale curricula in ESG assurance or IoT security, forcing providers to poach staff or fund multi-year apprenticeships that delay capacity relief.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and ESG Verification Demand

- Digital-Device Proliferation and Cybersecurity Testing

- SME Price-Sensitivity to Premium TIC Fees

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing dominated the France testing, inspection, and certification market with 58.94% revenue in 2025, anchored by laboratory-intensive fields such as pharmaceuticals and food safety. Certification, however, is poised for the strongest 5.12% CAGR because the Cyber Resilience Act, NIS2, and the Corporate Sustainability Reporting Directive all stipulate third-party attestations that in-house labs cannot deliver. The France TIC market size for certification is therefore set to expand steadily through 2031. Providers able to combine pre-market tests with post-market surveillance inside a single audit package are winning multi-year contracts, evidencing how regulation converts certification from a cost center into a revenue enabler.

Testing remains indispensable where high-frequency sampling or destructive assays are mandatory, yet its growth is steadier. Inspection services fill the middle ground by supporting asset-integrity programs in energy, elevators and construction. The emerging France TIC market share for hybrid solutions that blend all three services underpins the sector's long-run stability.

Outsourced contracts held 64.31% share in 2025 and are forecast to climb at a 4.93% CAGR, the fastest in this segmentation. Tightened COFRAC scope-management rules have raised the fixed cost of maintaining in-house ISO 17025 accreditation, prompting even large manufacturers to shift routine audits outside. The France testing, inspection, and certification (TIC) market size captured by external providers therefore widens each year as accredited majors spread compliance overhead across hundreds of clients.

In-house teams persist only for proprietary or classified work, such as aerospace failure analysis or pharmaceutical formulation studies. Yet even these actors outsource periodic legal audits to reduce payroll costs. Private five-generation networks enable remote verification, shrinking the advantage once held by resident inspectors. Over the forecast horizon, the France TIC market share of in-house services is expected to erode incrementally.

List of Companies Covered in this Report:

- Bureau Veritas SA

- SGS France SAS

- Apave SA

- Dekra SE France

- Eurofins Scientific SE

- Intertek France SAS

- SOCOTEC SA

- TUV SUD France SAS

- TUV Rheinland France SARL

- TUV Nord France SAS

- ALS France SARL

- Element Materials Technology France

- Kiwa France SAS

- Applus + France SAS

- DNV France SAS

- Lloyd's Register Emea Branch France

- UL Solutions France SARL

- BSI Group France SAS

- Control Union France

- Cotecna Inspection France

- AFNOR Certification

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory EU and French Regulatory Compliance Surge

- 4.2.2 Outsourcing of TIC Functions by Large Enterprises

- 4.2.3 Sustainability/ESG Verification Demand

- 4.2.4 Digital-Device Proliferation and Cybersecurity Testing

- 4.2.5 Hydrogen and Battery Gigafactory Build-Out Needs

- 4.2.6 5G-Enabled Remote/Digital Inspections Adoption

- 4.3 Market Restraints

- 4.3.1 Shortage of Accredited Labs and Skilled Auditors

- 4.3.2 SME Price-Sensitivity to Premium TIC Fees

- 4.3.3 Patch-work local environmental rules (ZFE-m etc.)

- 4.3.4 Strategic Sector Protectionism Delaying Approvals

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Industry Vertical

- 5.3.1 Consumer Goods and Retail

- 5.3.2 ICT and Telecom

- 5.3.3 Automotive and Transportation

- 5.3.4 Aerospace and Defense

- 5.3.5 Oil, Gas and Petrochemicals

- 5.3.6 Energy and Utilities

- 5.3.7 Industrial Manufacturing and Machinery

- 5.3.8 Chemicals and Materials

- 5.3.9 Construction and Infrastructure

- 5.3.10 Life Sciences and Healthcare

- 5.3.11 Food, Agriculture and Beverage

- 5.3.12 Others Industry Verticals

- 5.4 By Mode of Service Delivery

- 5.4.1 On-site

- 5.4.2 Off-site / Laboratory

- 5.4.3 Remote / Digital

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bureau Veritas SA

- 6.4.2 SGS France SAS

- 6.4.3 Apave SA

- 6.4.4 Dekra SE France

- 6.4.5 Eurofins Scientific SE

- 6.4.6 Intertek France SAS

- 6.4.7 SOCOTEC SA

- 6.4.8 TUV SUD France SAS

- 6.4.9 TUV Rheinland France SARL

- 6.4.10 TUV Nord France SAS

- 6.4.11 ALS France SARL

- 6.4.12 Element Materials Technology France

- 6.4.13 Kiwa France SAS

- 6.4.14 Applus + France SAS

- 6.4.15 DNV France SAS

- 6.4.16 Lloyd's Register Emea Branch France

- 6.4.17 UL Solutions France SARL

- 6.4.18 BSI Group France SAS

- 6.4.19 Control Union France

- 6.4.20 Cotecna Inspection France

- 6.4.21 AFNOR Certification

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment