|

시장보고서

상품코드

2063364

NPK 비료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)NPK Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

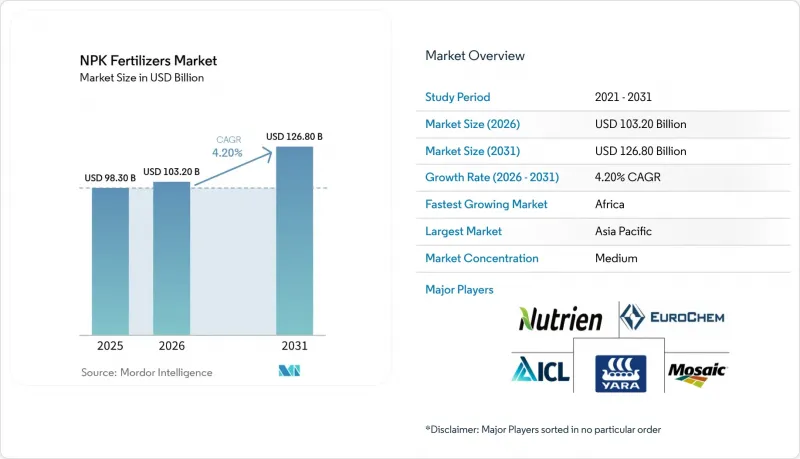

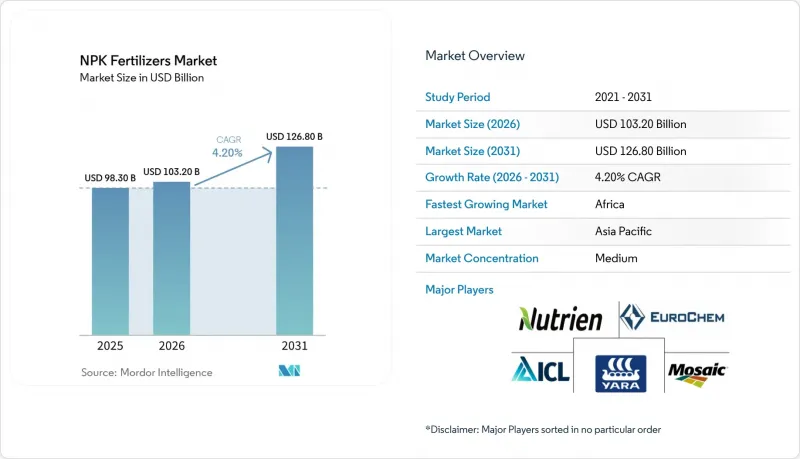

Mordor Intelligence에 의하면, NPK 비료 시장 규모는 2025년 983억 달러로 평가되었고, 2026년 1,032억 달러로 추정되고, 2031년까지 1,268억 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 4.2%를 나타낼 것으로 예측됩니다.

본 보고서는 형태별(건조 및 입상, 액체, 수용성 분말), 작물 유형별(곡물, 과일 및 채소, 지방종자 및 콩류, 기타 작물), 시용 방법별(토양 살포, 비료 관개, 엽면 살포), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 NPK 비료 시장 동향 및 분석

인구 증가에 따른 식량 수요의 급증

인구 증가에 따라 제한된 경작지에서 더 높은 수확량을 달성해야 한다는 농업 시스템에 대한 압박이 커지고 있어, 전 세계 비료 수요는 꾸준히 증가하고 있습니다. 유엔(UN)에 따르면, 세계 인구는 2050년까지 97억 명에 달할 것으로 예측됩니다. 이러한 인구 증가는 특히 지속 가능한 작물 생산성을 촉진하는 균형 잡힌 NPK(질소, 인, 칼륨) 비료 제품의 소비 패턴에 직접적인 영향을 미치고 있습니다. 농가에서는 환경 및 토지 이용의 제약 속에서 증가하는 식량 수요에 대응하는 동시에 토양의 비옥도를 유지하기 위해, 영양 효율이 높은 농업 기법의 도입이 확대되고 있습니다.

정부의 양분 이용 효율화 인센티브

주요 농업국에서 정부의 이니셔티브는 균형 잡힌 비료 시비 촉진과 양분 이용 효율(NUE) 향상에 크게 기여하고 있습니다. 인도에서는 '영양소 기반 보조금(NBS)' 제도가 인 및 칼륨 비료 사용을 지원하고 있으며, 질소계 비료에 대한 과도한 의존을 줄이는 것을 목표로 하고 있습니다. 이러한 정책 덕분에 농가들의 구매 결정은 영양 성분이 균형 있게 배합된 NPK 비료 쪽으로 기울고 있습니다. 전 세계적으로 지속가능성에 관한 규제가 더욱 엄격해짐에 따라, 이러한 조치들이 효율적인 비료 제품 및 통합 영양 관리 기법의 도입을 촉진할 것으로 예측됩니다.

칼륨 및 암모니아 가격 변동

암모니아 관련 비료 가격의 변동은 NPK 비료 시장의 원가 구조에 계속해서 영향을 미치고 있습니다. 세계은행의 원자재 시장 데이터에 따르면, 요소 가격은 2026년 2월 톤당 472달러에서 2026년 3월에는 톤당 725.6달러로 크게 상승하여, 단기적인 가격 변동이 뚜렷한 것으로 나타났습니다. 요소는 암모니아에서 직접 제조되기 때문에 이러한 가격 변동은 주로 천연가스 가격 변동에 영향을 받는 질소 투입 비용의 불안정성을 여실히 드러내고 있습니다. 이러한 변동성은 NPK 비료의 생산 비용을 상승시키고, 농가의 구매 부담을 가중시키며, 조달 주기를 혼란스럽게 하여, 결국 지역 간 수요 패턴에 편차를 초래하게 됩니다.

부문별 분석

2025년에는 완전 용해성 영양소와 균일한 공급이 필요한 비료 관개 시스템의 도입 확대에 힘입어, 액체 제제가 시장 점유율 61.3%를 차지하며 1위를 차지했습니다. 이 제품들은 영양분의 정밀한 공급을 가능하게 하고 관개 시 손실을 줄여주므로, 고부가가치 작물이나 관리형 농업 시스템에 적합합니다. 또한, 각 제조업체는 내식성 탱크나 계량 시스템 등 액체 비료의 저장, 운송, 시비 인프라 개선에도 힘쓰고 있습니다. 이러한 추세는 특히 정밀 농업이나 절수형 농업 기술을 도입한 지역에서 액체 비료에 대한 수요를 촉진하고 있습니다.

건조 및 입상 비료는 취급이 간편하고 비용 효율이 높아, 대규모 밭작물 재배에 여전히 필수적입니다. 생산자들이 첨단 과립화 기술 및 입자 크기 최적화에 투자함에 따라, 건조 및 입상 비료 시장 규모는 2026-2031년 연평균 성장률(CAGR) 3.4%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 입자가 균일한 비료는 살포 정밀도와 가변 시비 장치와의 호환성을 높여줍니다. 각사는 분진 발생을 억제하고 제품의 일관성을 높이기 위해 코팅 및 선별 시스템의 업그레이드를 추진하고 있습니다. 액체와 입자 형태 모두를 생산할 수 있는 유연한 제조 체계를 통해 생산자는 수요 변동이나 원자재 가격 변동에 유연하게 대응할 수 있게 되었습니다.

지역별 분석

아시아태평양은 인도와 중국 등 국가들의 견조한 농업 생산과 높은 비료 소비에 힘입어, 2025년에는 53.1%라는 가장 높은 시장 점유율을 차지한 것으로 평가되었습니다. 이 지역은 광대한 경작지, 다작 재배 주기, 그리고 균형 잡힌 비료 시비를 장려하는 정부의 이니셔티브 덕분에 혜택을 누리고 있습니다. 국내 생산 능력 확대와 비료 밸류체인 전반의 통합을 통해 공급 안정성이 향상되고 있습니다. 게다가 인구 증가와 식량 수요 증가가 계속해서 비료 소비를 견인하고 있어, 이 지역이 세계 비료 사용량에서 차지하는 주도적 지위를 더욱 공고히 하고 있습니다.

아프리카 시장 규모는 비료 혼합 시설에 대한 투자 확대와 농업의 현대화를 배경으로, 2026-2031년 연평균 성장률(CAGR) 5.8%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 각국 정부와 개발 기관은 토양의 건전성과 작물의 생산성을 높이기 위해 균형 잡힌 비료 시비를 적극적으로 추진하고 있습니다. 현지 생산 능력 확대로 인해 수입 의존도가 낮아지고, 비료 공급 상황이 개선되고 있습니다. 주식 작물의 재배 확대와 이를 뒷받침하는 농업 정책이 맞물리면서, 아프리카 주요 경제권 전반에 걸쳐 영양 솔루션에 대한 수요가 증가하고 있습니다.

유럽과 북미는 성숙한 시장이며, 수요는 주로 지속가능성과 관련된 규제 및 정책과 효율성을 중시하는 농업 관행에 의해 주도되고 있습니다. 이 지역들의 환경 정책은 과도한 비료 사용을 억제하는 한편, 영양분의 적정 시비를 장려하고 있습니다. 농가들은 정밀 농업 기술과 개선된 영양 관리 방법을 점점 더 많이 도입하고 있습니다. 이러한 추세가 구매 행태를 형성하며, 고효율이고 환경 기준을 충족하는 비료 제품에 대한 수요를 이끌고 있습니다. 국제비료협회(IFA)에 따르면, 2024-2025 비료 연도의 전 세계 비료 수요는 질소 1억 1,400만 톤, 인산 4,700만 톤, 칼륨 4,000만 톤을 포함해 약 2억 100만 톤의 영양소에 달했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the nPK fertilizers market size is projected to grow from USD 98.3 billion in 2025 and USD 103.2 billion in 2026 to USD 126.8 billion by 2031, registering a CAGR of 4.2% between 2026 and 2031.

This report is Segmented by Form (Dry/Granular, Liquid, and Water-Soluble Powder), by Crop Type (Cereals and Grains, Fruits and Vegetables, Oilseeds and Pulses, and Other Crops), by Mode of Application (Soil Broadcasting, Fertigation, Foliar Spray), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global NPK Fertilizers Market Trends and Insights

Population-Driven Food-Demand Surge

Global fertilizer demand is steadily increasing as population growth places greater pressure on agricultural systems to achieve higher yields from limited arable land. According to the United Nations (UN), the global population is projected to reach 9.7 billion by 2050 . This population growth is directly impacting fertilizer consumption patterns, particularly for balanced NPK (Nitrogen, Phosphorus, and Potassium) products that promote sustainable crop productivity. Farmers are increasingly implementing nutrient-efficient practices to preserve soil fertility while addressing rising food demand amid environmental and land-use constraints.

Government Nutrient-Efficiency Incentives

Government initiatives are significantly contributing to the promotion of balanced fertilization and the enhancement of nutrient-use efficiency (NUE) in key agricultural economies. In India, the Nutrient Based Subsidy (NBS) scheme supports the use of phosphorus and potassium fertilizers, aiming to reduce the over-reliance on nitrogen-based inputs. These policies are shaping farmers' purchasing decisions toward NPK fertilizers with balanced nutrient compositions. As global sustainability regulations become more stringent, such measures are anticipated to drive the adoption of efficient fertilizer products and integrated nutrient management practices.

Potash and Ammonia Price Volatility

Fluctuations in ammonia-related fertilizer prices continue to impact cost structures in the NPK fertilizers market. According to the World Bank Commodity Markets, urea prices rose significantly from USD 472 per metric ton in February 2026 to USD 725.6 per metric ton in March 2026, indicating notable short-term volatility . Since urea is directly derived from ammonia, these price fluctuations underscore instability in nitrogen input costs, primarily influenced by changes in natural gas prices. This volatility increases production costs for NPK fertilizers, reduces affordability for farmers, and disrupts procurement cycles, ultimately resulting in inconsistent demand patterns across regions.

Other drivers and restraints analyzed in the detailed report include:

- Precision Fertilization Adoption

- Shift to Balanced NPK Blends in Specialty Crops

- Stricter Emission Rules on Urea Granulation Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid formulations led with the largest 61.3% of market share in 2025, supported by increasing adoption of fertigation systems that require fully soluble nutrients and uniform delivery. These products enable precise nutrient application and reduce losses during irrigation, making them suitable for high-value crops and controlled farming systems. Manufacturers are also improving storage, transport, and application infrastructure for liquids, including corrosion-resistant tanks and metering systems. This shift is reinforcing demand for liquid fertilizers, particularly in regions adopting precision agriculture practices and water-efficient farming techniques.

Dry/granular fertilizers remain essential for large-scale field crops due to ease of handling and cost efficiency. The dry/granular market size is projected to grow at the fastest 3.4% CAGR from 2026 to 2031 as producers invest in advanced granulation technologies and particle-size optimization. Uniform granules improve spreading accuracy and compatibility with variable rate equipment. Companies are upgrading coating and screening systems to reduce dust formation and enhance product consistency. Flexible manufacturing setups that support both liquid and granular formats are enabling producers to adapt to fluctuating demand and feedstock price dynamics.

Geography Analysis

Asia-Pacific is projected to hold the largest market share of 53.1% in 2025, driven by robust agricultural output and high fertilizer consumption in countries such as India and China. The region benefits from extensive arable land, multiple cropping cycles, and government initiatives promoting balanced fertilization. Expansion of domestic production capacity and integration across fertilizer value chains are enhancing supply stability. Additionally, the rising population and increasing food demand continue to fuel nutrient consumption, solidifying the region's leadership in global fertilizer usage.

Africa market size is projected to grow at the fastest CAGR of 5.8% from 2026 to 2031, driven by rising investments in fertilizer blending facilities and agricultural modernization. Governments and development organizations are actively promoting balanced fertilization to enhance soil health and crop productivity. The expansion of local production capacity is reducing reliance on imports and improving access to fertilizer. Growth in staple crop cultivation, coupled with supportive agricultural policies, is boosting demand for nutrient solutions across key African economies.

Europe and North America represent mature markets where demand is primarily driven by sustainability regulations and efficiency-focused farming practices. Environmental policies in these regions encourage optimized nutrient application while discouraging excessive fertilizer use. Farmers are increasingly adopting precision agriculture technologies and improved nutrient management practices. These trends are shaping purchasing behaviors and driving demand for high-efficiency, environmentally compliant fertilizer products. According to the International Fertilizer Association, global fertilizer demand reached approximately 201 million metric tons of nutrients in the 2024/25 fertilizer year, including 114 million metric tons of nitrogen, 47 million metric tons of phosphate, and 40 million metric tons of potash .

- Yara International ASA

- Nutrien Ltd.

- The Mosaic Company

- EuroChem Group AG

- ICL Group Ltd.

- CF Industries Holdings, Inc.

- OCP S.A.

- K+S Aktiengesellschaft

- Coromandel International Limited

- Borealis AG

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Public Joint Stock Company Acron

- Stanley Agriculture Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Population-driven food-demand surge

- 4.2.2 Precision fertilization adoption

- 4.2.3 Shift to balanced NPK blends in specialty crops

- 4.2.4 Government nutrient-efficiency incentives

- 4.2.5 Carbon-credit revenue for low-nitrous-oxide NPKs

- 4.2.6 Phosphate recovery from wastewater plants

- 4.3 Market Restraints

- 4.3.1 Potash and ammonia price volatility

- 4.3.2 Stricter emission rules on urea granulation lines

- 4.3.3 Rapid acreage shift to pulses and legumes

- 4.3.4 Rise of biological N-P-K substitutes

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Form

- 5.1.1 Dry/Granular

- 5.1.2 Liquid

- 5.1.3 Water-Soluble Powder

- 5.2 By Crop Type

- 5.2.1 Cereals and Grains

- 5.2.2 Fruits and Vegetables

- 5.2.3 Oilseeds and Pulses

- 5.2.4 Other Crops

- 5.3 By Mode of Application

- 5.3.1 Soil Broadcasting

- 5.3.2 Fertigation

- 5.3.3 Foliar Spray

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 Russia

- 5.4.3.4 United Kingdom

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Turkey

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 Nigeria

- 5.4.6.2 South Africa

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 Nutrien Ltd.

- 6.4.3 The Mosaic Company

- 6.4.4 EuroChem Group AG

- 6.4.5 ICL Group Ltd.

- 6.4.6 CF Industries Holdings, Inc.

- 6.4.7 OCP S.A.

- 6.4.8 K+S Aktiengesellschaft

- 6.4.9 Coromandel International Limited

- 6.4.10 Borealis AG

- 6.4.11 Haifa Group

- 6.4.12 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.13 Public Joint Stock Company Acron

- 6.4.14 Stanley Agriculture Group Co., Ltd.