|

시장보고서

상품코드

2063367

건설용 카메라 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Construction Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

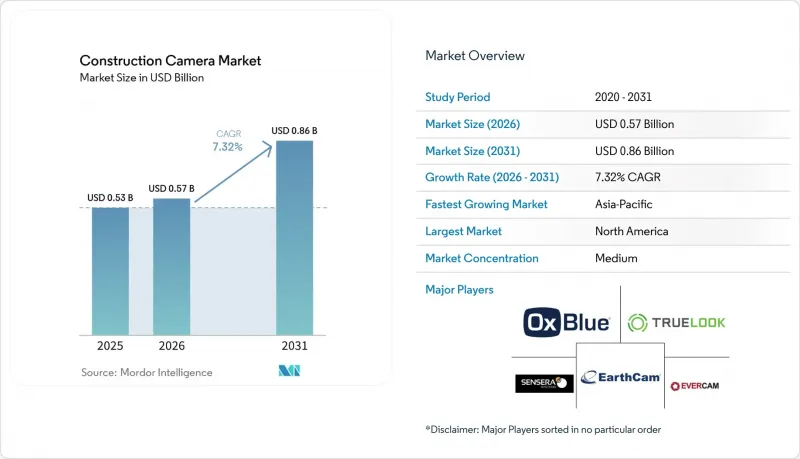

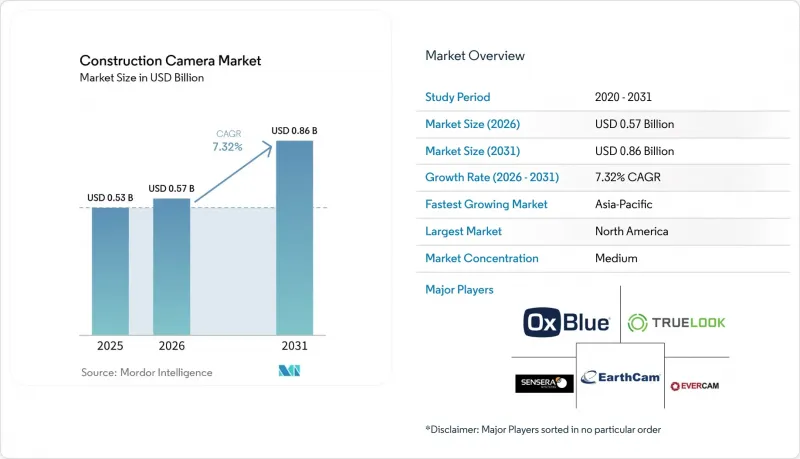

Mordor Intelligence에 의하면, 건설용 카메라 시장 규모는 2025년 5억 3,000만 달러로 평가되었고, 2026년에는 5억 7,000만 달러로 추정되고, 2031년까지 8억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 7.32%로 성장할 전망입니다.

본 보고서는 제품 유형별(고정형 카메라, PTZ 카메라 등), 전원별(AC 전원 시스템, 태양광 발전 시스템 등), 연결 방식별(4G/5G 셀룰러, Wi-Fi/메쉬 등), 용도별(진행 상황 모니터링 및 기록 등), 최종 사용자 산업별(종합 건설사 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 건설용 카메라 시장 동향 및 인사이트

엣지 AI를 활용한 안전 및 규정 준수 분석

카메라에 탑재된 엣지 프로세서는 현재 개인보호구(PPE)(PPE) 미착용, 접근으로 인한 위험, 출입 금지 구역 침입을 200밀리초 이내에 감지합니다. 조기 도입 기업들은 2025년까지 OSHA(미국 직업안전보건청)의 기록 대상인 사고를 34% 감축하게 되며, 이를 통해 도급업체는 산재보험료 인하 협상을 진행할 수 있게 됩니다. 로컬 추론을 통해 현장에서 전송되는 것은 사고 메타데이터뿐이므로 개인정보가 보호되며, 캘리포니아주 의회 법안 1221호 및 GDPR(EU 개인정보보호규정)의 요건을 충족합니다. 도입은 여전히 더 심각한 위험에 직면한 철골 조립 및 전기 공사 분야에 집중되어 있지만, 칩셋 가격 하락으로 인해 3년 이내에 일반 건설업 분야로도 그 혜택이 확대될 전망입니다.

Procore 및 Autodesk BIM 워크플로와의 통합

플러그 앤 플레이 방식의 애플리케이션 프로그래밍 인터페이스(API)를 통해 현장 감독관은 프로젝트 대시보드를 떠나지 않고도 일일 로그를 열고 타임스탬프를 클릭하기만 하면 동기화된 이미지를 불러올 수 있습니다. Procore의 ROI 조사에 따르면, 이러한 통합 기능을 활용하는 건설사는 2026년에 재시공 비용을 23% 절감하고 공사 기간 초과를 18% 줄였다고 보고했습니다. 현장 작업자가 실측 이미지를 통합된 BIM 모델과 대조함에 따라, 설치가 허용 오차 범위를 벗어날 경우 설계자는 거의 실시간으로 경고를 받을 수 있어, 과거에는 수주가 걸리던 피드백 루프가 단축됩니다.

다중 거점 운영 시 높은 초기 하드웨어 비용

10-20건의 프로젝트를 관리하는 중규모 건설업체는 멀티 카메라 시스템을 도입하기 위해 5만-15만 달러라는 막대한 투자 비용을 책정해야 합니다. 구독형 모델은 초기 비용을 절감함으로써 보다 경제적인 도입 방안을 제공하지만, 대부분의 경우 기업을 장기 계약(보통 36개월 계약)에 묶어두게 됩니다. 이러한 계약의 경우, 차량 1대당 최대 1만 800달러의 총비용이 발생할 수 있으며, 계약 기간 중 프로젝트 작업량이 감소할 경우 도급업체에게 문제가 될 수 있습니다. 게다가 브라질의 영상 장비에 부과되는 16%의 수입 관세와 같은 외부 요인이 비용을 더욱 상승시켜 조달 비용을 높이고 있습니다. 아프리카의 일부 국가에서는 장비 구매를 위한 금융 지원 옵션에 대한 접근성이 제한적이며, 이용이 가능한 경우에도 연 12%라는 높은 금리가 부과되는 경우가 많아, 이는 추가적인 장애 요인이 되어 구매 결정을 지연시키고 해당 지역에서의 첨단 카메라 시스템 도입을 저해하고 있습니다.

부문별 분석

건설용 카메라 시장 규모는 제품 유형별로 분류되며, 고정식 유닛이 매출의 42.51%를 차지했습니다. 건설업체들은 몇 달에 걸친 공사를 단일 관점에서 처리할 수 있는 고속도로나 평탄한 산업용 부지에서 이러한 저비용 모델을 선택하고 있습니다. 그러나 초고층 빌딩이나 교각에서는 작업자가 매주 크레인의 위치를 변경하기 때문에 고정식 유닛을 사용하면 시야가 가려지게 됩니다. 그 결과, 이동식 트레일러 및 크레인 탑재형 장비는 연평균 9.37%의 성장률을 기록하며 건설용 카메라 시장 전체의 성장률을 상회하고 있습니다. 이동식 PTZ 카메라 1대로 여러 대의 고정식 장비를 대체할 수 있으므로, 데이터 통신량 절감과 현장 출장 횟수 감소로 이어집니다. 그러나 모터의 구조가 복잡해짐에 따라, 특히 모래먼지가 많은 연안 지역의 사막이나 강풍이 부는 북극권에서는 유지보수 부담이 커집니다.

또한, 모바일 솔루션은 정교한 분석 기능을 통해 프리미엄 가격 책정이 가능하게 합니다. 각 업체는 팬-틸트-줌(PTZ) 로봇과 엣지 AI 모듈을 결합하여 층별 거푸집 공사의 진행 상황을 파악하고, 해당 데이터를 일정 관리 소프트웨어에 피드백함으로써 진척 가치 지표(Earned Value)를 산출하고 있습니다. 렌탈 차량 대수가 증가하고 있는 이유는 소유주들이 셀룰러 통신 패키지가 미리 설정된 상태로 인도되는 대차대조표 외 자산인 장비를 선호하기 때문입니다. 아시아태평양과 중동에서 메가 프로젝트 파이프라인이 확대됨에 따라, 이동이 용이한 시추 장비에 대한 수요가 증가하고 있으며, 예측 기간 동안 제품 유형의 변화가 정착되고 있습니다.

2025년에는 태양광 발전 설비가 전원 부문의 51.33%를 차지했으며, 현재 이 부문이 건설용 카메라 시장에서 가장 큰 점유율을 차지하고 있습니다. 변환 효율은 22%에 달하며, 인산철 리튬 배터리를 통해 가동 시간이 연장됨에 따라 AC 전원 방식의 대체 제품을 상회하는 연평균 성장률(CAGR) 9.53%가 예상됩니다. 송전망 확장에 여전히 1마일당 1만 5천-3만 달러의 비용이 소요되므로, 6개월마다 현장을 옮길 경우 총 소유 비용 측면에서 태양광 발전이 더 유리합니다. 2025년에 특허를 취득한 셀룰러 통신 대역폭 제어 기술은 배터리 잔량이 적은 상태에서도 영상 비트레이트를 낮춤으로써, 새로운 패널을 추가하지 않고도 작동 시간을 유지합니다.

배터리 전용 및 하이브리드 시스템은 패널의 감가상각이 현실적이지 않은 90일 미만의 해체 및 현장 준비 계약에 적합합니다. 도시 재개발 지역에서는 트레일러나 타워 크레인을 위한 임시 전력 공급 시설이 이미 갖춰져 있기 때문에 AC 전원 방식의 PoE 카메라가 여전히 유용합니다. 전반적으로, 태양광 발전의 신뢰성 향상과 공공 입찰에서의 탄소 감축 목표 달성 요건 충족이 건설용 카메라 시장의 장기적인 핵심 위치를 확고히 하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 38.83%를 차지했습니다. 이는 건설업체의 배상 책임 비용을 최대 25% 절감해 주는 보험사의 보험료 공제에 의해 뒷받침되고 있습니다. 59억 달러 규모의 고디 하우 국제교와 같은 미국의 메가 프로젝트에서는 수십 대의 이동식 PTZ 카메라가 도입되어 있으며, 실시간 영상 전송을 위한 민간 5G 백본의 혜택을 누리고 있습니다. 캐나다의 ‘무역 다각화 회랑 기금’은 연방 정부가 자금을 지원하는 도로 및 항만에서 타임랩스 촬영을 의무화하고 있어, 카메라 입찰 수요를 창출하고 있습니다. 멕시코에서는 미국의 수출 관리 감사에 대응해야 하는 니어쇼어링 산업 플랜트가 잇따르고 있어, 이에 따라 가동 첫날부터 지속적인 시각적 감시 시스템을 도입해야 합니다.

아시아태평양은 각국 정부가 교통 회랑, 해저 터널, 스마트 시티 구역에 수십억 달러의 예산을 배정하고 있어 9.57%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 중국에서 진행 중인 420억 달러 규모의 도시 현대화 프로그램에서는 자금 지원 조건으로 부패 방지 대책에 대한 가시적인 증거를 요구하고 있습니다. 인도의 브라마푸트라 강 터널과 두브리-훌바리 교량에서는 국가고속도로청의 품질 규정을 충족하기 위해 EPC 계약에 카메라 설치 조항이 포함되어 있습니다. 일본의 지진 재해 복구 지침에서는 모든 내진 보강 공사에 카메라 설치를 의무화하고 있는 반면, 한국에서는 BIM과 연동된 영상 오버레이를 시범 운영하여 미완료 사항 목록의 처리 주기를 단축하고 있습니다. 이러한 정책 덕분에 건설용 카메라 시장에는 장기적인 수요가 자리 잡고 있습니다.

유럽에서는 비즈니스 기회와 규정 준수 관련 마찰 간의 균형이 잘 잡혀 있습니다. GDPR(EU 개인정보보호규정) 규정에 따라, 사건과 관련이 없는 한 영상 보관 기간은 30일로 제한되며, 공급업체는 익명화 서비스를 제공해야 합니다. 영국의 '건축물 안전법'에 따르면 고층 건축물에 디지털 트윈 도입이 의무화되어 있으며, 카메라는 시설 관리의 전 생애 주기에 걸쳐 활용되는 도구로 자리 잡고 있습니다. 중동에서는 NEOM과 같은 정부 주도의 도시 개발 프로젝트에서 수천 제곱킬로미터에 달하는 태양광 발전식 카메라의 설치가 요구되고 있습니다. 에티하드 레일이 110억 달러를 투자해 건설한 철도망에서는 인적이 드문 사막의 선로변에 60대의 카메라가 설치되어 있어, 극한의 기온이 내환경성이 뛰어난 장비에 대한 수요를 얼마나 가속화하고 있는지를 보여주고 있습니다. 남미와 아프리카는 수입 관세와 높은 차입 비용으로 인해 뒤처져 있지만, 유료 도로의 컨세션 모델에 카메라 도입 요건이 명시되기 시작하면서 성장의 씨앗이 뿌려지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the construction camera market size is expected to increase from USD 0.53 billion in 2025 to USD 0.57 billion in 2026 and reach USD 0.86 billion by 2031, growing at a CAGR of 7.32% over 2026-2031.

This report is Segmented by Product Type (Fixed Position Cameras, PTZ Cameras, and More), Power Source (AC-Powered Systems, Solar-Powered Systems, and More), Connectivity (4G/5G Cellular, Wi-Fi/Mesh, and More), Application (Progress Monitoring and Documentation, and More), End-User Industry (General Contractors, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Camera Market Trends and Insights

Edge AI Safety-Compliance Analytics

Edge processors in cameras now flag missing PPE, proximity hazards, and restricted-zone intrusions in under 200 milliseconds. Early adopters cut OSHA-recordable incidents by 34% in 2025, helping contractors negotiate lower workers' compensation premiums. Local inference preserves privacy because only incident metadata leaves the jobsite, satisfying California Assembly Bill 1221 and GDPR mandates. Uptake remains concentrated among steel erection and electrical trades that face higher severity risks, but declining chipset prices should extend the benefits to general trades within three years.

Integration with Procore and Autodesk BIM Workflows

Plug-and-play application programming interfaces allow superintendents to open a daily log, click a timestamp, and call up synchronized imagery without leaving their project dashboard. Construction firms using such integrations reported 23% lower rework costs and 18% fewer schedule overruns in 2026, according to Procore's ROI study. As field crews align as-built imagery with federated BIM models, designers receive near-real-time alerts when installations deviate from tolerances, closing feedback loops that once spanned weeks.

High Upfront Multi-Site Hardware Costs

Mid-size contractors managing 10-20 projects are required to allocate a significant investment of USD 50,000-150,000 to deploy multi-camera systems. While subscription-based models provide a more accessible entry point by reducing upfront costs, they often bind firms into long-term commitments, typically 36-month contracts. These contracts can add up to a total cost of USD 10,800 per unit, posing challenges for contractors if their project workloads decrease during the contract period. Additionally, external factors, such as the 16% import duty on imaging equipment in Brazil, further inflate costs, making procurement more expensive. In several African nations, limited access to equipment financing options, often available at high 12% APR rates, adds another layer of difficulty, delaying purchase decisions and hindering the adoption of advanced camera systems in these regions.

Other drivers and restraints analyzed in the detailed report include:

- Solar-Powered Autonomous Deployments

- Growing Adoption of Remote Project-Management Platforms

- Stricter Privacy and Worker-Surveillance Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The construction camera market size is by product type, with fixed-position units accounting for 42.51% of revenue. Contractors choose these low-cost models for highways and flat industrial sites where a single vantage point covers months of work. Yet on skyscrapers and bridge pylons, crews reposition cranes weekly, and fixed units lose sightlines. Mobile trailer and crane-mounted rigs, therefore, grow at 9.37% annually, outpacing the overall construction camera market. One mobile PTZ can replace several static units, reducing data plan usage and truck rolls. However, increased motor complexity raises maintenance, especially in dusty Gulf deserts or Arctic winds.

Mobile solutions also unlock premium pricing through advanced analytics. Vendors bundle pan-tilt-zoom robotics with edge AI modules that recognize formwork progression floor by floor, feeding earned-value metrics into scheduling software. Rental fleets expand because owners prefer off-balance-sheet equipment that arrives pre-configured with cellular packages. As megaproject pipelines thicken in Asia-Pacific and the Middle East, demand for easily relocated rigs cements the product-type shift over the forecast horizon.

Solar installations commanded 51.33% of the power-source segment in 2025, giving the category the highest construction camera market share at present. Rising conversion efficiencies now reach 22%, and lithium iron phosphate batteries lengthen runtime, driving a 9.53% CAGR projection that outstrips AC-powered alternatives. Extending grid service still costs USD 15,000-30,000 per mile, so the total cost of ownership favors solar when jobsites move every six months. Cellular throttling tech patented in 2025 cuts image bitrate under low-battery states, preserving uptime without new panels.

Battery-only and hybrid systems are suitable for demolition and site prep contracts lasting under 90 days, where panel amortization is unrealistic. In urban infill, AC-powered PoE cameras remain viable because temporary service already exists for trailers and tower cranes. Overall, solar's expanding reliability and compliance with carbon-reduction targets in public bids assure its position as the long-term backbone of the construction camera market.

Geography Analysis

North America accounted for 38.83% of global revenue in 2025, sustained by insurer premium credits that cut builders' liability costs by up to 25%. US megaprojects like the USD 5.9 billion Gordie Howe International Bridge deploy dozens of mobile PTZ rigs and benefit from private 5G backbones for real-time feed delivery. Canada's Trade Diversification Corridors Fund requires time-lapse documentation on federally financed roads and ports, creating a pipeline of camera tenders. Mexico follows with near-shoring industrial plants that must meet US export-control audits and, therefore, install continuous visual monitoring from day one.

Asia-Pacific is forecast to post the highest CAGR of 9.57% as governments allocate multibillion-dollar budgets for transport corridors, underwater tunnels, and smart-city districts. China's USD 42 billion urban modernization program ties funding to visual proof of anti-corruption safeguards. India's Brahmaputra tunnel and Dhubri-Phulbari Bridge embed camera clauses into EPC contracts to satisfy National Highways Authority quality protocols. Japan's earthquake reconstruction guidelines mandate cameras on all seismic retrofits, while South Korea pilots BIM-linked video overlays that shorten punch-list cycles. These policies embed long-term demand into the construction camera market.

Europe balances opportunity with compliance friction. GDPR rules limit footage retention to 30 days unless tagged to incidents, pushing vendors to offer anonymization services. The United Kingdom's Building Safety Act requires digital twins for high-rise assets, turning cameras into lifelong facility management tools. In the Middle East, sovereign-funded cities like NEOM require solar-powered cameras across thousands of square kilometers. Etihad Rail's USD 11 billion network mounted 60 units along remote desert trackage, demonstrating how thermal extremes accelerate demand for ruggedized rigs. South America and Africa trail because of import tariffs and high borrowing costs, yet concession models for toll roads are beginning to state camera deliverables, planting early seeds for growth.

- EarthCam, Inc.

- OxBlue Corporation

- Sensera Systems, Inc.

- TrueLook, Inc.

- Evercam Limited

- Brinno Inc.

- iBEAM Systems, Inc.

- CamDo Solutions Inc.

- Jobcam Pty Ltd

- Buildcam LLC

- HoloBuilder, Inc.

- SiteCams LLC

- OnSite View, Inc.

- Fast Motion GmbH

- Structionsite (DroneDeploy)

- Matterport, Inc.

- Forsight AI, Inc.

- Digital Eagle Technology Development Co., Ltd.

- IVC Mobile Vision, Inc.

- Outdoor Cameras Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Remote Project-Management Platforms

- 4.2.2 High-Resolution Time-Lapse for Stakeholder Marketing

- 4.2.3 Integration with Procore/Autodesk and BIM Workflows

- 4.2.4 Solar-Powered Autonomous Deployments

- 4.2.5 Edge AI Safety-Compliance Analytics

- 4.2.6 Insurance Premium Discounts for Visual Documentation

- 4.3 Market Restraints

- 4.3.1 High Upfront Multi-Site Hardware Costs

- 4.3.2 Bandwidth and Cloud-Storage Expenditures

- 4.3.3 Stricter Privacy/Worker-Surveillance Regulations

- 4.3.4 Electronics-Tariff Volatility on Imaging Components

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Fixed Position Cameras

- 5.1.2 PTZ Cameras

- 5.1.3 360°/Panoramic Cameras

- 5.1.4 Mobile Trailer and Crane-Mounted Cameras

- 5.2 By Power Source

- 5.2.1 AC-Powered Systems

- 5.2.2 Solar-Powered Systems

- 5.2.3 Battery-Only/Hybrid Systems

- 5.3 By Connectivity

- 5.3.1 4G/5G Cellular

- 5.3.2 Wi-Fi / Mesh

- 5.3.3 Wired Ethernet/PoE

- 5.4 By Application

- 5.4.1 Progress Monitoring and Documentation

- 5.4.2 Security and Surveillance

- 5.4.3 Marketing and Stakeholder Engagement

- 5.5 By End-User Industry

- 5.5.1 General Contractors

- 5.5.2 Owners / Developers

- 5.5.3 Government and Infrastructure Agencies

- 5.5.4 Industrial EPC and Energy Firms

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 EarthCam, Inc.

- 6.4.2 OxBlue Corporation

- 6.4.3 Sensera Systems, Inc.

- 6.4.4 TrueLook, Inc.

- 6.4.5 Evercam Limited

- 6.4.6 Brinno Inc.

- 6.4.7 iBEAM Systems, Inc.

- 6.4.8 CamDo Solutions Inc.

- 6.4.9 Jobcam Pty Ltd

- 6.4.10 Buildcam LLC

- 6.4.11 HoloBuilder, Inc.

- 6.4.12 SiteCams LLC

- 6.4.13 OnSite View, Inc.

- 6.4.14 Fast Motion GmbH

- 6.4.15 Structionsite (DroneDeploy)

- 6.4.16 Matterport, Inc.

- 6.4.17 Forsight AI, Inc.

- 6.4.18 Digital Eagle Technology Development Co., Ltd.

- 6.4.19 IVC Mobile Vision, Inc.

- 6.4.20 Outdoor Cameras Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment