|

시장보고서

상품코드

2063375

아프리카의 데이터센터 액침 냉각액 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Africa Data Center Immersion Cooling Fluid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

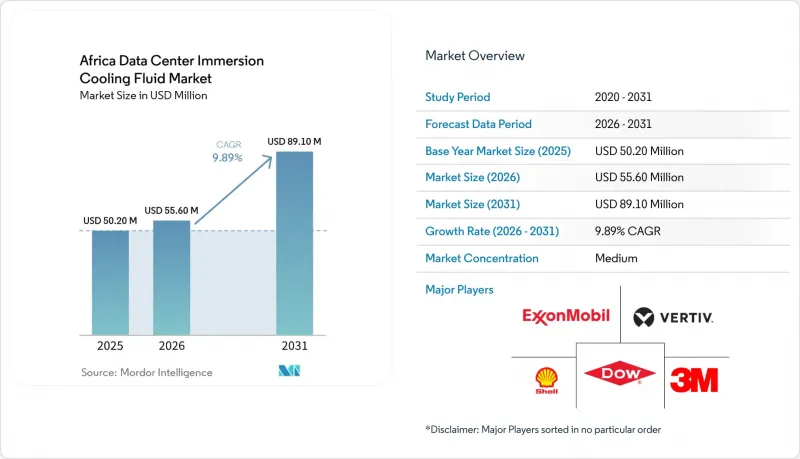

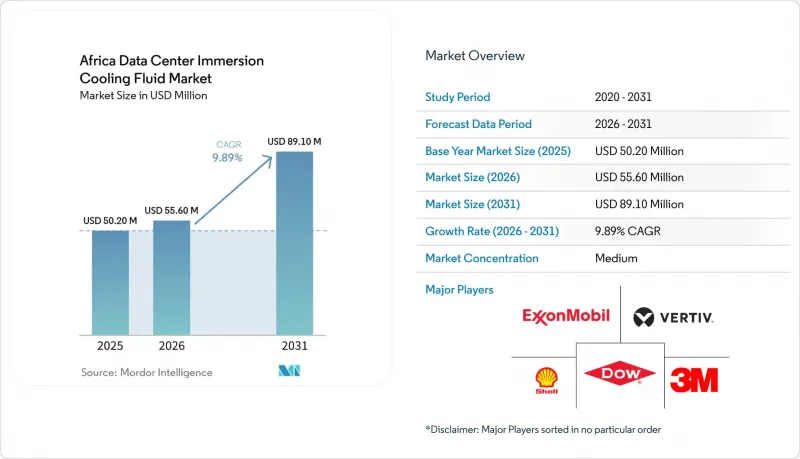

Mordor Intelligence에 의하면, 아프리카의 데이터센터 액침 냉각액 시장 규모는 2025년 5,020만 달러로 평가되었고, 2026년 5,560만 달러로 추정되고, 2031년까지 8,910만 달러로 확대될 전망이며, 2026-2031년 CAGR 9.89%를 나타낼 것으로 예측됩니다.

본 보고서는 유체 유형별(광물유 및 합성 탄화수소 등), 상 유형별(단상 및 이상), 데이터센터 유형별(클라우드 서비스 제공업체 및 코로케이션 등), 최종 사용자 산업별(IT/ITES 및 BFSI 등), 지역별(브라질 및 아르헨티나 등)로 세분화되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아프리카의 데이터센터 침지 냉각 유체 시장 동향 및 인사이트

요하네스버그 및 나이로비 회랑 지역의 하이퍼스케일 시설 확장

아프리카에서 가장 활발한 두 데이터센터 회랑은 현재 Teraco의 4억 4,200만 달러 규모 시설 확장 및 Equinix의 3억 9,000만 달러 규모 진출 계획에 힘입어 성장하고 있습니다. 이들 모두 100kW 이상의 랙을 수용할 수 있는 수냉식 홀을 갖추고 있습니다. 높은 광섬유 밀도, 캐리어 호텔, 그리고 해저 케이블과의 근접성 덕분에 사업자는 유럽 허브까지 40밀리초 미만의 지연 시간을 보장할 수 있으며, 이는 GPU 훈련 워크로드의 필수 조건입니다. 이 프로젝트의 금융 기관은 PUE 목표치를 1.2 미만으로 설정할 것을 요구하고 있으며, 이에 따라 액체 냉각이 사실상 표준 아키텍처로 자리 잡았습니다. 기기 OEM 업체들도 이러한 투자 동향에 발맞추어 유체 시스템의 리드 타임 단축을 도모하기 위해 하우텐 주와 키암부 군에 사전 재고 보관 거점을 마련하고 있습니다. 이러한 집적 효과로 인해 절연체 공급업체의 물류 비용이 절감되어, 2차 도시권 건설에서도 대규모 계약이 가능해졌습니다.

전기 요금 인상이 TCO 최적화를 촉진

2024년 나이지리아의 밴드 A 요금이 225 나이라/kWh(0.14달러/kWh)로 급등함에 따라, Tier III 시설의 운영비는 30% 이상 증가했습니다. 케냐의 상업용 요금은 0.202달러/kWh로 더 높으며, 한편 남아프리카공화국에서는 2025년 에스콤(Eskom)의 요금 인상으로 인해 대규모 전력 사용자의 평균 부담률이 18.7% 상승할 전망입니다. 수냉 방식은 서버 팬의 전력 소비를 줄이고 칠러의 부하를 제거함으로써 에너지 수요를 40-50% 절감하고, 블렌드 PUE를 1.05 수준까지 낮춥니다. 이를 통해 투자 회수 기간이 2-3년 단축됩니다. 현재 CFO들은 투자 분석서에 비용 인플레이션 시나리오를 반영하고 있으며, 자산 수명의 4년 차 이후에는 수냉 방식이 가장 비용 효율적인 선택지라고 결론 짓는 경우가 많아지고 있습니다. 또한, 요금 인상 압력으로 인해 현장형 태양광 발전과 축전지를 활용한 마이크로그리드에 대한 관심도 높아지고 있습니다. 그 설비 투자액은 침지 냉각을 통한 공조 설비의 설치 면적 절감과 자연스럽게 부합하는 것입니다.

특수 절연액의 현지 배합이 부족해 수입이 급증하고 있습니다.

사하라 이남 아프리카에는 절연유 ISO 인증 블렌딩 라인을 갖춘 시설이 단 두 곳뿐이어서, 대부분의 구매자는 ISO 탱크 1기당 3,000달러가 넘는 운송비를 지불하고 완제품을 수입할 수밖에 없습니다. 관세는 HS 코드 분류에 따라 5-10% 범위이며, 외화 부족으로 인해 통관이 수 주간 지연되는 경우가 많아, 그 결과 랙이 가동 불능 상태에 빠졌습니다. 소규모 사업자는 최소 발주 수량을 충족하지 못해, 계약 가격보다 15-20% 높은 스팟 프리미엄을 지불할 수밖에 없습니다. 국내 화학 제조업체들은 위탁 혼합 계약을 검토해 왔으나, 원료에 대한 높은 순도 요건으로 인해 테이크 오어 페이(최소 구매 보장) 물량이 보장되지 않는 한 투자를 주저하고 있습니다. 현지 생산 능력이 향상될 때까지는 공급 리스크와 급등한 운송비가 가격에 민감한 대도시권에서의 보급을 저해할 것으로 보입니다.

부문별 분석

2025년, 아프리카 데이터센터용 액침 냉각 유체 시장에서 광물유는 가격 경쟁력과 폭넓은 공급 가능성으로 인해 48.0%라는 최대 점유율을 차지했습니다. 바이오 에스터는 비용이 높은 편이지만, 자산운용사들이 지속가능성 공시를 면밀히 검토하는 가운데, 해당 부문에서 가장 높은 연평균 성장률(CAGR) 11.9%로 성장을 지속하고, 있습니다. 조달 체계 전반에 걸쳐 PFAS 무함유 의무화가 확대됨에 따라, 아프리카 데이터센터용 액침 냉각 유체 시장에서 바이오 에스테르 시장 규모는 급격히 확대될 것으로 예측됩니다. 합성 탄화수소는 틈새 시장인 고온 용도를 대상으로 하고 있으나, 불소계 제품은 PFAS 금지 조치로 인해 감소 추세를 보이고 있습니다.

TotalEnergies(BioLife)나 Cargill(NatureCool)과 같은 바이오 에스터 공급업체들은 하이퍼스케일 사업자들에게 생분해성의 이점을 강조하고 있으며, 또한, Chemours가 2025년 5월 Navin Fluorine과 체결한 제휴를 통해 Opteon의 생산 거점이 아프리카 대륙에 더 가까워지게 됩니다. 현지 배합 제조업체들은 수입 비용을 절감하기 위해 팜유 유래 원료를 모색하고 있지만, 자금 조달 문제는 여전히 남아 있습니다.

단상 설계는 2025년 매출의 73.5%를 차지했으며, 간편한 도입을 원하는 사업자들 사이에서 아프리카 데이터센터 액침 냉각액 시장 점유율의 기반을 형성하고 있습니다. 2상 시스템은 현재로서는 소수이지만, 100kW를 초과하는 GPU 랙 밀도를 구현할 수 있어 연평균 11.7%의 성장이 예상됩니다. 하이퍼스케일 AI 클러스터가 이 토폴로지를 대규모로 도입한다면, 아프리카 데이터센터 액침 냉각액 시장의 2상 유체 시장 규모는 2030년까지 두 배로 증가할 가능성이 있습니다.

존슨 컨트롤즈가 2025년 9월에 출시한 모듈형 CDU는 플러그 앤 플레이 방식을 통해 확장성을 제공함으로써 복잡성에 대한 우려를 해소하고 있습니다. 라고스와 나이로비에서 진행된 초기 시범 운영 결과, 공랭식 및 CRAH(냉각 공기 재순환) 개조 방식과 비교했을 때 TCO(총 소유 비용)를 20% 절감할 수 있음이 입증되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the africa data center immersion cooling fluid market size is projected to expand from USD 50.20 million in 2025 and USD 55.60 million in 2026 to USD 89.10 million by 2031, registering a CAGR of 9.89% between 2026 to 2031.

This report is Segmented by Fluid Type (Mineral Oil and Synthetic Hydrocarbon, and More), Phase Type (Single-Phase and Two-Phase), Data Center Type (Cloud Service Providers and Colocation, and More), End-User Industry (IT/ITES and BFSI, and More), and Geography (Brazil and Argentina, and More). The Market Forecasts are Provided in Terms of Value (USD).

Africa Data Center Immersion Cooling Fluid Market Trends and Insights

Hyperscale build-outs in Johannesburg and Nairobi corridors

Africa's two most active data-center corridors are now anchored by Teraco's USD 442 million facility expansion and Equinix's USD 390 million entry plan, both of which specify immersion-ready halls capable of 100 kW-plus racks. High fiber density, carrier hotels, and submarine-cable proximity let operators guarantee sub-40 ms latency to European hubs, a prerequisite for GPU training workloads. Project lenders insist on PUE targets under 1.2, effectively locking in liquid cooling as the baseline architecture. Equipment OEMs follow the investment, placing forward-stock depots in Gauteng and Kiambu counties to shorten lead times for fluid systems. The clustering effect lowers logistics costs for dielectric suppliers, making bulk contracts viable for secondary metro builds.

Rising electricity tariffs driving TCO optimization

Nigeria's Band A tariff leap to NGN 225/kWh (USD 0.14/kWh) in 2024 pushed operating expenditure up by more than 30% for Tier III facilities. Kenya's commercial tariff sits even higher at USD 0.202/kWh, while South Africa's 2025 Eskom hike averages 18.7% on large-power users. Immersion cooling cuts server-fan draw and eliminates chiller loads, shrinking energy needs 40-50% and pushing blended PUE close to 1.05, which in turn shaves two to three years off payback periods. CFOs now build tariff-inflation scenarios into investment memos, often finding liquid cooling the least-cost option beyond year 4 of asset life. The tariff pressure also boosts interest in on-site solar-plus-battery microgrids, whose capex aligns naturally with immersion's reduced HVAC footprint.

Scarce local blending of specialty dielectrics inflating imports

Only two sub-Saharan facilities possess ISO-certified blending lines for dielectric fluids, forcing most buyers to import finished product at freight rates exceeding USD 3,000 per ISO tank. Duties range between 5-10% depending on HS code classification, and forex shortages often delay customs clearance by weeks, leaving racks idle. Smaller operators cannot meet minimum-order quantities, paying spot premiums of 15-20% over contract pricing. Domestic chemical firms have considered toll-blending agreements, yet high feedstock purity requirements deter investment without guaranteed take-or-pay volumes. Until local capacity improves, supply risk and elevated landed cost will cap adoption in price-sensitive metros.

Other drivers and restraints analyzed in the detailed report include:

- Severe water stress in Cape Town and Sahel favoring liquid cooling

- Pan-African AI/ML clusters for fintech and e-commerce

- Higher up-front CAPEX vs. legacy air cooling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oil secured the highest 48.0% share of the Africa data center immersion cooling fluid market in 2025, owing to favorable pricing and broad availability. Bio-esters, though costlier, post the segment's quickest 11.9% CAGR as asset managers scrutinize sustainability disclosures. The Africa data center immersion cooling fluid market size for bio-esters is projected to climb sharply as PFAS-free mandates spread across procurement frameworks. Synthetic hydrocarbons target niche high-heat applications, while fluorocarbon products trend downward following PFAS prohibitions.

Bio-ester suppliers such as TotalEnergies (BioLife) and Cargill (NatureCool) pitch biodegradability advantages to hyperscale bidders, and Chemours' May 2025 alliance with Navin Fluorine adds Opteon production closer to the continent. Local formulators explore palm-derivative feedstocks to cut import bills, though financing hurdles persist.

Single-phase designs represented 73.5% of 2025 revenue, anchoring the Africa data center immersion cooling fluid market share among operators seeking straightforward rollout. Two-phase installations, while only a minority today, are forecast to grow 11.7% annually as they enable GPU rack densities exceeding 100 kW. The Africa data center immersion cooling fluid market size for two-phase fluids could double by 2030 if hyperscale AI clusters adopt the topology at scale.

Johnson Controls' September 2025 modular CDU launch mitigates complexity fears by offering plug-and-play expansion; early pilots in Lagos and Nairobi demonstrate 20% TCO savings versus air-cooled plus CRAH retrofits.

List of Companies Covered in this Report:

- 3M

- The Dow Chemical Company

- Exxon Mobil Corporation

- Shell plc

- The Chemours Company

- Cargill Incorporated

- Castrol Limited (BP)

- FUCHS SE

- The Lubrizol Corporation

- Engineered Fluids Inc.

- Submer Technologies S.L.

- Asperitas

- Iceotope Technologies

- LiquidStack

- Green Revolution Cooling

- Vertiv

- Schneider Electric

- Dell Technologies

- Supermicro

- Asetek

- FluoroCool

- BitCool

- DCX - The Liquid Cooling Co.

- Allied Control Ltd.

- Giga Cooling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale build-outs in Johannesburg and Nairobi corridors

- 4.2.2 Rising electricity tariffs driving TCO optimisation

- 4.2.3 Severe water-stress in Cape Town and Sahel favouring liquid cooling

- 4.2.4 Pan-African AI/ML clusters for fintech and e-commerce

- 4.2.5 Data-centre tax incentives (e.g., Kenya Investment Promotion Act)

- 4.2.6 Shift to PFAS-free bio-ester fluids for ESG reporting

- 4.3 Market Restraints

- 4.3.1 Scarce local blending of specialty dielectrics inflating imports

- 4.3.2 Higher up-front CAPEX vs. legacy air cooling

- 4.3.3 Absence of African immersion-cooling safety standards

- 4.3.4 Supply-chain risk amid global PFAS phase-out

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS

- 5.1 By Fluid Type

- 5.1.1 Mineral Oil

- 5.1.2 Synthetic Hydrocarbon

- 5.1.3 Fluorocarbon-based Fluids

- 5.1.4 Bio-based Esters

- 5.2 By Phase Type

- 5.2.1 Single-Phase

- 5.2.2 Two-Phase

- 5.3 By Data Center Type

- 5.3.1 Cloud Service Providers

- 5.3.2 Colocation

- 5.3.3 On-Premise / Enterprise / Edge

- 5.4 By End-User Industry

- 5.4.1 IT / ITES

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Government and Defense

- 5.4.5 Media and Entertainment

- 5.4.6 Other End-Users

- 5.5 By Country

- 5.5.1 South Africa

- 5.5.2 Nigeria

- 5.5.3 Kenya

- 5.5.4 Egypt

- 5.5.5 Morocco

- 5.5.6 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 3M

- 6.2.2 The Dow Chemical Company

- 6.2.3 Exxon Mobil Corporation

- 6.2.4 Shell plc

- 6.2.5 The Chemours Company

- 6.2.6 Cargill Incorporated

- 6.2.7 Castrol Limited (BP)

- 6.2.8 FUCHS SE

- 6.2.9 The Lubrizol Corporation

- 6.2.10 Engineered Fluids Inc.

- 6.2.11 Submer Technologies S.L.

- 6.2.12 Asperitas

- 6.2.13 Iceotope Technologies

- 6.2.14 LiquidStack

- 6.2.15 Green Revolution Cooling

- 6.2.16 Vertiv

- 6.2.17 Schneider Electric

- 6.2.18 Dell Technologies

- 6.2.19 Supermicro

- 6.2.20 Asetek

- 6.2.21 FluoroCool

- 6.2.22 BitCool

- 6.2.23 DCX - The Liquid Cooling Co.

- 6.2.24 Allied Control Ltd.

- 6.2.25 Giga Cooling

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment