|

시장보고서

상품코드

2063376

하이브리드 라벨 인쇄 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hybrid Label Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

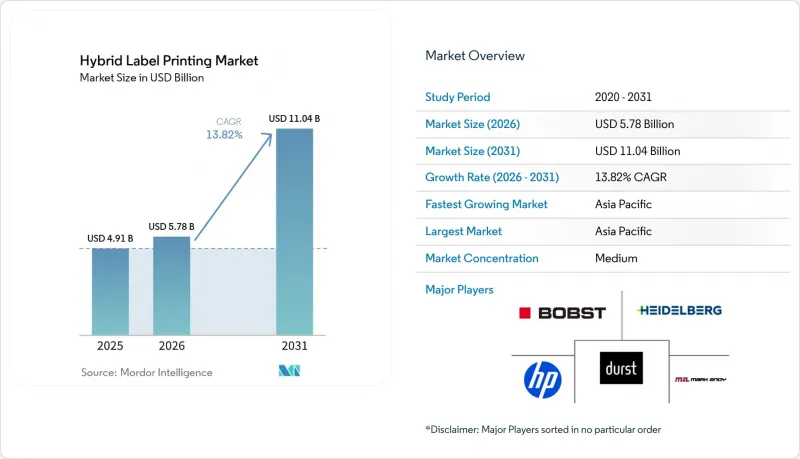

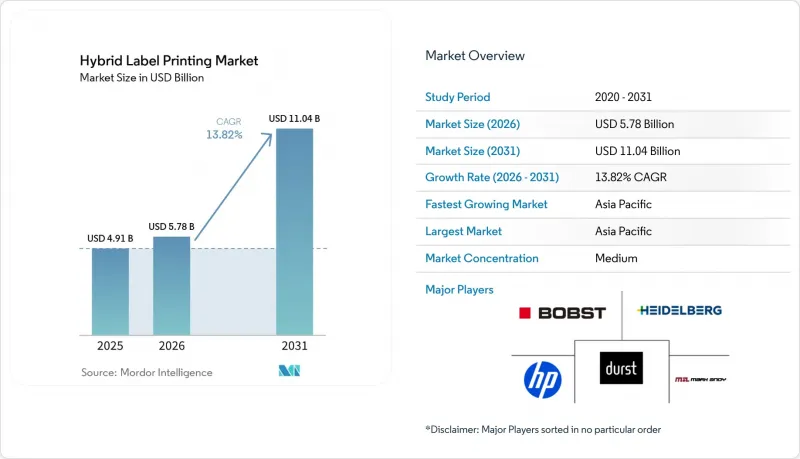

Mordor Intelligence에 의하면, 하이브리드 라벨 인쇄 시장 규모는 2025년에 49억 1,000만 달러로 평가되었고, 2026년 57억 8,000만 달러로 추정되고, 2031년까지 110억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 13.82%를 나타낼 전망입니다.

본 보고서는 인쇄 기술별(플렉소 및 UV 잉크젯 하이브리드, 플렉소 및 일렉트로포토그래픽 하이브리드 등), 인쇄기 유형별(나로우브 등), 잉크 유형별(UV-LED 경화형 잉크 등), 기판 유형별(종이 및 판지, 필름 등), 최종 사용자 산업별(식품, 음료, 의약품 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 하이브리드 라벨 인쇄 시장 동향 및 인사이트

소량 SKU 증가와 개인화 수요

소비재 공급업체들은 현재 수백 가지에 달하는 제품 라인업을 취급하고 있으며, 2024년 이후 최소 주문 수량을 60% 줄이고 1,000미터 미만의 소량 생산이 일상화되고 있습니다. 하이브리드 인쇄기는 재조정 없이 디지털 인쇄와 플렉소 인쇄를 실시간으로 원활하게 전환할 수 있어, 이러한 작업 환경에서 뛰어난 성능을 발휘하며 길이가 다른 모든 작업에 걸쳐 단위당 경제성을 유지합니다. 유럽에서 도입이 예정된 '디지털 제품 여권' 제도는 가변 데이터를 포장 관련 법규에 명시함으로써 하이브리드 인쇄의 보급을 가속화하고 있습니다. 예전에는 지역별 프로모션 자료를 1년에 한 번 인쇄하던 브랜드도, 현재는 분기마다 그래픽을 업데이트하고 있으며, 이러한 빈도의 업데이트는 통합된 하이브리드 워크플로우가 있어야만 가능합니다. 이와 동시에 음료 제조업체들은 수축 슬리브의 QR 코드를 로열티 프로그램과 연동하고 있으며, 플렉소 인쇄 공급망 내에서 정확하고 정밀한 위치 조정이 가능한 디지털 장식 기술에 대한 컨버터 수요가 증가하고 있습니다.

UV 잉크젯과 플렉소의 품질 격차 해소

1,200×1,200 dpi의 해상도와 ±5마이크로미터의 토출 정밀도로 작동하는 후지필름 디매틱스의 헤드는 잉크젯 인쇄와 애닐록스 기반 인쇄 사이에 오랫동안 존재해 온 불투명도 및 미세 문자의 선명도 차이를 해소했습니다. 이러한 품질의 균일화를 통해, 기존에는 오프셋 인쇄나 그라비아 인쇄가 주류를 이루던 의약품 및 화장품 라벨 인쇄가 가능해졌습니다. 현재 각 변환기 제조업체들은 풀블리드 컬러, 마이크로 텍스트, 바코드를 한 번의 인쇄 과정으로 처리하고 있으며, 검사원이 이를 구분할 수 없습니다는 점을 확신하고 있습니다. 품질 면에서의 타협이 사라짐에 따라 브랜드 감사도 간소화되었으며, 감사는 엄격한 반면 속도에 대한 기대도 높은 아시아 전역의 규제가 엄격한 공급망에서 하이브리드 방식의 도입이 촉진되고 있습니다.

높은 초기 설비 투자

완전 통합형 하이브리드 플랫폼의 가격은 200만 달러에서 800만 달러에 달하며, 단일 기술 인쇄기에 비해 40-60% 더 비싸기 때문에 많은 중견 변환 업체들이 도입을 보류하고 있습니다. 하이델베르거 드루크마시넨사의 리스 제도를 통해 초기 비용은 70% 절감되지만, 그럼에도 불구하고 이자 부담이 초기 현금 흐름을 압박하고 있습니다. 아시아의 소규모 변환업체들은 컨소시엄 소유의 설비 풀에 생산량을 집중시키는 경우가 많지만, 소유권이 분산되어 예방 정비 계획이 복잡해지고, 투자 수익률(ROI) 회수 기간이 길어지고 있습니다. 신흥국 정부는 설비 투자를 상쇄하기 위해 가속 상각 제도를 도입하기 시작했으나, 이러한 우대 조치는 여전히 불충분합니다.

부문별 분석

2025년, UV 잉크젯·플렉소·하이브리드 장비는 하이브리드 라벨 인쇄 시장의 46.83%를 차지했으며, 다단계 공정에 대응할 수 있는 민첩성을 추구하는 컨버터들에게 표준 아키텍처로서의 입지를 공고히 했습니다. 인라인형 올인원 하이브리드 시장은 현재 규모가 작지만, 2031년까지 연평균 성장률(CAGR) 16.21%를 나타낼 것으로 예측되며, 이는 해당 부문이 긴밀하게 통합되고 소프트웨어로 제어되는 생산 셀로 전환되고 있음을 보여줍니다. 특히, 전자광학 하이브리드 기술은 불투명한 백색층이나 금속박에 대해 극히 정밀한 위치 정렬이 요구되는 고급 화장품 분야에서 지속적인 관심을 받고 있습니다. 스테이션당 40만 달러 미만의 가격대로 도입 가능한 디지털 바 레트로핏은 소규모 기업이 전체 라인 교체 비용을 부담하지 않고도 가변 데이터 인쇄 업무에 단계적으로 진입할 수 있는 길을 열어줍니다.

이러한 플랫폼에 통합된 AI 기반 비전 시스템은 기존의 오프라인 검사와 비교해 이미 폐기물을 15-20% 줄였습니다. 이러한 효율성은 품질이 극히 중요한 산업, 특히 제약 업계에서 하이브리드 라벨 인쇄 시장의 입지를 더욱 공고히 하고 있습니다. 예측 기간 동안 생산성 향상의 대부분은 하드웨어 교체가 아닌 소프트웨어 업그레이드를 통해 이루어질 것이며, 이는 주요 OEM 업체들이 채택하고 있는 구독형 수익 모델을 강화하는 결과를 가져올 것입니다. 그 결과, 하이브리드 라벨 인쇄 시장은 소규모 수제 맥주 라벨 제조업체부터 다국적 대형 포장 기업에 이르기까지, 모든 규모의 변환 업체들의 기술 로드맵에서 결정적인 위치를 차지하고 있습니다.

와이드 웹형 하이브리드 기기는 2025년에 매출의 48.26%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 15.18%로 성장할 것으로 전망되어, 2025년 이후 면적이 30% 확대된 대형 물류 라벨 시장에서 이 기기가 수행할 핵심적인 역할을 여실히 보여주고 있습니다. 나로우브형 유닛은 시장 점유율이 점차 줄어들고 있지만, 마이크론 단위의 정밀도 조절이 필요한 전자기기 및 의료기기 분야에서는 여전히 없어서는 안 될 존재입니다. 미드웹 인쇄기는 이러한 양극단을 연결하는 가교 역할을 하며, 와이드웹 기계와 같은 설치 공간의 제약을 초래하지 않으면서도 포맷의 유연성을 필요로 하는 컨버터 업체에 서비스를 제공함으로써, 경쟁력 있는 중견 시장 내 틈새 시장을 구축하고 있습니다.

RFID 지원 출하 라벨을 도입한 전자상거래 물류센터들은 2열 인쇄가 가능한 와이드 웹 장비에 대한 투자를 확대하고 있으며, 인력을 증원하지 않고도 처리량을 두 배로 늘리고 있습니다. 이에 반해, 좁은 폭 인쇄기 제조업체들은 웹 가이드 및 터렛 리와인더 시스템의 자동화를 통해 작업자 대 인쇄기 비율을 1대 3으로 달성함으로써 인건비를 절감하고 있습니다. 중형 웹 플랫폼은 소규모 맞춤형 생산에서 산업 규모 생산으로 사업을 확장하는 기업들에게 전환기의 자산으로서 그 역할을 점점 더 잘 수행하고 있으며, 기술 도입 비용을 경제적으로 절감함으로써 하이브리드 라벨 인쇄 시장의 공유 생태계를 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 35.27%를 차지한 것으로 평가되었으, 중국의 제조 규모, 인도의 제약 산업 확대, 그리고 아세안(ASEAN) 국가들의 정부 주도의 스마트 공장 구상에 힘입어 연평균 성장률(CAGR) 15.25%를 나타낼 것으로 전망됩니다. 중국의 컨버터는 매일 수백만 개의 소포를 발송하는 크로스보더 전자상거래 플랫폼에 대응하기 위해 와이드 웹형 하이브리드 기계를 도입하고 있습니다. 한편, 인도의 의약품 수출업체들은 미국 FDA의 수입 기준을 충족하기 위해 저이동성 시스템에 투자하고 있습니다. 일본과 한국은 특히 AI 기반 비전 시스템 및 세라믹 잉크젯 노즐 기술 분야에서 첨단 연구개발(R&D)에 기여하며, 지역 혁신 사이클을 가속화하고 있습니다.

북미는 성숙한 시장이지만, '식품안전현대화법'에 따라 실시간 추적성이 의무화됨에 따라 각 변환업체들이 기존의 플렉소 인쇄 라인을 폐지하고, QR 코드의 가변 배치가 가능한 하이브리드 플랫폼으로의 전환을 추진하는 등 건전한 설비 갱신 추세가 유지되고 있습니다. 미국은 또한 중서부에 위치한 대규모 위탁 포장 허브의 혜택을 누리고 있으며, 이곳에서는 의약품 및 건강기능식품 라벨 생산이 한곳에 집중되어 있습니다. 멕시코는 니어쇼어링의 선두주자로 부상하고 있으며, USMCA(미국·멕시코·캐나다 협정) 규정에 따라 하이브리드 장비를 관세 없이 수입하여 완제품을 광범위한 지역으로 수출하고 있습니다.

유럽의 성장은 정책 주도의 디지털화를 반영하고 있습니다. '디지털 제품 여권', 화학물질 관리 규정(REACH), 생산자 책임 확대(EPR)에 따른 수수료 등은 모두 주문형 가변 데이터를 지원하는 하이브리드 워크플로우를 뒷받침하고 있습니다. 독일에서는 중견/중소기업(미텔슈탄트)의 컨버터 기반이 설비 도입의 토대가 되고 있는 반면, 영국의 생명과학 코리더는 의약품 수요를 견인하고 있습니다. 동유럽은 비용 경쟁력이 있는 노동력을 공급하는 한편, 서유럽의 경쟁사들과의 차별화를 꾀하기 위해 최첨단 기계를 도입하고 있으며, 2031년까지 하이브리드 라벨 인쇄 시장을 뒷받침할 범유럽적인 설비 교체 주기를 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the hybrid label printing market size was valued at USD 4.91 billion in 2025 and is estimated to grow from USD 5.78 billion in 2026 to reach USD 11.04 billion by 2031, at a CAGR of 13.82% during the forecast period (2026-2031).

This report is Segmented by Printing Technology (Flexo-UV Inkjet Hybrid, Flexo-Electrophotographic Hybrid, and More), Press Type (Narrow-Web, and More), Ink Type (UV-LED Curable Inks, and More), Substrate Type (Paper and Paperboard, Films, and More), End-User Industry (Food, Beverages, Pharmaceuticals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Hybrid Label Printing Market Trends and Insights

Short-Run SKU Proliferation and Personalization Demands

Consumer-goods suppliers now juggle hundreds of product variants, slashing minimum order quantities by 60% since 2024 and making runs of under 1,000 meters routine. Hybrid presses excel under this workload because they seamlessly switch between digital and flexo printing on the fly without requiring recalibration, thereby preserving unit economics across variable-length jobs. Europe's incoming Digital Product Passport scheme accelerates uptake by hard-coding variable data into packaging legislation. Brands that previously printed region-specific promotions annually now refresh graphics quarterly, a cadence only feasible with integrated hybrid workflows. In tandem, beverage marketers have linked QR codes on shrink sleeves to loyalty programs, raising converter demand for precise, in-register digital embellishment within flexographic supply chains.

Rising Quality Parity of UV-Inkjet with Flexo

Fujifilm Dimatix heads operating at 1,200 X 1,200 dpi and +-5 µm drop accuracy have erased the historic gap in opacity and fine text clarity between inkjet and anilox-based printing. This parity unlocks pharmaceutical and cosmetic labels that previously defaulted to offset or gravure printing. Converters now run full-bleed color, microtext, and barcodes in one pass, confident that inspectors cannot distinguish between them. The removal of quality compromises also simplifies brand audits, driving hybrid adoption into highly regulated supply chains across Asia, where audits are rigorous yet speed expectations remain high.

High Initial Capital Expenditure

Fully integrated hybrid platforms range from USD 2 million to USD 8 million, a 40-60% premium over single-technology presses, keeping many mid-size converters on the sidelines. Although leasing schemes from Heidelberger Druckmaschinen cut up-front payments by 70%, interest expenses still erode early cash flows. Smaller Asian converters often pool volumes into consortium-owned equipment parks, but ownership fragmentation complicates preventive maintenance planning and lengthens ROI timelines. Emerging-market governments have started offering accelerated depreciation to offset Capex, yet such incentives remain patchy.

Other drivers and restraints analyzed in the detailed report include:

- Converter Push for Single-Pass Inline Finishing

- Hybrid Presses Embedded with AI Predictive Maintenance

- Shortage of Dual-Skilled (Flexo and Digital) Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, UV-inkjet flexo hybrids accounted for a 46.83% share of the hybrid label printing market, reinforcing their status as the baseline architecture for converters seeking multi-process agility. Inline all-in-one hybrids, though smaller today, are forecast to log a 16.21% CAGR to 2031, indicating the segment's pivot toward tightly integrated, software-orchestrated production cells. Notably, electrophotographic hybrids find sustained interest in luxury cosmetics where opaque white layers and metallic foils require ultra-precise registration. Retrofittable digital bars, priced under USD 400,000 per station, provide smaller firms with an incremental pathway into variable-data jobs without triggering full-line replacement costs.

AI-powered vision systems embedded in these platforms already pare waste by 15-20% compared with legacy offline inspection. That efficiency further solidifies the hybrid label printing market's position in quality-critical verticals, especially the pharmaceutical industry. Over the forecast horizon, software upgrades rather than hardware swaps will deliver most productivity gains, reinforcing the subscription-based revenue models adopted by leading OEMs. Consequently, the hybrid label printing market occupies a decisive position in technology roadmaps across every tier of converter, from boutique craft-beer labelers to multinational packaging conglomerates.

Wide-web hybrids accounted for 48.26% of revenue in 2025 and are projected to expand at a 15.18% CAGR through 2031, underscoring their central role in large-format logistics labels, which have grown 30% in area since 2025 Narrow-web units, while ceding share, remain indispensable for electronics and medical devices that demand micron-level registration. Mid-web presses bridge these extremes, serving converters that require format agility without incurring wide-web floor-space penalties, thus anchoring a competitive mid-market niche.

E-commerce warehouses adopting RFID-enabled shipping labels are prompting wide-web investments that unlock two-lane printing, doubling throughput without new headcount. Narrow-web players counter by automating web-guiding and turret-rewind systems, achieving an operator-to-press ratio of 1:3 and thereby trimming labor costs. Mid-web platforms are increasingly acting as transitional assets for firms scaling from artisanal runs to industrial work, supporting the hybrid label printing market share ecosystem by keeping the technology ladder financially accessible.

Geography Analysis

Asia-Pacific generated 35.27% of 2025 revenue and is poised for a 15.25% CAGR, driven by China's manufacturing scale, India's pharmaceutical expansion, and state-backed smart factory initiatives across ASEAN economies. Chinese converters deploy wide-web hybrids to serve cross-border e-commerce platforms that ship millions of parcels daily, while Indian drug exporters invest in low-migration systems to meet U.S. FDA import standards. Japan and South Korea contribute high-end R&D, especially in AI-enabled vision systems and ceramic inkjet nozzle technologies, amplifying regional innovation cycles.

North America, though mature, sustains healthy upgrade momentum as the Food Safety Modernization Act compels real-time traceability, encouraging converters to retire legacy flexo lines in favor of hybrid platforms capable of variable QR code placement. The United States further benefits from large-scale contract packaging hubs in the Midwest, which consolidate pharmaceutical and nutraceutical label runs under one roof. Mexico emerges as a near-shoring winner, importing hybrid equipment duty-free under USMCA rules and exporting finished goods into the wider region.

Europe's growth reflects policy-led digitalization: the Digital Product Passport, REACH chemicals management, and extended producer responsibility fees all favor hybrid workflows for on-demand variable data. Germany anchors equipment adoption through its sizable Mittelstand converter base, while the United Kingdom's life-science corridor boosts pharmaceutical demand. Eastern Europe offers cost-competitive labor but adopts top-tier machinery to differentiate against Western rivals, reinforcing a pan-European upgrade cycle that sustains the hybrid label printing market through 2031.

- Bobst Group SA

- Heidelberger Druckmaschinen AG

- Mark Andy Inc.

- Durst Group AG

- HP Inc.

- Fujifilm Holdings Corporation

- Xeikon BV (Flint Group)

- Nilpeter A/S

- Konica Minolta, Inc.

- Koenig & Bauer AG

- Omet S.r.l.

- MPS Systems B.V.

- Screen Holdings Co., Ltd.

- Epson Corporation

- Uteco Converting S.p.A.

- Windmoller & Holscher KG

- Comexi Group Industries S.A.U.

- AB Graphic International Ltd.

- CEI BossJet

- Grafotronic AB

- Lombardi Converting Machinery S.p.A.

- Delta ModTech

- Kento Digital Printing S.L.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Short-Run SKU Proliferation and Personalization Demands

- 4.2.2 Rising Quality Parity Of UV-Inkjet with Flexo

- 4.2.3 Converter Push for Single-Pass Inline Finishing

- 4.2.4 Hybrid Presses Embedded with AI Predictive Maintenance

- 4.2.5 Leasing Models Lowering Capex Hurdle

- 4.2.6 Brand-Owner Demand For QR-Enabled Digital Product Passports

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure

- 4.3.2 Shortage of Dual-Skilled Operators

- 4.3.3 Supply-Risk on Platinum-Based Silicone Liners

- 4.3.4 Tariff Volatility on Electronic Components for Inkjet Heads

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Flexo-UV Inkjet Hybrid

- 5.1.2 Flexo-Electrophotographic Hybrid

- 5.1.3 Retrofitted Digital Print Bars

- 5.1.4 Inline All-in-One Hybrid Systems

- 5.1.5 Other Printing Technologies

- 5.2 By Press Type

- 5.2.1 Narrow-web

- 5.2.2 Mid-web

- 5.2.3 Wide-web

- 5.3 By Ink Type

- 5.3.1 UV-LED Curable Inks

- 5.3.2 Water-based Inkjet Inks

- 5.3.3 LED Dual-Cure Flexo Inks

- 5.3.4 Low-migration Inks

- 5.4 By Substrates

- 5.4.1 Paper and Paperboard

- 5.4.2 Films (PP, PE, PET)

- 5.4.3 Metallic and Foil

- 5.4.4 Specialty and Sustainable Stocks

- 5.4.5 Other Substrates

- 5.5 By End-user Industry

- 5.5.1 Food

- 5.5.2 Beverages

- 5.5.3 Pharmaceuticals

- 5.5.4 Personal Care and Cosmetics

- 5.5.5 Industrial and Chemical

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bobst Group SA

- 6.4.2 Heidelberger Druckmaschinen AG

- 6.4.3 Mark Andy Inc.

- 6.4.4 Durst Group AG

- 6.4.5 HP Inc.

- 6.4.6 Fujifilm Holdings Corporation

- 6.4.7 Xeikon BV (Flint Group)

- 6.4.8 Nilpeter A/S

- 6.4.9 Konica Minolta, Inc.

- 6.4.10 Koenig & Bauer AG

- 6.4.11 Omet S.r.l.

- 6.4.12 MPS Systems B.V.

- 6.4.13 Screen Holdings Co., Ltd.

- 6.4.14 Epson Corporation

- 6.4.15 Uteco Converting S.p.A.

- 6.4.16 Windmoller & Holscher KG

- 6.4.17 Comexi Group Industries S.A.U.

- 6.4.18 AB Graphic International Ltd.

- 6.4.19 CEI BossJet

- 6.4.20 Grafotronic AB

- 6.4.21 Lombardi Converting Machinery S.p.A.

- 6.4.22 Delta ModTech

- 6.4.23 Kento Digital Printing S.L.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment