|

시장보고서

상품코드

2063386

석유 및 가스 산업용 밸브 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Valves In Oil And Gas Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

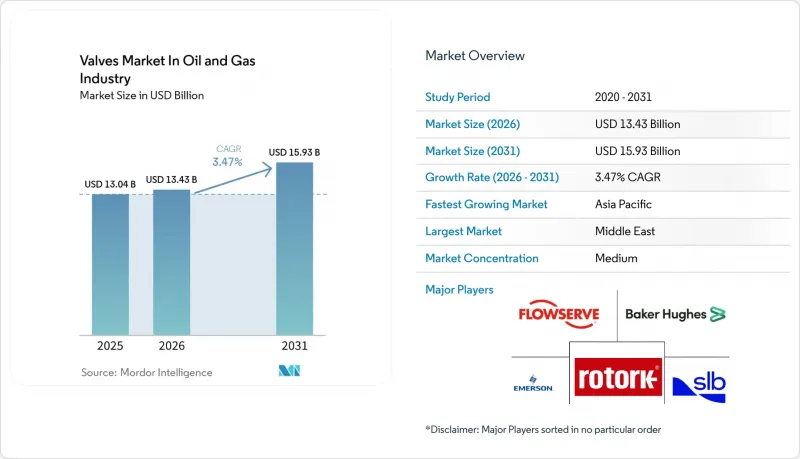

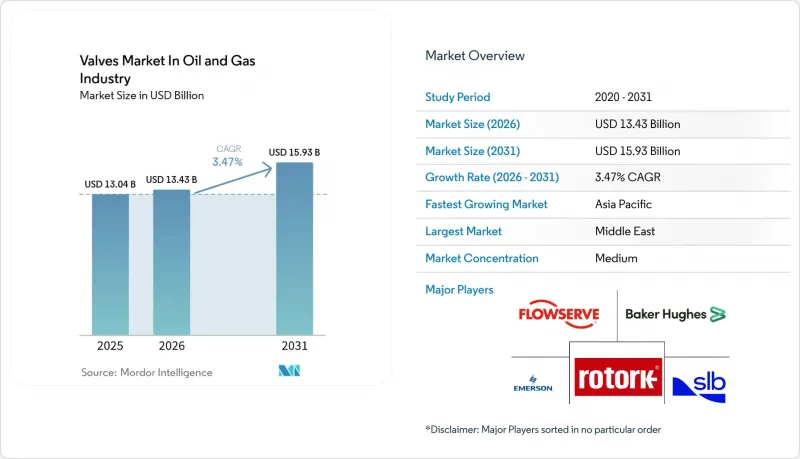

Mordor Intelligence에 의하면, 석유 및 가스 산업용 밸브 시장 규모는 2025년 130억 4,000만 달러로 평가되었습니다. 2026년에는 134억 3,000만 달러로 확대되어 2031년까지 159억 3,000만 달러에 이를 것으로 예측되며, CAGR은 3.47%를 나타낼 전망입니다.

본 보고서는 밸브 유형(볼 밸브, 게이트 밸브, 글로브 밸브, 기타), 재질(주강, 단조강, 스테인리스, 기타), 용도(업스트림, 중류, 기타), 작동 방식(수동, 공압식, 기타), 크기(6인치 이하, 6-12인치, 12-24인치, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

석유 및 가스 산업용 밸브 시장 동향 및 전망

확대되는 업스트림·중류 파이프라인 프로젝트

업스트림 부문의 지출은 전년 대비 4% 감소했음에도 불구하고, 2025년에는 5,700억 달러까지 회복되었으며, 분석가들은 2030년까지 7,380억 달러로 증가할 것으로 예측했습니다. 브라질의 심해 개발 프로젝트와 사우디아라비아의 비전통 가스 개발 사업에서는 사워 가스 대응용 고압 게이트 밸브 및 볼 밸브에 관한 다년 계약이 체결되었습니다. 중류 부문의 성장도 마찬가지였는데, 엠브리지(Embridge)사가 2024년에 14억 달러 규모의 가스 파이프라인을 승인한 데 이어, ADNOC는 내식성 체크 밸브가 필요한 24억 달러 규모의 해수 주입 네트워크에 자금을 지원했습니다. 중국의 국가전망은 48인치 간선 파이프라인을 증설하고 있어, 24인치 이상의 밸브에 대한 수요를 끌어올리고 있습니다. API 6D 및 ISO 15848 준수는 현재 표준 조달 조건으로 자리 잡고 있습니다.

LNG 터미널 건설의 급증

2030년까지 연간 약 3,000억 m³ 규모의 신규 액화 설비 완공이 예정되어 있으며, 그 선두에는 2025년에 승인된 800억 m³ 규모의 프로젝트가 있습니다. 카타르 에너지(Qatar Energy)가 추진하는 300억 달러 규모의 노스 필드 확장 계획은 생산 능력을 연간 1억 2,600만 톤으로 확대하기 위해, -196°C의 환경에서도 사용 가능하도록 설계된 수천 개의 극저온용 볼 밸브와 트리플 오프셋 버터플라이 밸브가 필요합니다. 인도, 베트남, 필리핀 각지의 수입 터미널에서는 현지 재고를 보유하고 있으며, 베이커 휴즈(Baker Hughes)로부터 API 6FA 내화 검사 인증을 취득한 공급업체가 우선적으로 선정됩니다. 연평균 성장률(CAGR) 4.72%로 성장하고 있는 합금강과 듀얼페이즈강은 LNG 설비 특유의 열 사이클로 인한 손상을 견뎌냅니다. EPC 계약에 포함된 현지 사후 서비스 조항은 멀리 떨어진 공급업체에게 진입 장벽이 되고 있습니다.

원유 가격 변동이 설비 투자를 억제

2024년부터 2025년에 걸쳐 브렌트 원유 가격은 배럴당 70-90달러 사이에서 등락을 거듭했으며, 이로 인해 최종 투자 결정이 지연되면서 수익성이 낮은 프로젝트용 밸브 수주가 감소했습니다. 셰일 업체들이 성장보다 자유 현금 흐름을 우선시한 결과, 2025년 업스트림 부문 지출은 전년 대비 4% 감소한 5,700억 달러를 기록했습니다. 퍼미안 분지의 생산자들은 파이프라인 연결을 미루면서 유정 밸브 수요를 위축시켰습니다. 한편, 북해와 멕시코만의 자산에 대해서는 비용이 많이 드는 해저 설비 교체보다는 해체 조치가 선택되었습니다. 사업자들은 예비 재고를 보유하는 것을 꺼리기 때문에 경기 침체기에는 미결제 주문 잔고가 회복기보다 더 빠르게 감소합니다. 그 결과, 공급업체들은 수익의 주기적인 변동에 직면하게 되었으며, 생산 계획 수립이 복잡해지고 있습니다.

부문별 분석

디지털 트윈의 활용에 힘입어 제어 밸브 시장은 연평균 성장률(CAGR) 5.12%로 확대될 것으로 예상되며, 석유 및 가스 산업의 전체 밸브 시장 성장률을 상회하는 성장이 전망됩니다. 2025년 시점에서 온/오프 차단 용도에서는 볼 밸브가 33.53%의 점유율을 유지한 반면, 고압 시추 및 해저 트리에서는 게이트 밸브가 주류를 이루었습니다. 플러그 밸브와 버터플라이 밸브는 연마성 슬러리 및 대구경 저압 배관 분야에서 틈새 시장을 개척하고 있습니다. 석유 및 가스 산업의 제어 밸브 시장은 예측 분석을 통한 처리 능력 최적화가 진행됨에 따라 확대될 것으로 전망됩니다.

예지 보전을 통해 제어 밸브의 가동률은 높은 수준으로 유지되고 있으며, 사업자는 API 607 화재 검사 외에도 ISO 15848에 따른 누출 배출량 평가를 실시하도록 요구받고 있습니다. 전동 구동 방식은 조절 정밀도를 향상시켜 제어 밸브의 발전을 촉진하고 있습니다. 새로운 규격이 제정될 때마다 시장 진입 장벽이 높아져, 세계적 규모의 검사 시설과 디지털 서비스 제품군을 갖춘 기존 기업들을 보호하고 있습니다.

2025년에는 주강이 27.31%의 점유율을 차지했으나, 산성 가스나 수소 혼합 가스의 사용에 따라 내식성 향상이 요구됨에 따라, 합금강과 듀얼 페이즈 강은 연평균 4.72%의 성장이 예상됩니다. 현재 카타르의 확장된 노스필드 공정 라인에는 2상강이 채택되어 있으며, 에머슨의 HV-7000 수소 조절기에는 니켈 합금이 사용되고 있습니다. NACE MR0175 규격 준수가 보편화됨에 따라, 석유 및 가스 산업에서 합금강 밸브 시장 점유율은 확대될 전망입니다.

1만 psi급 유정 입구 설비에는 여전히 단조강이 필수적이지만, 저압이며 부식성이 높은 아민 유닛에는 복합재 본체가 사용되고 있습니다. 확실한 원자재 식별과 제철소 검사 보고서 제출이 의무화되어 있으며, 이로 인해 관리 비용이 증가하므로 통합된 야금 실험실을 갖춘 기존 공급업체에게 유리하게 작용하고 있습니다.

지역별 분석

아시아태평양은 중국의 파이프라인 및 송전망 통합과 인도의 도시 가스망 확충을 주축으로, 2025년 매출의 41.09%를 차지했습니다. National Pipeline Network Company는 48인치 간선 파이프라인을 부설하고 있으며, 이로 인해 2상강 버터플라이 밸브에 대한 수요가 증가하고 있습니다. 한편, 인도의 규제 당국은 API 6D 준수를 의무화하고 있어, 규격 미달 수입품은 시장에서 배제되고 있습니다. 일본과 한국은 수소 시범 사업을 추진하고 있으며, 이로 인해 니켈 합금 트림에 대한 틈새 수요가 창출되고 있습니다. 동남아시아의 LNG 수입 터미널은 재기화 능력을 확대하고 있지만, 자금 조달의 장벽으로 인해 진전이 더딘 임베디드니다.

중동은 2031년까지 연평균 성장률(CAGR) 4.76%를 나타낼 것으로 전망됩니다. 카타르 에너지의 노스 필드 확장 프로젝트에서는 영하 196℃를 견딜 수 있는 수천 개의 극저온용 밸브가 지정되어 있으며, 사우디아라비아의 자프라 타이트 가스 개발 프로젝트에서는 황화수소에 내성이 있는 2상강 트림이 요구되고 있습니다. ADNOC의 해수 주입 네트워크에서는 고염분 유체에 대응할 수 있는 내식성 체크 밸브가 요구되고 있습니다. 지역 국영 석유 회사의 자금 지원 덕분에 이 프로젝트는 원유 가격 변동으로부터 보호받고 있으며, 예측 가능한 수주 흐름이 유지되고 있습니다.

북미에서는 멕시코만 연안의 LNG 수출 플랜트와 퍼미안 분지에서 뻗어 나가는 수송 파이프라인이 주목을 받고 있습니다. 미국은 2025년까지 연간 800억 m³의 액화 능력을 승인했으며, 이에 따라 대구경 차단밸브에 대한 수요가 증가하고 있습니다. 한편, 노후화된 멕시코만 플랫폼의 폐쇄에 따라 해저용 차단밸브의 개보수 수요도 지속되고 있습니다. 유럽 시장은 탄화수소 생산량 감소에 따라 축소 추세를 보이고 있지만, 고압 CO2 밸브가 필요한 수소 혼합 가스 및 탄소 포집 프로젝트로 사업 중심을 옮기고 있습니다. 남미는 브라질의 프레솔트층과 아르헨티나의 바카 무에르타 인프라에 의존하고 있으며, 아프리카의 성장은 나이지리아의 가스 수익화와 모잠비크 LNG에 달려 있지만, 정치적 리스크로 인해 그 기세가 주춤하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the valves market in oil and gas industry size is expected to grow from USD 13.04 billion in 2025 to USD 13.43 billion in 2026 and is forecast to reach USD 15.93 billion by 2031, advancing at a 3.47% CAGR.

This report is Segmented by Valve Type (Ball Valve, Gate Valve, Globe Valve, and More), Material (Cast Steel, Forged Steel, Stainless Steel, and More), Application (Upstream, Midstream, and More), Actuation Type (Manual, Pneumatic, and More), Size (Less Than 6 Inch, 6 To12 Inch, 12 To 24 Inch, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Valves Market In Oil And Gas Industry

Growing Upstream And Midstream Pipeline Projects

Upstream spending rebounded to USD 570 billion in 2025 despite a 4% year-over-year dip, and analysts see an upswing to USD 738 billion by 2030. Deepwater programs in Brazil and unconventional gas in Saudi Arabia are locking in multi-year contracts for high-pressure gate and ball valves rated for sour service.Midstream growth is similar, as Enbridge approved a USD 1.4 billion gas line in 2024 while ADNOC funded a USD 2.4 billion seawater-injection network that requires corrosion-resistant check valves. China's national grid is adding 48-inch trunk lines, boosting demand for valves above 24 inches. Compliance with API 6D and ISO 15848 is now standard procurement language.

Surge In LNG Terminal Constructions

Roughly 300 billion m3 per year of new liquefaction capacity is scheduled for completion by 2030, led by 80 billion m3 sanctioned in the United States during 2025. QatarEnergy's USD 30 billion North Field expansion raises capacity to 126 million tpa and needs thousands of cryogenic ball and triple-offset butterfly valves engineered for -196 °C duty. Import terminals across India, Vietnam, and the Philippines prefer suppliers with local inventory and API 6FA fire-testing certification from Baker Hughes. Alloy and duplex steels, growing at a 4.72% CAGR, counter thermal-cycling damage inherent in LNG service. Local after-sales clauses in EPC contracts raise barriers for distant vendors.

Crude Oil Price Volatility Dampening CAPEX

Brent fluctuated between USD 70 and USD 90 per barrel in 2024-2025, stalling final investment decisions and trimming valve orders for marginal projects. Upstream spending slipped 4% year over year to USD 570 billion in 2025, as shale operators favored free cash flow over growth. Permian producers deferred tie-ins, softening demand for wellhead valves, while North Sea and Gulf of Mexico assets leaned toward decommissioning rather than costly subsea replacements. Downturns shrink order books faster than recoveries expand them because operators hesitate to carry spare inventory. Suppliers thus face cyclic revenue swings that complicate production planning.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Adoption Of Digital And Smart Valves

- Stringent Global Safety And Emission Regulations

- Intensifying Shift Toward Renewable Energy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Control valves, aided by digital twins, are expected to advance at a 5.12% CAGR, outpacing the overall valves market in oil and gas industry. Ball valves retained a 33.53% share in 2025 for on-off isolation, while gate valves dominate in high-pressure drilling and subsea trees. Plug and butterfly valves carve out niches in abrasive slurries and large-diameter low-pressure lines. The oil and gas industry's control valve market is projected to expand as predictive analytics sharpen throughput optimization.

Predictive maintenance keeps control-valve uptime high, compelling operators to specify ISO 15848 fugitive-emission ratings alongside API 607 fire testing. Electric actuation improves throttling accuracy, reinforcing the growth of control valves. Competitive entry barriers rise with each new standard, safeguarding incumbents that boast global test facilities and digital-service suites.

Cast steel held a 27.31% share in 2025, but alloy and duplex steels are forecast to grow 4.72% annually as sour-gas and hydrogen blends require enhanced corrosion resistance. Duplex grades now line Qatar's expanded North Field process trains, while nickel alloys equip Emerson's HV-7000 hydrogen regulator. The oil and gas industry's alloy steel valve market share is set to increase as NACE MR0175 compliance becomes routine.

Forged steel remains vital for 10,000 psi wellheads, whereas composite bodies are used for low-pressure, highly corrosive amine units. Positive material identification and mill test reports are mandatory, adding administrative cost that favors established suppliers with integrated metallurgy labs.

Geography Analysis

Asia-Pacific generated 41.09% of 2025 revenue, anchored by China's pipeline-grid integration and India's city-gas buildout. National Pipeline Network Company deploys 48-inch mains, raising the need for duplex-steel butterfly valves, while India's regulator demands API 6D compliance, shutting out low-spec imports. Japan and South Korea pursue hydrogen pilots, creating niche orders for nickel-alloy trim. Southeast Asian LNG import terminals are adding regas capacity but advancing slowly due to financing hurdles.

The Middle East is projected to have a 4.76% CAGR to 2031. QatarEnergy's North Field expansion specifies thousands of cryogenic valves engineered for minus 196 °C, and Saudi Arabia's Jafurah tight-gas development calls for hydrogen-sulfide-resistant duplex-steel trim. ADNOC's seawater-injection network demands corrosion-proof check valves for high-salinity fluids. Regional national-oil-company funding shields projects from crude swings, sustaining predictable order flows.

North America focuses on LNG export trains along the Gulf Coast and takeaway pipelines leaving the Permian Basin. The United States sanctioned 80 billion m3 per year of liquefaction capacity in 2025, triggering demand for large-diameter isolation valves. Meanwhile, the decommissioning of aging Gulf of Mexico platforms sustains retrofit activity for subsea isolation valves. Europe's market contracts amid declining hydrocarbon volumes, yet pivots to hydrogen blends and carbon-capture projects that require high-pressure CO2 valves. South America depends on Brazil's pre-salt fields and Argentina's Vaca Muerta infrastructure, while Africa's growth hinges on Nigerian gas monetization and Mozambique LNG, tempered by political risk.

- Emerson Electric Co.

- Flowserve Corporation

- Schlumberger N.V.

- Baker Hughes Company

- Rotork plc

- Alfa Laval AB

- Crane Co.

- Metso Corporation

- KITZ Corporation

- IMI plc

- Samson AG

- Valmet Oyj

- Velan Inc.

- Honeywell International Inc.

- Parker Hannifin Corporation

- AVK Holding A/S

- CIRCOR International, Inc.

- The Weir Group plc

- Pentair plc

- Neway Valve (Suzhou) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Upstream and Midstream Pipeline Projects

- 4.2.2 Accelerating Adoption of Digital and Smart Valves

- 4.2.3 Stringent Global Safety and Emission Regulations

- 4.2.4 Surge in LNG Terminal Constructions

- 4.2.5 Hydrogen-Ready Valve Designs for Energy Transition

- 4.2.6 Aging Offshore Assets Requiring Valve Retrofits

- 4.3 Market Restraints

- 4.3.1 Crude Oil Price Volatility Dampening CAPEX

- 4.3.2 Intensifying Shift Toward Renewable Energy

- 4.3.3 Alloy and Stainless-Steel Cost Spikes from Trade Tariffs

- 4.3.4 Rising Cybersecurity Risks in Connected Valve Networks

- 4.4 Industry Value, Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Valve Type

- 5.1.1 Ball Valve

- 5.1.2 Gate Valve

- 5.1.3 Globe Valve

- 5.1.4 Butterfly Valve

- 5.1.5 Check Valve

- 5.1.6 Plug Valve

- 5.1.7 Control Valve

- 5.2 By Material

- 5.2.1 Cast Steel

- 5.2.2 Forged Steel

- 5.2.3 Stainless Steel

- 5.2.4 Alloy and Duplex Steels

- 5.2.5 Non-Metallic, Composite

- 5.3 By Application

- 5.3.1 Upstream (Drilling, Wellhead, Artificial Lift)

- 5.3.2 Midstream (Pipelines, Terminals, Storage)

- 5.3.3 Downstream (Refining, Petrochemical)

- 5.3.4 Liquefied Natural Gas (LNG) Facilities

- 5.4 By Actuation Type

- 5.4.1 Manual

- 5.4.2 Pneumatic

- 5.4.3 Electric

- 5.4.4 Hydraulic, Electro-Hydraulic

- 5.5 By Size

- 5.5.1 Less than 6 inch

- 5.5.2 6 to 12 inch

- 5.5.3 12 to 24 inch

- 5.5.4 More than 24 inch

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Australia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Emerson Electric Co.

- 6.4.2 Flowserve Corporation

- 6.4.3 Schlumberger N.V.

- 6.4.4 Baker Hughes Company

- 6.4.5 Rotork plc

- 6.4.6 Alfa Laval AB

- 6.4.7 Crane Co.

- 6.4.8 Metso Corporation

- 6.4.9 KITZ Corporation

- 6.4.10 IMI plc

- 6.4.11 Samson AG

- 6.4.12 Valmet Oyj

- 6.4.13 Velan Inc.

- 6.4.14 Honeywell International Inc.

- 6.4.15 Parker Hannifin Corporation

- 6.4.16 AVK Holding A/S

- 6.4.17 CIRCOR International, Inc.

- 6.4.18 The Weir Group plc

- 6.4.19 Pentair plc

- 6.4.20 Neway Valve (Suzhou) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment