|

시장보고서

상품코드

2063387

DDoS 보호 및 완화 보안 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)DDOS Protection And Mitigation Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

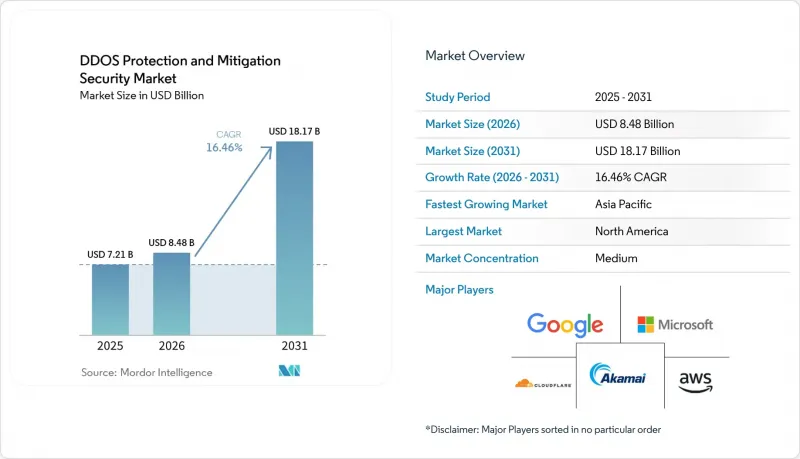

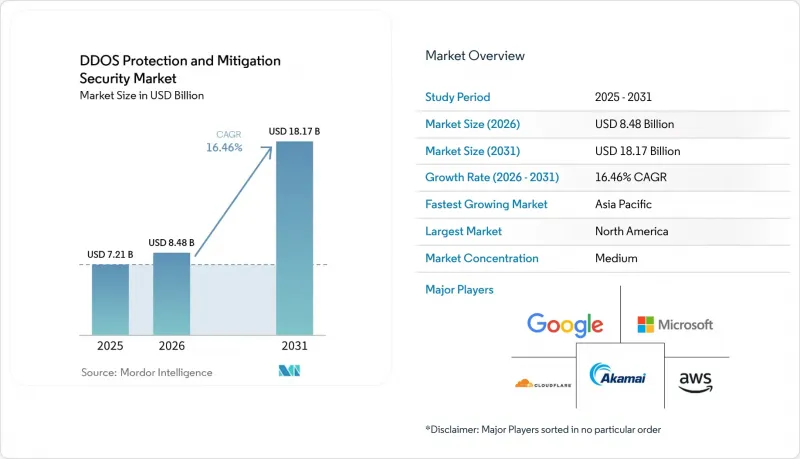

Mordor Intelligence에 의하면, DDoS 보호 및 완화 보안 시장 규모는 2025년에 72억 1,000만 달러로 평가되었습니다. 2026년에 84억 8,000만 달러에서 2031년까지 181억 7,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 16.46%로 성장할 것으로 전망됩니다.

본 보고서는 구성 요소(하드웨어, 소프트웨어, 서비스), 도입 형태(On-Premise, 클라우드), 조직 규모(중소기업, 대기업), 최종 사용자 산업(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 DDoS 보호 및 완화 보안 시장 동향 및 인사이트

고도화된 다중 벡터 공격의 급증

구글은 2024년 8월, 초당 3억 9,800만 건이라는 전례 없는 규모의 HTTP/2 래피드 리셋 요청을 처리했습니다. 이는 현대의 공격 캠페인이 대량 공격, 프로토콜 기반 공격, 용도 기반 공격 벡터를 어떻게 융합하고 있는지를 보여줍니다. 공격자들이 속도 제한을 우회하는 프로토콜의 특성을 악용하는 사례가 증가하고 있어, 조직들은 정적 시그니처에만 의존하는 대신 정상 트래픽을 프로파일링하는 행동 분석 기술을 도입할 수밖에 없는 상황에 처해 있습니다. 사건 1건당 평균 복구 비용이 250만 달러에 달했다는 사실은 2024년 기업의 보안 예산이 전년 대비 45% 증가한 이유를 여실히 보여줍니다. 공격이 네트워크, 용도, DNS 각 계층을 동시에 횡단하는 가운데, 구매자들은 전체 벡터에 걸친 통합적인 가시성을 우선시하고 있습니다. 이에 따라 DDoS 보호 및 완화 보안 시장에서는 독립형 어플라이언스보다 상호 연관된 텔레메트리 데이터를 제공하는 플랫폼이 선호되고 있습니다.

IoT와 엣지 디바이스의 보급

시스코는 2030년까지 293억 대의 연결 기기가 존재할 것으로 예측하고 있으며, 이들 각각이 봇넷의 잠재적 노드가 될 수 있습니다. 산업용 IoT의 도입으로 공격 대상 영역은 확대되고 있지만, 많은 운영 기술(OT) 네트워크에서는 여전히 인라인 완화 조치가 부족합니다. 엣지 워크로드는 기존 방식의 스크러빙을 복잡하게 만듭니다. 왜냐하면 트래픽을 멀리 떨어진 센터로 우회시키면, 산업 제어에 필수적인 10밀리초 이하의 지연 시간 요건을 충족할 수 없게 되기 때문입니다. 따라서 제조 기업들은 On-Premise 또는 하이브리드형 하드웨어를 도입하여 검사 기능을 기계 근처에 배치하는 한편, 트래픽 양의 급증에 대비해 클라우드 용량을 확보하고 있습니다. 5G 네트워크 슬라이스에서도 유사한 경향이 나타나며, 특정 서비스 계층을 겨냥한 표적형 공격에 대응하기 위해서는 엣지 환경에서 세밀한 대책을 적용하는 것이 필수적입니다.

고도 완화 솔루션의 높은 비용

연간 5만 달러에서 50만 달러 규모의 계약이 필요한 엔터프라이즈급 플랫폼은 많은 중소기업에게 가격이 너무 비쌉니다. 교육 및 튜닝 비용을 더하면 총 소유 비용이 두 배로 늘어나, 예산에 제약이 있는 기업들은 방화벽에만 의존하는 부분적인 대책으로 내몰리고 있습니다. 벤더는 종량제 요금제로 대응하고 있지만, 간소화된 서비스와 AI 기능이 풍부하게 탑재된 프리미엄 번들 사이에는 여전히 기능적인 격차가 존재합니다. 그 결과 발생한 양극화로 인해, DDoS 보호 및 완화 보안 시장은 위협에 대한 노출 정도가 아니라 지출 능력에 따라 양분되어 있습니다.

부문별 분석

2024년, DDoS 보호 및 완화 보안 시장 점유율의 46.33%를 해당 서비스가 차지했으며, 기술 인력 부족으로 인해 아웃소싱을 선택할 수밖에 없는 실정이 드러났습니다. 관리형 서비스 제공업체는 연중무휴 24시간 모니터링 및 사고 대응 서비스를 제공하고 있으며, 조직의 78%는 이를 사내에서 유지하기 어렵다고 느끼고 있습니다. 그러나 DDoS 보호 및 완화 보안 시장에서 소프트웨어에 할당되는 비중은 가장 빠르게 증가하고 있으며, AI 탑재 플랫폼은 2031년까지 연평균 성장률(CAGR) 18.16%를 나타낼 것으로 예측됩니다. 적응형 알고리즘은 공격 패턴을 실시간으로 학습하고 완화 임계값을 자동으로 재조정하지만, 이는 하드웨어 어플라이언스만으로는 구현할 수 없는 기능입니다. 그럼에도 불구하고, 결정론적 지연이 최우선으로 고려되는 고빈도 거래 등, 마이크로초 단위의 응답이 요구되는 분야에서는 하드웨어가 여전히 필수적입니다. 이에 따라, 고객이 관리하는 전략 엔진을 중심으로 전문적인 운영 관리를 제공하는 ‘서비스+소프트웨어’ 형태의 하이브리드 패키지가 등장하고 있습니다. 이러한 조합을 통해 고객은 관리 권한을 유지하면서 24시간 365일 운영을 전문 인력에게 위임할 수 있게 됩니다.

하드웨어 공급업체들은 클라우드 스크러빙 풀과 직접 통합되는 어플라이언스에 가속기 및 텔레메트리 피드를 탑재함으로써, 이익률 하락 압력에 대응하고 있습니다. Cloudflare의 Magic Transit은 피크 시간대의 이벤트에서 초당 3,200만 건의 HTTP 요청을 처리하며, 클라우드 큐잉이 On-Premise 패킷 필터링을 어떻게 보완하는지 보여줍니다. 규제 감사에서 종단 간 추적 가능성이 요구되는 가운데, 서비스, 소프트웨어, 하드웨어 등 각 요소 전반에 걸친 트래픽을 로그로 기록하는 통합 솔루션이 조달 과정에서 우선적으로 고려되고 있습니다. 그 결과, 통합된 대시보드를 통해 관리되는 경우가 늘어나고 있는 생태계에서 서비스는 수익의 기반, 소프트웨어는 성장의 원동력, 하드웨어는 지연 시간 대응 수단으로서의 역할을 계속해서 수행하고 있습니다.

2024년 매출의 63.21%를 클라우드 도입이 차지했으며, 이는 구매자들이 유연한 경제성을 선호하는 경향을 반영했습니다. 구매 비용, 감가상각비, 인건비를 고려할 때, 하이퍼스케일 클라우드의 볼륨 기반 완화 조치는 동등한 On-Premise 용량에 비해 60-70% 저렴한 비용으로 이용할 수 있습니다. AWS Shield Advanced는 용량 계획 수립 없이도 테라비트급 트래픽 급증을 흡수할 수 있도록 자동 스케일링을 수행함으로써 유틸리티 모델의 유효성을 입증하고 있습니다. DDoS 보호 및 완화 보안 시장 규모에는 특히 결제 처리 및 산업 자동화 분야에서 데이터 주권이나 1밀리초 미만의 지연 시간이 현지 검사를 필요로 하는 틈새 영역이 포함되어 있습니다.

그 결과, 하이브리드 방식이 주류를 이루고 있습니다. 대기업의 3분의 2는 클라우드 대역폭과 On-Premise 인텔리전스를 융합하여, 용도 계층에서의 필터링이 오리진 서버에 가장 가까운 곳에서 수행되도록 하고 있습니다. 엣지 컴퓨팅으로 인해 트래픽이 클라우드, 코어, 엣지를 가로지르게 되면서, 분산형 전략의 일관성에 대한 요구가 높아지고 있습니다. 따라서, 신규 도입을 놓고 경쟁하는 벤더들은 “한 번 감지하면 모든 곳에 적용”할 수 있도록 하는 중앙 집중식으로 오케스트레이션된 플랫폼을 제공해야 합니다. 5G의 확산에 따라 엣지 노드의 수가 증가함에 따라, 아키텍처 구성은 로컬 적용을 기반으로 한 클라우드 버스트를 더욱 중시하는 방향으로 전환되고 있습니다.

지역별 분석

북미는 2025년, 연간 180억 달러를 넘는 안정적인 연방 정부 지출에 힘입어 전 세계 매출의 39.61%를 차지했습니다. 실리콘밸리에 모여 있는 주요 클라우드 벤더와 스타트업들은 제품 주기를 단축하여, 현지 구매자들이 새로운 기능을 조기에 테스트하고 도입할 수 있도록 하고 있습니다. 캐나다 역시 비슷한 수준의 성숙도를 보이고 있으며, 미국의 제로 트러스트 프레임워크와 부합하는 중요 인프라 지침에 힘입어 발전하고 있습니다.

아시아태평양은 가장 빠른 성장세를 보이고 있으며, 이 지역의 DDoS 보호 및 완화 보안 시장 규모는 2031년까지 연평균 성장률(CAGR) 17.93%로 성장할 것으로 전망됩니다. 중국의 사이버 보안법은 데이터의 현지 보관을 의무화하고 있으며, 국내 스크리닝 센터와 국제적인 백본 용량을 결합한 하이브리드 방식의 도입이 촉진되고 있습니다. 인도의 ‘디지털 인디아’ 이니셔티브에 따라, 2024년 연방 정부의 사이버 보안 관련 지출은 34% 증가했습니다. 이는 경계 방어에서 적극적인 회복탄력성으로의 정책 전환을 반영하고 있습니다. 일본은 제조업의 가동 시간과 스마트 팩토리의 지속성을 최우선으로 하고 있어, 저지연 하드웨어 주변기기 분야에서 큰 비즈니스 기회가 창출되고 있습니다.

유럽의 NIS2 지침은 중요 인프라 전반의 복원력 확보를 위해 2024년 10월을 기한으로 정했습니다. 그 결과, 사업자들이 인증을 완료하고 EU 역내에 거점을 둔 스크리닝 노드를 찾게 될 것으로 예상에 따라, 조달 주기는 2024-2025년에 집중될 것으로 보입니다. 북유럽 국가들은 클라우드 도입을 주도하고 있지만, 독일은 엄격한 데이터 보호법을 준수하기 위해 하이브리드 아키텍처를 선호하고 있습니다. 중동 및 아프리카에서는 스마트시티 메가 프로젝트와 국영 석유 회사의 디지털화를 원동력으로 성장의 조짐이 보이지만, 인력 부족이 보급을 저해하고 있습니다. 남미에서는 은행 규제 강화에 따라 도입이 점차 확대되고 있지만, 통화 변동성으로 인해 설비 투자가 연기될 가능성이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the dDoS protection and mitigation security market size is projected to be USD 7.21 billion in 2025, USD 8.48 billion in 2026, and reach USD 18.17 billion by 2031, growing at a CAGR of 16.46% from 2026 to 2031.

This report is Segmented by Component (Hardware, and Software, Services), Deployment Mode (On-Premises, and Cloud), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global DDOS Protection And Mitigation Security Market Trends and Insights

Surge in Sophisticated Multi-Vector Attacks

Google mitigated an unprecedented 398 million HTTP/2 rapid-reset requests per second in August 2024, demonstrating how modern campaigns blend volumetric, protocol, and application vectors. Attackers are increasingly exploiting protocol quirks that bypass rate-limiting, compelling organizations to adopt behavioral analytics that profile legitimate traffic instead of relying solely on static signatures. Recorded average remediation costs of USD 2.5 million per incident underscore why enterprise security budgets increased by 45% year-over-year in 2024. As attacks traverse network, application, and DNS layers simultaneously, buyers prioritize unified visibility across vectors. Accordingly, the DDoS protection and mitigation security market favors platforms supplying correlated telemetry rather than standalone appliances.

Proliferation of IoT and Edge Devices

Cisco projects 29.3 billion connected devices by 2030, each of which could be a potential node in a botnet. Industrial IoT rollouts magnify attack surfaces, yet many operational technology networks still lack inline mitigation. Edge workloads complicate legacy scrubbing, because detouring traffic to distant centers breaches the sub-10 millisecond latency envelope critical for industrial control. Manufacturing companies, therefore, procure on-premises or hybrid hardware, keeping inspection proximate to machines while reserving cloud capacity for volumetric overflow. The same dynamic arises in 5G network slices, where targeted assaults on specific service tiers necessitate fine-grained policy enforcement at the edge.

High Cost of Advanced Mitigation Solutions

Enterprise-grade platforms, which require annual commitments of USD 50,000 to USD 500,000, price out many SMEs. The total cost of ownership doubles once training and tuning are added, nudging budget-constrained firms toward partial coverage that relies on firewalls alone. While vendors respond with pay-as-you-go tiers, functional gaps persist between simplified offerings and AI-rich premium bundles. The resulting bifurcation segments the DDoS protection and mitigation security market around spending power rather than threat exposure.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Cloud-Based Services

- Mandates for Zero-Trust Architecture

- Limited Awareness Among SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services captured 46.33% of the DDoS protection and mitigation security market share in 2024, emphasizing how skill shortages compel outsourcing. Managed service providers supply 24/7 monitoring and incident response that 78% of organizations find difficult to sustain in-house. The DDoS protection and mitigation security market size allocation toward software, however, is rising fastest, with AI-enabled platforms forecast to grow at an 18.16% CAGR through 2031. Adaptive algorithms learn attack patterns in real time, automatically retuning mitigation thresholds, a feature that hardware appliances alone cannot emulate. Yet hardware remains vital for microsecond-sensitive sectors such as high-frequency trading, where deterministic latency is paramount. Hybrid service-plus-software bundles therefore emerge, offering managed expertise around customer-controlled policy engines. This combination allows clients to maintain oversight while delegating 24/7 operations to specialized personnel.

Hardware vendors address margin pressure by embedding accelerators and telemetry feeds into appliances that integrate directly with cloud scrubbing pools. Cloudflare's Magic Transit processed 32 million HTTP requests per second during peak events, evidencing how cloud queuing complements on-premises packet filtering. As regulatory audits demand end-to-end traceability, integrated solutions that log traffic across services, software, and hardware elements gain procurement preference. Consequently, services remain the revenue anchor, software the growth engine, and hardware the latency hedge in an ecosystem increasingly orchestrated from unified dashboards.

Cloud deployments accounted for 63.21% of 2024 revenue, reflecting buyers' preference for elastic economics. Volumetric mitigation in hyperscale clouds costs 60-70% less than comparable on-premises capacity when factoring in purchase, depreciation, and staffing. AWS Shield Advanced auto-scales to absorb terabit-class floods with no capacity planning, validating the utility model. Nevertheless, the DDoS protection and mitigation security market size encompasses niches where data sovereignty and sub-millisecond latency necessitate local inspection, particularly in payment clearing or industrial automation.

Hybrid patterns consequently prevail. Two-thirds of large enterprises blend cloud bandwidth with on-premises intelligence, ensuring that application-layer filtering remains closest to the origin servers. Edge computing amplifies the need for distributed policy coherence because traffic now traverses cloud, core, and edge. Vendors competing for new deployments must therefore supply centrally orchestrated platforms that detect once and enforce everywhere. As 5G rollouts increase the number of edge nodes, the architecture mix further favors cloud bursting backed by local enforcement.

Geography Analysis

North America retained 39.61% of global revenue in 2025, anchored by consistent federal spending that tops USD 18 billion annually. Large cloud vendors and start-ups clustered in Silicon Valley accelerate product cycles, allowing local buyers to pilot emerging features early. Canada reflects a similar level of maturity, bolstered by critical infrastructure guidelines that align with U.S. zero-trust frameworks.

The Asia-Pacific region registers the swiftest expansion, with the DDoS protection and mitigation security market size in the region projected to grow at a 17.93% CAGR through 2031. China's Cybersecurity Law requires localized data residency, prompting hybrid deployments that blend domestic scrubbing centers with international backbone capacity. India's Digital India initiative raised federal cyber outlays 34% in 2024, reflecting a policy pivot from perimeter defense toward proactive resilience. Japan prioritizes manufacturing uptime and smart-factory continuity, creating sizable opportunities for low-latency hardware adjuncts.

Europe's NIS2 directive imposes October 2024 deadlines for resilience across critical infrastructure. Procurement cycles are consequently expected to concentrate in 2024-2025 as operators seek certified, EU-domiciled scrubbing nodes. Nordic countries lead in cloud adoption, while Germany favors hybrid architectures to satisfy strict data-protection statutes. The Middle East and Africa show nascent growth driven by smart-city megaprojects and national oil company digitization, but face skills shortages that slow penetration. South America gradually scales adoption as banking regulation tightens, yet currency volatility can defer capital spending.

- Cloudflare Inc.

- Akamai Technologies Inc.

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC

- Imperva Inc.

- Radware Ltd.

- Netscout Systems Inc.

- Verisign Inc.

- Neustar Security Services Inc.

- Arbor Networks Inc.

- F5 Inc.

- Corero Network Security plc

- Link11 GmbH

- StackPath LLC

- Nexusguard Ltd.

- CenturyLink Communications LLC (Lumen Technologies)

- Fastly Inc.

- Limelight Networks Inc. (Edgio Inc.)

- NSFOCUS Technologies Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Sophisticated Multi-Vector Attacks

- 4.2.2 Proliferation of IoT and Edge Devices

- 4.2.3 Rapid Adoption of Cloud-Based Services

- 4.2.4 Mandates for Zero-Trust Architecture

- 4.2.5 Growing Availability of DDoS-for-Hire Services

- 4.2.6 Integration of AI for Real-Time Mitigation

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Mitigation Solutions

- 4.3.2 Limited Awareness Among SMEs

- 4.3.3 False Positive Concerns in Automated Defenses

- 4.3.4 Evolving Encryption Standards Hindering Traffic Inspection

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Government

- 5.4.4 E-Commerce and Retail

- 5.4.5 Healthcare

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cloudflare Inc.

- 6.4.2 Akamai Technologies Inc.

- 6.4.3 Amazon Web Services Inc.

- 6.4.4 Microsoft Corporation

- 6.4.5 Google LLC

- 6.4.6 Imperva Inc.

- 6.4.7 Radware Ltd.

- 6.4.8 Netscout Systems Inc.

- 6.4.9 Verisign Inc.

- 6.4.10 Neustar Security Services Inc.

- 6.4.11 Arbor Networks Inc.

- 6.4.12 F5 Inc.

- 6.4.13 Corero Network Security plc

- 6.4.14 Link11 GmbH

- 6.4.15 StackPath LLC

- 6.4.16 Nexusguard Ltd.

- 6.4.17 CenturyLink Communications LLC (Lumen Technologies)

- 6.4.18 Fastly Inc.

- 6.4.19 Limelight Networks Inc. (Edgio Inc.)

- 6.4.20 NSFOCUS Technologies Group Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment