|

시장보고서

상품코드

2063388

생물제제 위탁연구기관(CRO) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Biologics Contract Research Organization (CRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

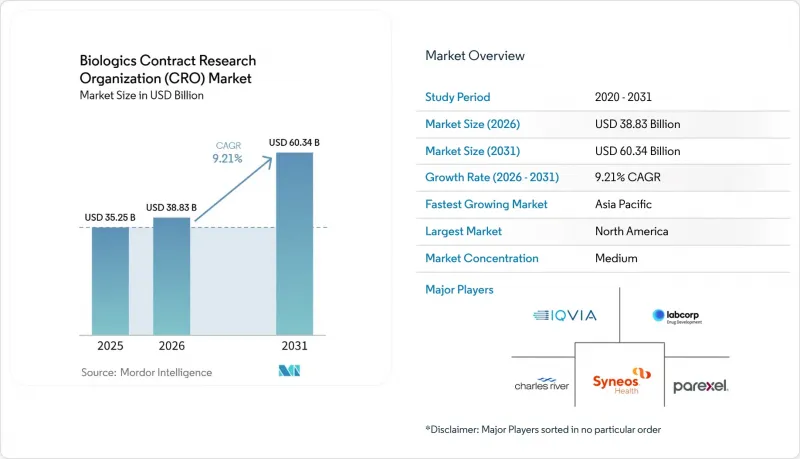

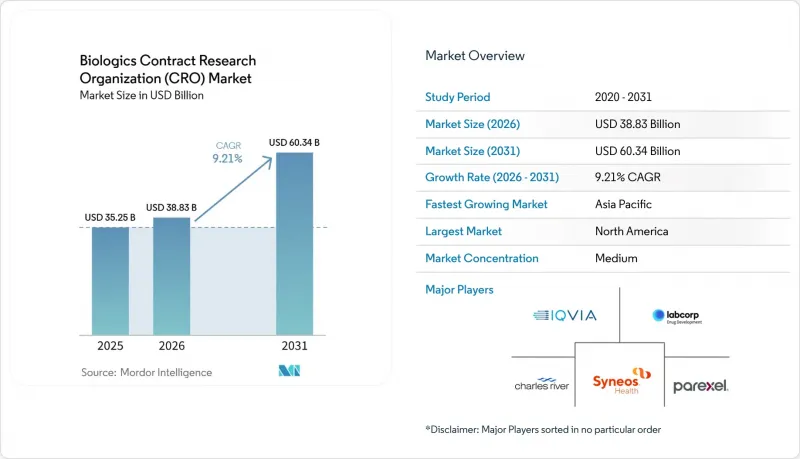

Mordor Intelligence에 의하면, 생물제제 위탁연구기관(CRO) 시장 규모는 2025년 352억 5,000만 달러로 평가되었습니다. 2026년에는 388억 3,000만 달러로 확대되어 2031년까지 603억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 9.21%로 성장할 전망입니다.

본 보고서는 서비스 유형(전임상·분석 서비스, 임상 검사 서비스, 기타), 단계(전임상, 1상, 기타), 치료 분야(종양학, 면역학·염증, 기타), 최종 사용자(바이오의약품·바이오기술 기업, 기타), 지역(북미, 유럽, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 생물제제 위탁연구기관(CRO) 시장 동향 및 인사이트

신규 바이오의약품 및 바이오시밀러의 도입 급증

FDA는 2024년부터 2025년에 걸쳐 16종의 바이오시밀러를 승인했습니다. 여기에는 상호 교환 가능한 아달리무맙과 우스테키누맙의 바이오시밀러가 포함되어 있으며, 이 두 약물의 합계는 약 200억 달러 규모의 원개발 의약품 매출에 해당합니다. 후원 기업은 비교 분석을 외부에 위탁하고 있습니다. 이는 사내 연구실에는 일반적으로 검증된 고성능 분석법이 부족하기 때문입니다. 따라서 생물제제 위탁연구기관(CRO) 시장에서는 전체 매출보다 전임상 및 분석 서비스 부문에서 더 강력한 성장세가 나타나고 있습니다. 유로핀스와 SGS는 이러한 수요 급증에 대응하기 위해 2024년 이후 각각 15대 이상의 LC-MS 장비를 추가로 도입했습니다. 상호 교환성 시험에는 여러 약물을 교차시키는 크로스오버 시험 설계가 필요하지만, 이를 프로토콜 편차 없이 수행할 수 있는 것은 경험이 풍부한 CRO뿐이며, 이로 인해 실적이 입증된 제공업체의 전략적 가치가 높아지고 있습니다.

생체 분자의 복잡성이 증가함에 따라 전문적인 분석이 필수적

이중 특이성 항체, ADC, 융합 단백질의 경우, 직교적 특성 평가, 수소-중수소 교환, 분석용 초원심분리, 저온 전자현미경(cryo-EM)이 필요하지만, 이러한 분석은 대부분 사내 품질 관리 예산 범위를 초과합니다. 2024년에 발표된 FDA 지침에서는 다중 특이성 융합 단백질의 로트 간 일관성을 확인하기 위해, 신청자에게 최소 5가지의 분석 방법을 사용할 것을 요구하고 있습니다. 찰스 리버(Charles River)는 2025년, 극저온 전자현미경(cryo-EM) 및 HDX-MS의 역량 확충을 위해 8,000만 달러를 투자하며, 생물제제 위탁연구기관(CRO) 시장에서의 리더십을 강화했습니다. 당사슬 프로파일링은 IND 신청 승인 여부를 결정하는 주요 요인으로 부상하고 있으며, 많은 의뢰사가 검증된 LC-MS 워크플로우를 갖춘 실험실에 당사슬 매핑을 외주화하고 있습니다.

분산형 바이오 검사에서 사이버 보안 및 데이터 무결성에 대한 위험

CRO의 임상시험 데이터베이스를 표적으로 한 랜섬웨어 공격은 2024년에 42% 급증하여, FDA의 경고장 발부와 사이버 보험료 인상을 초래했습니다. 제로 트러스트 아키텍처와 블록체인 감사 추적 시스템의 도입으로 인해 연간 IT 예산에 200만-500만 달러가 추가되어, 소규모 연구소에게는 큰 부담이 되고 있습니다.

부문별 분석

2025년, 바이오의약품 위탁 연구 기관(CRO) 시장의 매출의 75.23%를 임상 검사 서비스가 차지했습니다. 이는 피험자 등록, 전 세계 임상시험 기관에 대한 모니터링, 실시간 안전성 모니터링에 소요되는 막대한 비용을 반영한 것입니다. 스폰서는 일반적으로 단일 후기 단계 종양학 검사에 5,000만 달러 이상을 투자하는 것이 일반적이며, 이를 통해 임상 부문의 우위가 확고해지고 있습니다. 그러나 규제 당국이 바이오시밀러의 비교 평가 패키지에 대해 직교 분석, 1차 구조, 고차 구조, 당사슬 구조, 생물학적 활성을 요구하고 있기 때문에 전임상·분석 서비스 시장은 연평균 성장률(CAGR) 9.60%로 확대될 것으로 전망됩니다. 전임상 고객들은 법정 검사 및 면역원성 스크리닝에 대한 신속한 대응을 중요시하기 때문에 대규모 LC-MS 장비군과 검증된 ELISA 패널을 보유한 CRO는 높은 요금을 책정하고 있습니다. 품질 및 규제 컨설팅은 규모는 작지만 수익성이 높은 틈새 시장으로 자리 잡고 있으며, 최고 수준의 서비스 제공업체들은 CMC 신청 서류 작성이나 FDA에 대한 IND 신청 전 지원 서비스에 대해 시간당 300-500달러의 수수료를 청구하고 있습니다.

분산형 임상 검사가 보급됨에 따라 2세대 서비스 라인이 등장하고 있습니다. 라보코프의 2024년판 원격 모니터링 플랫폼은 참가자의 자택에서 사이토카인 측정값을 스트리밍으로 전송함으로써, 면역학 검사를 위한 시설 방문 횟수를 줄이는 동시에 피험자 모집을 신속하게 진행합니다. 찰스 리버사는 이중 특이성 항체와 CAR-T 프로그램을 주축으로, 2025년에 비인간 영장류를 이용한 독성 시험 수주가 25% 증가했습니다. 파렉셀의 규제 인텔리전스 포털은 전 세계 CMC 관련 과제를 실시간으로 파악하여, 신청 준비 기간을 3-6개월 단축합니다. 전반적으로, 생물제제 위탁연구기관(CRO) 시장은 정밀 분석, 데이터 시각화, 선제적인 규제 전략을 통해 임상 프로그램의 위험을 줄이기를 희망하는 의뢰사들로부터 혜택을 받고 있습니다.

2025년 수익의 75.10%는 임상시험 단계의 활동이 차지했으며, 3상 임상시험만 보더라도 광범위한 임상시험 기관 네트워크와 수년에 걸친 추적 조사를 통해 4,000만-8,000만 달러의 비용이 소요되는 경우가 많습니다. 적응형 퍼스트-인-휴먼 임상시험 설계로 인해, 특히 약력학적 바이오마커나 바스켓 임상시험 코호트가 포함되는 경우, 1상 임상시험의 데이터 양이 증가하고 비용도 급등하고 있습니다. Medpace의 2025년형 하이브리드 설계는 중앙 투여 클리닉과 재택 약물 동태 샘플링을 결합함으로써, 데이터 품질을 유지하면서 환자 1인당 비용을 30% 절감합니다. 한편, 비임상 프로젝트는 연평균 성장률(CAGR) 9.30%로 가속화되고 있는데, 이는 각 후원사가 IND 신청 전에 제형 최적화, 개발 가능성 스크리닝, 면역원성 위험 평가에 투자하고 있기 때문입니다.

또한, AI 도구가 인실리코(in silico)를 통해 응집성 및 점도와 관련된 과제를 파악할 수 있게 됨에 따라, 화학자들이 성공 확률이 높은 후보 화합물을 우선적으로 선정할 수 있게 되었고, 신약 개발 예산도 증가하고 있습니다. NIH는 2025년, 신약 개발과 전임상 독성 검사를 연결하는 대학 CRO 컨소시엄에 1억 2,000만 달러를 지원하여, 서비스 제공업체의 초기 단계 업무 파이프라인을 확대했습니다. 유전자 치료에 대한 시판 후 15년간의 장기 모니터링을 요구하는 규제상의 압력으로 인해, 4상 임상시험은 점점 더 중요한 수익원이 되고 있습니다. 전반적으로 모든 단계가 생물제제 위탁연구기관(CRO) 시장에 기여하고 있지만, 리스크를 중시하는 의뢰사는 비용이 많이 드는 후기 단계에서의 실패를 피하기 위해 초기 단계의 분석에 자금을 집중적으로 배분하고 있습니다.

지역별 분석

북미는 바이오의약품 기업 본사가 밀집해 있고, NIH(미국 국립보건원)로부터 막대한 자금을 지원받으며, 바이오시밀러 및 유전자 치료에 관한 지침 수립에서 FDA(미국 식품의약국)가 주도적인 역할을 한 덕분에 2025년 매출의 45.32%를 차지했습니다. 그럼에도 불구하고, 규제 합리화와 비용 측면에서의 우위가 중국, 인도, 일본, 한국의 투자자들을 끌어들이고 있는 만큼, 아시아태평양은 연평균 성장률(CAGR) 9.90%를 나타낼 것으로 전망됩니다. 중국 국가의약품감독관리국(NMPA)은 ICH Q5E를 도입한 후, 2024년부터 2025년에 걸쳐 27개의 바이오시밀러를 승인함으로써 국내 승인까지 소요되는 기간을 18개월 단축했습니다. 인도 의약품 규제 당국(CDSCO)의 저위험 분자에 대한 국내 임상시험 면제, 일본의 외삽 기준 통합, 한국의 12개월 신속 심사 제도는 이 지역의 매력을 한층 더 공고히 하고 있습니다.

유럽은 여전히 중요한 시장이며, 독일, 영국, 프랑스가 2025년 매출의 상당 부분을 차지했습니다. 독일 연방 교육연구부는 2025년에 중개생물학 분야에 8억 유로를 배정했으며, 이 자금은 주로 CRO가 관리하는 임상 네트워크를 통해 제공됩니다. 중동 및 아프리카와 남미는 규모는 작지만 성장세를 보이고 있으며, 브라질의 15개월 바이오시밀러 심사 같은 신속 승인 절차가 그 원동력이 되고 있습니다. 호주와 한국은 ICH 준수 및 연구개발 세액 공제의 혜택을 받고 있습니다. 캐나다와 멕시코는 국경을 넘는 시료 운송 절차를 간소화하는 USMCA(미국·멕시코·캐나다 협정)의 규정에 따라 혜택을 보고 있습니다. 남아프리카와 GCC는 환자 수가 많아 대규모 코호트 연구가 가능한 감염병 임상 검사를 유치하고 있으며, WHO가 지원하는 규제 역량 구축을 통해 미국 및 EU에 제출하는 데 사용되는 데이터의 이식성이 향상되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the biologics contract research organization market size is expected to increase from USD 35.25 billion in 2025 to USD 38.83 billion in 2026 and reach USD 60.34 billion by 2031, growing at a CAGR of 9.21% over 2026-2031.

This report is Segmented by Service Type (Pre-Clinical & Analytical Services, Clinical Trial Services and More), Phase (Pre-Clinical, Phase I, and More), Therapeutic Area (Oncology, Immunology & Inflammation, and More), End User (Biopharmaceutical & Biotech Firms, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Biologics Contract Research Organization (CRO) Market Trends and Insights

Surging Adoption of Novel Biologics & Biosimilars

The FDA cleared sixteen biosimilars across 2024 and 2025, including interchangeable adalimumab and ustekinumab versions that together replace reference sales of roughly USD 20 billion. Sponsors outsource comparability analytics because internal labs generally lack validated high-throughput assays, which is why the biologics contract research organization market posts stronger growth in Pre-clinical & Analytical Services than overall revenue. Eurofins and SGS have expanded LC-MS fleets by more than fifteen units each since 2024 to manage the influx . Interchangeability studies require multi-switch crossover designs that only experienced CROs can execute without protocol deviations, reinforcing the strategic value of seasoned providers.

Growing Complexity of Biomolecules Necessitating Specialized Analytics

Bispecific antibodies, ADCs, and fusion proteins demand orthogonal characterization hydrogen-deuterium exchange, analytical ultracentrifugation, and cryo-EM, which sits beyond most in-house quality-control budgets. FDA guidance issued in 2024 asks sponsors to use at least five analytic modalities to confirm lot-to-lot consistency for multispecific constructs. Charles River invested USD 80 million in 2025 for additional cryo-EM and HDX-MS capacity, reinforcing its leadership in the biologics contract research organization market. Glycosylation profiling has emerged as a gating factor for IND acceptance, pushing many sponsors to outsource glycan mapping to labs with validated LC-MS workflows.

Cyber-Security & Data-Integrity Risks in Distributed Biotesting

Ransomware incidents against CRO trial databases shot up 42 % in 2024, prompting FDA warning letters and higher cyber-insurance premiums. Implementation of zero-trust architectures and blockchain audit trails adds USD 2-5 million to annual IT budgets, costs that small labs struggle to absorb.

Other drivers and restraints analyzed in the detailed report include:

- Cost Pressure & Need for Faster Time-to-Market Encouraging Outsourcing

- Cell & Gene Therapy Pipeline Expansion Boosting Demand for Advanced Bio-Analytics

- Scarcity of High-End Biologics Expertise in Emerging Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical Trial Services generated 75.23 % of the biologics contract research organization market revenue in 2025, reflecting the sheer cost of patient enrollment, global site monitoring, and real-time safety oversight. Sponsors routinely spend USD 50 million or more on a single late-stage oncology trial, cementing the clinical category's dominance. However, Pre-clinical & Analytical Services are forecast to expand at 9.60 % CAGR as agencies demand orthogonal analytics, primary structure, higher-order structure, glycosylation, and bioactivity for biosimilar comparability packages. Pre-clinical clients value rapid turnaround on method validation and immunogenicity screening, so CROs with large LC-MS fleets and validated ELISA panels command premium fees. Quality & Regulatory Consulting remains a slim but profitable niche; top-tier providers bill USD 300-500 per hour for CMC dossier drafting and FDA pre-IND support.

Second-generation service lines are emerging as decentralized trials gain traction. Labcorp's 2024 remote-monitoring platform streams cytokine readouts from participants' homes, cutting site visits and speeding recruitment in immunology trials. Charles River booked a 25 % rise in non-human-primate toxicology studies in 2025, driven by bispecific and CAR-T programs. Parexel's Regulatory Intelligence portal flags global CMC gaps in real time, trimming submission readiness by three to six months. Altogether, the biologics contract research organization market benefits from sponsors eager to de-risk clinical programs through better analytics, data visualization, and proactive regulatory strategy.

Clinical Trial phase activities captured 75.10 % of 2025 revenue, with Phase III studies alone often costing USD 40-80 million due to extensive site networks and multi-year follow-up. Adaptive first-in-human designs are making Phase I work more data-rich and expensive, especially when pharmacodynamic biomarkers or basket-trial cohorts are involved. Medpace's 2025 hybrid design combines central infusion clinics with home pharmacokinetic sampling, trimming per-patient costs by 30 % while maintaining data quality. Meanwhile, Pre-clinical projects are accelerating at 9.30 % CAGR as sponsors invest in formulation optimization, developability screening, and immunogenicity risk assessment before filing an IND.

Discovery budgets also rise as AI tools flag aggregation or viscosity liabilities in silico, allowing chemists to prioritize high-probability candidates. NIH awarded USD 120 million in 2025 to university CRO consortia that bridge discovery and pre-clinical toxicology, feeding a pipeline of early-stage work to service providers. Regulatory pressure for long-term monitoring fifteen-year post-marketing follow-up for gene therapies, makes Phase IV an increasingly material revenue stream. Collectively, all stages contribute to the biologics contract research organization market, yet risk-conscious sponsors tilt funding toward early analytics to avoid costly late-phase failures.

Geography Analysis

North America captured 45.32 % of 2025 revenue thanks to a dense cluster of biopharma headquarters, high NIH funding, and FDA leadership in biosimilar and gene-therapy guidance. Nonetheless, the Asia-Pacific is projected to post a 9.90 % CAGR as streamlined regulations and cost arbitrage lure sponsors to China, India, Japan, and South Korea. China's NMPA green-lit 27 biosimilars across 2024-2025 after adopting ICH Q5E, shortening local timelines by eighteen months. India's CDSCO waiver of local trials for low-risk molecules, Japan's alignment of extrapolation, and South Korea's twelve-month fast-track review further solidify the region's appeal.

Europe remains vital, with Germany, the United Kingdom, and France combining for a significant share of 2025 turnover. Germany's Federal Ministry of Education and Research earmarked EUR 800 million in 2025 for translational biologics, often channeled through CRO-managed clinical networks. The Middle East & Africa and South America are smaller but growing, driven by fast-track pathways such as Brazil's fifteen-month biosimilar review. Australia and South Korea benefit from ICH alignment and R&D tax credits; Canada and Mexico gain from USMCA provisions that simplify cross-border sample flow. South Africa and GCC states attract infectious-disease trials where patient prevalence supports larger cohorts, and WHO-backed regulatory capacity building improves data portability to U.S. and EU submissions.

- Altasciences

- BioAgilytix Labs

- Charles River

- Eurofins

- Frontage Laboratories

- Genscript Biotech

- ICON

- IQVIA

- Jubilant Biosys

- KBI Biopharma

- LabCorp

- Lonza Bioscience Solutions

- Medpace Holdings

- Parexel International

- PPD (Thermo Fisher Scientific)

- Rentschler Biopharma

- Samsung Biologics CRO Services

- SGS

- Syneos Health

- WuXi App Tec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Novel Biologics & Biosimilars

- 4.2.2 Growing Complexity of Biomolecules Necessitating Specialized Analytics

- 4.2.3 Cost-Pressure & Need for Faster Time-To-Market, Encouraging Outsourcing

- 4.2.4 Cell & Gene Therapy Pipeline Expansion Boosting Demand for Advanced Bio-Analytics

- 4.2.5 AI/ML-Enabled In-Silico Biologics Design Services Offered by Cros

- 4.2.6 Regulatory Harmonization in APAC Facilitating Offshore Biologics Trials

- 4.3 Market Restraints

- 4.3.1 Stringent Global GMP/GLP Compliance Raising Operating Costs

- 4.3.2 Scarcity Of High-End Biologics Expertise in Emerging Regions

- 4.3.3 Shift Toward Integrated CDMO Models Cannibalizing Standalone CRO Revenue

- 4.3.4 Cyber-Security & Data-Integrity Risks in Distributed Biotesting

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of Substitutes

- 4.7.4 Threat of New Entrants

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Pre-clinical & Analytical Services

- 5.1.2 Clinical Trial Services

- 5.1.3 Quality & Regulatory Consulting

- 5.1.4 Bio-informatics & Data Management

- 5.2 By Phase

- 5.2.1 Pre-clinical

- 5.2.2 Phase I

- 5.2.3 Phase II

- 5.2.4 Phase III

- 5.2.5 Phase IV

- 5.3 By Therapeutic Area

- 5.3.1 Oncology

- 5.3.2 Immunology & Inflammation

- 5.3.3 Infectious Diseases

- 5.3.4 Rare Diseases

- 5.3.5 Others (Cardio-metabolic, Neurology)

- 5.4 By End User

- 5.4.1 Biopharmaceutical & Biotech Firms

- 5.4.2 Academic & Research Institutes

- 5.4.3 Government & Non-profit Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Altasciences

- 6.3.2 BioAgilytix Labs

- 6.3.3 Charles River Laboratories

- 6.3.4 Eurofins Scientific

- 6.3.5 Frontage Laboratories

- 6.3.6 Genscript Biotech

- 6.3.7 ICON plc

- 6.3.8 IQVIA

- 6.3.9 Jubilant Biosys

- 6.3.10 KBI Biopharma

- 6.3.11 Labcorp Drug Development

- 6.3.12 Lonza Bioscience Solutions

- 6.3.13 Medpace Holdings

- 6.3.14 Parexel International

- 6.3.15 PPD (Thermo Fisher Scientific)

- 6.3.16 Rentschler Biopharma

- 6.3.17 Samsung Biologics CRO Services

- 6.3.18 SGS SA

- 6.3.19 Syneos Health

- 6.3.20 WuXi AppTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment