|

시장보고서

상품코드

2063390

크레아티닌 측정 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Creatinine Measurement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

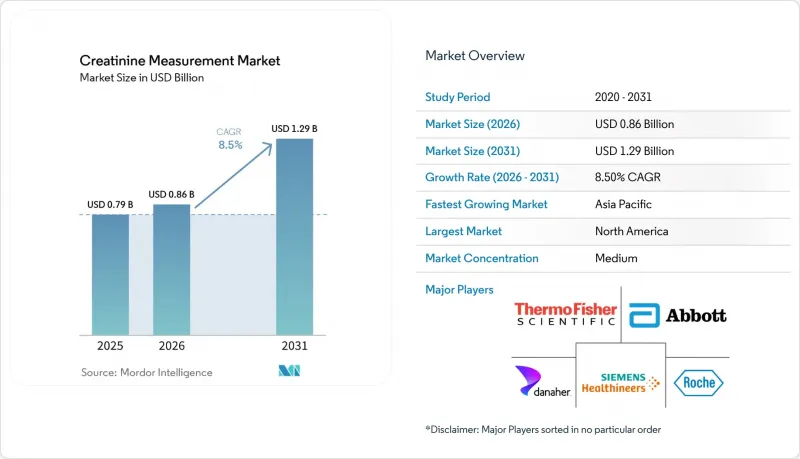

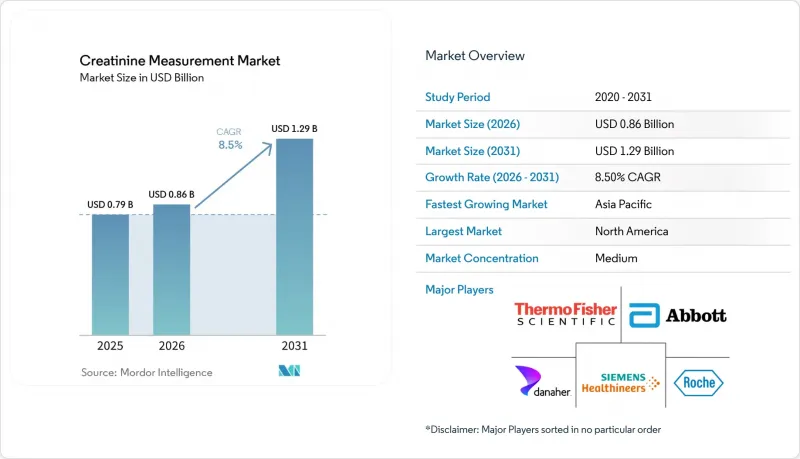

Mordor Intelligence에 의하면, 크레아티닌 측정 시장 규모는 2025년에 7억 9,000만 달러로 평가되었고, 2026년에 8억 6,000만 달러로 추정되고, 2031년까지 12억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 8.5%로 성장할 전망입니다.

본 보고서는 제품 유형별(시약 및 키트, 임상화학 분석기 등), 검사법별(자페법, 효소법), 검체 유형별(혈청 및 혈장, 전혈, 소변), 검사 환경별(중앙 검사실, 현장 검사), 최종 사용자별(병원 및 진료소, 진단실험실 등), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 크레아티닌 측정 시장 동향 및 분석

CKD(만성 신장 질환) 유병률 증가 및 선별 검사의 강화

미국에서는 3,500만 명 이상의 성인이 만성 신장 질환(CKD)을 앓고 있으며, 중국에서는 1억 3,200만 명의 국민이 신기능 저하를 겪고 있지만, 자신의 병세를 인지하고 있는 중국 환자는 고작 12.5%에 불과합니다. 현재 각국의 보건 당국은 크레아티닌 및 eGFR 검사를 1차 의료 프로토콜에 포함하고 있으며, 중국의 2024년판 지역 보건 지침에서는 휴대용 분석기를 활용한 대규모 선별 검사를 권고하고 있습니다. 일본의 투석 등록 데이터에 따르면, 2023년 환자 수는 34만 9,700명이며, 각 환자는 치료의 적정화를 도모하기 위해 매월 크레아티닌 검사를 받고 있습니다. 미국에서는 메디케어의 '성과 기반 인센티브 지급 제도(MIPS)'가 알부민/크레아티닌 비율 결과를 기록하는 의사에게 보상을 지급하고 있으며, 이로 인해 외래 검사 건수가 증가하고 있습니다. 이러한 프로그램들이 결합되어 검사실 및 현장 진단(POC) 채널 모두에 검체 유입이 활발해지면서 크레아티닌 측정 시장을 뒷받침하고 있습니다.

방사선과 및 중환자실에서 포인트 오브 케어 크레아티닌/eGFR 검사 도입

방사선과 및 중환자 치료팀은 크레아티닌 검사를 중앙 검사실에서 병상용 장비로 전환하여, 결과가 나오기까지 걸리는 시간을 몇 시간에서 몇 분으로 단축했습니다. 애보트의 i-STAT 카트리지는 65μL의 전혈로 2분 만에 결과를 도출하며, 2024년 퀸즐랜드주 중환자실 연구에서 중앙 검사실의 검사법과 상관관계 계수 R²=0.99를 나타냈습니다. 영국 국립의료기술평가원(NICE)은 조영제 투여 전 CT 검사 워크플로우에서 현장 진단용 크레아티닌 측정 장치를 권장하고 있으며, 응급 영상 진단 분야에서의 도입이 가속화되고 있습니다. 노바 바이오메디컬(Nova Biomedical)의 StatSensor는 손가락 끝에서 채혈한 후 30초 만에 기기에서 eGFR을 산출할 수 있어, 지역 약국이나 탄자니아의 자원이 제한된 HIV 진료소에서 활용이 확대되고 있습니다. 이러한 기능들은 신속한 의사결정을 통해 조영제 유발성 신증(CIN)을 예방하고, 환자의 진료 효율을 높여 크레아티닌 측정 시장의 가치 제안을 강화하고 있습니다.

자페법의 간섭 및 측정법 간 변동

빌리루빈이나 헤모글로빈에 의한 양의 간섭은 자페법의 측정값을 최대 20%까지 과대평가할 가능성이 있습니다. 반면, 항생제는 측정치를 낮춰 투약 오류의 위험을 초래할 우려가 있습니다. 2025년 『Annals of Laboratory Medicine』지에 실린 리뷰에서는 여러 기관의 결과를 집계하는 과정에서 4.6%의 LOINC 매핑 오류가 확인되었으며, 방법론의 불일치가 종단적 데이터의 신뢰성을 훼손할 가능성이 있다는 점이 부각되었습니다. 지멘스의 Atellica CH 크레아티닌 3 분석법은 레이트 블랭킹과 0.3 mg/dL의 바이어스 보정을 도입했으나, 효소법 시약과 비교할 때 비용 측면의 관성으로 인해 여전히 보급이 더딘 실정입니다. 이러한 과제들로 인해, 본래 호조를 보일 것으로 예상되었던 크레아티닌 측정 시장 전망은 주춤하고 있습니다.

부문별 분석

시약 및 키트는 2025년 매출의 42.55%를 차지했으며, 검사실이 다년간의 소모품 계약을 체결하고 있다는 점에서 크레아티닌 측정 시장 규모 내에서 가장 큰 점유율을 차지했습니다. 현장 진단 기기 및 휴대용 기기는 2분 이내에 결과를 보고해야 하는 영상 진단 프로토콜의 확산에 힘입어, 2031년까지 연평균 9.25%의 성장률을 보일 것으로 전망됩니다. 벡만 콜터(Beckman Coulter)사의 DxC 500i와 같은 임상화학 분석기는 시간당 800건의 검사를 수행하며, 핵심 검사실의 경쟁력을 유지하고 있습니다. 한편, 로슈사의 cobas c 703은 처리 능력을 두 배로 늘려 시간당 2,000건의 검사를 수행함으로써 시약 수요를 뒷받침하고 있습니다.

이 교정기 및 제어 장비는 매출 규모는 작지만, NIST SRM 967b에 대한 분석 추적성을 확보하고 있으며 CLIA의 품질 요건을 충족합니다. 로슈가 펜츠베르크에 건설 중인 6억 유로 규모의 시설에서는 항체 및 효소 생산을 자동화하여 전 세계 고객에 대한 공급 체계를 강화할 예정입니다. 지멘스는 e-connected Atellica 시스템에서 98%의 가동률을 보장함으로써 서비스 차별화를 꾀하고 있습니다. 신흥국 시장에서는 아시아산 제네릭 시약이 가격 압박을 가하고 있지만, 서비스 계약 번들 및 가동률 보장을 통해 다국적 기업들은 크레아티닌 측정 시장에서 경쟁력을 유지하고 있습니다.

2025년, 자페법은 확고한 분석 장비 도입 실적과 20-30%의 비용 우위를 바탕으로 크레아티닌 측정 시장 점유율의 54.53%를 차지했습니다. 검사실이 IDMS 기준과의 부합성을 높이고 간섭을 줄이도록 요구되는 가운데, 효소법을 이용한 측정법은 2031년까지 연평균 성장률(CAGR) 9.05%로 확대되고 있습니다. 크레아티닌 측정 업계는 규제 측면에서의 지원도 받고 있습니다. FDA의 투여량 지침은 의약품 라벨을 준수하는 데 있어 효소법을 사실상 권장하고 있습니다.

각 벤더사는 두 가지 전략을 동시에 추진하고 있습니다. 로슈와 벡만콜터는 자페법과 효소법 시약을 모두 갖추고 있어, 예산이 제한적인 검사실이 단계적으로 전환할 수 있도록 지원하고 있습니다. 지멘스의 개선된 Jaffe법은 기존 시스템의 수명을 연장하는 동시에 빌리루빈의 간섭을 줄이기 위한 레이트 블랭킹 기능을 제공합니다. 다기관 공동 연구 네트워크가 데이터의 조화를 요구하는 가운데, 효소법의 보급은 자페법의 우위를 서서히 잠식해 나가며 크레아티닌 측정 시장의 성장세를 더욱 가속화할 것입니다.

지역별 분석

북미는 2025년 매출의 41.15%를 차지했으며, 57만 1,000명의 투석 환자, ACR 검사에 대한 메디케어 인센티브, 그리고 eGFR 보고를 우선시하는 FDA 지침에 힘입고 있습니다. 캐나다는 응급실 대기 시간을 단축하기 위해 현장 진단 장비에 투자하고 있는 반면, 멕시코에서는 성장하는 민간 진단 부문이 중저가 분석 장비를 도입하고 있습니다.

유럽의 국민건강보험 제도와 IVDR 규제가 측정 방법의 표준화를 이끌고 있습니다. 영국의 NEQAS 데이터는 효소법이 Jaffe법보다 KDIGO의 편향 목표를 더 적절히 충족한다는 사실을 뒷받침하고 있으며, 이는 국민보건서비스(NHS)의 조달 정책을 형성하는 데 기여하고 있습니다. 로슈의 펜츠베르크 공장은 2028년까지 유럽 대륙의 시약 공급망을 강화할 전망입니다. 그러나 ESUR의 위험도 분류 프로토콜에 따라, 방사선과에서 시행되는 현장 검사 건수가 감소할 가능성이 있습니다.

아시아태평양은 연평균 성장률(CAGR) 9.51%를 나타낼 것으로 예측되며, 이는 각 지역 중 가장 높은 성장률입니다. 중국의 1억 3,200만 명에 달하는 만성 신장 질환(CKD) 환자 수, 인도의 확대되는 검사 네트워크, 그리고 일본에서 세계 최고 수준인 투석 환자 수가 수요를 견인하고 있습니다. 지역 의료 분야의 선별 검사 지침과 단계적 치료 모델은 휴대용 분석 기기의 보급을 촉진하고 있습니다. 한국과 호주는 시장 규모는 작지만, AI의 급속한 도입과 명확한 규제가 특징이며, IDMS 준수 검사법의 조기 도입을 촉진하고 있습니다. 중동 및 아프리카와 남미는 시장 규모는 작지만 재생품 분석 장비나 저가 시약을 도입하고 있는 반면, 걸프협력회의(GCC) 회원국들은 고급 병원 인프라에 투자하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the creatinine measurement market size is projected to be USD 0.79 billion in 2025, USD 0.86 billion in 2026, and reach USD 1.29 billion by 2031, growing at a CAGR of 8.5% from 2026 to 2031.

This report is Segmented by Product Type (Reagents & Kits, Clinical Chemistry Analyzers, and More), Test Method (Jaffe, Enzymatic), Sample Type (Blood Serum/Plasma, Whole Blood, Urine), Testing Setting (Central Laboratory, Point-Of-Care), End User (Hospitals & Clinics, Diagnostic Laboratories, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Creatinine Measurement Market Trends and Insights

Rising CKD Prevalence And Screening Intensity

CKD affects more than 35 million adults in the United States, while China counts 132 million citizens with reduced kidney function, yet only 12.5% of Chinese patients are aware of their condition. National health agencies now embed creatinine and eGFR testing into primary-care protocols, and China's 2024 community-health guidelines direct mass screening with portable analyzers. Japan's dialysis registry reported 349,700 patients in 2023, each undergoing monthly creatinine checks to fine-tune treatment adequacy. In the United States, Medicare's Merit-based Incentive Payment System rewards physicians who document albumin-to-creatinine ratio results, lifting outpatient test volumes. Together, these programs funnel high-frequency samples into both laboratories and point-of-care channels, sustaining the creatinine measurement market.

Adoption Of Point-Of-Care Creatinine/eGFR Testing In Radiology And Critical Care

Radiology and intensive-care teams are relocating creatinine testing from central labs to bedside devices, shrinking turnaround from hours to minutes. Abbott's i-STAT cartridge delivers results in two minutes from 65 µL of whole blood and demonstrated an R2 = 0.99 correlation with core-lab assays in a 2024 Queensland ICU study. The U.K. National Institute for Health and Care Excellence endorses point-of-care creatinine devices for pre-contrast CT workflows, accelerating adoption in emergency imaging. Nova Biomedical's StatSensor generates eGFR on-device in 30 seconds from a fingerstick, expanding use in community pharmacies and low-resource HIV clinics in Tanzania. These capabilities reinforce the value proposition of the creatinine measurement market where rapid decision making prevents contrast-induced nephropathy and accelerates patient throughput.

Jaffe Method Interferences And Between-Method Variability

Positive interference from bilirubin and hemoglobin can inflate Jaffe results by up to 20%, while antibiotics may suppress readings, risking medication errors. A 2025 Annals of Laboratory Medicine review showed 4.6% LOINC mapping errors when aggregating multi-site results, underscoring how unharmonized methods can compromise longitudinal data. Siemens' Atellica CH Creatinine 3 assay introduces rate blanking and a 0.3 mg/dL bias correction but still faces cost-driven inertia compared with enzymatic reagents. These issues temper the otherwise robust outlook for the creatinine measurement market.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Jaffe To IDMS-Traceable Enzymatic Assays

- Expansion Of ACR Screening In Diabetes And Hypertension Programs

- Substitution Risk From Alternative Renal Biomarkers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits contributed 42.55% of 2025 revenue, establishing the largest slice of the creatinine measurement market size as laboratories lock into multi-year consumable contracts. Point-of-care meters and handhelds are forecast to rise 9.25% annually to 2031, propelled by imaging-suite protocols that demand under-two-minute turnaround. Clinical chemistry analyzers like Beckman Coulter's DxC 500i run 800 tests per hour, safeguarding core-lab dominance, while Roche's cobas c 703 doubles throughput to 2,000 tests per hour, underpinning reagent demand.

Calibrators and controls, though smaller in sales, secure assay traceability to NIST's SRM 967b and satisfy CLIA quality mandates. Roche's EUR 600 million facility under construction in Penzberg will automate antibody and enzyme production, reinforcing supply lines for global customers. Siemens promises 98% uptime on e-connected Atellica systems, sharpening service differentiation. In emerging economies, generic reagents from Asia introduce price pressure, yet bundled service contracts and uptime guarantees keep multinationals competitive within the creatinine measurement market.

Jaffe chemistry controlled 54.53% of the creatinine measurement market share in 2025 thanks to entrenched analyzer fleets and a 20-30% cost edge. Enzymatic assays are advancing at a 9.05% CAGR to 2031 as laboratories seek tighter alignment with IDMS standards and lower interference. The creatinine measurement industry also benefits from regulatory nudges; the FDA's dosing guidance effectively favors enzymatic methods for drug-label compliance.

Vendors pursue a dual-track strategy. Roche and Beckman Coulter list both Jaffe and enzymatic reagents, allowing budget-constrained labs to transition gradually. Siemens' modified Jaffe assay extends the life of legacy systems while offering rate blanking to cut bilirubin interference. As multi-center research networks demand harmonized data, enzymatic uptake will continue to erode Jaffe dominance, reinforcing momentum in the creatinine measurement market.

Geography Analysis

North America held 41.15% of 2025 revenue, propelled by 571,000 dialysis patients, Medicare incentives for ACR testing, and FDA guidance that prioritizes eGFR reporting. Canada invests in point-of-care devices to cut emergency wait times, while Mexico's expanding private diagnostic sector taps mid-range analyzers.

Europe's universal health systems and IVDR regulations guide method standardization. UK NEQAS data affirm enzymatic assays meet KDIGO bias targets better than Jaffe methods, shaping National Health Service procurement. Roche's Penzberg facility will bolster continental reagent supply chains by 2028. Yet ESUR risk-stratification protocols may temper radiology-point-of-care volumes.

Asia-Pacific is forecast to post a 9.51% CAGR, the fastest among regions. China's 132 million-patient CKD burden, India's expanding lab chains, and Japan's world-leading dialysis prevalence fuel demand. Community-health screening directives and tiered care models favor portable analyzers. South Korea and Australia, though smaller, feature rapid AI adoption and regulatory clarity, fostering early uptake of IDMS-aligned assays. Middle East, Africa, and South America contribute modest volumes but adopt refurbished analyzers and lower-priced reagents, while Gulf Cooperation Council countries invest in premium hospital infrastructure.

- Abbott Laboratories

- Beckman Coulter (Danaher)

- Beijing Leadman Biochemistry

- Dialab GmbH

- DiaSys Diagnostic Systems

- Diazyme Laboratories

- Elitech Group

- FUJIFILM (Wako Diagnostics)

- HemoCue

- Kanto Chemical

- Mindray

- Nova Biomedical

- Pointe Scientific (HORIBA)

- QuidelOrtho

- Radiometer

- Randox Laboratories

- Roche

- Sekisui Diagnostics

- Sentinel Diagnostics

- Mindray

- Siemens Healthineers

- Teco Diagnostics

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising CKD prevalence and screening intensity

- 4.2.2 Adoption of point-of-care creatinine/eGFR testing in radiology and critical care

- 4.2.3 Shift from Jaffe to IDMS-traceable enzymatic assays

- 4.2.4 Expansion of ACR (albumin-to-creatinine ratio) screening in diabetes and hypertension programs

- 4.2.5 Implementation of race-free CKD-EPI eGFR reporting in labs

- 4.3 Market Restraints

- 4.3.1 Jaffe method interferences and between-method variability

- 4.3.2 Reagent price pressure and commoditization in clinical chemistry

- 4.3.3 Substitution risk from alternative renal biomarkers in specific pathways

- 4.3.4 Guideline shifts that reduce routine pre-contrast testing in low-risk populations

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Reagents & Kits

- 5.1.2 Clinical Chemistry Analyzers

- 5.1.3 POC Devices - Meters/Handhelds

- 5.1.4 POC Cartridges/Strips

- 5.1.5 Calibrators & Controls

- 5.2 By Test Method

- 5.2.1 Jaffe (kinetic/compensated)

- 5.2.2 Enzymatic (IDMS-traceable)

- 5.3 By Sample Type

- 5.3.1 Blood (Serum/Plasma)

- 5.3.2 Whole Blood (POC)

- 5.3.3 Urine

- 5.4 By Testing Setting

- 5.4.1 Central Laboratory

- 5.4.2 Point-of-Care

- 5.5 By End User

- 5.5.1 Hospitals & Clinics

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Primary Care/Outpatient

- 5.5.4 Dialysis Centers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Beckman Coulter (Danaher)

- 6.3.3 Beijing Leadman Biochemistry

- 6.3.4 Dialab GmbH

- 6.3.5 DiaSys Diagnostic Systems

- 6.3.6 Diazyme Laboratories

- 6.3.7 ELITechGroup

- 6.3.8 FUJIFILM (Wako Diagnostics)

- 6.3.9 HemoCue

- 6.3.10 Kanto Chemical

- 6.3.11 Mindray

- 6.3.12 Nova Biomedical

- 6.3.13 Pointe Scientific (HORIBA)

- 6.3.14 QuidelOrtho

- 6.3.15 Radiometer

- 6.3.16 Randox Laboratories

- 6.3.17 Roche Diagnostics

- 6.3.18 Sekisui Diagnostics

- 6.3.19 Sentinel Diagnostics

- 6.3.20 Shenzhen Mindray Bio-Medical Electronics

- 6.3.21 Siemens Healthineers

- 6.3.22 Teco Diagnostics

- 6.3.23 Thermo Fisher Scientific

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment