|

시장보고서

상품코드

2063396

첨단 약물전달 CDMO : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Advanced Drug Delivery CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

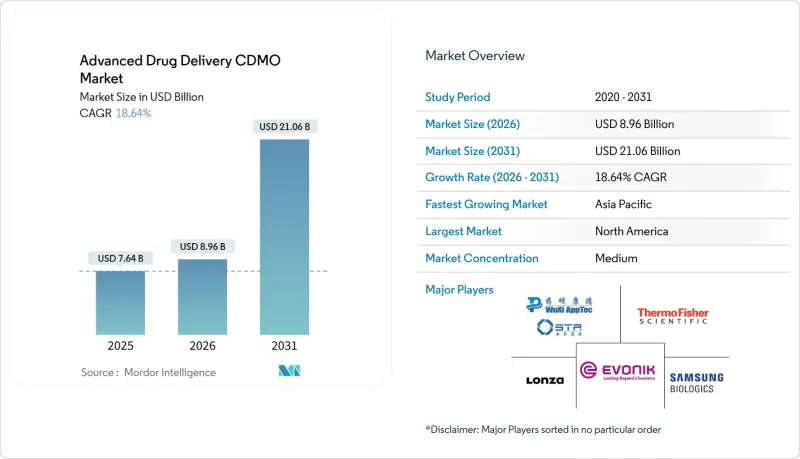

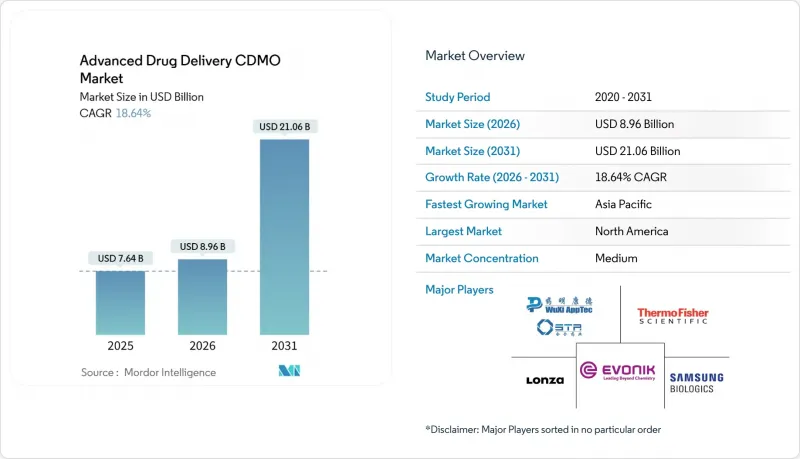

Mordor Intelligence에 의하면, 첨단 약물전달 CDMO 시장은 2025년 76억 4,000만 달러로 평가되었습니다. 2026년에는 89억 6,000만 달러에 달하고 2026-2031년에 걸쳐 CAGR 18.64%로 성장을 지속하여, 2031년까지 210억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 약물전달 기술(나노 입자 기반 전달, 기타), 서비스 유형(제제 설계 및 제제 개발, 기타), 분자 유형(저분자 화합물, 기타), 치료 분야(종양학, 기타), 고객 유형(제약 회사 및 생명공학 기업, 기타), 지역(북미, 기타)별로 세분화되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 첨단 약물전달 CDMO 시장 동향 및 인사이트

복잡한 바이오의약품에 대한 수요 증가

블록버스터 항체의 특허 만료에 더해, 후원사가 3억 달러 규모의 포유류 세포 배양 시설에 대한 자금 지원에 소극적인 태도를 보이고 있어, 이 프로젝트는 CDMO로 전환되고 있습니다. 후지필름·디오신즈는 2025년 4월, 레제네론사와 30억 달러 규모의 10년 제조 계약을 체결했습니다. 이는 현재까지 체결된 단일 CDMO 계약 중 최대 규모입니다. 삼성바이오로직스는 2025년 상반기에 33억 달러 규모의 신규 계약을 수주하며, 다년간의 생산 물량을 보장하는 대형 계약의 매력을 입증하고 있습니다. 현재 미국에서는 규제 당국에 의해 70종 이상의 바이오시밀러가 승인되어, 이에 따라 공급이 급증하고 있습니다. 이러한 상황은 검증된 세포 배양 및 무균 제조 설비를 보유한 CDMO에게 유리하게 작용하고 있습니다.

시장 출시 기간을 단축하는 아웃소싱

API부터 의약품 제제에 이르는 통합 모델을 통해, 전임상 단계에서의 인계부터 첫 인체 투여까지의 기간이 약 40% 단축되어, 벤처 기업은 더 조기에 수익을 창출할 수 있게 됩니다. 화이자의 CentreOne 사업부는 자사의 종단간 역량을 활용한 고객들이 여러 공급업체를 조율해야 하는 고객들보다 6개월 더 빨리 IND(신약 임상시험 신청)를 제출했다고 보고했습니다. 현재 미국과 EU의 규제 당국은 신규 배송 플랫폼에 대해 공동으로 자문을 제공하고 있으며, 이에 따라 심사 과정의 불확실성이 줄어들면서 스폰서들의 선호도는 검증된 규제 대응 실적을 보유한 CDMO로 쏠리고 있습니다. Fujifilm의 KojoX 네트워크와 같은 일회용 모듈형 바이오리액터 팜을 통해 CDMO는 몇 주 만에 임상용 배치 생산을 시작할 수 있으며, 상용화 협상을 병행하면서 프로그램의 시작을 가속화할 수 있습니다.

막대한 설비 투자와 검증 비용

항체-약물 복합체(ADC)의 단일 상업용 생산 라인을 구축하는 데는 2억 달러 이상의 비용이 소요되며, 여기에 가동 전 검증 비용으로 2,000만 달러가 추가로 발생합니다. 론자(Lonza)가 5억 스위스 프랑을 투자한 ‘Ibex Dedicate ADC’ 허브와, 삼성이 21억 달러를 투자한 ‘Bio Campus IV’는 이러한 재정적 장벽을 상징하는 사례입니다. 다제품 생산 설비의 경우, 두 번째 생물학적 제제를 도입할 때 FDA 지침에 따라 새로운 세척 검사 및 잔류물 검사가 필요하기 때문에 소요 기간이 2배로 늘어납니다. 2025년 채권 시장에서는 CDMO용 대출 금리가 벤치마크 금리보다 250베이시스포인트 높은 수준을 보였으며, 이는 기술의 노후화에 대한 대출 기관의 경계심을 반영했습니다.

부문별 분석

나노 입자 제제는 2025년 매출의 37.90%를 차지하며, 첨단 약물전달 CDMO 시장의 핵심으로서의 입지를 확고히 다졌습니다. COVID-19 mRNA 백신의 개발을 가능하게 한 지질 나노입자 툴킷은 현재 암 치료 및 희귀질환 프로그램의 기반이 되고 있으며, 무균 마이크로플루이딕스 기술과 고전단 믹서에 대한 수요를 촉진하고 있습니다. 지질 나노입자와 더 광범위한 지질 기반 시스템은 2031년까지 19.42%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이러한 효과는 순환 시간의 연장 및 말초 장기에 대한 뛰어난 축적성에서 비롯된 것으로, 이로 인해 전신 독성이 완화됩니다. PLGA 마이크로스피어를 기반으로 한 지속형 주사제는 최대 6개월 동안 안정적인 혈장 농도를 유지함으로써, 조현병 및 HIV 예방 치료에서 나타나는 복약 순응도 문제를 해결하고 큰 시장 점유율을 확보했습니다. 경피 흡수 및 마이크로니들 혁신 기술은 주사를 꺼리는 환자층에 대응하는 한편, 서방형 경구 투여 플랫폼은 만성 질환 관리 분야에서 여전히 주류를 이루고 있습니다. 나노 입자, 지질 나노 입자, 데포 제제 등 각 라인을 병행하여 보유한 CDMO는 분자의 라이프사이클 전반에 걸쳐 의뢰사의 선택지를 확보해 주는 다양한 치료 영역을 아우르는 계약을 수주하고 있습니다.

분석 및 특성 평가 부문은 2031년까지 19.21%라는 가장 높은 성장률을 보일 것으로 예상되며, 전 세계적으로 즉시 주입 가능한 제형으로의 전환에 힘입어 성장이 확실시되고 있습니다. ISO 클래스 5 기준을 충족하는 무균 아이솔레이터는 특히 고점도 바이오의약품 분야에서 고가에 거래되고 있습니다. 인실리코 모델을 활용하는 프리포뮬레이션 연구소는 다운스트림 공정에서의 수정 작업을 줄여주며, 통합된 분석 및 포장 시스템은 실시간 제품 출하와 ICH Q12의 지속적인 검증 요건을 충족합니다. 환자별 라벨링 및 일련번호 부여 서비스는 임상 검사 분야의 ‘라스트 마일’ 물류 문제를 해결함으로써 추가 수익을 창출하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 43.25%를 차지했습니다. 보스턴, 샌프란시스코, 샌디에이고 클러스터 인근에 위치한 FDA 검사 완료 시설에서는 ‘브레이크스루’ 및 ‘RMAT’ 지정에 따라 신속한 심사가 제공되고 있습니다. 미국은 세계 최대 규모의 충전 및 포장(필·마무리) 거점을 보유하고 있으나, 2024년에는 가동률이 85%를 넘어섰고, 슬롯 가격과 리드타임이 상승하고 있습니다. 캐나다에서는 연구개발 세액 공제율이 35%로 적용되는 반면, 멕시코는 지리적 이점을 살려 FDA와 COFEPRIS의 이중 감독 하에 있음에도 불구하고 무균 주사제 제조 거점으로 주목받고 있습니다.

유럽은 EMA(유럽의약품청)의 중앙 승인 제도를 바탕으로 견고한 시장 점유율을 유지하고 있으며, 스위스, 독일, 영국에는 첨단 바이오의약품 제조 시설이 입지해 있습니다. 영국의 ILAP(독립 의약품 평가 프로그램)은 시장 출시까지의 기간을 단축시켜, WuXi와 Samsung Biologics가 GMP 기준을 충족하는 생산 공간을 확충하는 계기가 되고 있습니다. 이탈리아와 스페인은 남유럽과 MENA 지역 수요에 대응하기 위해 바이오시밀러 생산 규모를 확대하고 있지만, 인프라 측면에서는 북유럽보다 5년 뒤처져 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년까지 21.03%의 성장률이 예상됩니다. 중국의 2024년 정책에 따라 생물학적 제제의 승인 기간이 12개월로 단축됨에 따라, 다국적 기업들은 전 세계 공급망에 중국의 CDMO를 도입하고 있습니다. 인도의 Biocon과 Piramal은 비용에 민감한 지역 시장을 공략하기 위해 펩타이드 및 바이오시밀러의 생산 능력을 확대했습니다. 호주와 유럽의약품청(EMA) 간의 상호 승인 협정에 따라, 유럽에서 승인된 제품은 간이 심사를 거쳐 시장에 진출할 수 있게 되었으며, EU 내 공장에서 오세아니아로 제품을 공급하는 것이 가능해졌습니다. 라틴아메리카의 상황은 여전히 제각각입니다. 아르헨티나의 통화 변동이 신규 건설을 가로막고 있지만, 기존 GMP 거점은 해당 지역의 희귀질환 임상 검사를 활용하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the advanced drug delivery cDMO market is expected to grow from USD 7.64 billion in 2025 to USD 8.96 billion in 2026 and is forecasted to reach USD 21.06 billion by 2031 at 18.64% CAGR over 2026-2031.

This report is Segmented by Drug Delivery Technology (Nanoparticle-Based Delivery and More), Service Type (Pre-Formulation & Formulation Development and More), Molecule Type (Small Molecules and More), Therapeutic Area (Oncology and More), Client Type (Pharmaceutical and Biotechnology Company and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Advanced Drug Delivery CDMO Market Trends and Insights

Increase in Demand for Complex Biologics

Blockbuster antibody patent expiries, coupled with sponsor reluctance to fund USD 300 million mammalian-cell suites, are pushing projects to CDMOs. FUJIFILM Diosynth secured a USD 3 billion, ten-year manufacturing pact with Regeneron in April 2025, the largest single CDMO contract to date. Samsung Biologics booked USD 3.3 billion in new deals in 1H 2025, underscoring the appeal of mega-contracts that guarantee multi-year slots. Regulators have now cleared more than 70 biosimilars in the United States, creating a supply rush that favors CDMOs holding validated cell-culture and aseptic suites.

Outsourcing to Accelerate Time-to-Market

Integrated API-to-drug-product models cut the interval from pre-clinical handoff to first-in-human dosing by roughly 40%, giving venture-backed firms earlier revenue recognition. Pfizer's CentreOne unit reported that clients leveraging its end-to-end capability filed INDs six months sooner than those coordinating multiple vendors. United States and EU regulators now offer joint advice on novel delivery platforms, reducing review uncertainty and tilting sponsor preference toward CDMOs with proven regulatory track records. Single-use, modular bioreactor farms, such as FUJIFILM's KojoX network, allow CDMOs to spin up clinical batches in weeks, accelerating program starts while commercial talks proceed in parallel.

High Capital Expenditure & Validation Costs

Building a single commercial line for antibody-drug conjugates can top USD 200 million, with validation adding another USD 20 million before launch. Lonza's CHF 500 million Ibex Dedicate ADC hub and Samsung's USD 2.1 billion Bio Campus IV exemplify the financial hurdle. Multi-product plants face doubled timelines because introducing a second biologic necessitates new cleaning studies and residue testing per FDA guidance. Debt markets in 2025 priced CDMO loans 250 basis points over benchmark rates, reflecting lender caution around technology obsolescence.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Injectable and Controlled-Release Formats

- Regulatory Incentives for Advanced Therapies

- Stringent Multi-region Compliance Audits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nanoparticle formats held 37.90% of 2025 revenue, cementing their role as the backbone of the Advanced Drug Delivery CDMO market. The lipid nanoparticle toolkit that enabled COVID-19 mRNA vaccines now underpins oncology and rare-disease programs, pushing demand for sterile microfluidics and high-shear mixers. Liposomal and broader lipid-based systems are forecast to post the fastest 19.42% CAGR through 2031. This momentum rests on prolonged circulation times and superior end-organ accumulation, which trim systemic toxicity. Long-acting injectables built on PLGA microspheres captured a meaningful share by delivering stable plasma levels for up to six months, addressing adherence gaps in schizophrenia and HIV prophylaxis. Transdermal and microneedle innovations cater to needle-averse cohorts, while controlled-release oral platforms continue to dominate chronic disease management. CDMOs that house parallel nanoparticle, liposome, and depot lines are winning cross-modality contracts that preserve sponsor optionality over the molecule's life cycle.

Analytical and characterization, the fastest-growing segment at 19.21% through 2031, secure their lift from the global pivot toward ready-to-inject formats. Aseptic isolators that meet ISO Class 5 norms command premium pricing, especially for high-viscosity biologics. Pre-formulation labs that use in silico models reduce downstream rework, and bundled analytical packages meet real-time release and ICH Q12 continuous-verification requirements. Patient-specific labeling and serialization services generate incremental revenue by solving last-mile clinical-trial logistics challenges.

Geography Analysis

North America delivered 43.25% of global revenue in 2025. FDA-inspected facilities near Boston, San-Francisco, and San Diego clusters offer expedited review under Breakthrough and RMAT designations. The United States has the world's most significant fill-finish footprint, yet utilization exceeded 85% in 2024, inflating slot prices and lead times. Canada extends 35% R&D tax credits, while Mexico's proximity lures sterile injectable manufacturing despite dual FDA-COFEPRIS oversight.

Europe retains a solid share on the back of the EMA's centralized approval, with Switzerland, Germany, and the United Kingdom housing advanced biologic suites. The UK's ILAP shortens time-to-market, attracting WuXi and Samsung Biologics to add GMP floor space. Italy and Spain scale biosimilar output to meet Southern Europe and MENA demand, though infrastructure lags Northern Europe by 5 years.

Asia-Pacific is the fastest-growing region, with 21.03% growth through 2031. China's 2024 policy reduced biologic approval timelines to 12 months, prompting multinationals to include Chinese CDMOs in their global supply chains. India's Biocon and Piramal expanded peptide and biosimilar capacity to serve cost-sensitive geographies. Australia's mutual-recognition pact with the EMA lets European-approved products enter on abbreviated review, enabling Oceania supply from EU plants. Latin America remains mixed; Argentina's currency swings deter new builds, but existing GMP sites tap regional rare-disease trials.

- Ajinomoto Bio-Pharma Services

- Alcami

- Baxter

- Delpharm

- Emergent

- Evonik Health Care

- Fareva

- Jubilant HollisterStier

- Lonza Group

- PCI Pharma Services

- Piramal Group

- Recipharm

- Samsung Group

- Siegfried Holding AG

- SK pharmteco

- Thermo Fisher Scientific Inc. (Patheon)

- Vetter Pharma

- WuXi STA (WuXi AppTec)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand for Complex Biologics

- 4.2.2 Outsourcing to Accelerate Time-to-Market

- 4.2.3 Growth in Injectable and Controlled-Release Formats

- 4.2.4 Regulatory Incentives for Advanced Therapies

- 4.2.5 Micro-Batch Capacity for High-Potency Drugs

- 4.2.6 3D-Printed Implantable Delivery Systems

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure & Validation Costs

- 4.3.2 Stringent Multi-region Compliance Audits

- 4.3.3 Excipients Supply-chain Bottlenecks

- 4.3.4 Shortage of skilled professionals in nano-encapsulation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Delivery Technology

- 5.1.1 Nanoparticle-based Delivery

- 5.1.2 Liposomal / Lipid-based Delivery

- 5.1.3 Long-acting Injectables

- 5.1.4 Implantable Delivery Systems

- 5.1.5 Transdermal Patches & Microneedles

- 5.1.6 Oral Controlled-Release Systems

- 5.1.7 Other Advanced Delivery Technology

- 5.2 By Service Type

- 5.2.1 Pre-formulation & Formulation Development

- 5.2.2 Analytical & Characterization Services

- 5.2.3 Scale-up & Process Development

- 5.2.4 Clinical & Commercial Manufacturing

- 5.2.5 Fill -finish & Aseptic Processing

- 5.2.6 Packaging & Kitting

- 5.2.7 Others Service Type

- 5.3 By Molecule Type

- 5.3.1 Small Molecules

- 5.3.2 Biologics & Biosimilars

- 5.3.3 Gene & Cell Therapies

- 5.3.4 Peptide & Oligonucleotide Therapeutics

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Central Nervous System Disorders

- 5.4.3 Infectious Diseases & Vaccines

- 5.4.4 Cardiovascular & Metabolic Disorders

- 5.4.5 Rare Diseases & Orphan Indications

- 5.4.6 Other Therapeutic Areas

- 5.5 By Client Type

- 5.5.1 Pharmaceutical and Biotechnology Company

- 5.5.2 Academic and Government Institutions

- 5.5.3 Others Client Type

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 United Kingdom

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Ajinomoto Bio-Pharma Services

- 6.3.2 Alcami Corporation

- 6.3.3 Baxter

- 6.3.4 Delpharm

- 6.3.5 Emergent

- 6.3.6 Evonik Health Care

- 6.3.7 Fareva

- 6.3.8 Jubilant HollisterStier

- 6.3.9 Lonza Group AG

- 6.3.10 PCI Pharma Services

- 6.3.11 Piramal Pharma Solutions

- 6.3.12 Recipharm AB

- 6.3.13 Samsung Biologics

- 6.3.14 Siegfried Holding AG

- 6.3.15 SK pharmteco

- 6.3.16 Thermo Fisher Scientific Inc. (Patheon)

- 6.3.17 Vetter Pharma

- 6.3.18 WuXi STA (WuXi AppTec)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment