|

시장보고서

상품코드

2063415

가정용 수면 검사 기기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Home Sleep Screening Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

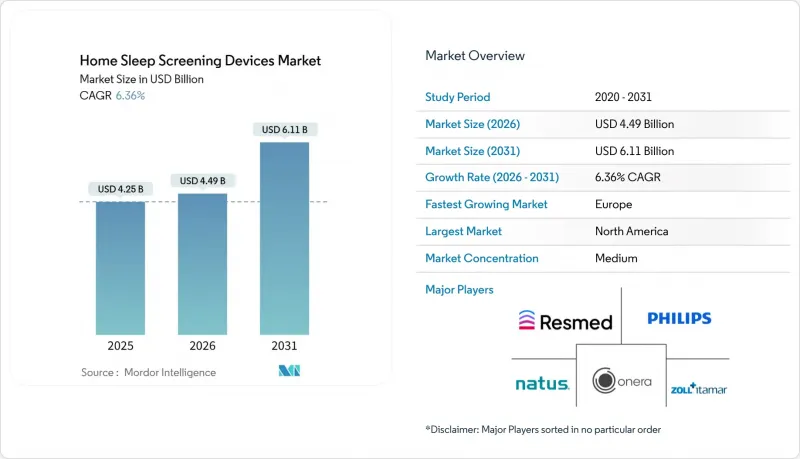

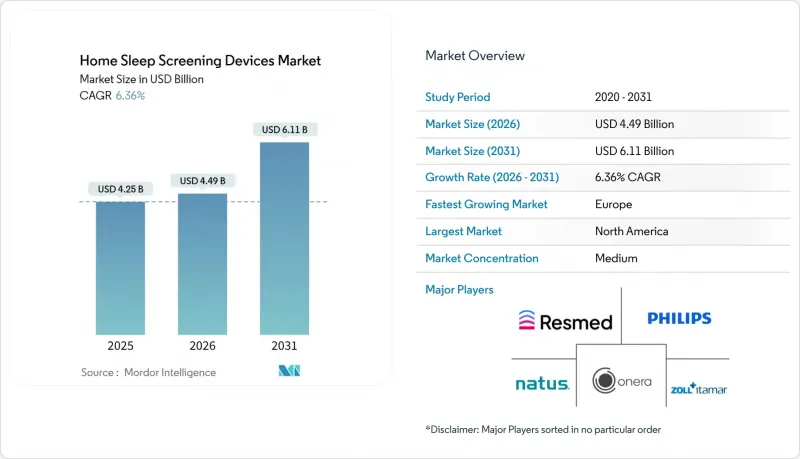

Mordor Intelligence에 의하면, 가정용 수면 검사 기기 시장 규모는 2025년 42억 5,000만 달러로 평가되었습니다. 2026년 44억 9,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 6.36%를 나타내, 2031년에는 61억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 검사 유형(유형 II, 유형 III, 유형 IV), 판매 채널(온라인, 오프라인) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 가정용 수면 검사 기기 시장 동향 및 인사이트

주요 시장에서 지불자 주도의 HSAT 보험 적용 및 코딩

메디케어의 LCD L33405 및 CPT 95800/95801/95806에 따라 무인 검사에 대한 지급이 표준화되었으나, 2025년 의사 보수 일정에서는 특정 코드가 삭제되어 파생 채널에만 의존하는 기기가 제외되었습니다. 이 규정은 비강 유량 및 호흡 노력 데이터를 수집하는 4채널 유형 III 시스템을 우대하고 있어, 구매 동향을 기존 DME 공급업체 쪽으로 기울게 하고 있습니다. UnitedHealthcare를 비롯한 민간 보험사들은 메디케어의 방침을 반영하여 기술자에 의한 수동 평가를 의무화하고 있으며, 이로 인해 기존의 업무 흐름이 더욱 공고해지고 있습니다. 따라서 스타트업 기업들은 적용 규정이 완화된 자비 진료나 고용주 대상 프로그램을 겨냥해 일회용 웨어러블 기기를 출시하고 있습니다. 이러한 추세로 인해, 저사양 센서형 웨어러블 기기에 대한 소비자의 관심이 계속해서 높아지는 상황에서도, 가정용 수면 스크리닝 기기 시장은 규제를 준수하는 하드웨어에 계속 의존하게 될 것입니다.

비용과 편의성을 추구한 재택 진단으로의 전환

HSAT 비용은 검사 1회당 150-600달러인 반면, 시설 내에서 실시하는 수면 다원검사(PSG)는 1,000-1만 달러가 들기 때문에 의료 제공업체에게는 즉각적인 경제적 이점이 있습니다. 2024년 VA(재향군인부)의 분석에 따르면, HSAT는 운영일당 1,211달러의 수익을 창출한 반면, PSG는 902달러에 그쳤으며, 이로 인해 병원들의 재택 검사 경로 도입이 가속화되고 있습니다. ResMed사의 NightOwl과 같이 10박 사용이 승인된 일회용 솔루션은 더 풍부한 종단적 데이터를 통해 비용 대비 효과를 높이고 있습니다. GEM SLEEP을 비롯한 소비자 직접 판매 플랫폼은 단 189달러에 우편 키트를 발송하고 있으며, 중등도에서 중증의 수면무호흡증(OSA)을 앓고 있음에도 진단을 받지 못한 2,000만 명의 미국인을 주요 타겟으로 삼고 있습니다.

그러나 재택 검사에서는 데이터 결손으로 인해 검사당 비용이 15-20% 상승하고, 검사 결과의 13.5%가 불확실한 상태로 남게 되므로 고가의 추적 PSG가 필요하게 됩니다. 그럼에도 불구하고, 높은 편의성 덕분에 구매 결정이 재택형 모델로 기울어지고 있으며, 이는 가정용 수면 선별 기기 시장의 꾸준한 성장을 뒷받침하고 있습니다.

임상적 제한 및 수기 재평가

AASM 지침에 따르면, HSAT의 적용 대상은 검사 전 확률이 매우 높고 중대한 동반 질환이 없는 성인으로 제한하고 있습니다. 2026년 스페인에서 329명의 환자를 대상으로 실시된 다기관 공동 연구에 따르면, 중증 OSA의 경우 자동 채점 결과와 PSG 결과가 96.2% 일치했으나, 중증도와 관계없이 전체적으로는 일치율이 41.6%로 떨어졌으며, 이로 인해 전문의에 의한 재평가의 필요성이 부각되었습니다. 수동 재평가에는 건당 15-30분이 소요되어, 자동화를 통한 업무 부담 경감의 이점을 상쇄해 버립니다. 또한, 1차 진료 경로에서의 치료 순응도는 수면 전문의 코호트와 비교했을 때 13% 더 낮아, 장기적인 예후 위험을 드러내고 있습니다. 이러한 장벽들로 인해 가정용 수면 선별 기기 시장의 성장 속도가 둔화되고 있습니다.

부문별 분석

2025년에는 유형 III 시스템이 시장의 66.23%를 차지했습니다. 이는 메디케어와 대부분의 민간 보험사가 단순한 폐쇄성 수면무호흡증의 경우, 이 정도면 충분하다고 판단하기 때문입니다. 그럼에도 불구하고, 유형 IV 디바이스는 저렴한 가격, 소비자에게 직접 판매, 그리고 단일 채널의 데이터를 분석할 수 있는 AI 덕분에 2031년까지 연평균 9.21%라는 가장 높은 성장률을 유지할 것으로 전망됩니다. 이러한 1채널 또는 2채널 제품(대개 맥박 산소 포화도 측정, 활동도 측정 또는 단일 리드 심전도)은 보험 적용 진단을 위한 CMS(미국 의료보험서비스센터)의 4채널 요건을 충족한 적은 없지만, 그 장점은 무시할 수 없습니다.

검사 비용은 약 150-300달러이며, 센서의 착용감도 편안하여 환자는 비강 캐뉼라나 가슴 벨트의 번거로움 없이 1주일 이상 계속 착용할 수 있습니다. 이러한 장점 덕분에, 개인 부담 건강검진, 기업 대상 프로그램 및 지속적인 모니터링 분야에서 인기를 끌고 있습니다. 2024년 초에 승인된 삼성의 ‘갤럭시 워치’는 일반 소비자용 웨어러블 기기가 이 분야에 진출하고 있음을 보여주고 있는 반면, SleepImage는 단일 유도 심전도를 이용해 수면 품질 지수를 산출하며, 현재 2세 아동부터 사용이 승인되어 있습니다. 레스메드사의 ‘나이트올’은 10박 동안의 검사가 승인된 일회용 PAT 기기로, 유형 III와 유형 IV의 경계선에 위치하고 있습니다. 이는 렌탈에 따른 물류 비용보다 일회용의 경제성이 더 높은 여러 날에 걸친 검사라는 틈새 시장을 명확히 겨냥한 것입니다.

완전한 수면 단계 분류를 위한 뇌파(EEG) 및 턱근육 근전도(EMG)를 포함한 제2형 기기는 비용이 비싸고 설정에 시간이 오래 걸리기 때문에 틈새 시장 수준에 머물러 있지만, 복잡한 증례에서는 그 진가를 발휘합니다. 이 분야에서 Huxley Medical사의 SANSA 패치는 중추성 수면 무호흡증에 대해 100%의 민감도와 99%의 특이도를 보여주고 있습니다.

지역별 분석

북미는 2025년 매출의 49.34%를 차지했습니다. 이는 메디케어의 통합된 HSAT 코드(95800/95801/95806)와, 검사실의 밀린 업무 해소를 서두르는 대규모 의료 시스템의 지원 덕분입니다. 이 시장의 상당 부분은 미국이 주도하고 있으며, 약 5,400만 명의 성인이 경증에서 중증의 수면무호흡증(OSA)을 앓고 있고, 그중 2,000만 명 이상이 여전히 진단받지 못한 상태입니다. 최근 진료보수 개정에 따른 보수 삭감과 2023년 파생 채널 금지 조치로 인해 가격이 압박을 받으면서, 싱글 채널형 웨어러블 기기의 보급이 주춤하고 있습니다. 2026년 메이요 클리닉의 검토에 따르면, 1차 진료에서 HSAT 경로를 통해 치료까지의 대기 기간 중앙값이 113일에서 28일로 단축된 것으로 나타났으나, 전문의가 관리하는 환자의 경우 야간 PAP 준수율이 13% 향상되었으며, 속도와 장기적인 치료 성과 사이의 상충 관계가 부각되었습니다. 캐나다의 보험 적용 범위는 주마다 다르며, 온타리오주와 브리티시컬럼비아주가 선도하고 있지만, 멕시코에서는 민간 보험이 세분화되어 있어 주요 도시 이외의 지역에서는 보급률이 여전히 낮은 임베디드니다. 고위험군 성인을 대상으로 한 검사가 널리 시행되고 있는 현재, 각 기업은 여성, 소수자 집단, 어린이 등 진단이 충분히 이루어지지 않는 그룹에 주목하고 있습니다. WatchPAT(12세 이상) 및 SleepImage(2세 이상)에 대한 FDA 승인으로 인해 해당 부문으로의 진출 길이 열렸으나, 보험사의 정책은 아직 이를 따라가지 못하고 있는 상황입니다.

유럽에서는 의료기기 규정(MDR)에 따른 기준 통일, 디지털 헬스 프로그램을 통한 보험 적용 범위 확대, 그리고 Philips 레스피로닉스(Philips Respironics)와의 화해 합의로 인해 고객들이 새로운 공급업체로 전환하고 있는 만큼, 2031년까지의 연평균 성장률(CAGR)은 8.09%를 나타낼 것으로 전망됩니다. 독일의 DiGA 체계에서는 이미 AI를 활용한 평가를 수행하는 수면 앱에 대한 보험 급여가 이루어지고 있으며, 프랑스의 PECAN 패스웨이와 영국의 NICE 지침 역시 1차 진료 분야에서 HSAT의 활용을 지원하고 있습니다. 그러나 자금 조달 상황은 제각각입니다. 독일, 프랑스, 영국에서는 탄탄한 공공 지원이 이루어지고 있지만, 남유럽 및 동유럽의 많은 국가에서는 본인 부담이나 민간 보험에 의존하고 있습니다. MDR의 강화된 증거 요건은 신규 진출기업에게는 장벽이 되지만, 강력한 임상 데이터를 보유한 기업에게는 유리하게 작용합니다. 투자자들의 관심은 여전히 높습니다. Onera Health가 2024년에 진행한 3,000만 유로 규모의 시리즈 C 투자 유치와 독일 내 7곳에서 실시된 검증 시험은 패치형 플랫폼에 대한 높은 신뢰도를 입증하고 있습니다.

아시아태평양에서는 막중한 질병 부담과 시장 접근성의 불균형이 공존하고 있습니다. 중국 성인 OSA 유병률은 지난 20년 동안 8.1%에서 26.9%로 급증했으며(약 1억 7,600만 명), 그러나 성별 보험 적용 현황은 일관되지 않아 유병률이 높음에도 불구하고 지방 환자들은 종종 본인 부담으로 비용을 지불하고 있습니다. 알리페이의 AI 도구 ‘Hang Hao Meng’은 이미 300만 명 이상의 사용자를 선별하여 9만 100건의 잠재적 사례를 파악했으나, 전국적인 보험 환급 정책이 없어 많은 환자가 진단 검사를 받지 못하고 있습니다. 일본의 잘 구축된 수면 의학 네트워크는 HSAT의 꾸준한 활용을 뒷받침하고 있지만, 국민건강보험에서는 여전히 검사실에서의 검사가 우선시되고 있습니다. 인도에서는 전문의가 도시 지역에 집중되어 있다는 점과 ‘아유슈만 바라트’ 하에서 통일된 HSAT 지급 제도가 없습니다는 점이 여전히 걸림돌로 작용하고 있습니다. 그 밖의 지역 중 중동 및 아프리카 및 남미는 여전히 초기 단계 시장입니다. 이 지역에서의 도입은 GCC 국가들, 남아프리카공화국, 브라질, 아르헨티나의 민간 클리닉을 중심으로 진행되고 있습니다. 수입 관세, 복잡한 승인 절차, 공공 자금 부족이 성장을 저해하고 있지만, 브라질의 SUS나 남아프리카공화국의 NHI에서 진행 중인 시범 사업이 확대된다면 접근성이 향상될 가능성이 있습니다. 현지 인증 및 환경 규제를 준수하는 것은 해당 지역에 진출하려는 전 세계 제조업체들에게 추가적인 비용 부담을 안겨줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the home sleep screening devices market size is expected to grow from USD 4.25 billion in 2025 to USD 4.49 billion in 2026 and is forecast to reach USD 6.11 billion by 2031 at 6.36% CAGR over 2026-2031.

This report is Segmented by Test Type (Type II, Type III, Type IV), Distribution Channel (Online, Offline), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Home Sleep Screening Devices Market Trends and Insights

Payer-Aligned HSAT Coverage and Coding in Key Markets

Medicare's LCD L33405 and CPT 95800/95801/95806 have standardized payment for unattended studies, but the 2025 Physician Fee Schedule trimmed certain codes and barred devices that rely only on derived channels. The rule favors four-channel Type III systems that collect nasal flow and respiratory effort data, tilting purchasing toward established DME suppliers. Private insurers, led by UnitedHealthcare, mirror Medicare's stance and require manual technologist scoring, further entrenching incumbent workflows. Startups therefore steer disposable wearables to cash-pay and employer programs where coverage rules are looser. These dynamics will keep the Home Sleep Screening Devices market anchored to rule-compliant hardware, even as consumer interest in low-sensor wearables continues to rise.

Shift to Home Diagnostics for Cost and Convenience

HSAT costs range from USD 150 to USD 600 per study, compared with USD 1,000-10,000 for in-lab polysomnography, creating an immediate economic appeal for providers. A 2024 VA analysis showed that HSAT generated USD 1,211 in revenue per operational day, compared with USD 902 for PSG, accelerating hospital adoption of home pathways. Disposable solutions such as ResMed's NightOwl, cleared for ten-night use, strengthen the cost-benefit equation with richer longitudinal data. Direct-to-consumer platforms, including GEM SLEEP, ship mail-order kits for as little as USD 189 and target the 20 million undiagnosed Americans with moderate-to-severe OSA.

However, at-home data loss lifts per-test cost by 15-20%, and 13.5% of studies remain inconclusive, prompting costly follow-up PSG. Even so, the convenience premium is shifting purchase decisions toward home models, supporting steady gains for the Home Sleep Screening Devices market.

Clinical Limits and Manual Overread

AASM guidelines restrict HSAT to adults with high pretest probability and no major comorbidities. A 2026 Spanish multicenter study of 329 patients found autoscoring matched PSG for severe OSA in 96.2% of cases, but agreement fell to 41.6% across all severities, underscoring the need for specialist review. Manual overread adds 15-30 minutes per study and dulls the labor-saving edge of automation. Lower therapy adherence in primary-care pathways 13% below sleep-specialist cohorts-exposes long-term outcome risks. These barriers temper the growth velocity of the Home Sleep Screening Devices market.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Wearable and Patch Sensors

- Telemedicine Workflow and AI-Assisted Scoring Integration

- Uneven Reimbursement and Procurement Hurdles in Developing Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type III systems controlled 66.23% of the market in 2025 because Medicare and most private insurers view them as adequate for straightforward obstructive sleep apnea cases. Even so, Type IV devices are on track to grow the fastest-9.21% a year through 2031-due to lower prices, direct-to-consumer sales, and AI that can interpret single-channel data. These one- or two-channel products (often pulse oximetry, actigraphy, or single-lead ECG) have never met CMS's four-channel rule for reimbursed diagnosis, yet their advantages are hard to ignore.

A test costs about USD 150-300, the sensors are more comfortable, and patients can wear them for a week or longer without the hassle of nasal cannulas or chest belts. That combination makes them popular for cash-pay wellness checks, employer programs, and ongoing monitoring. Samsung's Galaxy Watch, cleared in early 2024, shows how consumer wearables are moving into this space, while SleepImage uses single-lead ECG to generate a Sleep Quality Index and now has clearance for children as young as two. ResMed's NightOwl-a disposable PAT device approved for ten-night studies-sits on the borderline between Type III and Type IV, aiming squarely at the multi-night niche where single-use economics beat rental logistics.

Type II devices, which include EEG and chin EMG for full sleep staging, stay niche because they cost more and take longer to set up, but they shine in complex cases-an area Huxley Medical's SANSA patch now addresses with 100% sensitivity and 99% specificity for central sleep apnea.

Geography Analysis

North America generated 49.34% of 2025 revenue, helped by Medicare's uniform HSAT codes (95800/95801/95806) and large health systems eager to clear lab backlogs. The United States drives most of this value, with about 54 million adults living with mild-to-severe OSA and more than 20 million of them still undiagnosed. Recent fee-schedule cuts and the 2023 ban on derived channels have squeezed prices and slowed uptake of single-channel wearables. A 2026 Mayo Clinic review showed that primary-care HSAT pathways trimmed the median wait for treatment from 113 to 28 days, but specialist-managed patients logged 13% better nightly PAP adherence, highlighting a trade-off between speed and long-term outcomes. Canada's coverage varies by province-Ontario and British Columbia lead-while Mexico's fragmented private insurance keeps adoption low outside major cities. With high-probability adults now widely tested, companies are turning to underdiagnosed groups such as women, minority communities, and children. FDA clearances for WatchPAT (12 years and older) and SleepImage (down to age 2) open these segments, although payer policies are still catching up.

Europe is on track for an 8.09% CAGR through 2031 as the Medical Device Regulation (MDR) aligns standards, digital-health programs expand reimbursement, and the Philips Respironics consent decree pushes customers toward new suppliers. Germany's DiGA framework already reimburses AI-scored sleep apps, while France's PECAN pathway and NICE guidance in the UK support HSAT use in primary care. Funding, however, is uneven: Germany, France, and the UK provide solid public support, whereas much of Southern and Eastern Europe rely on out-of-pocket spending or private cover. MDR's tougher evidence rules raise hurdles for small entrants but reward firms with strong clinical data. Investor interest remains high; Onera Health's EUR 30 million Series C round in 2024 and its seven-site German validation study underscore confidence in patch-based platforms.

Asia-Pacific combines a heavy disease burden with patchy market access. China's adult OSA prevalence jumped from 8.1% to 26.9% over two decades-about 176 million people-yet provincial insurance coverage is inconsistent and rural patients often pay cash despite higher prevalence rates. Alipay's Hang Hao Meng AI tool has already screened more than 3 million users and flagged 90,100 potential cases, but without a national reimbursement policy, many never move to diagnostic testing. Japan's mature sleep-medicine network supports steady HSAT use, though its national insurance still favors lab studies. India remains limited by an urban concentration of specialists and no unified HSAT payment under Ayushman Bharat. Elsewhere, the Middle East & Africa and South America are still early-stage markets. Adoption there centers on private clinics in the GCC, South Africa, Brazil, and Argentina. Import duties, complex approvals, and absent public funding hold back growth, though pilot projects in Brazil's SUS and South Africa's NHI could widen access if they scale. Compliance with local certifications and environmental rules adds further cost for global manufacturers looking to enter these regions.

- Bittium

- BRAEBON Medical

- Cadwell Industries

- Cleveland Medical Devices Inc

- Compumedics

- Koninklijke Philips

- MyCardio LLC

- Natus Medical

- Nonin Medical

- Nox Medical

- Onera Health

- Resmed

- SOMNOmedics

- Watermark Medical

- ZOLL Itamar

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Payer-Aligned HSAT Coverage and Coding in Key Markets

- 4.2.2 Shift To Home Diagnostics for Cost and Convenience

- 4.2.3 Advancements In Wearable/Patch Sensors And PAT/PPG Platforms

- 4.2.4 Telemedicine Workflow And AI-Assisted Scoring Integration

- 4.2.5 AI-Derived Total Sleep Time Enabling Higher Reimbursements Were Permitted

- 4.2.6 New De Novo and Pediatric-Clearances Expand Eligible Populations

- 4.3 Market Restraints

- 4.3.1 Clinical Limitations and Manual Overread; Restricted to Uncomplicated Adults

- 4.3.2 Uneven Reimbursement and Procurement Hurdles in Developing Markets

- 4.3.3 CMS Prohibition on Derived/Virtual Channels Limits Some Novel Devices

- 4.3.4 At-Home Data Loss/Retests and Logistics Increase Per-Test Cost

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Type II

- 5.1.2 Type III

- 5.1.3 Type IV

- 5.2 By Distribution Channel

- 5.2.1 Online

- 5.2.2 Offline

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Bittium

- 6.3.2 BRAEBON Medical

- 6.3.3 Cadwell Industries

- 6.3.4 Cleveland Medical Devices Inc

- 6.3.5 Compumedics

- 6.3.6 Koninklijke Philips

- 6.3.7 MyCardio LLC

- 6.3.8 Natus Medical

- 6.3.9 Nonin Medical

- 6.3.10 Nox Medical

- 6.3.11 Onera Health

- 6.3.12 ResMed Inc.

- 6.3.13 SOMNOmedics

- 6.3.14 Watermark Medical

- 6.3.15 ZOLL Itamar

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment