|

시장보고서

상품코드

2063419

기초 인슐린 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Basal Insulin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

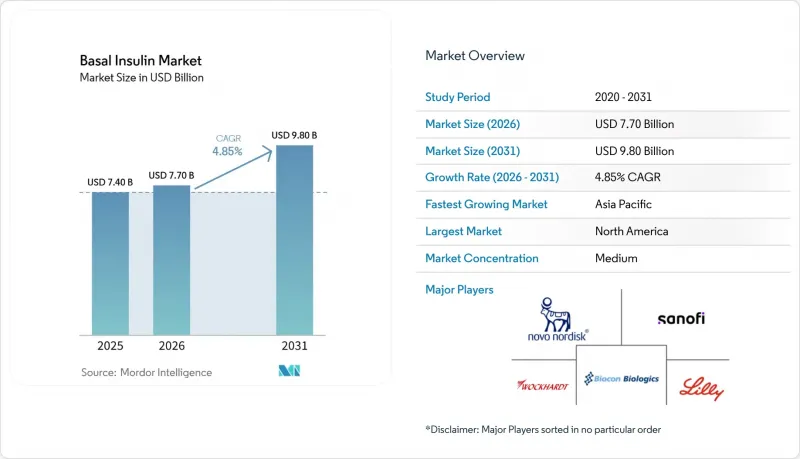

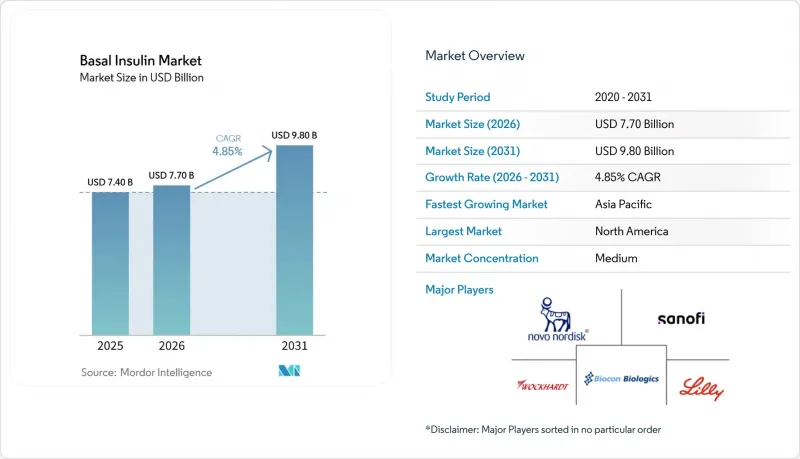

Mordor Intelligence에 의하면, 기초 인슐린 시장 규모는 2025년 74억 달러로 평가되었습니다. 2026년 77억 달러로 확대되어 2031년까지 98억 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 4.85%를 나타낼 전망입니다.

본 보고서는 분자별(그랄긴, 데테밀, 데글루덱, 기타), 투여 기기별(바이알·주사기, 프리필드 일회용 펜 등), 환자 유형(1형 당뇨병, 기타), 유통 채널(병원 약국, 소매 약국, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 기초 인슐린 시장 동향 및 분석

전 세계 당뇨병 유병률 증가

NCD 얼라이언스에 따르면, 현재 전 세계 성인의 9명 중 1명 이상이 당뇨병을 앓고 있으며, 2045년까지 8억 5,300만 명으로 증가할 것으로 예측됩니다. 현재 신규 확진자의 대부분은 저·중소득국에서 발생하고 있지만, 치료에 대한 접근성은 역학적 수요를 따라가지 못하고 있습니다. 2025년 12월 노보노르디스크가 인도에서 주당 24달러라는 가격으로 출시한 ‘오젠픽’과 같은 적극적인 현지 가격 전략은 판매량 확대에 기여하는 한편, 이익률을 압박하고 있습니다. 미국에서는 CDC(미국 질병통제예방센터)의 추산에 따르면 3,800만 명이 당뇨병을 앓고 있습니다. 2026년 시범 프로그램에 따라 메디케어 수급자 중 일부가 GLP-1 제제의 보험 적용 대상이 되면서, 인슐린 치료를 시작할 예정이었던 많은 환자들이 인크레틴 요법으로 전환하고 있습니다. 따라서 기초 인슐린 시장은 절대적으로는 확대되고 있지만, 치료 알고리즘의 발전에 따라 적격 환자 수라는 분모가 축소되는 과제에 직면해 있습니다.

장시간 작용형 인슐린 아날로그의 보급

그랄긴, 데글루덱, 데테밀은 안전성 측면에서 NPH 인슐린을 대체했으나, 현재는 바이오시밀러와의 경쟁으로 인해 아날로그 제제의 가격 프리미엄이 잠식되고 있습니다. 셈그리는 란타스의 정가보다 64% 저렴한 가격에 출시되었으며, UC 헬스가 제공한 실제 임상 데이터에서 동등한 혈당 조절 효과를 보였습니다. 사노피의 메릴로그는 2026년 2월 미국에서 승인된 최초의 속효성 바이오시밀러가 되었으며, 기초 인슐린 아날로그 후속 제품의 승인을 가속화하는 선례를 마련했습니다. 2026년에 개정된 ‘Diabetes Canada’ 지침은 1형 당뇨병 환자에서 이코덱의 저혈당 위험에 대해 주의를 환기하고 있으며, 이는 선진국 시장에서는 아날로그 제제의 보급이 정체되는 반면, 바이오시밀러가 합리적인 가격으로 그 격차를 메워주는 신흥 지역에서는 보급이 확대될 것임을 시사합니다.

GLP-1 제제의 보급이 기초 인슐린 도입을 늦춥니다.

SURPASS-4 임상시험에서 틸제파티드는 그랄긴에 비해 인슐린 투여량을 71% 감소시켰으며, 기초 인슐린을 치료 단계의 더 뒤쪽으로 밀어내는 것으로 나타났습니다. SUSTAIN-4 및 그 이후의 임상시험에서 세마글루티드가 HbA1c 감소와 10-15%의 체중 감소라는 두 가지 이점을 지닌 것으로 확인되어, GLP-1 수용체 작용제가 2형 당뇨병 치료에 있어 우선적으로 선택되는 주사제로 자리매김하고 있습니다. 경구용 제제인 노보의 세마글루티드(2025년 12월 승인)와 릴리의 올포글리프론(2026년 4월 승인)은월149달러로, 주사 치료의 장벽을 없애고 기초 인슐린 스타터 팩과 동등한 비용을 실현합니다. 2027년부터 적용될 메디케어의 세마글루티드월274달러 협상 가격은 GLP-1 수용체 작용제에 대한 지불 주체의 선호를 확고히 하고, 선진국 시장에서 기초 인슐린의 도입을 축소시킬 것입니다.

부문별 분석

데테미르는 2031년까지 연평균 성장률(CAGR) 5.67%를 나타낼 것으로 예측되며, 이는 기초 인슐린 제제 중 가장 높은 성장률입니다. 이러한 회복에는 세 가지 요인이 있습니다. 첫째, 신흥 시장에서 바이오시밀러가 브랜드 의약품보다 훨씬 저렴한 가격에 출시되기 때문에 의약품 예산이 제한된 지역에서 하루 2회 투여하는 데테미르가 매력적인 선택지로 떠오르고 있습니다. 둘째, 비용에 민감한 지역의 지급 기관은 고가의 1일 1회 투여 제품이 아닌, 이러한 저가 대안을 처방 목록에 포함하도록 유도하고 있습니다. 셋째, 임상의들은 GLP-1 제제의 병용 요법을 경제적으로 감당할 수 없는 비만 2형 당뇨병 환자들에게 데테미르가 체중에 영향을 미치지 않는다는 특성에 가치를 두고 있습니다.

2025년에도 사노피의 란타스와 투제오에 힘입어 그랄긴이 분자 시장 점유율의 45.67%를 차지하며 선두 자리를 지켰지만, 셈그리나 레즈보글라와 같은 바이오시밀러들이 가격 경쟁력을 무기로 그 지위를 서서히 잠식하고 있습니다. '트레시바'라는 이름으로 판매되고 있는 데글루덱은 투여의 유연성이라는 강점을 유지하고 있지만, 미국 내 가격 압박과 바이오시밀러와의 경쟁에 직면해 있어 성장률은 한 자릿수 초반에 머물고 있습니다. ‘기타’ 그룹(주 1회 투여하는 이코덱 및 릴리사의 파이프라인 제품인 에프시토라 알파)은 2026년 3월 아위크리가 2형 당뇨병 적응증으로 FDA 승인을 획득하며 입지를 다졌으나, 1형 당뇨병 적응증에서는 제외되어 있기 때문에 인슐린 사용자의 대다수로만 제한되어 있습니다.

2025년에는 프리필드 펜이 58.34%의 점유율로 1위를 차지했으나, 재사용 가능한 펜과 스마트 펜은 2031년까지 연평균 성장률(CAGR) 6.12%를 기록하며 기초 인슐린 시장 전체의 성장률을 상회하고 있습니다. 북미에서는 기존 바이알이 차지하는 기초 인슐린 시장 점유율이 감소하고 있지만, 인도와 사하라 이남 아프리카에서는 투여량의 상당 부분을 여전히 바이알에 의존하고 있습니다. ADA(미국당뇨병학회)의 지침 변경에 따라, 스마트 펜과 CGM 세트가 미국 내 보험사들의 우선 처방 의약품 목록에 등재되는 사례가 급속히 늘어나고 있습니다. 펜과 풀루프 펌프의 중간에 위치하는 인슬렛(Inslet)사의 ‘옴니팟 GO’(기초 인슐린 전용 튜브리스 펌프)는 2030년까지 상당한 시장 점유율을 확보할 가능성이 있습니다.

입소메드와 BD가 공동으로 개발 중인 자동 주사기는 고점도 바이오의약품을 대상으로 하며, 인슐린 시장의 집중적인 성장을 기대하고 있습니다. 데이터 플랫폼이 자체 개발한 펜형 인슐린 주사기와 자사 브랜드 CGM을 결합함으로써 벤더 종속성이 강화되고, 환자의 전환 비용이 증가하며, 제조업체 시장 점유율이 공고해지고 있습니다.

지역별 분석

북미는 2025년 기초 인슐린 시장 규모의 43.89%를 차지했으나, 메디케어의 본인부담 상한액에 힘입은 반면, GLP-1 제제로의 급속한 전환과 바이오시밀러로 인한 가격 압박으로 인해 성장에 제약을 받았습니다. 2027년 이후, 연방 정부의 가격 협상을 통해 세마글루티드의 가격이 대폭 인하됨에 따라, 인슐린이 처방 목록에서 더욱 제외될 가능성이 높습니다. 생산 능력 확대를 위해 노보가 노스캐롤라이나주에 41억 달러 규모로 건설한 충전 및 마무리 공장과 릴리가 위스콘신주에 30억 달러 규모로 건설한 거점은 인슐린 및 인크레틴 제제 포트폴리오 전체에 대한 수요를 충족시키고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 6.32%를 기록하며 모든 지역을 앞지를 것으로 전망됩니다. 2026년 3월 인도에서 세마글루타이드의 특허가 만료됨에 따라 50종 이상의 브랜드 제네릭 의약품이 쏟아져 나오면서, GLP-1의 가격을 압박하는 동시에 치료 순서를 재편하게 되었습니다. 중국의 규제 개혁에 따라 현지 바이오시밀러 승인이 가속화되고 있습니다. 시칸제약의 데글루덱 허가 신청은 다국적 기업에 맞서 국내 기업이 직면한 과제를 여실히 드러내고 있습니다. 각 제조업체는 ‘현지 생산·현지 공급’을 통한 공급 확보와 관세상의 우위를 확보하기 위해 지역 공장에 20억 달러 이상을 투자하고 있습니다.

유럽 및 중동 및 아프리카에서는 한 자릿수 중반대의 성장이 예상됩니다. 엄격한 상호 대체성에 관한 규제가 바이오시밀러의 보급을 저해하고 있는 반면, 불균일한 보험급여 제도가 신약 시장 진입을 가로막고 있습니다. 사노피가 추진하는 13억 유로 규모의 프랑크푸르트 거점 확장 사업(2029년 완공 예정)은 란타스와 투조의 바이오시밀러가 보급될 때 지역 수요를 뒷받침하기 위한 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the basal insulin market size is expected to increase from USD 7.40 billion in 2025 to USD 7.70 billion in 2026 and reach USD 9.80 billion by 2031, growing at a CAGR of 4.85% over 2026-2031.

This report is Segmented by Molecule (Glargine, Detemir, Degludec, Others), Delivery Device (Vials & Syringes, Pre-Filled Disposable Pens, and More), Patient Type (Type-1 Diabetes, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Basal Insulin Market Trends and Insights

Rising Global Diabetes Prevalence

According to NCD Alliance over one in nine adults worldwide now live with diabetes, with projections indicating a rise to 853 million by 2045. Low- and middle-income nations now account for most new diagnoses, but therapeutic access lags epidemiologic need. Aggressive local-pricing strategies such as Novo Nordisk's USD 24-per-week Ozempic launch in India in December 2025 unlock volume yet compress margins. In the United States, the CDC estimates 38 million people have diabetes; A modest share of Medicare beneficiaries gained GLP-1 coverage under 2026 pilots, redirecting many prospective insulin starts to incretin therapy. The basal insulin market therefore expands in absolute terms while facing a shrinking eligible numerator as treatment algorithms evolve.

Adoption of Long-Acting Insulin Analogues

Glargine, degludec, and detemir displaced NPH insulin on safety grounds, but biosimilar competition now erodes the analogue premium. Semglee launched at 64% below Lantus list price and delivered equivalent glycemic control in real-world evidence from UC Health . Sanofi's Merilog became the first rapid-acting biosimilar approved in the United States in February 2026, establishing precedent that accelerates basal-analogue follow-ons. Updated 2026 Diabetes Canada guidelines caution about hypoglycemia risk for icodec in type-1 diabetes, indicating analogue uptake will plateau in developed markets but rise in emerging regions where biosimilars bridge affordability gaps.

GLP-1 Uptake Delaying Basal Starts

SURPASS-4 showed tirzepatide reduced insulin initiation by 71% versus glargine, pushing basal insulin deeper into treatment lines . SUSTAIN-4 and subsequent trials confirm semaglutide's dual benefit of HbA1c lowering and 10-15% body-weight reduction, making GLP-1s the preferred injectable for type-2 diabetes. Oral formulations-Novo's semaglutide (approved December 2025) and Lilly's orforglipron (approved April 2026) at USD 149 per month-remove injection barriers and equalize cost with basal insulin starter packs. Medicare's negotiated USD 274 monthly semaglutide price effective 2027 cements payer bias toward GLP-1s, compressing basal starts in developed markets.

Other drivers and restraints analyzed in the detailed report include:

- Once-Weekly Basal Insulin Pipeline Momentum

- Integration with CGM-Enabled Smart Pens

- High Analogue Pricing & Reimbursement Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Detemir is projected to grow at a 5.67% CAGR through 2031, the fastest rate among basal insulin molecules. Three factors explain the rebound. First, emerging-market biosimilars launch at prices significantly below branded analogues, making twice-daily detemir attractive where drug budgets are tight. Second, payers in cost-sensitive regions steer formularies toward these lower-priced options rather than premium once-daily products. Third, clinicians see value in detemir's weight-neutral profile for obese type-2 patients who cannot afford GLP-1 combinations.

Glargine still led with 45.67% of molecule share in 2025, supported by Sanofi's Lantus and Toujeo, but biosimilars such as Semglee and Rezvoglar are eroding that position with price discounts. Degludec, marketed as Tresiba, retains a dosing-flexibility edge yet faces U.S. price pressure and biosimilar competition that limits its growth to low-single digits. The Others group-once-weekly icodec and Lilly's pipeline efsitora alfa-secured a toehold after Awiqli won FDA approval in March 2026 for type-2 diabetes, though exclusion from type-1 indications confines uptake to majority of insulin users.

Pre-filled pens led with 58.34% share in 2025; however, reusable and smart pens outpace overall basal insulin market growth at 6.12% CAGR through 2031. The basal insulin market share commanded by traditional vials has fallen in North America, whereas India and sub-Saharan Africa still rely on them for significant portion of doses. Smart-pen-CGM bundles are rapidly gaining preferred-drug-list placement among U.S. payers following ADA guideline changes. Insulet's Omnipod GO basal-only tubeless pump-positioned between pens and full-loop pumps-could capture notable share by 2030.

Ypsomed-BD autoinjector development targets high-viscosity biologics, anticipating concentrated insulin growth. Vendor lock-in strengthens as data platforms pair proprietary pens with branded CGMs, raising patient switching costs and reinforcing manufacturer share.

Geography Analysis

North America retained 43.89% of basal insulin market size in 2025, buoyed by Medicare copay caps but constrained by rapid GLP-1 substitution and biosimilar price pressure. Federal negotiation reducing semaglutide pricing significantly from 2027 will likely further shift formularies away from insulin. Capacity expansions Novo's USD 4.1 billion North Carolina fill-finish plant and Lilly's USD 3 billion Wisconsin site-hedge demand across insulin and incretin portfolios.

Asia-Pacific is projected to grow at a 6.32% CAGR, outpacing all regions. India's March 2026 semaglutide patent lapse opened a flood of more than 50 branded generics, compressing GLP-1 prices and reshaping therapeutic sequencing. China's regulatory reforms accelerate local biosimilar approvals; Sihuan's degludec filing underlines domestic challengers to multinationals. Manufacturers invest more than USD 2 billion in regional plants to secure "local-for-local" supply and tariff advantages.

Europe and Middle East & Africa register mid-single-digit growth. Stringent interchangeability rules slow biosimilar penetration, while heterogeneous reimbursement frameworks fragment market access for novel formulations. Sanofi's EUR 1.3 billion Frankfurt expansion (completion 2029) aims to support regional demand once Lantus and Toujeo biosimilars proliferate.

- Biocon Biologics Ltd

- Biosidus S.A.

- Bioton

- Eli Lilly and Company

- Emcure Pharmaceuticals

- Gan & Lee Pharmaceuticals

- Gedeon Richter Plc

- Geropharm

- Lupin

- Novo Nordisk

- Pfizer

- Sanofi

- SEDICO Pharmaceutical Co.

- Tonghua Dongbao

- Viatris

- Wanbang Biopharma

- Wockhardt

- Zhuhai United Laboratories

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Diabetes Prevalence

- 4.2.2 Biosimilar Insulin Market Expansion

- 4.2.3 Adoption of Long-Acting Insulin Analogues

- 4.2.4 Once-Weekly Basal Insulin Pipeline Momentum

- 4.2.5 Shift From Vials to Pre-Filled Pens

- 4.2.6 Integration With CGM-Enabled Smart Pens

- 4.3 Market Restraints

- 4.3.1 High Analogue Pricing & Reimbursement Gaps

- 4.3.2 Regulatory Complexity for Biosimilars

- 4.3.3 GLP-1 Uptake Delaying Basal Starts

- 4.3.4 Manufacturing Scale-Up Bottlenecks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Molecule

- 5.1.1 Glargine

- 5.1.2 Detemir

- 5.1.3 Degludec

- 5.1.4 Others

- 5.2 By Delivery Device

- 5.2.1 Vials & Syringes

- 5.2.2 Pre-filled Disposable Pens

- 5.2.3 Re-usable / Smart Pens

- 5.2.4 Pump-based Basal Delivery

- 5.3 By Patient Type

- 5.3.1 Type-1 Diabetes

- 5.3.2 Type-2 Diabetes

- 5.3.3 Gestational Diabetes

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Biocon Biologics Ltd

- 6.3.2 Biosidus S.A.

- 6.3.3 Bioton S.A.

- 6.3.4 Eli Lilly and Company

- 6.3.5 Emcure Pharmaceuticals Ltd.

- 6.3.6 Gan & Lee Pharmaceuticals

- 6.3.7 Gedeon Richter Plc

- 6.3.8 Geropharm

- 6.3.9 Lupin Limited

- 6.3.10 Novo Nordisk A/S

- 6.3.11 Pfizer Inc.

- 6.3.12 Sanofi S.A.

- 6.3.13 SEDICO Pharmaceutical Co.

- 6.3.14 Tonghua Dongbao

- 6.3.15 Viatris Inc.

- 6.3.16 Wanbang Biopharma

- 6.3.17 Wockhardt Ltd

- 6.3.18 Zhuhai United Laboratories Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment