|

시장보고서

상품코드

2063426

적외선 LED 칩 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Infrared (IR) LED Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

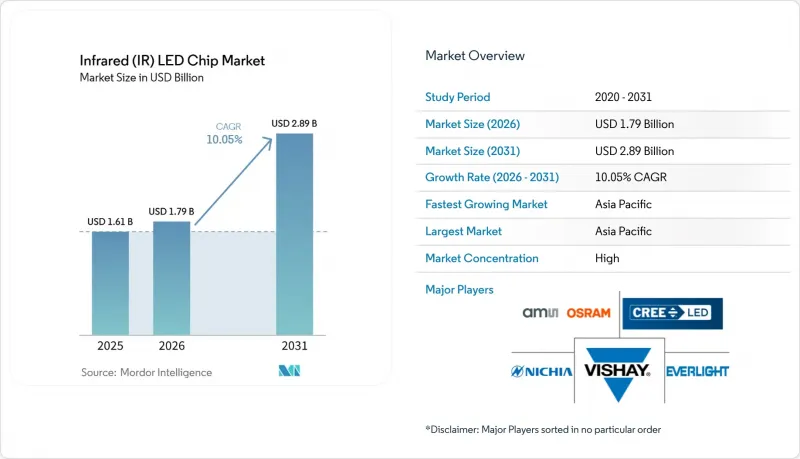

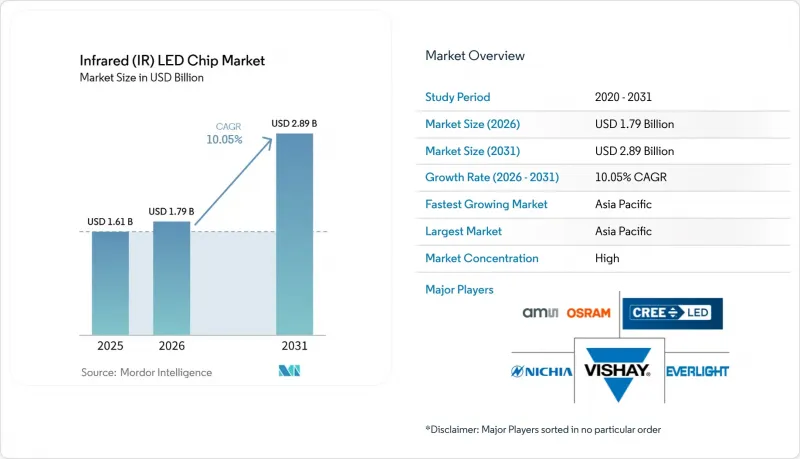

Mordor Intelligence에 의하면, 적외선 LED 칩 시장 규모는 2025년 16억 1,000만 달러로 평가되었습니다. 2026년 17억 9,000만 달러로 확대되어 2031년까지 28억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 10.1%를 나타낼 전망입니다.

본 보고서는 파장 범위(근적외선, 단파장 적외선 및 확장 적외선), 출력(저출력, 중출력 및 고출력), 용도(소비자용 전자기기, 자동차, 산업용 및 머신 비전, 보안 및 감시, 헬스케어 및 의료) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 적외선 LED 칩 시장 동향 및 분석

소비자용 전자기기에서의 채택 확대

각 스마트폰 제조업체들은 OLED 디스플레이 뒷면에 적외선 방출기를 재배치하여 화면 하단 얼굴 인식을 구현하고 있습니다. 이러한 설계 변경으로 인해, 흡수 스택 층을 통과하여 높은 복사 플럭스를 공급하는 소형 칩이 유리해집니다. 휴대폰, 태블릿, 스마트 스피커, 증강현실(AR) 헤드셋 외에도 제스처 인식 및 깊이 매핑을 위해 850나노미터 어레이가 탑재되어 있습니다. 소비자용 웨어러블 기기 분야에서는 830-850나노미터 파장의 LED를 이용해 콜라겐을 자극하는 FDA 승인 치료용 마스크가 보급되면서, 이에 따라 총 잠재 시장(TAM)이 확대되고 있습니다. 미용·웰니스 분야로의 다각화는 주기적인 스마트폰 교체에 대한 의존도를 낮추는 동시에, 소형 고효율 칩에 대한 지속적인 수요를 뒷받침하고 있습니다. 그 결과, 기기 제조업체들이 생체 인식의 정확도를 유지하기 위해 더 얇은 패키지와 더 좁은 파장 대역을 요구함에 따라, 적외선 LED 칩 시장에 안정적인 수요가 발생하고 있습니다.

자동차용 운전자 모니터링 및 ADAS 시스템의 확대

Euro NCAP의 2026년 평가 기준에 따르면, 시선 추적을 통한 운전자 모니터링 항목에 최대 25점의 안전 평가 점수가 부여되며, 사실상 승용차에 근적외선 조명이 필수적으로 적용되어야 합니다. 미국과 중국의 규제 당국도 유사한 규정을 마련하고 있어, -40°C에서 125°C 범위에서 파장 안정성을 유지하는 AEC-Q102 인증 이미터에 대한 전 세계적인 수요가 동시에 증가하고 있습니다. 이에 대응하여 공급업체는 피크 광출력을 향상시키면서 소비 전류와 발열을 줄인 5접합 레이저 다이오드를 적용하고 있으며, 이를 통해 LiDAR 모듈은 200미터를 넘는 거리의 물체를 감지할 수 있게 됩니다. Tier 1 통합업체들은 대량 생산을 위한 인증 절차를 시작했으며, 주요 파운드리 업체들 시장 점유율을 확보하기 위해 다년간공급 계약을 체결하고 있습니다. 이러한 요건들은 도입을 가속화하고 있으며, 안전 전자기기 로드맵에서 적외선 LED 칩 시장이 차지하는 매우 중요한 역할을 강화하고 있습니다.

치열한 경쟁이 이익률을 압박하고 있습니다.

중국 제조업체들은 원자재 가격 급등을 상쇄하기 위해 2025년에 평균 판매 가격을 5-10% 인상했으나, 전 세계 LED 패키징 매출액은 여전히 4% 감소한 것으로 나타나 범용 등급 제품공급 과잉을 시사하고 있습니다. 수직 통합은 부분적인 보호 효과를 가져오고 있으며, 대만과 유럽의 기존 기업들은 가격 경쟁을 피하기 위해 마이크로 LED와 레이저 아키텍처에 주력하고 있습니다. 산안광전(Sanan)의 루미레즈(Lumileds) 인수가 진행 중이며, 이로 인해 비용 시너지가 발생해 유럽 자동차용 LED 가격에 압박을 가할 가능성이 있습니다. 독자적인 지적재산권을 보유하지 않은 중소 공급업체들은 이익률 압박과 시장 철수 위기에 직면해 있으며, 이러한 추세로 인해 적외선 LED 칩 업계 전반에서 업계 재편 움직임이 활발해지고 있습니다.

부문별 분석

850-950나노미터의 근적외선 대역은 2025년 적외선 LED 칩 시장 매출의 절반 이상을 차지했으며, 이는 저비용 실리콘 광검출기와의 원활한 결합은 물론, 스마트폰, 자동차 운전자 모니터링, 방범 카메라 분야에서 확고한 입지를 반영한 것입니다. 1,000-1,700나노미터 파장대를 가진 단파장 적외선 장치는 식품 가공업체와 재활용 업체가 가시광선 시스템으로는 식별할 수 없는 폴리머나 수분 함량을 파악하는 하이퍼스펙트럼 선별기를 도입함에 따라, 2031년까지 연평균 10.68%라는 가장 높은 성장률을 나타낼 것으로 전망됩니다.

Cimbria사의 SEA.HY 선별기와 Imec사의 스냅샷 이미저를 통해, 정밀한 파장 제어가 실시간 가공 라인에서 분류 정확도를 얼마나 향상시키는지 입증하고 있습니다. 유럽연합(EU)의 재활용 의무와 북미의 식품 안전 규제가 수요를 견인하는 요인이 되어, 스펙트럼 범위가 더 좁은 칩의 가격 상승을 뒷받침하고 있습니다. 1,700나노미터를 초과하는 장파장 적외선 솔루션은 항공우주 분야에 적용되고 있으나, 인듐-갈륨-비소(IGAr) 검출기의 높은 비용이 판매량을 제한하고 있습니다. 에피 웨이퍼의 균일성과 패키징용 방열판에 대한 지속적인 기술 혁신을 통해, 광범위한 적외선 LED 칩 시장에서 단파장 솔루션의 가치 제안이 강화되고 있습니다.

지역별 분석

아시아태평양은 2025년 적외선 LED 칩 시장 매출의 49.53%를 차지했으며, 중국, 대만, 한국의 업체들이 에피택시 및 패키징 생산 능력을 확대하고 있는 만큼 연평균 성장률(CAGR) 11.22%를 기록할 전망입니다. Sanan Optoelectronics는 2025년 상반기에 89억 8,700만 위안(12억 4,000만 달러)의 매출을 기록하여 17.03% 증가했습니다. 이는 고급 자동차 및 소비자용 부문으로의 진출이 확대되었음을 반영하고 있습니다. 대만의 Ennostar는 상품화(commoditization)로 인한 가격 하락을 피하기 위해 마이크로 LED 및 수직 공진기 면발광 레이저(VCSEL)로의 전환을 추진하고 있는 반면, 일본공급업체들은 자동차 품질 기준을 충족하는 개별 전력 소자에 주력하고 있습니다. 지역 산업단지 내에서의 수직 통합을 통해 사이클 타임이 단축되어, 적외선 LED 칩 시장의 경쟁력 있는 원가 구조를 뒷받침하고 있습니다.

북미와 유럽에서의 진전은 완만하지만, 자동차 인증 및 국방 프로그램에서 매우 중요한 역할을 하고 있습니다. ams OSRAM은 오스트리아에 14억 유로(15억 8,000만 달러) 규모의 백엔드 시설을 건설하기 위해 EU로부터 2억 2,700만 유로(2억 5,600만 달러)의 자금을 조달하는 데 성공했습니다. 이는 아시아공급 리스크에 대한 전략적 헤지 수단이 됩니다. ams OSRAM과 니치아(Nichia) 간의 특허 교차 라이선싱을 통해 소송으로 인한 혼란이 해소되었으며, 차세대 이미터에 대한 투자가 촉진되고 있습니다. 이 지역들은 광생물학적 안전성 및 전자기 호환성에 관한 적합성 시험의 거점이기도 하여, 전 세계 자동차 제조업체 및 의료기기 제조업체들이 자사 제품에 이를 설계에 채택하도록 확실히 뒷받침하고 있습니다.

남미, 중동 및 아프리카 시장 점유율은 작지만, 야간 감시나 교통 분석이 필요한 인프라 프로젝트의 혜택을 받고 있습니다. 중동에서는 중요 자산의 보호가 최우선으로 여겨지고 있어, 940나노미터 파장의 은폐형 카메라의 대규모 도입이 추진되고 있습니다. 유럽의 개인정보 보호 관련 법규로 인해 생체 인증 기술 도입이 지연될 가능성은 있지만, 세분화된 규제를 잘 헤쳐 나가는 공급업체들은 지리적으로 균형 잡힌 성장을 실현하고 있습니다. 그 결과, 지역별 동향에 따라 적외선 LED 칩 시장에서 아시아태평양이 공급 측면에서 우위를 유지하는 한편, 다른 지역에서도 프리미엄 틈새 시장이 유지되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the infrared (IR) LED chip market size is expected to increase from USD 1.61 billion in 2025 to USD 1.79 billion in 2026 and reach USD 2.89 billion by 2031, growing at a CAGR of 10.1% over 2026-2031.

This report is Segmented by Wavelength Range (Near Infrared, Short-Wave Infrared, and Extended Infrared), Power Output (Low Power, Medium Power, and High Power), Application (Consumer Electronics, Automotive, Industrial and Machine Vision, Security and Surveillance, and Healthcare and Medical), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Infrared (IR) LED Chip Market Trends and Insights

Rising Adoption In Consumer Electronics

Smartphone makers are repositioning infrared emitters behind organic light-emitting diode displays to enable under-screen facial recognition, a redesign that favors miniaturized chips that deliver high radiant flux through absorptive stack layers. Beyond handsets, tablets, smart speakers, and augmented-reality headsets, 850-nanometer arrays are embedded for gesture recognition and depth mapping. Consumer wearables benefit from FDA-cleared therapy masks that use 830-850-nanometer LEDs to stimulate collagen, widening the total addressable market. Diversification into beauty and wellness reduces dependence on cyclical phone refreshes and supports recurring demand for compact, high-efficiency chips. The result is steady pull-through for the infrared LED chip market as device makers seek thinner packages and tighter wavelength bins to maintain biometric accuracy.

Expansion Of Automotive Driver Monitoring And ADAS Systems

Euro NCAP's 2026 protocol awards up to 25 safety points for eye-tracking driver monitoring, effectively making near-infrared illumination mandatory in passenger cars. U.S. and Chinese regulators are drafting similar language, synchronizing global demand for AEC-Q102 qualified emitters that remain wavelength-stable from -40 °C to 125 °C. Suppliers respond with five-junction laser diodes that lift peak optical power while easing current draw and heat generation, enabling LiDAR modules to detect objects beyond 200 meters. Tier-one integrators have begun high-volume qualification, anchoring multiyear supply agreements that lock in share for leading foundries. These mandates accelerate adoption curves and reinforce the pivotal role of the infrared LED chip market in the safety electronics roadmap.

Intense Price Competition Compressing Margins

Chinese producers lifted average selling prices 5-10% in 2025 to offset raw material inflation, yet global LED packaging revenue still slipped 4%, signaling oversupply in commodity grades. Vertical integration offers partial insulation, with Taiwanese and European incumbents focusing on microLED and laser architectures to escape price wars. Sanan's pending acquisition of Lumileds adds cost synergy that could pressure European automotive LED pricing. Smaller suppliers without differentiated intellectual property face margin squeeze and potential exit, a dynamic that keeps consolidation high throughout the infrared LED chip industry.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand For Night-Vision Security And Surveillance Cameras

- Increasing Use In Healthcare Diagnostics And Wearable Devices

- Supply-Chain Vulnerability To Gallium And Arsenic Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The near-infrared band between 850-950 nanometers accounted for more than half of the infrared (IR) LED chip market 2025 revenue, reflecting its seamless pairing with low-cost silicon photodetectors and entrenched position in smartphones, automotive driver monitoring, and security cameras. Short-wave infrared devices spanning 1,000-1,700 nanometers are projected to register the fastest growth at 10.68% annually through 2031 as food processors and recyclers adopt hyperspectral sorters that identify polymers and moisture levels invisible to visible-light systems.

Cimbria's SEA.HY sorter and Imec's snapshot imager demonstrate how precise wavelength control improves classification accuracy in real-time processing lines. European Union recycling mandates and North American food-safety regulations act as pull factors, supporting premium pricing for chips with tighter spectral bins. Although extended-infrared solutions beyond 1,700 nanometers cater to aerospace, the higher cost of indium gallium arsenide detectors constrains volume. Continuous innovation in epi-wafer uniformity and packaging heatsinks strengthens the value proposition of short-wave solutions within the broader infrared (IR) LED chip market.

Geography Analysis

Asia-Pacific generated 49.53% of the infrared (IR) LED chip market's 2025 revenue and is on track for an 11.22% CAGR as Chinese, Taiwanese, and South Korean vendors expand epitaxial and packaging capacity. Sanan Optoelectronics posted RMB 8.987 billion (USD 1.24 billion) first-half-2025 revenue, up 17.03%, reflecting deeper penetration into premium automotive and consumer segments. Taiwan's Ennostar shifts toward microLED and vertical-cavity surface-emitting lasers to escape commodity pricing, while Japanese suppliers focus on discrete power devices supporting automotive quality standards. Vertical integration within regional industrial parks compresses cycle times and underpins the infrared LED chip market's competitive cost base.

North America and Europe advance more slowly but play a pivotal role in automotive qualification and defense programs. ams OSRAM secured EUR 227 million (USD 256 million) of EU funding to build a EUR 1.4 billion (USD 1.58 billion) back-end facility in Austria, a strategic hedge against Asian supply risk. Patent cross-licensing between ams OSRAM and Nichia resolves litigation distraction and channels investment into next-generation emitters. These regions also anchor compliance testing for photobiological safety and electromagnetic compatibility, locking in design-wins from global carmakers and medical device firms.

South America, the Middle East, and Africa hold smaller shares but benefit from infrastructure projects that require night-vision surveillance and traffic analytics. The Middle East prioritizes critical-asset protection, supporting large-scale deployments of covert 940 nanometer cameras. European privacy legislation may slow biometric roll-outs, but suppliers able to navigate fragmented regulations capture geographically balanced growth. Consequently, regional dynamics preserve Asia-Pacific's supply dominance while sustaining premium niches elsewhere within the infrared LED chip market.

- ams OSRAM AG

- Nichia Corporation

- Everlight Electronics Co., Ltd.

- Cree LED

- Vishay Intertechnology, Inc.

- Epistar Corporation

- Lite-On Technology Corporation

- Lextar Electronics Corporation

- Kingbright Company, LLC

- Lumileds Holding B.V.

- High Power Lighting Corporation

- EPILEDS Technologies Inc.

- ROHM Co., Ltd.

- ON Semiconductor Corporation

- Ushio Inc.

- Marktech Optoelectronics

- Excelitas Technologies Corp.

- Toyoda Gosei Co., Ltd.

- Samsung Electronics Co., Ltd.

- Stanley Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption in Consumer Electronics

- 4.2.2 Growing Demand for Night-Vision Security and Surveillance Cameras

- 4.2.3 Expansion of Automotive Driver Monitoring and ADAS Systems

- 4.2.4 Increasing Use in Healthcare Diagnostics and Wearable Devices

- 4.2.5 Integration with SWIR Hyperspectral Imaging for Food and Recycling Sorting

- 4.2.6 Contactless Smart-Retail Shelves Using Low-Power IR LED Arrays

- 4.3 Market Restraints

- 4.3.1 Intense Price Competition Compressing Margins

- 4.3.2 Thermal Management Challenges at High Radiant Flux

- 4.3.3 Supply-Chain Vulnerability to Gallium and Arsenic Restrictions

- 4.3.4 Privacy Concerns Limiting Large-Scale Biometric Deployments

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wavelength Range

- 5.1.1 Near Infrared

- 5.1.2 Short-Wave Infrared

- 5.1.3 Extended Infrared

- 5.2 By Power Output

- 5.2.1 Low Power

- 5.2.2 Medium Power

- 5.2.3 High Power

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Industrial and Machine Vision

- 5.3.4 Security and Surveillance

- 5.3.5 Healthcare and Medical

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 India

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Nichia Corporation

- 6.4.3 Everlight Electronics Co., Ltd.

- 6.4.4 Cree LED

- 6.4.5 Vishay Intertechnology, Inc.

- 6.4.6 Epistar Corporation

- 6.4.7 Lite-On Technology Corporation

- 6.4.8 Lextar Electronics Corporation

- 6.4.9 Kingbright Company, LLC

- 6.4.10 Lumileds Holding B.V.

- 6.4.11 High Power Lighting Corporation

- 6.4.12 EPILEDS Technologies Inc.

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 ON Semiconductor Corporation

- 6.4.15 Ushio Inc.

- 6.4.16 Marktech Optoelectronics

- 6.4.17 Excelitas Technologies Corp.

- 6.4.18 Toyoda Gosei Co., Ltd.

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 Stanley Electric Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment