|

시장보고서

상품코드

2063433

자율적 수요 감지 및 인지적 예측 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Autonomous Demand Sensing And Cognitive Forecasting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

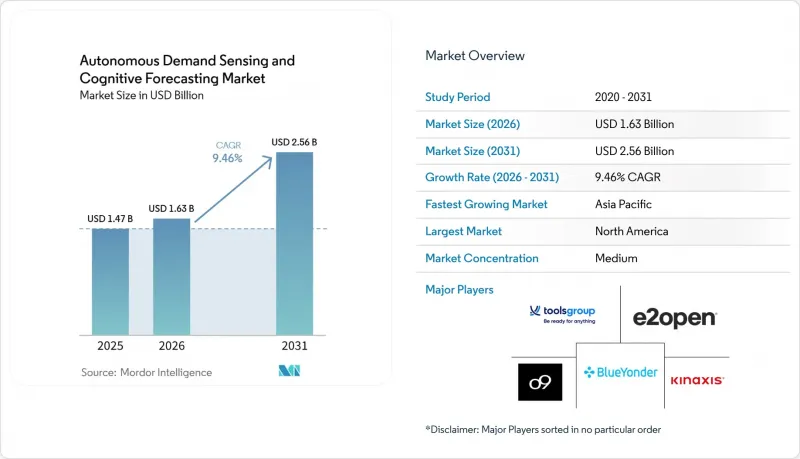

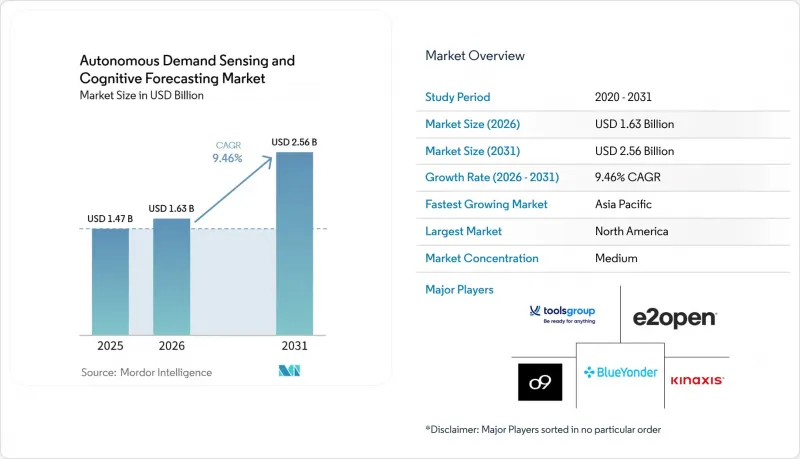

Mordor Intelligence에 의하면, 자율적 수요 감지 및 인지적 예측 시장 규모는 2025년 14억 7,000만 달러로 평가되었습니다. 2026년 16억 3,000만 달러로 확대되어 2031년까지 25억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 9.46%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 방식(클라우드, On-Premise, 하이브리드), 최종 사용자 산업(소비재, 소매 및 전자상거래, 자동차 및 운송 등), 예측 기법(머신러닝 기반 예측 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 자율적 수요 감지 및 인지적 예측 시장 동향과 인사이트

POS 및 전자상거래 채널을 통한 AI 기반 실시간 수요 신호 수집

소매업체와 소비재 브랜드들은 주 단위의 일괄 예측에서 벗어나, 1초 미만의 간격으로 결제 데이터, 클릭 스트림, 소셜 미디어 여론을 분석하는 스트리밍 파이프라인으로 전환하고 있습니다. 월마트는 네트워크 전체에 9,000만 개의 IoT 센서를 배치하여 온도, 습도, 위치 데이터를 엣지 디바이스에 집계하고 있습니다. 엣지 디바이스에서는 신호를 정제하고 압축한 후 클라우드 모델로 전송함으로써 지연 시간과 대역폭 비용을 절감하고 있습니다. 이러한 선행 지표를 기상 데이터와 결합한 기업들의 보고에 따르면, 시장 심리가 급격히 상승하거나 지역별 폭염이 수요에 영향을 미칠 때 예측 오차가 15%-25% 감소하고 정확도가 5%-8% 향상된 것으로 나타났습니다. 지속적인 재계산을 통해 계획 주기가월단위에서 시간 단위로 단축되어, 이상 상황이 발생한 순간 계획 담당자가 안전 재고 설정을 조정할 수 있게 됩니다.

클라우드 네이티브형 공급망 플랫폼의 보급 확대

SAP Integrated Business Planning이나 Kinaxis RapidResponse와 같은 클라우드 네이티브 제품군은 2025년에 1,200개 이상의 기업에서 신규 도입 실적을 기록했습니다. 이는 공급망 책임자가 구독형 가격 체계와 유연한 컴퓨팅 환경으로의 전환을 통해 레거시 시스템 업그레이드에 수반되는 위험을 완화했기 때문입니다. 퍼블릭 클라우드의 확장성은 시간당 수천 건의 시나리오를 검증하는 몬테카를로 시뮬레이션을 뒷받침하며, 즉시 사용 가능한 커넥터를 통해 별도의 사용자 정의 코드 없이도 영업, 재무, 물류 시스템에서 데이터를 가져올 수 있습니다. 하이브리드 구성은 개인을 식별할 수 있는 정보를 On-Premise에 보관하면서, 피크 시간대에는 모델 훈련 워크로드를 퍼블릭 리전으로 분산 처리함으로써 유럽 및 중국의 데이터 거주 요건을 충족하고, 도입을 더욱 가속화합니다.

데이터의 사일로화와 마스터 데이터의 낮은 품질

많은 기업에서는 여전히 수요, 제품, 고객 관련 기록이 서로 분리된 ERP(기업 자원 계획), 창고 관리, CRM(고객 관계 관리) 시스템에 분산되어 보관되고 있습니다. SKU 중복, 측정 단위의 불일치, 계층 필드의 누락은 모델의 정확도를 떨어뜨리고 도입 기간을 길어지게 합니다. 중견 기업의 경우 마스터 데이터 통합 프로젝트에 12-18개월이 소요되고, 초기 비용으로 50만-200만 달러가 추가로 드는 경우가 많아, 자율적 수요 감지 및 인지적 예측 기술 시장 도입이 지연되고 있습니다. 합병 및 인수(M&A)는 모델 훈련을 시작하기 전에 인수 측이 서로 다른 스키마를 통합해야 하기 때문에 이 과제를 더욱 복잡하게 만듭니다.

부문별 분석

자율적 수요 감지 및 인지적 예측 시장의 서비스 부문은 기업들이 데이터 정제, 모델 재훈련, 에이전트형 AI 워크플로우 관리를 컨설턴트에 의존하는 경향이 있기 때문에 2031년까지 연평균 성장률(CAGR) 9.86%를 나타낼 것으로 전망됩니다. 소프트웨어 부문은 데이터 수집, 특징량 엔지니어링, 확률적 예측 엔진을 통합한 플랫폼에 대한 라이선스 계약을 반영하여 매출 비중 48.31%를 유지했습니다. 조직들이 예측 정확도가 지속적인 특징량 업데이트, 프롬프트 엔지니어링, 그리고 가드레일 모니터링에 달려 있다는 점을 인식함에 따라, 관리형 서비스에 대한 수요가 증가하고 있습니다. 이러한 업무는 사내 팀에서 처리할 자원이 부족한 경우가 많습니다.

구축 파트너는 패션 소매업을 위한 계절성 곡선이든, 제약 회사를 위한 일련번호 부여 워크플로우이든, 업계 고유의 노하우를 반영하고 있습니다. 또한, On-Premise 마스터 데이터와 퍼블릭 클라우드상의 트레이닝 클러스터를 동기화하는 하이브리드 배포를 조정 중이며, 이는 규제 대상 부문에 있어 필수적인 요건입니다. 이러한 서비스의 성장세는 핵심 플랫폼 주변의 파트너 생태계를 확대시키고 있으며, 2031년까지 공급업체의 수익 구조를 재편할 가능성이 높습니다.

2025년에는 클라우드 구성이 자율적 수요 감지 및 인지적 예측 시장의 56.43%를 차지했습니다. 이는 유연한 컴퓨팅 환경 덕분에 몬테카를로법의 실행과 외부 데이터의 가져오기가 간소화되었기 때문입니다. 하이브리드 구성은 연평균 성장률(CAGR) 10.06%로 성장을 지속하고, 있으며, 이는 도입 방식 중 가장 높은 성장률입니다. 이는 유럽 및 중국의 데이터 소재지 관련 법규에 따라 기밀 데이터는 로컬 서버에 보관해야 하는 의무가 있는 반면, 익명화된 집계 데이터에 대해서는 클라우드의 훈련 노드로 전송하는 것이 허용되기 때문입니다. Kubernetes를 중심으로 한 오케스트레이션을 통해 워크로드 배치가 추상화되므로, 데이터 사이언스자는 로컬에서 프로토타입을 제작한 후 코드를 수정하지 않고도 모델을 프로덕션 클러스터에 배포할 수 있습니다.

하이브리드 도입은 단계적이고 체계적인 전환 과정도 지원합니다. 조직은 일반적으로 수요 예측 워크로드를 새로운 시스템으로 이전하는 것부터 시작하여, 초기 변경 사항이 관리 가능하고 위험이 낮도록 보장합니다. 이 단계가 성공적으로 완료되면, 공급 계획, 네트워크 설계 및 통합 사업 계획 모듈로의 전환 단계로 넘어갑니다. 이러한 단계적 접근 방식을 통해 대규모 변화에 수반되는 위험을 최소화하고, 각 단계에서 점진적인 가치를 실현할 수 있게 됩니다. 또한, 전환 기간 동안에도 미션 크리티컬한 On-Premise 시스템이 계속 가동되어 영향을 받지 않도록 보장하며, 원활하고 효율적인 전환 경험을 제공합니다.

지역별 분석

2025년, 북미는 전 세계 매출의 34.74%를 차지했습니다. 이는 팬데믹 회복기에 포춘 500에 선정된 소매업체, 자동차 OEM 및 소비재 대기업들이 엔터프라이즈 스위트에 수요 예측 엔진을 통합한 것이 뒷받침된 결과입니다. 이 지역은 성숙한 클라우드 스택과 풍부한 데이터 사이언스 인재 풀을 강점으로 삼고 있습니다. 연방 정부의 식품 안전 및 의약품 추적성에 관한 법률이 지속적인 모니터링을 촉진하는 한편, 니어쇼어링 추세가 멕시코 시설과의 국경을 초월한 협력을 뒷받침하고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 10.67%를 나타낼 것으로 예측되며, 이는 세계 최고 수준입니다. 중국의 크로스보더 전자상거래 급증, 인도의 지방 도시에서의 디지털화, 그리고 일본의 노동력 고령화에 따른 자동화의 필요성이 지출의 기반이 되고 있습니다. 2026년에 개정된 중국의 데이터 전송 지침에서는 익명화된 집계 데이터는 분석 목적으로 해외로 전송할 수 있음이 명확히 규정되어, 하이브리드 방식의 도입을 촉진하고 있습니다. 인도에서는 퍼블릭 클라우드 가격 하락과 정부의 AI 로드맵이 소매업 및 제조업 분야의 도입을 촉진하고 있습니다. 한국, 호주, 아세안 국가들도 비슷한 궤적을 밟고 있지만, 그 기반은 더 소규모입니다.

나머지 수익은 유럽, 중동 및 아프리카, 그리고 남미가 차지하고 있습니다. 유럽의 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))으로 인해 프로젝트 리드타임이 길어지고 있지만, 해당 지역의 선진적인 산업 기반이 지속가능성 및 폐기물 감축 분야의 활용 사례를 주도하고 있습니다. 아랍에미리트(UAE)와 사우디아라비아가 주도하는 중동에서는 수요 예측과 도시 물류를 통합한 스마트시티 시범 사업에 자금이 투입되고 있습니다. 남미에서는 전자상거래의 가속화로 인해 마켓플레이스들이 물류 거점 최적화를 추진하고 있지만, 거시경제의 변동으로 인해 브라질과 아르헨티나를 제외한 지역에서는 지출이 억제되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the autonomous demand sensing and cognitive forecasting market size is expected to increase from USD 1.47 billion in 2025 to USD 1.63 billion in 2026 and reach USD 2.56 billion by 2031, growing at a CAGR of 9.46% over 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), End-User Industry (Consumer Packaged Goods, Retail and E-Commerce, Automotive and Transportation, and More), Forecasting Technique (Machine Learning Based Forecasting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Autonomous Demand Sensing And Cognitive Forecasting Market Trends and Insights

AI-Based Real-Time Demand Signal Capture from POS and E-Commerce Channels

Retailers and consumer packaged goods brands have upgraded from weekly batch forecasts to streaming pipelines that parse checkout, clickstream, and social media sentiment at sub-second intervals. Walmart's roll-out of 90 million IoT sensors across its network funnels temperature, humidity, and position data into edge devices that cleanse and compress signals before dispatching them to cloud models, cutting latency and bandwidth costs. Enterprises that combine these leading indicators with weather data report 15%-25% lower forecast error and 5%-8% additional accuracy when sentiment spikes or regional heatwaves influence demand. Continuous recalculation narrows planning cycles from monthly to hourly, letting planners adjust safety-stock settings the moment anomalies surface.

Rising Adoption of Cloud-Native Supply-Chain Platforms

Cloud-native suites such as SAP Integrated Business Planning and Kinaxis RapidResponse attracted more than 1,200 new logos in 2025 as supply chain chiefs de-risked legacy upgrades by moving to subscription pricing and elastic compute. Public-cloud scalability underpins Monte Carlo simulations that test thousands of scenarios per hour, while out-of-the-box connectors pull data from sales, finance, and logistics systems without custom code. Hybrid topologies further accelerate adoption by keeping personally identifiable information on-premise while bursting model-training workloads to public regions during peak cycles, satisfying European and Chinese data-residency rules.

Data Silos and Poor Master-Data Quality

Many enterprises still house demand, product, and customer records in isolated enterprise resource planning, warehouse management, and customer relationship management systems. Duplicate SKUs, inconsistent units of measure, and missing hierarchy fields undermine model accuracy and extend implementation timelines. Mid-sized organizations often face 12- to 18-month master-data harmonization projects that add USD 0.5 million to USD 2 million in up-front cost, delaying autonomous demand sensing and cognitive forecasting market deployments. Mergers and acquisitions compound the challenge as acquirers must reconcile disparate schemas before model training can begin.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Proliferation of IoT Sensors across Logistics Nodes

- Integration of Generative AI for Scenario-Driven Forecasting

- High Total Cost of Ownership for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services segment of the autonomous demand sensing and cognitive forecasting market is projected to grow at a 9.86% CAGR through 2031 as enterprises lean on consultants to clean data, retrain models, and manage agentic AI workflows. The software segment retained a 48.31% revenue share, reflecting license commitments to platforms that bundle data ingestion, feature engineering, and probabilistic forecasting engines. Demand for managed services has intensified as organizations realize that forecast accuracy hinges on continuous feature updates, prompt engineering, and guardrail monitoring that internal teams often lack the bandwidth to perform.

Implementation partners embed industry know-how, whether it is seasonality curves for fashion retailers or serialization workflows for pharmaceutical manufacturers. They also orchestrate hybrid deployments that synchronize on-premise master data with public-cloud training clusters, a prerequisite for regulated sectors. This services momentum is widening partner ecosystems around core platforms and is likely to reshape vendor revenue mixes by 2031.

Cloud configurations accounted for 56.43% of the autonomous demand sensing and cognitive forecasting market share in 2025, as elastic compute simplifies Monte Carlo runs and external data ingestion. Hybrid setups are on track for a 10.06% CAGR, the fastest among deployment modes, as European and Chinese data-residency statutes require sensitive data to remain on local servers while permitting anonymized aggregates to flow to cloud training nodes. Kubernetes-centric orchestration abstracts workload placement, enabling data scientists to prototype locally and deploy models to production clusters without code rewrites.

Hybrid adoption also supports a gradual and systematic migration process. Organizations typically begin by transitioning demand-sensing workloads to the new system, ensuring that initial changes are manageable and low-risk. Once this phase is successfully implemented, they proceed with migrating supply planning, network design, and integrated business-planning modules. This step-by-step approach minimizes the risks associated with large-scale transformations and allows companies to realize incremental value at each stage. Furthermore, it ensures that mission-critical on-premises systems remain operational and unaffected during the transition, providing a seamless, efficient migration experience.

Geography Analysis

North America accounted for 34.74% of global revenue in 2025, buoyed by Fortune 500 retailers, automotive OEMs, and consumer packaged goods giants that embedded demand-sensing engines in enterprise suites during pandemic recovery. The region benefits from mature cloud stacks and an abundant data-science talent pool. Federal food-safety and pharmaceutical traceability laws encourage continuous monitoring, while nearshoring trends drive cross-border synchronization with Mexican facilities.

Asia-Pacific is forecast to post a 10.67% CAGR between 2026 and 2031, the highest worldwide. China's cross-border e-commerce surge, India's tier-2 city digitization, and Japan's aging-workforce automation imperatives underpin spending. Updated 2026 Chinese data-transfer guidelines clarify that anonymized aggregates can be sent out of the country for analysis, catalyzing hybrid adoption. In India, public cloud price drops and government AI roadmaps have driven adoption across retail and manufacturing. South Korea, Australia, and ASEAN countries mirror this trajectory, albeit from smaller bases.

Europe, the Middle East and Africa, and South America share the remaining revenue. Europe's General Data Protection Regulation lengthens project lead times, yet the bloc's advanced industrial base drives sustainability and waste-minimization use cases. The Middle East, led by the United Arab Emirates and Saudi Arabia, funds smart-city pilots that integrate demand sensing with urban logistics. South America's e-commerce accelerationis drivings marketplaces to optimize fulfillment locations, though macroeconomic volatilityis temperings spending outside Brazil and Argentina.

- o9 Solutions Inc.

- Blue Yonder Group Inc.

- Kinaxis Inc.

- E2open Parent Holdings Inc.

- ToolsGroup B.V.

- Anaplan Inc.

- Aera Technology Inc.

- Antuit.ai LLC

- Relex Solutions Oy

- Logility Inc.

- John Galt Solutions Inc.

- Llamasoft Inc.

- Demand Driven Technologies LLC

- Business Forecast Systems Inc. (Forecast Pro)

- Lokad SAS

- GMDH LLC

- Prevedere Inc.

- DataRobot Inc.

- Inform Software

- Solvoyo Cozum Yazilim A.S.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Based Real-Time Demand Signal Capture from POS and E-Commerce Channels

- 4.2.2 Rising Adoption of Cloud-Native Supply-Chain Platforms

- 4.2.3 Rapid Proliferation of IoT Sensors across Logistics Nodes

- 4.2.4 Integration of Generative AI for Scenario-Driven Forecasting

- 4.2.5 Increasing Use of External Data Lakes (Weather Social Mobility)

- 4.2.6 Vendor-Managed Inventory Programs Expanding to Tier-2 Cities

- 4.3 Market Restraints

- 4.3.1 Data Silos and Poor Master-Data Quality

- 4.3.2 High Total Cost of Ownership for SMEs

- 4.3.3 Regulatory Barriers on Cross-Border Data Flow

- 4.3.4 Shortage of Domain-Specific AI Talent

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By End-User Industry

- 5.3.1 Consumer Packaged Goods

- 5.3.2 Retail and E-Commerce

- 5.3.3 Automotive and Transportation

- 5.3.4 Industrial Manufacturing

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Food and Beverage

- 5.3.7 Logistics and Supply Chain

- 5.3.8 Energy and Utilities

- 5.3.9 Other End-User Industries

- 5.4 By Forecasting Technique

- 5.4.1 Machine Learning Based Forecasting

- 5.4.2 Deep Learning Based Forecasting

- 5.4.3 Traditional Statistical Models Enhanced with AI

- 5.4.4 Reinforcement Learning Approaches

- 5.4.5 Hybrid Models

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 o9 Solutions Inc.

- 6.4.2 Blue Yonder Group Inc.

- 6.4.3 Kinaxis Inc.

- 6.4.4 E2open Parent Holdings Inc.

- 6.4.5 ToolsGroup B.V.

- 6.4.6 Anaplan Inc.

- 6.4.7 Aera Technology Inc.

- 6.4.8 Antuit.ai LLC

- 6.4.9 Relex Solutions Oy

- 6.4.10 Logility Inc.

- 6.4.11 John Galt Solutions Inc.

- 6.4.12 Llamasoft Inc.

- 6.4.13 Demand Driven Technologies LLC

- 6.4.14 Business Forecast Systems Inc. (Forecast Pro)

- 6.4.15 Lokad SAS

- 6.4.16 GMDH LLC

- 6.4.17 Prevedere Inc.

- 6.4.18 DataRobot Inc.

- 6.4.19 Inform Software

- 6.4.20 Solvoyo Cozum Yazilim A.S.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment