|

시장보고서

상품코드

2063445

CHO 기반 바이오시밀러 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)CHO-based Biosimilars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

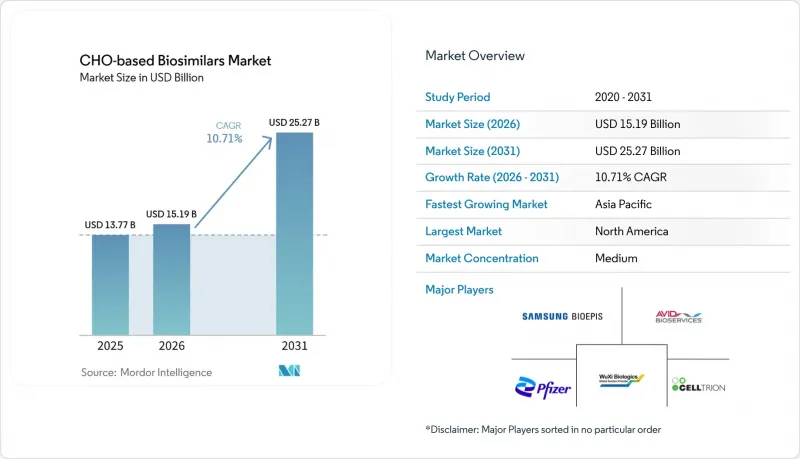

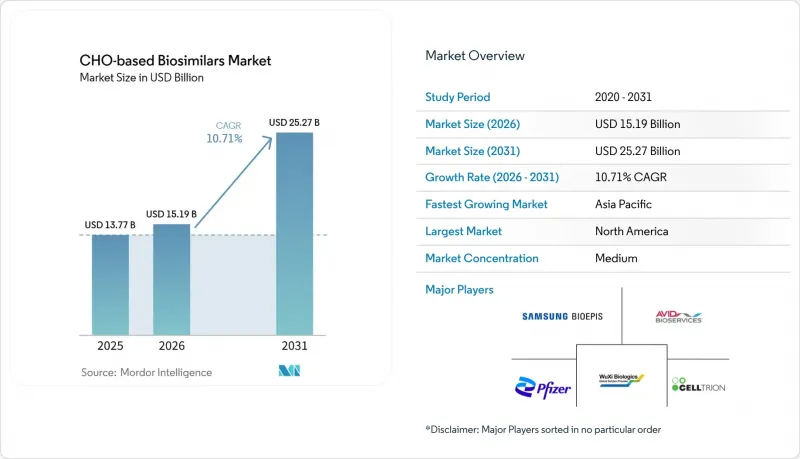

Mordor Intelligence에 의하면, CHO 기반 바이오시밀러 시장 규모는 2025년 137억 7,000만 달러에서 2026년에는 151억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 10.71%로 성장을 지속하여, 2031년까지 252억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 및 서비스(제품(단일클론 항체, Fc 융합 단백질, 당단백질 호르몬, C5 억제제 등), 서비스·플랫폼), 임상 적응증(종양학, 자가면역·염증, 안과, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 CHO 기반 바이오시밀러 시장 동향 및 인사이트

고가치 바이오의약품의 독점권 상실이 가속화되고 있습니다.

연간 매출액이 2,000억-4,000억 달러 규모인 블록버스터 제품들은 2030년까지 특허 보호가 만료될 전망이며, 그중에서도 키트루다, 스텔라라, 데노스맙이 특히 두드러집니다. 이러한 분자 중 상당수는 복잡한 당사슬 구조를 가지고 있어, 고정밀 CHO 플랫폼이 필요합니다. 이는 자본력이 약한 기업에게는 진입 장벽이 되지만, 신속하게 동등성을 입증할 수 있는 선행 기업에게는 유리하게 작용합니다. 출시 후 18개월 동안은 프리미엄 가격을 유지할 수 있는 경우가 많지만, 후발 진출기업들은 이익률의 급격한 하락에 직면하게 됩니다. 이러한 추세에 따라, CHO 기반 바이오시밀러 시장은 규모를 무기로 삼는 기존 기업군과 틈새 시장을 공략하는 전문 기업군으로 양극화가 진행되고 있습니다. 그 결과, 단순히 특허 기간에 맞추어 개발을 진행하는 것뿐만 아니라, 생산 능력 확보와 규제 당국과의 조기 협력이 이제 더욱 결정적인 요소가 되었습니다. 면역학 및 인슐린 분야에서 바이오시밀러의 보급률은 출시 후 5년 이내에 완만한 확산에 그쳤습니다. 이는 종양학이나 안과 분야에서 높은 보급률과 비교했을 때, 외래 진료 현장에서 처방집에 대한 관행이 여전히 뿌리 깊게 자리 잡고 있음을 여실히 보여줍니다. 이러한 양극화는 규제상 상호교환성 인정이 상징적으로는 중요하지만, 지불자가 처방 목록을 재구성하고 단기적인 혼란 비용을 감수하려는 의지에 비하면 그 중요성은 낮음을 시사합니다.

FDA/EMA의 바이오시밀러 승인 절차 효율화

2025년 말까지 FDA는 20개의 참조 물질을 대상으로 한 90개의 바이오시밀러를 승인하여 70%의 상용화율을 달성했습니다. 2025년 9월에 발표된 지침에 따르면, 렉틴 마이크로어레이를 이용한 당사슬 프로파일링이 간소화되어 분석 위험이 대폭 감소했습니다. 유럽에서는 EMA의 상호교환성에 대한 견해 표명이 각국의 대체 정책을 뒷받침하여, 프랑스, 독일, 네덜란드에서의 도입을 가속화했습니다. 요건의 조화를 통해 임상 개발 기간이 단축되었으며, 이는 전 세계적으로 동시에 신청을 진행할 수 있는 풍부한 자원을 보유한 후원사에게 유리하게 작용하고 있습니다. 중소기업들은 지식 격차를 해소하고 포트폴리오 전반에 걸쳐 규정 준수 비용을 분산시키기 위해 CDMO와의 제휴를 점점 더 확대되고 있습니다.

미국의 PBM 리베이트 및 처방약 목록의 동향이 약국 급여 분야에서의 보급을 지연시키고 있습니다.

지불자 컨소시엄 덕분에 종양학 및 안과 분야에서의 도입은 가속화되었으나, 면역학 및 인슐린 분야에서는 순가격의 우위를 훼손하는 뿌리 깊은 리베이트 계약으로 인해, 출시 후 5년이 지났음에도 보급률은 여전히 25%에 그치고 있습니다. 환자 지원 프로그램은 선도 제약사를 더욱 보호하고 있어, 외래 진료 현장에서 CHO 기반 바이오시밀러의 단기적인 성장 여지를 제한하고 있습니다. 규제 당국과 고용주의 지속적인 감시가 PBM에 조정을 요구할 가능성은 있지만, 그 일정은 여전히 불투명합니다.

부문별 분석

이 제품은 2025년 매출의 60.35%를 차지했습니다. 2024년에는 단일클론 항체만으로도 전 세계 매출의 상당 부분을 차지한 반면, Fc 융합 단백질과 당단백질 호르몬은 크게 뒤처졌습니다. 셀트리온과 삼성바이오에피스의 연속 생산 시설은 1그램당 원가를 80달러 미만으로 억제하는 것을 목표로 하고 있으며, 이를 통해 통합형 기업들은 가격 하락에 대비한 체제를 갖추고 있습니다.

신생 바이오테크 기업들이 CDMO에 대한 아웃소싱을 확대함에 따라, 관련 서비스 및 플랫폼 시장은 2031년까지 연평균 성장률(CAGR) 12.65%를 나타낼 것으로 예측됩니다. WuXi Biologics의 UITM 플랫폼은 2,000 L 규모의 GMP 환경에서 18 g/L를 달성했으며, 이는 자산을 최소화한 접근 방식이 소규모 의뢰사가 막대한 설비 투자를 피하는 데 도움이 됨을 보여줍니다. 또한, 이러한 구조를 통해 아시아태평양의 시설로 추가 생산량이 유입됨에 따라, CHO 기반 바이오시밀러 시장에서 해당 지역이 비용 최적화된 제조 거점으로서의 역할이 강화되고 있습니다.

지역별 분석

북미는 2025년에 42.15%의 점유율을 차지했습니다. 이는 90건의 FDA 승인과, 12개월에 걸쳐 휴미라의 바이오시밀러 도입을 대폭 촉진한 보험사의 적극적인 유도책에 힘입은 결과입니다. 포화 상태에 이른 부문에서는 성장이 정체될 것으로 예상되지만, 키트루다 및 기타 항암제의 특허 만료(LoE)가 임박해 있어 새로운 급증을 가져올 것으로 보입니다.

유럽은 절대적인 매출액은 낮지만, 정책 면에서 리더십을 발휘하고 있습니다. 영국, 프랑스, 독일에서는 입찰 제도를 통해 가격 인하가 실현되어, 2020년 이후 의료 제도에서 100억 유로 이상의 비용 절감을 가져왔습니다. 자동 대체의 시행 상황은 국가마다 다르며, 제조업체는 가격 책정 및 계약 전략을 현지 상황에 맞추어 조정할 수밖에 없는 상황에 처해 있습니다.

아시아태평양은 2024년 말까지 중국에서 누적 87건의 승인이 예상되고, 일본에서 시장에 처음 출시되는 제품에 대한 프리미엄 가격 책정이 뒷받침됨에 따라 2031년까지 연평균 성장률(CAGR) 12.34%를 나타낼 것으로 전망됩니다. 인도와 한국은 지역적 생산 우위를 확대하고 있으며, 삼성바이오에피스는 세계 공급의 기반이 될 57만 1,000리터의 생산 능력을 목표로 하고 있습니다. 중동 및 아프리카 및 남미 시장은 여전히 발전 단계에 있지만, 시범 입찰과 현지 규제 개혁을 통해 서서히 진전을 보이고 있으며, 궁극적으로는 CHO 기반 바이오시밀러 시장의 기반을 확대해 나갈 것으로 보입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the cHO-based biosimilars market size is expected to grow from USD 13.77 billion in 2025 to USD 15.19 billion in 2026 and is forecast to reach USD 25.27 billion by 2031 at 10.71% CAGR over 2026-2031.

This report is Segmented by Products & Services {Products (Monoclonal Antibodies, Fc-Fusion Proteins, Glycoprotein Hormones, C5 Inhibitors, and More), Services & Platform}, Clinical Indication (Oncology, Autoimmune & Inflammatory, Ophthalmology, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global CHO-based Biosimilars Market Trends and Insights

Accelerating Loss of Exclusivity for High-Value Biologics

Blockbusters with annual sales of USD 200 billion to USD 400 billion will lose protection by 2030, with Keytruda, Stelara, and denosumab prominent among them . Many of these molecules carry complex glycosylation patterns that require high-fidelity CHO platforms, which discourage less-capitalized players but reward early movers who can quickly validate comparability. Premium pricing often holds during the first 18 months after launch, but late entrants face steep margin compression. The dynamic is splitting the CHO-based biosimilars market into a tier of scale-driven incumbents and a cluster of niche specialists. As a result, capacity reservation and early regulatory engagement are now more decisive than simply aligning with patent windows. Biosimilar uptake in immunology and insulin classes reached a modest penetration within 5 years of launch, compared with high adoption in oncology and ophthalmology, underscoring the persistence of formulary inertia in outpatient settings. This bifurcation suggests that regulatory interchangeability designations, while symbolically important, matter less than payer willingness to restructure formularies and absorb short-term disruption costs.

FDA / EMA Streamlining of Biosimilar Approval Pathways

By the end of 2025, the FDA had authorized 90 biosimilars across 20 reference molecules, achieving a 70% commercialization rate. Guidance released in September 2025 simplified glycosylation profiling using lectin microarrays, significantly reducing analytical risk . In Europe, the EMA's interchangeability position statement spurred national substitution policies, accelerating adoption in France, Germany, and the Netherlands. Harmonized requirements have shortened clinical development timelines, which benefits resource-rich sponsors that can run concurrent global filings. Smaller firms are increasingly pairing with CDMOs to bridge knowledge gaps and amortize compliance costs across portfolios.

US PBM Rebate/Formulary Dynamics Delay Uptake in Pharmacy-Benefit Classes

Although payer consortia have accelerated adoption in oncology and ophthalmology, immunology, and insulin still see only 25% penetration five years post-launch due to entrenched rebate contracts that blunt net price advantages. Patient assistance programs further insulate originators, limiting near-term upside for CHO-based biosimilars in outpatient settings. Ongoing scrutiny by regulators and employers may pressure PBMs to adjust, but the timeline remains uncertain.

Other drivers and restraints analyzed in the detailed report include:

- Payer Cost-Containment and Tendering Expand Access and Uptake

- EU Scientific Interchangeability and Adoption Mechanisms

- Biosimilar "Void" for Many Upcoming LoEs Due to Technical Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Products contributed 60.35% of 2025 revenue. Monoclonal antibodies alone represented a significant share of global revenue in 2024, while Fc-fusion proteins and glycoprotein hormones trailed by wide margins . Continuous-processing facilities from Celltrion and Samsung Bioepis aim to keep per-gram COGS below USD 80, positioning integrated players to withstand price erosion.

Services and platforms are expected to register a 12.65% CAGR through 2031, as emerging biotechs outsource to CDMOs. WuXi Biologics' UITM platform achieved 18 g/L at 2,000 L GMP scale, illustrating how asset-light pathways help small sponsors sidestep heavy capital outlays. The arrangement also channels incremental volume into Asia-Pacific facilities, reinforcing the region's role as a cost-optimized manufacturing hub in the CHO-based biosimilars market.

Geography Analysis

North America commanded a 42.15% share in 2025, supported by 90 FDA approvals and aggressive payer steering that drove significant Humira biosimilar uptake over 12 months. Growth is expected to plateau in saturated classes, yet upcoming LoEs for Keytruda and other oncology agents will spark new surges.

Europe combines lower absolute revenue with policy leadership; tendering delivered price drops in the United Kingdom, France, and Germany, saving health systems more than EUR 10 billion since 2020. Implementation of automatic substitution varies by country, compelling manufacturers to localize pricing and contracting strategies.

Asia-Pacific is forecast to post a 12.34% CAGR to 2031, underpinned by China's 87 cumulative approvals by year-end 2024 and Japan's premium pricing for first-to-market products. India and South Korea extend regional production advantages, with Samsung Bioepis targeting 571,000 L capacity to anchor global supply. Markets in the Middle East, Africa, and South America remain nascent but show gradual progress through pilot tenders and local regulatory reforms, ultimately broadening the footprint of the CHO-based biosimilars market.

- Abzena

- Aragen life Sciences

- Avid Bioservices

- Celltrion

- CHO Plus

- Enzene Biosciences

- Evotec

- ExcellGene

- Henlius

- Olon France

- Organon

- Patheon Pharma Services

- Peak Proteins

- Pfizer

- Samsung Bioepis

- Thermo Fisher Scientific

- Wuxi Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Loss of Exclusivity for High-Value Biologics

- 4.2.2 FDA/EMA Streamlining of Biosimilar Approval Pathways

- 4.2.3 Payer Cost-Containment and Tendering Expand Access and Uptake

- 4.2.4 EU Scientific Interchangeability and National Adoption Mechanisms

- 4.2.5 CHO Process Intensification/Continuous Bioprocessing Drives 40-80% COGS Reductions

- 4.2.6 Precision Glycoengineering/Advanced Analytics Reduce Comparability Risk/Costs

- 4.3 Market Restraints

- 4.3.1 US PBM Rebate/Formulary Dynamics Delay Uptake in Pharmacy-Benefit Classes

- 4.3.2 Biosimilar "Void" For Many Upcoming LoEs

- 4.3.3 Price-Erosion/Tender Concentration Risks Sustainability and Shortages

- 4.3.4 CHO Glycosylation/CQA Control Complexity Raises Development/Manufacturing Risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Products & Services

- 5.1.1 Products

- 5.1.1.1 Monoclonal antibodies (mAbs)

- 5.1.1.2 Fc-fusion proteins

- 5.1.1.3 Glycoprotein hormones (e.g., EPO, FSH)

- 5.1.1.4 C5 inhibitors (eculizumab)

- 5.1.1.5 RANKL inhibitors (denosumab)

- 5.1.1.6 Anti-VEGF fusion proteins (aflibercept)

- 5.1.2 Services & Platform

- 5.1.1 Products

- 5.2 By Clinical Indication

- 5.2.1 Oncology

- 5.2.2 Autoimmune & Inflammatory

- 5.2.3 Ophthalmology (retina)

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abzena

- 6.3.2 Aragen life Sciences

- 6.3.3 Avid Bioservices

- 6.3.4 Celltrion

- 6.3.5 CHO Plus

- 6.3.6 Enzene Biosciences

- 6.3.7 Evotec

- 6.3.8 ExcellGene

- 6.3.9 Henlius

- 6.3.10 Olon France

- 6.3.11 Organon

- 6.3.12 Patheon Pharma Services

- 6.3.13 Peak Proteins

- 6.3.14 Pfizer Inc.

- 6.3.15 Samsung Bioepis

- 6.3.16 Thermo Fisher Scientific

- 6.3.17 Wuxi Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment