|

시장보고서

상품코드

2063454

AI 기반 수술 로봇 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI-based Surgical Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

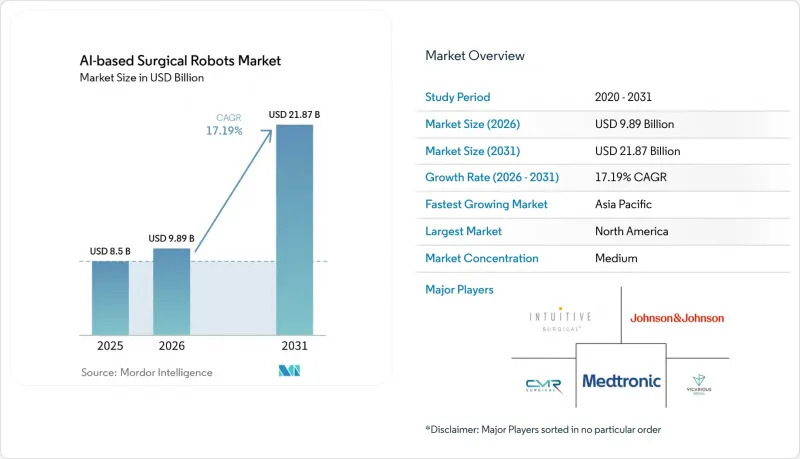

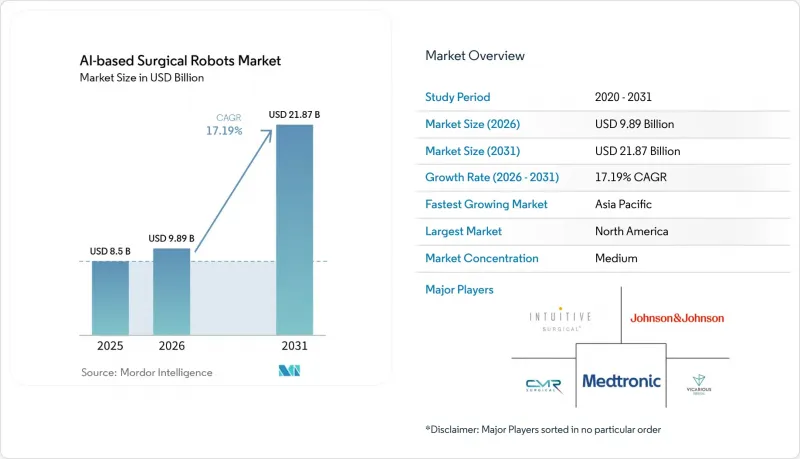

Mordor Intelligence에 의하면, AI 기반 수술 로봇 시장 규모는 2025년 85억 달러로 평가되었습니다. 2026년에는 98억 9,000만 달러로 확대되어 2026-2031년 CAGR은 17.19%를 나타내, 2031년까지 218억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(수술 시스템, 기구·부속품 등), 용도(일반외과, 비뇨기과, 산부인과, 정형외과 등), 최종 사용자(병원, 외래수술센터(ASC)), 지역(북미, 유럽, 아시아·태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 AI 기반 수술 로봇 시장 동향 및 인사이트

수술 건수가 많은 전문 분야에서 MIS에서 로봇 보조 수술로의 전환

로봇 시스템은 대장·직장 외과, 비만 외과, 비뇨기과 분야의 수술에서 복강경 수술을 점차 대체하고 있습니다. 이는 인체공학적 개선과 3D 영상 기술 덕분에, 다기관 공동 연구에서 개복 수술로의 전환율이 8%에서 3%로 감소했기 때문입니다. 비만 외과 프로그램에서는 처음 20건의 로봇 보조 슬리브 위절제술 시행 후, 수술 시간이 대폭 단축되었다고 보고되었습니다. 2025년, 비뇨기과 분야는 전 세계 로봇 수술 전체에서 큰 비중을 차지했지만, 근치적 전립선 전적출술에서의 보급률은 정체 상태에 이르렀으며, 그 성장세는 신장 적출술 및 신우 성형술로 옮겨가고 있습니다. 산부인과 분야에서는 자궁 적출술에 대한 메디케어 환급 기준이 균등화됨에 따라 도입이 가속화되고 있으며, 병원 내 이용 사례가 확대되고 있습니다. 이러한 증례 수 증가로 인해, 연간 150건 이상의 대상 증례를 다루는 시설에서는 설비 투자 회수 기간이 3년 미만으로 단축됩니다.

AI를 활용한 시각화, 의사결정 지원, 데이터 분석을 통해 예측 정확도가 향상됨

da Vinci 5와 같은 차세대 플랫폼에서 힘 감각 센서 및 형광 매핑 모듈이 승인됨에 따라, 문합 전에 허혈 조직을 식별하는 수술 중 관류 평가가 가능해집니다. 메드트로닉의 Touch Surgery Enterprise는 Hugo RAS의 모든 사례를 모범 사례 프로토콜과 자동으로 대조하고, 해당 데이터를 인증 대시보드에 반영함으로써 의료 과실 위험을 줄여줍니다. ActivSight와 같은 타사 애드온은 실시간 하이퍼스펙트럼 오버레이를 통해 담낭 절제술 시 담관 손상을 60% 감소시킵니다. 각 수술에 대한 주석이 달린 동영상이 클라우드 저장소에 업로드되면, 그로 인해 발생하는 네트워크 효과로 모델의 정확도가 향상되고, 병원은 특정 생태계에 더욱 얽매이게 됩니다. 2028년까지 주요 제조업체에서 소프트웨어가 하드웨어를 넘어서는 매출총이익 비중을 차지하게 될 것으로 예측됩니다.

높은 총 소유 비용

da Vinci Xi의 정가는 250만 달러이며, 연간 서비스료 18만 달러에 더해 사례당 2,500달러의 소모품 비용이 발생하므로, 지역 병원의 7년간 총 지출은 500만 달러를 초과합니다. 연간 수술 건수가 100건 미만인 의료기관에서는 시스템의 40%가 적자 상태로 운영되고 있습니다. 10회 사용이 가능한 EndoWrist 기구는 6-8회 사용 주기로 성능이 저하되기 때문에 사실상 일회용 방식의 경제성을 강요받고 있습니다. 중국의 신생 기업들은 플랫폼 일체를 80만 달러, 수술 1건당 600달러에 판매하며 기존 제조업체들에 대한 가격 압박을 가하고 있습니다. 기기를 무제한으로 이용할 수 있는 구독형 번들은 CFO들이 장기적인 락인(lock-in)을 꺼리기 때문에 도입률이 낮은 임베디드니다.

부문별 분석

2025년, AI 기반 수술 로봇 시장에서 수술 시스템이 30.25%로 가장 큰 점유율을 차지했으며, 기구 및 액세서리는 연평균 성장률(CAGR) 19.90%를 기록했습니다. 의료기기 및 서비스는 이미 인튜이티브사의 2025년 매출의 상당 부분을 차지했으며, 이는 해당 분야가 일회성 하드웨어 판매에서 지속적인 수익 모델로 전환되고 있음을 보여주었습니다.

소프트웨어 분석 모듈은 콘솔 1대당 연간 5만-15만 달러의 구독 수익을 창출하고 있으며, 이 높은 매출 총이익률은 AI 기반 수술용 로봇 업계 전체의 전략적 우선순위를 재편하고 있습니다. ActivSight를 120개 시설에 도입함으로써, 2025년에는 1,800만 달러의 지속적인 수익이 창출되었습니다. OEM 업체들이 예측 분석, 수술 계획, 수술 후 벤치마크를 모든 라이선스 갱신에 포함함에 따라, 이러한 모듈을 다루는 AI 기반 수술 로봇 시장 규모는 두 자릿수 성장률을 기록하며 확대될 것으로 전망됩니다.

지역별 분석

아시아태평양은 성장의 원동력이며, 2031년까지 연평균 19.78%의 성장률이 예상됩니다. 이는 중국 공급업체들이 서유럽 국가들의 가격보다 약 절반 수준에 전체 플랫폼을 판매하고 있으며, 인도와 동남아시아 정부들이 설비 투자에 대해 막대한 보조금을 지급하고 있기 때문입니다. 중국의 MicroPort MedBot과 Tinavi는 2025년에 콘솔 가격을 약 80만 달러로 책정함으로써 현지 시장에서 상당한 시장 점유율을 확보했으며, 이에 따라 Intuitive와 Medtronic은 저가형 제품 라인업을 마련했습니다. 인도에서는 2025년에 120개의 시스템이 도입되었으며, 그 대부분은 중동 및 아프리카에서 온 외국인 환자(1건당 8,000-1만 2,000달러를 지불)를 수용하는 대도시권에 집중되어 있습니다.

북미는 2025년 총 매출의 47.09%를 차지하며 여전히 매출 1위를 유지했지만, 비뇨기과 및 일반외과 분야에서의 보급이 정체기에 접어들면서 성장률은 둔화되고 있습니다. 미국은 전립선 전적출술, 자궁 전적출술, 대장·직장 수술에 대한 메디케어 적용 외에도, 현재 외래수술센터(ASC)에서 시행되는 인공 슬관절 치환술 총 건수의 30%에 대한 자금 지원을 제공하는 민간 보험사의 지원 덕분에 지역별 매출의 대부분을 차지하고 있습니다. 유럽은 매출액 기준으로 2위입니다. 독일은 식도 절제술 및 췌장 수술 비용을 보상하는 DRG 코드 하에서 180대를 도입할 예정이며, 2025년 도입 대수 기준으로 1위를 차지했습니다. 그러나 EU의 AI법에 따라 신제품을 시장에 출시할 때마다 12-18개월의 추가 기간과 500만-1,000만 달러의 추가 비용이 발생하게 되었습니다.

중동 및 아프리카에서의 도입은 정부계 펀드가 주력 프로그램에 자금을 지원하는 걸프 지역 거점에 집중되어 있습니다. UAE와 사우디아라비아의 거점 병원에서는 연간 총 8,000건의 로봇 수술을 시행하고 있습니다. 남아프리카공화국의 12대 도입 실적은 주로 민간 병원 체인에 집중되어 있으며, 공공 예산은 감염병 치료에 중점을 두고 있습니다. 남미의 강점은 브라질에 있으며, 이 나라의 민간 그룹인 Rede D'Or와 Hapvida는 2025년에 1만 5,000건의 수술을 시행했습니다. 아르헨티나에서는 민간 보험 적용 대상에 전립선 전적출술 및 비만 수술을 위한 콘솔 8대가 추가되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the aI-based surgical robots market size is expected to grow from USD 8.5 billion in 2025 to USD 9.89 billion in 2026 and is forecast to reach USD 21.87 billion by 2031 at 17.19% CAGR over 2026-2031.

This report is Segmented by Component (Surgical Systems, Instruments & Accessories, and More), Application (General Surgery, Urology, Gynecology, Orthopedics, and More), End User (Hospitals, and Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global AI-based Surgical Robots Market Trends and Insights

MIS Shift to Robotic-Assisted Surgery Across High-Volume Specialties

Robotic systems are displacing laparoscopy in colorectal, bariatric, and urologic cases because improved ergonomics and 3-D vision reduce conversion-to-open rates from 8% to 3% in multi-center studies. Bariatric programs report significantly shorter operative times after the first 20 robotic sleeve-gastrectomy cases . Urology holds a significant share of all robotic procedures worldwide in 2025, yet penetration has plateaued in radical prostatectomy, shifting incremental growth to nephrectomy and pyeloplasty. Gynecologic adoption accelerates under Medicare reimbursement parity for hysterectomy, widening hospital use cases. These volume gains shorten capital payback periods to fewer than three years for facilities performing at least 150 eligible cases annually.

AI-Enabled Visualization, Decision Support, and Data Insights Improve Predictability

Clearance of force-sensing and fluorescence-mapping modules on next-generation platforms such as da Vinci 5 enables intraoperative perfusion assessment that flags ischemic tissue before anastomosis. Medtronic's Touch Surgery Enterprise automatically benchmarks every Hugo RAS case against best-practice pathways, feeding credentialing dashboards that lower malpractice exposure. Third-party add-ons like ActivSight decrease bile-duct injuries by 60% in cholecystectomy through real-time hyperspectral overlays . Each procedure uploads annotated video to cloud repositories, and the resulting network effects improve model accuracy, further locking hospitals into specific ecosystems. By 2028, software is projected to contribute a greater share of gross profit than hardware for leading manufacturers.

High Total Cost of Ownership

A da Vinci Xi lists at USD 2.5 million and carries USD 180,000 in annual service plus USD 2,500 per-case disposable costs, bringing seven-year outlays above USD 5 million for community hospitals. Forty percent of systems in sub-100-case facilities operate at negative margins. Degradation of ten-use EndoWrist instruments after six to eight cycles effectively forces single-use economics. Chinese entrants sell complete platforms at USD 800,000 and USD 600 per procedure, fueling price pressure on incumbents. Subscription bundles offering unlimited instruments have low adoption as CFOs resist long-term lock-ins.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Indications and Procedure Volumes in Soft Tissue and Orthopedics

- Outpatient/ASC Migration Enabling Compact Systems and Higher Utilization

- Learning Curve and OR Workflow Disruption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surgical Systems contributed a leading 30.25% to the AI-based surgical robots market in 2025, while instruments & accessories posted a 19.90% CAGR. Instruments and Services already provide the majority of Intuitive's 2025 revenue, signaling the sector's pivot from one-time hardware sales to annuity models.

Software & Analytics Modules attract annual subscriptions of USD 50,000-150,000 per console, and their high gross margins are reshaping strategic priorities across the AI-based surgical robots industry. ActivSight's 120 hospital installations generated USD 18 million in recurring revenue in 2025. The AI-based surgical robots market size for these modules is projected to expand at double-digit rates as OEMs embed predictive analytics, case planning, and postoperative benchmarking into every license renewal.

Geography Analysis

Asia-Pacific is the growth engine, set to grow 19.78% annually through 2031, as Chinese vendors sell full platforms at roughly half the Western price and governments in India and Southeast Asia subsidize capital outlays significantly. China's MicroPort MedBot and Tinavi held a notable local share in 2025 by pricing consoles at around USD 800,000, prompting Intuitive and Medtronic to draft economy-tier offers. India added 120 systems in 2025, largely in metro hubs catering to inbound patients from the Middle East and Africa who pay USD 8,000-12,000 per case.

North America remains the revenue leader at 47.09% of the 2025 total, yet its trajectory is moderating as urology and general-surgery penetration plateaus. The United States accounts for the majority of regional income thanks to Medicare coverage for prostatectomy, hysterectomy, and colorectal procedures, plus commercial-payer backing that now funds 30% of total-knee procedures in ASCs. Europe sits second by revenue; Germany led 2025 installs with 180 units under DRG codes that reimburse esophagectomy and pancreatic work, but the EU AI Act now tacks on an extra 12-18 months and USD 5-10 million to each new product rollout.

Adoption in the Middle East and Africa clusters in Gulf hubs where sovereign wealth funds bankroll showpiece programs; UAE and Saudi reference centers together run 8,000 robotic cases a year. South Africa's 12-system footprint sits mostly in private chains, while public budgets focus on infectious-disease care. South America's strength lies in Brazil, whose private groups Rede D'Or and Hapvida performed 15,000 cases in 2025; Argentina added eight consoles for prostatectomy and bariatrics under private insurance cover

- Asensus Surgical (KARL STORZ)

- Brain Lab

- CMR Surgical

- Distalmotion

- Globus Medical

- Intuitive Surgical

- Johnson & Johnson

- Medicaroid (Kawasaki/Sysmex)

- Medtronic

- MicroPort MedBot

- Moon Surgical

- Noah Medical

- Renishaw

- Siemens Healthineers

- Smiths Group

- SS Innovations

- Stereotaxis

- Stryker

- THINK Surgical

- Vicarious Surgical

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 MIS Shift to Robotic-Assisted Surgery Across High-Volume Specialties

- 4.2.2 AI-Enabled Visualization, Decision Support, And Data Insights Improve Predictability

- 4.2.3 Expanding Indications and Procedure Volumes in Soft Tissue and Orthopedics

- 4.2.4 Outpatient/ASC Migration Enabling Compact Systems and Higher Utilization

- 4.2.5 Managed Service and Per-Procedure Pricing Models Lowering Capex Barriers

- 4.2.6 AI-Driven Training, Simulation, And Tele-Proctoring Compress Learning Curves

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership (Systems, Service, Limited-Use Instruments)

- 4.3.2 Learning Curve and OR Workflow Disruption Slow Early Throughput

- 4.3.3 EU AI Act High-Risk Compliance Adds Documentation and Audit Burdens

- 4.3.4 Cybersecurity And Hospital IT Integration Constraints on Connected ORs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Surgical Systems

- 5.1.2 Instruments & Accessories

- 5.1.3 Software & Analytics Modules

- 5.1.4 Services (installation, training, maintenance)

- 5.2 By Application

- 5.2.1 General Surgery (e.g., hernia, colorectal, bariatric)

- 5.2.2 Urology

- 5.2.3 Gynecology

- 5.2.4 Orthopedics (knee, hip, shoulder)

- 5.2.5 Neurosurgery

- 5.2.6 Cardiothoracic/Thoracic

- 5.2.7 Bronchoscopy/Endoluminal (lung)

- 5.2.8 Head & Neck / ENT

- 5.3 By End User

- 5.3.1 Hospitals (AMCs, tertiary centers)

- 5.3.2 Ambulatory Surgical Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Asensus Surgical (KARL STORZ)

- 6.3.2 Brainlab

- 6.3.3 CMR Surgical

- 6.3.4 Distalmotion

- 6.3.5 Globus Medical

- 6.3.6 Intuitive Surgical

- 6.3.7 Johnson & Johnson

- 6.3.8 Medicaroid (Kawasaki/Sysmex)

- 6.3.9 Medtronic

- 6.3.10 MicroPort MedBot

- 6.3.11 Moon Surgical

- 6.3.12 Noah Medical

- 6.3.13 Renishaw

- 6.3.14 Siemens Healthineers

- 6.3.15 Smith+Nephew

- 6.3.16 SS Innovations

- 6.3.17 Stereotaxis

- 6.3.18 Stryker

- 6.3.19 THINK Surgical

- 6.3.20 Vicarious Surgical

- 6.3.21 Zimmer Biomet

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment