|

시장보고서

상품코드

2063456

치과용 석고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dental Gypsum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

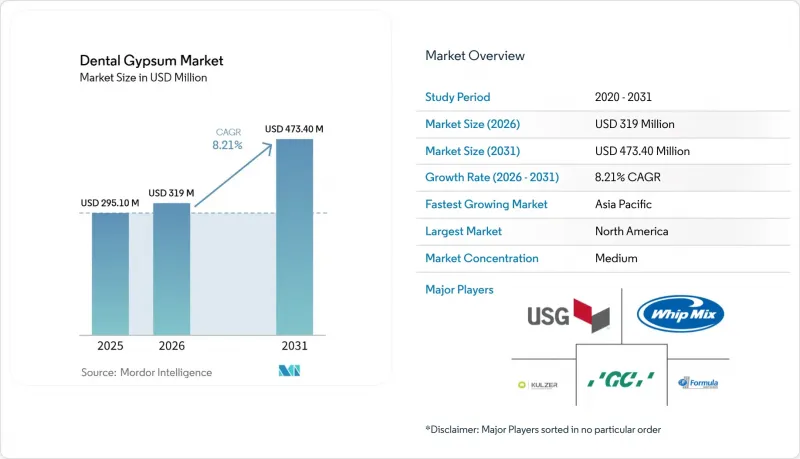

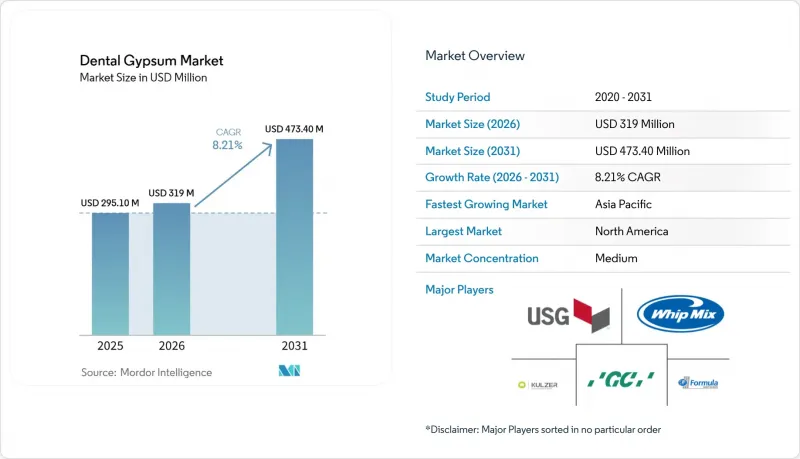

Mordor Intelligence에 의하면, 치과용 석고 시장 규모는 2025년 2억 9,510만 달러로 평가되었고, 2026년 3억 1,900만 달러로 추정되고, 2031년까지 4억 7,340만 달러로 확대될 전망이며, 2026-2031년 CAGR 8.21%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(유형 I, 유형 II, 유형 III, 기타), 용도별(검사 및 진단용 모형, 작업용 주형 및 다이, 기타), 최종 사용자별(치과 기공소, 치과 병원, 병원, 학술 및 교육 기관), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 치과용 석고 시장 동향 및 분석

보철 치료 건수 증가

북미와 서유럽의 고령화 추세가 크라운, 브릿지, 완전 틀니에 대한 수요를 견인하고 있으며, 이로 인해 2032년까지 수복 치료 매출이 연평균 6.1%의 속도로 증가할 것으로 전망됩니다. 디지털 틀니 덕분에 진료실에서의 내원 횟수가 3분의 1 가까이 줄어들었음에도 불구하고, 치과 기공소에서는 중합이나 교합 재장착 시 플라스크를 안정적으로 고정하기 위해 여전히 유형 III 석고 베이스를 주조하고 있습니다. 임상 연구를 통해 석고 마스터 캐스트가 화면상으로는 확인되지 않는 CAD/CAM 밀링으로 인한 결함을 감지하여, 치아의 가장자리 무결성을 확보할 수 있음이 확인되었습니다. 2달러짜리 석고 주형을 사용하면 3,000달러의 재제작 비용을 절감할 수 있기 때문에 임상의들은 이 재료를 품질 관리 절차에 포함시키고 있습니다. 그 결과, 2031년까지 보철 분야에서는 연간 1,400만 회 이상의 추가 주조가 예상되며, 이는 치과용 석고 시장의 꾸준한 성장을 뒷받침하게 될 것입니다.

치과 기공소의 확장 및 아웃소싱

ISO 규격에 따른 공차 표준화로 인해, 심천에서 주조된 다이와 시카고에서 밀링 가공된 크라운이 동일한 50마이크로미터의 허용 오차 범위 내에서 정밀하게 맞물리게 되었습니다. 이러한 규제 표준화로 인해 북미 CAD/CAM 크라운 및 브릿지 작업의 65% 이상이 아시아태평양의 슈퍼랩으로 이전되었고, 조달이 일원화됨에 따라 납품되는 유형 III의 비용은 주형당 0.50달러 미만으로 떨어지게 되었습니다. 2024년에 50만 명의 외국인 환자를 치료할 예정인 인도의 치과 관광 클리닉은 치료 계획용 가이드 제작에 석고를 선호하여 사용하는 자체 실험실을 보유하고 있으며, 이것이 향후 성장의 핵심 동력이 되고 있습니다. 자동 혼합 사일로와 진공 조절을 통해 경화 시간의 편차가 줄어든 덕분에, 대량 생산을 하는 연구소들은 광산 직송 가격으로 석고 원료를 확보하기 위해 다년 계약을 체결하고 있습니다. 이러한 추세가 맞물려 치과용 석고 시장의 장기적인 수요를 끌어올리고 있으며, 공급업체 간의 경쟁을 화학적 특성이 아닌 서비스 측면에서 더욱 치열하게 만들고 있습니다.

구강 스캐너의 급속한 보급으로 인해, 모형이 필요 없거나 프린트를 활용한 워크플로우가 가능해졌습니다.

2024년까지 스캐너 보급률은 일반 치과 의사의 경우 44%, 교정 치과 의사의 경우 45%에 달했으며, 임상의들은 물리적 인상 채득 없이도 단일 크라운을 밀링하거나 얼라이너를 주문할 수 있게 되었습니다. 파우더리스 광학 시스템을 통해 전체 치열 스캔 시간이 90초로 단축되어, 체어사이드 CAD/CAM 시스템을 통해 단 한 번의 내원만으로 당일 장착이 가능해졌습니다. 디지털 치료 1건당 200-300g의 제3종 석고가 절감되어, 이에 따른 수요가 감소하고 있습니다. 설비 투자 부담으로 인해 소규모 진료소나 지방 진료소에서의 도입은 여전히 주춤하고 있지만, 주요 도시 지역의 우편번호 구역에서는 이미 사용률이 60%를 넘어섰으며, 이는 치과용 석고 시장에 단기적인 타격을 주고 있습니다.

부문별 분석

유형 IV는 임플란트 검증 및 풀 아치 수복 시 5,000 psi를 초과하는 압축 강도가 요구되기 때문에 연평균 성장률(CAGR) 8.67%를 나타낼 것으로 전망되며, 치과용 석고 시장 내에서 프리미엄 가격대를 유지하고 있습니다. 유형 III는 고처리량 연구용 모형 분야에서 비용과 0.15%의 팽창률 일관성 간의 균형이 여전히 중요하게 여겨지고 있기 때문에 2025년 시점에서 치과용 석고 시장의 39.63% 점유율을 유지했습니다. 하루 200개 이상의 주형을 생산하는 연구소에 따르면, 자동 진공 믹서를 도입함으로써 기공률이 감소하고, 다이 조정 작업이 12% 줄어들었으며, 기공사의 작업 시간이 단축되었습니다. 유형 II는 교합기 장착 용도로서 틈새 시장을 유지하고 있는 반면, 유형 I은 특수한 무치악 인상 채취를 제외하고는 거의 사라졌습니다. 7,000 psi를 초과하는 신형 유형 V 석고는 지르코니아 기판에 적용할 수 있지만, 경화 시간이 길어 당일 마감 작업 흐름을 방해하기 때문에 보급은 제한적입니다.

ISO 6873 표준을 준수함으로써 공급업체는 전 세계적으로 동일한 배합 제품을 출하할 수 있게 되었으며, 이는 국경을 초월한 가격 수렴을 촉진하고 물류 효율성을 핵심적인 차별화 요인으로 전환하고 있습니다. Whip Mix사의 Silky-Rock은 0.09%의 선팽창률을 보이며, 5분 만에 분리됩니다. 이는 얼라이너 점검 수요가 급증함에 따라 바쁜 일정을 소화해야 하는 실험실에게 있어 이점입니다. Kulzer사의 'Die-Stone'은 미리 계량된 소포장을 제공하여 혼합 오차를 1g 미만으로 억제함으로써, 병원 내 밀링에 진출하는 소규모 클리닉의 도입을 촉진하고 있습니다. 경쟁이 치열해지는 가운데, 각 벤더들은 자동 디스펜서와 무진 포장 장비를 세트로 판매하고 있으며, 이를 통해 보다 광범위한 치과용 석고 시장에서 유형 IV의 장기적인 시장 침투가 확고해지고 있습니다.

지역별 분석

북미는 2025년 시장 규모의 38.13%를 차지했으며, 7,000개가 넘는 인증 실험실과 크라운 및 임플란트에 대한 광범위한 보험 적용이 이를 뒷받침하고 있습니다. 그러나 OSHA(미국 직업안전보건청)의 흡입성 실리카 규제로 인해 환기 및 모니터링 비용이 상승하고 있어, 일부 독립 연구소들은 모형 제작을 해외에 위탁하거나 실리카가 포함되지 않은 배합을 채택하는 방향으로 움직이고 있습니다. 따라서 이 지역의 치과용 석고 시장 규모는 치료 수요가 여전히 견조함에도 불구하고, 세계 평균보다 완만한 속도로 확대되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.41%를 나타낼 것으로 예측되며, 이는 전 세계에서 가장 빠른 성장 속도입니다. 중국의 슈퍼랩은 북미 CAD/CAM 사례의 3분의 2를 처리하고 있으며, ISO 기준에 부합하는 품질 보증으로 재제작률을 2% 미만으로 억제하고 있다는 점이 이를 뒷받침하고 있습니다. 인도의 인바운드 치과 관광 클리닉은 2025년 한 해에만 120만 개 이상의 진단용 모형을 제작하여 재료 수요를 견인하고 있습니다. 한국과 일본의 교정치과에서는 스캐너 보급률이 높음에도 불구하고 석고를 이용한 검증이 여전히 유지되고 있으며, 이는 정밀성을 중시하는 문화를 반영하고 있습니다. 이러한 요인들이 복합적으로 작용하여 조달 수요의 중심이 해당 지역으로 이동하고 있으며, 치과용 석고 시장 내 공급업체 간의 경쟁이 치열해지고 있습니다.

유럽에서는 고령화를 배경으로 안정적인 수요가 나타나고 있지만, 혼합 석고의 매립 처분 금지 조치로 인해 독일과 프랑스에서는 처분 비용이 톤당 150달러까지 치솟고 있습니다. 많은 치과 기공소들은 이러한 변화에 대응하여, 위험이 적은 학습용 모형을 프린팅 수지로 전환함으로써, 높은 정밀도가 요구되는 유형 IV 및 유형 V 용도에 석고 예산을 할당하고 있습니다. 중동 및 아프리카는 규모는 작지만, ISO 인증 자재 사용을 의무화하는 새로운 교육 병원이 개설되고 있어 장기적인 성장이 기대됩니다. 남미에서는 공공 구강 보건 프로그램과 대학 네트워크 덕분에 소폭이지만 안정적인 학습용 모형 수요가 유지되고 있으며, 이는 전 세계 치과용 석고 시장의 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the dental gypsum market size is projected to expand from USD 295.10 million in 2025 and USD 319 million in 2026 to USD 473.40 million by 2031, registering a CAGR of 8.21% between 2026 to 2031.

This report is Segmented by Product Type (Type I, Type II, Type III, and More), Application (Study/Diagnostic Models, Working Casts & Dies, and More), End User (Dental Laboratories, Dental Clinics, Hospitals & Academic/Teaching Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Dental Gypsum Market Trends and Insights

Rising Prosthodontic Case Volumes

The aging population in North America and Western Europe is driving demand for crowns, bridges, and complete dentures, lifting restorative revenues at a 6.1% trajectory to 2032 . Even as digital dentures trim chairside visits by almost one-third, laboratories still pour Type III bases to stabilize flasks during polymerization and occlusal remounting. Clinical studies confirm that gypsum master casts detect CAD/CAM milling artifacts invisible on-screen, safeguarding marginal integrity. Because a USD 2 gypsum pour averts a USD 3,000 remake, clinicians retain the material in their quality-control protocol. Consequently, prosthodontics is expected to add more than 14 million additional pours annually by 2031, underpinning steady expansion of the dental gypsum market.

Expansion of Dental Laboratories and Outsourcing

ISO-standard tolerance convergence now lets a die poured in Shenzhen seat a crown milled in Chicago with the same 50-micrometer margin fidelity. This regulatory parity catalyzed a shift of over 65% of North American CAD/CAM crown-and-bridge work to APAC super-labs, concentrating procurement and dropping delivered Type III costs below USD 0.50 per cast. Indian dental-tourism clinics, treating half a million foreign patients in 2024, own in-house labs that favor gypsum for treatment planning guides, adding another growth channel. Automated mixing silos and vacuum conditioning cut set-time variation, encouraging high-volume labs to sign multi-year contracts that secure raw gypsum at mine-gate pricing. These dynamics collectively lift long-term demand for the dental gypsum market and heighten supplier competition on service, not chemistry.

Rapid Adoption of Intraoral Scanners Enabling Model-Free or Printed Workflows

Scanner penetration reached 44% of general dentists and 45% of orthodontists by 2024, letting clinicians mill single-unit crowns or order aligners without physical impressions. Powder-free optics cut full-arch capture to 90 seconds, while chairside CAD/CAM systems present same-day placement in a single visit. Each digital case eliminates 200-300 grams of Type III stone, eroding incidental demand. Capital expense still curbs uptake in smaller or rural practices, but in top urban ZIP codes, usage already exceeds 60%, creating a near-term drag on the dental gypsum market.

Other drivers and restraints analyzed in the detailed report include:

- Orthodontic Treatment Growth, Especially in Asia-Pacific

- ISO 6873 Standardization Enabling Cross-Market Adoption

- Shift to 3-D-Printed Models Displacing Poured Stone in Labs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type IV captured an 8.67% CAGR outlook as implant verification and full-arch restorations require compressive strengths past 5,000 psi, sustaining premium pricing within the dental gypsum market size. Type III retained 39.63% dental gypsum market share in 2025 because high-throughput study models still favor its balance of cost and 0.15% expansion consistency. Laboratories producing more than 200 daily casts report that automated vacuum mixers trim porosity, cutting die adjustments by 12% and saving technician hours. Type II remains niche for articulator mounting, while Type I is largely obsolete outside specialized edentulous impressions. Emerging Type V stones, topping 7,000 psi, service zirconia substructures but face limited uptake due to longer set-times that hinder same-day workflows.

ISO 6873 alignment lets suppliers ship identical formulations worldwide, fostering cross-border price convergence and turning logistics efficiency into a core differentiator. Whip Mix's Silky-Rock achieves 0.09% linear expansion and separates in five minutes, an advantage for labs racing against surge volumes of aligner checks. Kulzer's Die-Stone offers pre-weighed satchels that reduce mixing errors to below 1 g, a driver of adoption among small clinics venturing into in-office milling. As competitive intensity rises, vendors bundle automated dispensers and dust-free packaging, cementing long-term penetration of Type IV within the broader dental gypsum market.

Geography Analysis

North America generated 38.13% of the 2025 value, anchored by more than 7,000 certified laboratories and widespread insurance coverage for crowns and implants. OSHA respirable-silica regulation, however, is inflating ventilation and monitoring costs, nudging some independent labs to outsource model production offshore or adopt silica-free formulations. The dental gypsum market size in the region is therefore expanding more slowly than the global average, even though procedural demand remains robust.

Asia-Pacific is forecast for an 8.41% CAGR through 2031, the fastest worldwide. Chinese super-labs process two-thirds of North American CAD/CAM cases, buoyed by ISO-aligned quality assurances that reduce remakes to under 2%. India's inbound dental-tourism clinics poured more than 1.2 million diagnostic casts in 2025 alone, reinforcing material pull. South Korean and Japanese orthodontic hubs maintain gypsum verification even with high scanner adoption, reflecting cultural emphasis on precision. Collectively, these drivers are tilting procurement gravity toward the region, intensifying supplier competition inside the dental gypsum market.

Europe shows stable, aging-driven demand but faces landfill bans on mixed gypsum that escalate disposal fees to USD 150 per ton in Germany and France. Many labs respond by shifting low-risk study models to printed resins, freeing gypsum budgets for high precision Type IV and Type V applications. The Middle East and Africa, while smaller, are opening new teaching hospitals that mandate ISO-certified materials, offering long-tail growth. South America's public oral-health programs and university networks sustain a modest but dependable call for study models, rounding out the global footprint of the dental gypsum market.

- BEGO

- Benco Dental

- Dentona AG

- Ernst Hinrichs Dental GmbH

- ETI Empire Direct

- Garreco LLC

- GC Corporation

- Henry Schein

- Heraeus Kulzer

- Ivoclar

- LASCOD S.p.A.

- Milton Bridge

- Saint-Gobain Formula GmbH

- SHERA Werkstoff-Technologie GmbH

- SILADENT Dr. Bohme & Schops

- USG

- Whip Mix Corporation

- YETI Dentalprodukte

- Yoshino Gypsum

- Zhermack SpA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prosthodontic Case Volumes

- 4.2.2 Expansion Of Dental Laboratories and Outsourcing

- 4.2.3 Orthodontic Treatment Growth, Especially In APAC

- 4.2.4 ISO 6873 Standardization Supports Quality and Cross-Market Adoption

- 4.2.5 Implant Model and Verification Workflows Still Favor High-Strength Die Stones

- 4.2.6 Cost/Time Advantage Of Gypsum For Select High-Throughput Study Models Vs 3-D Printed

- 4.3 Market Restraints

- 4.3.1 Rapid Adoption of Intraoral Scanners Enabling Model-Free or Printed Workflows

- 4.3.2 Shift To 3D-Printed Models Displacing Poured Stone in Labs

- 4.3.3 OSHA/NIOSH Silica Exposure Compliance Burden in Labs

- 4.3.4 Gypsum Disposal Constraints (H2S Risk) Raising Handling Costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Type I

- 5.1.2 Type II

- 5.1.3 Type III

- 5.1.4 Type IV

- 5.1.5 Type V

- 5.2 By Application

- 5.2.1 Study/diagnostic models

- 5.2.2 Working casts & dies

- 5.2.3 Implant models & verification jigs

- 5.2.4 Orthodontic models

- 5.2.5 Articulator mounting

- 5.2.6 Denture flasking/base pours

- 5.3 By End User

- 5.3.1 Dental Laboratories

- 5.3.2 Dental Clinics

- 5.3.3 Hospitals & Academic/Teaching Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 BEGO

- 6.3.2 Benco Dental

- 6.3.3 Dentona AG

- 6.3.4 Ernst Hinrichs Dental GmbH

- 6.3.5 ETI Empire Direct

- 6.3.6 Garreco LLC

- 6.3.7 GC Corporation

- 6.3.8 Henry Schein

- 6.3.9 Heraeus Kulzer

- 6.3.10 Ivoclar

- 6.3.11 LASCOD S.p.A.

- 6.3.12 Milton Bridge

- 6.3.13 Saint-Gobain Formula GmbH

- 6.3.14 SHERA Werkstoff-Technologie GmbH

- 6.3.15 SILADENT Dr. Bohme & Schops

- 6.3.16 USG

- 6.3.17 Whip Mix Corporation

- 6.3.18 YETI Dentalprodukte

- 6.3.19 Yoshino Gypsum

- 6.3.20 Zhermack SpA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment