|

시장보고서

상품코드

2063471

미스칸투스 기반 포장재 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Miscanthus-Based Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

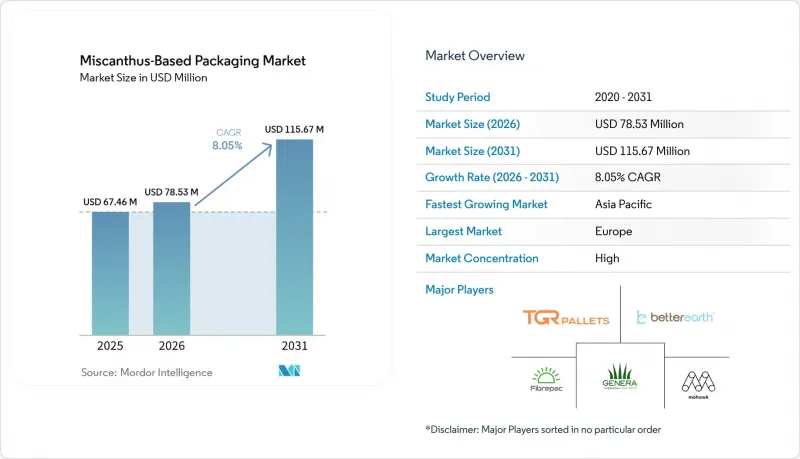

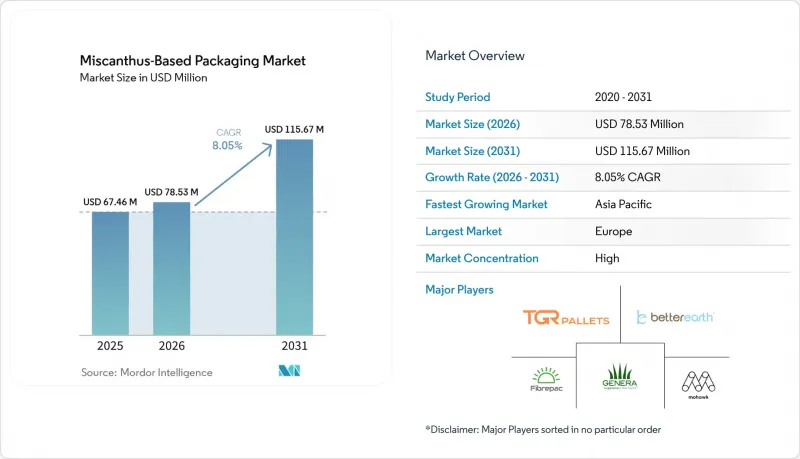

Mordor Intelligence에 의하면, 미스칸투스 기반 포장재 시장 규모는 2025년에 6,746만 달러로 평가되었습니다. 2026년에 7,853만 달러에서 2031년까지 1억 1,567만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 8.05%를 나타낼 것으로 전망됩니다.

본 보고서는 포장 형태(클램쉘 용기·트레이, 플레이트·볼, 보호 포장 등), 최종 이용 산업(외식 산업, 퍼스널케어 및 화장품, 소매 및 전자상거래, 식품 및 음료 등), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 미스칸투스 기반 포장재 시장 동향 및 인사이트

플라스틱 포장 감축을 위한 규제 움직임

유럽연합(EU)의 ‘포장 및 포장 폐기물 규정’은 2030년까지 모든 포장재를 재활용 가능하거나 퇴비화 가능하도록 의무화하고 있으며, 이로 인해 다층 플라스틱과 대부분의 폴리스티렌 제품이 사실상 배제됨에 따라 조달 부서는 원자재 선택지를 재검토할 수밖에 없게 되었습니다. 2024년부터 2025년에 걸쳐 미국의 7개 주에서 확대 생산자 책임(EPR) 법을 채택하여, 퇴비화 가능한 섬유 대체재에 경제적 이점을 제공하는 요금 제도를 도입하는 한편, 전국 브랜드의 의사결정 주기를 단축했습니다. 베트남이나 필리핀 등 아세안(ASEAN) 회원국에서는 이미 EPR 준수가 의무화되어 있으며, 인도네시아, 말레이시아, 태국도 2027년까지 단계적으로 동일한 의무를 도입할 예정이므로, 지역 소매업체들에게는 명확한 규제 전망이 열리고 있습니다. 이러한 정책들이 동시에 추진됨에 따라 도입 일정이 단축되었으며, 시행까지 남은 2년은 미스칸서스 가공업체들에게 있어 매우 중요한 상용화 단계가 되고 있습니다. 이 소재는 합성 결합제를 사용하지 않으면서도 EN 13432의 퇴비화 기준을 충족하므로, 생산자는 목재 펄프 솔루션 도입을 종종 지연시키는 고비용의 배합 변경 작업을 피할 수 있습니다.

발포 폴리스티렌을 대체할 섬유계 대체재의 확대

현재 전 세계 200개 이상의 관할 구역에서 폴리스티렌 사용 금지 조치가 시행되고 있지만, 최종 사용자들은 여전히 기존 EPS가 제공하던 단열성과 완충 성능을 요구하고 있습니다. PulPac사의 건식 성형 섬유 공정은 3.5초의 사이클 타임을 실현하고, 물을 대량으로 소비하는 건조 공정을 생략하며, EPS와 동등한 낙하 시험 성능을 지닌 복잡한 형상을 성형할 수 있는 한편, 에너지 소비량을 65% 절감합니다. 그래픽 패키징사는 2024년, 콜드체인용 컨테이너의 생산 능력을 확대하기 위해 8,500만 달러를 배정했습니다. 이는 대형 기존 기업들이 성형 섬유를 식품·의약품 분야의 EPS 후속 소재로 간주하고 있음을 뒷받침하는 것입니다. 미스칸서스 섬유는 활엽수 펄프에 비해 부피 밀도가 낮기 때문에 완성된 인서트의 무게가 가벼워집니다. 이를 통해, 부피 중량이 비용에 영향을 미치는 EC 소포 배송 네트워크에서 운임을 직접 절감할 수 있습니다. 이러한 운송상의 이점은 물류 담당자들로부터도 지지를 받고 있으며, 이 소재는 단순한 지속가능성 주장을 넘어선 가치 제안을 만들어내고 있습니다.

산업 규모에서의 가공 및 펄프화 인프라 부족

세계적으로 볼 때, 가동 중인 비목재 펄프 생산 라인은 15개 미만인 반면, 목재 펄프 공장은 400개 이상으로, 이러한 현저한 규모 격차가 미스칸서스의 급속한 보급을 제약하고 있음이 드러나고 있습니다. ANDRITZ사는 2025년에 Genera사와 제휴하여 미국 최초의 전용 유리섬유 생산 라인 가동을 시작했으나, 설치에 18-24개월이 소요되기 때문에 가공업체에 충분한 양의 제품이 공급되기 시작하는 것은 2027년 하반기가 될 전망입니다. 풀에 함유된 실리카가 소화조의 마모를 가속화하기 때문에 설비 비용은 목재 펄프로 만든 동급 제품보다 25-30% 더 비싸며, 이는 사업 시작의 걸림돌이 되어 자금 조달 모델을 복잡하게 만들고 있습니다. 미네랄스 테크놀로지스(Minerals Technologies)는 2025년에 3개의 성형 섬유 위성 공장을 설립했으나, 이들 공장은 여전히 수입된 비목재 펄프에 의존하고 있어, 하류 생산 능력이 업스트림 가공 설비를 앞지를 수 있음을 시사하고 있습니다. 따라서 현재의 도입 속도를 유지하기 위해서는 인프라 격차를 신속히 해소하는 것이 매우 중요합니다.

부문별 분석

2025년, 클램쉘 용기와 트레이는 미스칸서스 유래 포장재 시장의 42.34%를 차지했습니다. 이는 2026년 8월 유럽 및 미국의 일부 지자체에서 시행될 플라스틱 금지령에 앞서, 폴리스티렌 재질의 경첩이 달린 상자를 조기에 대체하기 시작한 패스트푸드점들의 움직임에 힘입은 결과입니다. 후타마키는 2024년부터 2025년에 걸쳐 전 세계 9곳의 공장에서 성형 섬유 제품의 생산 능력을 확대했습니다. 이는 규제 준수 패키지에 대한 수요가 급증할 것으로 예상에 따라 공급을 이에 맞추는 한편, 초섬유의 확장성에 대한 자신감을 반영한 것입니다. 사바트의 ‘Pulp-it!’ 시리즈는 2024년 아시아태평양의 업무용 케이터링 시장에서 30%의 매출 성장을 기록하며, 이 제품의 도입 열기가 더 이상 유럽 시장에만 국한되지 않음을 보여주었습니다. 그러나 유럽에서의 성장은 정체 국면에 접어들고 있습니다. 이는 PFAS 프리 코팅을 조기에 도입한 기업들이 공급 상황에 맞추어 재주문 주기를 늦추고 있기 때문이며, 향후 판매량 증가는 사업자별 보급률보다는 지역적 확대에 더 크게 좌우될 것임을 시사합니다. 그 결과, 미스칸서스에서 유래한 클램쉘 포장 시장 규모는 꾸준히 확대될 것으로 예상되지만, 그 속도는 새로운 용도 분야에 비해 완만할 것으로 보입니다.

보호용 포장 시장은 더욱 가파른 성장 궤도에 올라 있으며, 전자상거래 물류 센터와 전자기기 브랜드들이 ASTM D6400 표준을 준수하는 퇴비화 가능한 성형 섬유 삽입재로 전환을 추진함에 따라 2031년까지 연평균 9.78%의 성장률이 예상됩니다. Storopack은 2024년에 풀 섬유로 만든 완충재를 출시했으며, Cascades는 3억 5,000만 달러 규모의 성형 섬유 투자 계획 중 60% 이상을 보호용 제품에 할당하고 있어, 가공업체들이 이 고성장 틈새 시장을 우선시하고 있음이 드러나고 있습니다. 미스칸서스 섬유는 본질적으로 밀도가 낮기 때문에 더 가벼운 삽입재를 사용할 수 있어, 택배 업체가 부과하는 부피 중량 요금을 절감할 수 있습니다. 이를 통해 지속가능성에 기여할 뿐만 아니라, 명확한 경제적 이점도 얻을 수 있습니다. Fiberdom 및 Kiefel의 드라이 포밍 사업(2026년 2분기 시범 생산 예정)과 같은 기술 제휴를 통해, 보호 용도는 정밀한 표면 마감과 엄격한 공차가 요구되는 화장품 트레이 분야로 확대되고 있습니다. 자동화된 고속 생산 라인이 가동되기 시작하면, 보호 포장은 미스칸투스 기반 포장 시장 전체에서 주요 성장 동력으로 부상하며, 외식 산업용 포맷을 능가할 전망입니다.

지역별 분석

유럽은 2025년에 매출 점유율 38.21%를 유지했습니다. 이는 2030년까지 모든 포장재를 재활용 가능하거나 퇴비화 가능하도록 하는 명확한 규제 일정에 힘입은 것으로, 각 브랜드는 규정이 시행되기 훨씬 전에 규정을 준수하는 공급망을 확보해야만 하는 상황에 놓여 있습니다. 영국의 생산자는 2024년에 6,000-8,000헥타르의 미스칸서스를 재배하여, 다년 계약에 따라 혐기성 소화 발전 방식을 통해 연간 1만 톤을 처리하는 Fibrepac사의 링컨셔 공장에 원료를 공급했습니다. 공통농업정책(CAP)의 보조금을 통해 농가에는 매년 헥타르당 600-800유로(660-880달러)가 지급되고 있으며, 이는 안정적인 농가 출하 가격을 뒷받침하고 가공업체의 장기 계약 위험을 줄여주고 있습니다. 스트라 엔소가 2025년에 매트릭스 팩사의 소수 지분을 인수함에 따라, 유럽의 3개 하위 지역에 걸쳐 있는 8개의 성형 섬유 공장에 즉시 접근할 수 있게 되었으며, 이를 통해 지역 내 공급망이 강화되고 물류 과정에서 발생하는 배출량이 감소했습니다. 유럽투자은행이 에너지 사용량을 65% 절감하는 건식 성형 자동화 기술에 대해 풀팩(PulPac)에 2,000만 유로를 대출해 준 것은 기관 투자자들의 신뢰를 여실히 보여주는 동시에, 차세대 섬유 기술에 대한 지속적인 지원을 의미합니다.

아시아·태평양 지역은 2031년까지 연평균 10.45%의 성장률을 나타낼 것으로 전망됩니다. 이는 Minerals Technologies의 데이터에 따르면, 340억 달러가 넘는 섬유 포장 인프라가 건설 중이며, 그중 중국만 해도 230억 달러에 가까운 비중을 차지하고 있기 때문입니다. 베트남과 필리핀 등 아세안(ASEAN) 회원국들은 이미 2025년에 확대 생산자 책임(EPR) 제도를 도입했으며, 인도네시아, 말레이시아, 태국도 2027년까지 유사한 규제를 최종 확정할 예정이어서, 정책 측면에서 동조적인 호재가 발생할 것으로 보입니다. 지금까지 바이오매스 사업에서는 대나무와 스위치그래스가 우선적으로 사용되어 왔기 때문에 현지 미스칸투스 재배 면적은 여전히 소규모이며, 많은 가공업체들이 수입 펄프에 의존하고 있습니다. 그 결과, 입고 비용은 유럽의 벤치마크를 상회하고 있습니다. 매트릭스 팩사의 태국 공장은 동남아시아 외식 산업 바이어들에 대한 배송 경로를 단축함으로써 어느 정도 위험을 분산시키고 있지만, 안정적인 원료 공급은 여전히 해당 지역에서의 재배 확대에 달려 있습니다. 각국 정부는 미개발 지역에서 시범 프로그램을 시작하고 있지만, 본격적인 규모의 확대는 예측 기간 후반이 되어야 실현될 가능성이 있습니다.

북미는 아직 상업화의 초기 단계에 있지만, 주요 투자 동향을 보면 가공 과정의 병목 현상이 해소된다면 급속한 추격이 예상됩니다. 제네라사는 2025년 테네시주에서 3억 4,000만 달러 규모의 확장 공사를 완료하고, 연간 생산 능력 20억 개를 넘는 세계 최대 규모의 초섬유 포장 라인을 구축했습니다. 미국의 7개 주에서는 재활용이 불가능한 포장재에 대해 생산자 부담금을 부과하고 있으며, 이에 따라 전국적으로 사업을 전개하는 레스토랑 체인 및 전자상거래 소매업체들은 내륙 지역으로의 진출에 앞서 연안 시장에서 성형 섬유의 시범 도입을 추진하고 있습니다. 베터 어스(Better Earth)의 ‘파머스 파이버 컬렉션(Farmer's Fiber Collection)’은 중서부 지역 생산자로부터 직접 미스칸서스를 조달함으로써, 원료의 추적 가능성과 안정적인 가격 책정을 모두 실현하고 있습니다. 한편, 미국 농무부(USDA)의 비용 분담 보조금은 새로운 다년생 바이오매스 재배 면적의 도입 장벽을 낮추고 있습니다. 캐나다와 멕시코는 이러한 동향을 주시하고 있지만, 현재로서는 비목재 펄프 전용 생산 라인을 보유하고 있지 않아, 단기적인 무역 흐름은 국경을 넘는 공급이 주를 이룰 것으로 보입니다. 남미, 중동 및 아프리카는 현재로서는 아직 제한적이지만, 브라질과 아랍에미리트의 정책 입안자들은 미래의 순환형 경제 이니셔티브를 위한 청사진으로서 유럽의 규제를 높이 평가했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 전망과 시나리오 분석

KTH 26.06.24According to Mordor Intelligence, the miscanthus-Based packaging market size is projected to be USD 67.46 million in 2025, USD 78.53 million in 2026, and reach USD 115.67 million by 2031, growing at a CAGR of 8.05% from 2026 to 2031.

This report is Segmented by Packaging Format (Clamshell Containers and Trays, Plates and Bowls, Protective Packaging, and More), End-Use Industry (Foodservice, Personal Care and Cosmetics, Retail and E-Commerce, Food and Beverage, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Miscanthus-Based Packaging Market Trends and Insights

Regulatory Push Toward Reduction of Plastic Packaging

The European Union Packaging and Packaging Waste Regulation obliges all packaging to be recyclable or compostable by 2030, effectively disqualifying multilayer plastics and most polystyrene items, and thereby forcing procurement teams to reassess substrate choices. Seven U.S. states adopted extended producer-responsibility laws during 2024-2025, adding fee mechanisms that tilt economics in favor of compostable fiber alternatives and shorten decision cycles for national brands. ASEAN member countries such as Vietnam and the Philippines already require EPR compliance, while Indonesia, Malaysia, and Thailand are phasing in similar mandates by 2027, giving regional retailers a clear regulatory horizon. These synchronized policies compress adoption timelines, making the two-year window before enforcement a critical commercialization phase for miscanthus converters. Because the material meets EN 13432 compostability without synthetic binders, producers avoid costly reformulation rounds that often delay wood-pulp solutions.

Expansion of Fiber-Based Alternatives to Expanded Polystyrene

Municipal polystyrene bans now apply in more than 200 jurisdictions worldwide, yet end users still demand thermal insulation and cushioning metrics that historically required EPS. PulPac's dry-molded fiber process achieves 3.5-second cycle times, eliminates water-intensive drying, and yields complex geometries that match EPS drop-test performance while reducing energy consumption by 65%. Graphic Packaging earmarked USD 85 million in 2024 to install replicated capacity for cold-chain containers, confirming that large incumbents see molded fiber as an EPS successor for food and pharmaceuticals. Because miscanthus fiber has lower bulk density compared with hardwood pulp, finished inserts weigh less, which directly reduces freight fees on e-commerce parcel networks where dimensional weight influences cost. This shipping advantage resonates with logistics managers, giving the material a value proposition that extends beyond sustainability narratives.

Limited Industrial-Scale Processing and Pulping Infrastructure

Worldwide, fewer than 15 commercial non-wood pulping lines are operational, compared with more than 400 wood-pulp mills, underscoring a glaring scale deficit that constrains rapid miscanthus uptake. ANDRITZ partnered with Genera in 2025 to commission the first dedicated U.S. grass-fiber line, yet the 18-to-24-month installation window means meaningful volumes will not reach converters until late 2027. Equipment costs exceed wood-pulp analogs by 25-30% because silica embedded in grasses accelerates digester wear, adding to start-up hurdles and complicating financing models. Minerals Technologies opened three molded-fiber satellites in 2025 that still rely on imported non-wood pulp, illustrating how downstream capacity can race ahead of upstream processing assets. Closing the infrastructure gap quickly is therefore pivotal for maintaining the current adoption trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Non-Wood Fibers by Brands and Converters

- Supply Chain Diversification Away from Wood-Based Raw Materials

- Cost Competitiveness Relative to Established Fiber Source

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clamshell containers and trays commanded 42.34% of miscanthus-based packaging market share in 2025, fueled by quick-service restaurants that moved early to replace polystyrene hinged boxes ahead of the August 2026 plastic bans in Europe and several U.S. municipalities. Huhtamaki expanded molded-fiber capacity across nine global plants between 2024 and 2025, aligning supply with anticipated spikes in compliant packaging demand and reflecting confidence in grass-fiber scalability. Sabert's Pulp-it! line posted 30% sales growth in Asia-Pacific institutional catering during 2024, showing that adoption momentum is no longer confined to European markets. However, growth in Europe is beginning to plateau as early adopters delay reorder cycles to synchronize with PFAS-free coating availability, indicating that future volume gains will rely more on geographic expansion than on per-operator penetration. Consequently, the miscanthus-based packaging market size for clamshells is expected to rise steadily but at a moderating pace compared with nascent application areas.

Protective packaging is on a steeper trajectory, projected to grow 9.78% annually through 2031 as e-commerce fulfillment centers and electronics brands phase out EPS void-fill in favor of compostable molded-fiber inserts compliant with ASTM D6400. Storopack debuted grass-fiber cushioning in 2024, and Cascades allocated more than 60% of its USD 350 million molded-fiber capital plan to protective formats, underscoring how converters are prioritizing this high-growth niche. Miscanthus fiber's inherently lower density enables lighter inserts that trim dimensional-weight charges imposed by parcel carriers, providing a hard-dollar economic incentive on top of sustainability credentials. Technology partnerships such as Fiberdom and Kiefel's dry-forming initiative, scheduled for Q2 2026 pilot runs, expand protective applications into cosmetics trays requiring precise surface finishes and tight tolerances. As automated high-speed lines come online, protective packaging is poised to eclipse foodservice formats as the primary growth driver within the overall miscanthus-based packaging market.

Geography Analysis

Europe retained a 38.21% revenue share in 2025, driven by a clear regulatory timetable that requires all packaging to be recyclable or compostable by 2030, forcing brands to lock in compliant supply well before enforcement. United Kingdom growers cultivated between 6,000 and 8,000 hectares of miscanthus in 2024, delivering feedstock under multiyear contracts to Fibrepac's Lincolnshire plant that processes 10 000 tonnes annually using anaerobic-digestion power. Common Agricultural Policy subsidies pay farmers EUR 600-800 (USD 660-880) per hectare each year, underpinning stable farm-gate prices that de-risk long-term contracts for converters. Stora Enso's 2025 minority stake in Matrix Pack grants immediate access to eight molded-fiber plants across three European subregions, tightening regional loops that cut logistics emissions. Institutional confidence is evident in the European Investment Bank's EUR 20 million loan to PulPac for dry-forming automation that slices energy use by 65%, signaling continued backing for next-generation fiber technologies.

Asia-Pacific is projected to grow 10.45% annually through 2031 because more than USD 34 billion in fiber-packaging infrastructure is under construction, with China alone accounting for nearly USD 23 billion according to Minerals Technologies data. ASEAN members such as Vietnam and the Philippines already implemented extended producer responsibility in 2025, while Indonesia, Malaysia, and Thailand will finalize comparable mandates by 2027, creating a synchronized policy tailwind. Local miscanthus acreage remains small because biomass programs historically favored bamboo and switchgrass, so many converters rely on imported pulp, which lifts landed costs above European benchmarks. Matrix Pack's Thai facility offers a partial hedge by shortening delivery routes for Southeast Asian foodservice buyers, yet consistent feedstock supply still depends on expanded regional cultivation. Governments are beginning pilot programs on marginal land, but meaningful scale may not materialize until the latter half of the forecast period.

North America is at an earlier commercialization stage, yet anchor investments point toward rapid catch-up once processing bottlenecks ease. Genera completed a USD 340 million expansion in Tennessee during 2025, creating the world's largest grass-fiber packaging line with capacity exceeding 2 billion units annually. Seven U.S. states impose producer fees on non-recyclable packaging, pushing national restaurant chains and e-commerce retailers to trial molded fiber in coastal markets before rolling out inland. Better Earth's Farmer's Fiber Collection sources miscanthus directly from growers in the Midwest, pairing feedstock traceability with predictable pricing, while USDA cost-share grants lower establishment hurdles for new perennial biomass acreage. Canada and Mexico monitor these developments but currently lack dedicated non-wood pulping lines, suggesting cross-border supply will dominate near-term trade flows. South America and the Middle East and Africa remain marginal today, although policymakers in Brazil and the United Arab Emirates are assessing European regulations as potential blueprints for future circular-economy initiatives.

- Genera Inc.

- Fibrepac

- Mohawk (Fedrigoni Group)

- The Green Revolution BV

- Better Earth LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Key Insights on Miscanthus as an Alternative Fiber in Packaging

- 3.2 Commercial Readiness and Market Maturity Assessment

- 3.3 Strategic Positioning within the Global Fiber-Based Packaging Transition

- 3.4 Key Demand Drivers and Structural Constraints

- 3.5 High-Potential Application Areas with Near-Term Commercial Viability

- 3.6 Analyst Outlook on Scalability, Cost Competitiveness, and Adoption Timeline

4 MARKET LANDSCAPE

- 4.1 Current Stage of Market Development (Pilot to Early Commercialization)

- 4.2 Evolution of Miscanthus Utilization in Packaging Applications

- 4.3 Positioning within the Broader Fiber-Based Packaging Ecosystem

- 4.4 Market Dynamics

- 4.4.1 Market Drivers

- 4.4.1.1 Regulatory Push Toward Reduction of Plastic Packaging

- 4.4.1.2 Increasing Adoption of Non-Wood Fibers by Brands and Converters

- 4.4.1.3 Supply Chain Diversification Away from Wood-Based Raw Materials

- 4.4.1.4 Expansion of Fiber-Based Alternatives to Expanded Polystyrene (EPS)

- 4.4.1.5 Alignment with Regenerative Agriculture and Carbon Reduction Goals

- 4.4.1.6 Rising Investments in Regional Dry-Molded Fiber Capacity

- 4.4.2 Market Restraints

- 4.4.2.1 Limited Industrial-Scale Processing and Pulping Infrastructure

- 4.4.2.2 Cost Competitiveness Relative to Established Fiber Source

- 4.4.2.3 Technical Limitations in Barrier Properties and Functional Coatings

- 4.4.2.4 Absence of Standardized Certification Frameworks for Non-Wood Fibers

- 4.4.3 Emerging Trends and Innovation Developments

- 4.4.3.1 Increasing Use of Blended Fiber Formulations (Miscanthus with Wood/Recycled Fiber)

- 4.4.3.2 Adoption of Dry Molded Fiber and Low-Water Processing Technologies

- 4.4.3.3 Development of Localized and Integrated Supply Chain Models

- 4.4.3.4 Advancements in Bio-Based Barrier Coatings and PFAS-Free Solutions

- 4.4.1 Market Drivers

- 4.5 Value Chain Analysis: From Feedstock to Finished Packaging

- 4.5.1 Upstream Analysis: Cultivation and Feedstock Supply

- 4.5.1.1 Yield economics and harvesting cycles

- 4.5.1.2 Farmer participation models and incentives

- 4.5.1.3 Regional supply potential

- 4.5.2 Midstream Analysis: Fiber Processing and Pulp Production

- 4.5.2.1 Mechanical and chemical pulping processes

- 4.5.2.2 Fiber preprocessing and quality optimization

- 4.5.2.3 Blending strategies and material consistency

- 4.5.3 Downstream Analysis: Packaging Conversion Technologies

- 4.5.3.1 Wet molded fiber processes

- 4.5.3.2 Dry molded fiber processes

- 4.5.3.3 Thermoforming and shaping technologies

- 4.5.1 Upstream Analysis: Cultivation and Feedstock Supply

- 4.6 Distribution, Branding, and End-Use Integration

- 4.6.1 Technology Landscape and Processing Capabilities

- 4.6.2 Fiber Extraction and Pulping Technologies

- 4.6.3 Barrier Coating and Functionalization Technologies

- 4.6.4 Automation, Efficiency Improvements, and Scale-Up Innovations

- 4.6.5 Intellectual Property Landscape and Proprietary Technologies

- 4.7 Cost Structure and Economic Feasibility Analysis

- 4.7.1 Cost Breakdown Across the Value Chain

- 4.7.2 Comparative Cost Analysis with Wood Pulp and Alternative Fibers

- 4.7.3 Capital Investment Requirements for Processing and Conversion

- 4.7.4 Pricing Trends and Margin Considerations

- 4.8 Regulatory Landscape and Compliance Framework

- 4.8.1 Global Regulations Impacting Fiber-Based Packaging

- 4.8.2 Compostability and Biodegradability Standards

- 4.8.3 Food Contact and Safety Compliance Requirements

- 4.8.4 Certification Challenges for Non-Wood Fiber Materials

- 4.9 Miscanthus as a Lignocellulosic Fiber Source for Packaging Applications

- 4.9.1 Agronomic and Supply Characteristics of Miscanthus

- 4.9.1.1 Yield profile and harvesting cycles

- 4.9.1.2 Geographic suitability and cultivation conditions

- 4.9.2 Comparative Assessment with Alternative Fiber Sources

- 4.9.2.1 Wood pulp (hardwood and softwood)

- 4.9.2.2 Agricultural residues (bagasse, wheat straw, rice husk)

- 4.9.2.3 Dedicated fiber crops (bamboo, hemp)

- 4.9.3 Fiber Chemistry and Material Performance Characteristics

- 4.9.3.1 Cellulose, hemicellulose, and lignin composition

- 4.9.3.2 Fiber morphology and strength properties

- 4.9.3.3 Implications for different packaging formats

- 4.9.4 Environmental and Sustainability Performance

- 4.9.4.1 Carbon sequestration potential

- 4.9.4.2 Water and agrochemical requirements

- 4.9.4.3 Land use efficiency and non-competitive cultivation

- 4.9.5 Relevance of Miscanthus in Next-Generation Fiber-Based Packaging Systems

- 4.9.1 Agronomic and Supply Characteristics of Miscanthus

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Format

- 5.1.1 Clamshell Containers and Trays

- 5.1.2 Plates and Bowls

- 5.1.3 Protective Packaging (Cushioning, Inserts)

- 5.1.4 Other Packaging Formats

- 5.2 By End-use Industry

- 5.2.1 Foodservice

- 5.2.2 Personal Care and Cosmetics

- 5.2.3 Retail and E-commerce

- 5.2.4 Food and Beverage

- 5.2.5 Other End-use Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Rank Analysis

- 6.4 Company Profiles (Includes Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Genera Inc.

- 6.4.2 Fibrepac

- 6.4.3 Mohawk (Fedrigoni Group)

- 6.4.4 The Green Revolution BV

- 6.4.5 Better Earth LLC

- 6.5 Strategic Opportunity Mapping

- 6.5.1 High-Potential Application Areas for Market Entry

- 6.5.2 White Space Opportunities Across Regions and Value Chain Segments

- 6.5.3 Investment Opportunities in Processing and Conversion Infrastructure

- 6.5.4 Potential for Vertical Integration and Closed-Loop Systems

- 6.6 Risk Assessment and Market Uncertainty Analysis

- 6.6.1 Feedstock Supply and Agricultural Risks

- 6.6.2 Technology Scale-Up and Commercialization Risks

- 6.6.3 Market Adoption and Demand-Side Uncertainty

- 6.6.4 Competitive and Substitution Risks