|

시장보고서

상품코드

2063490

지방흡입 기기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Liposuction Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

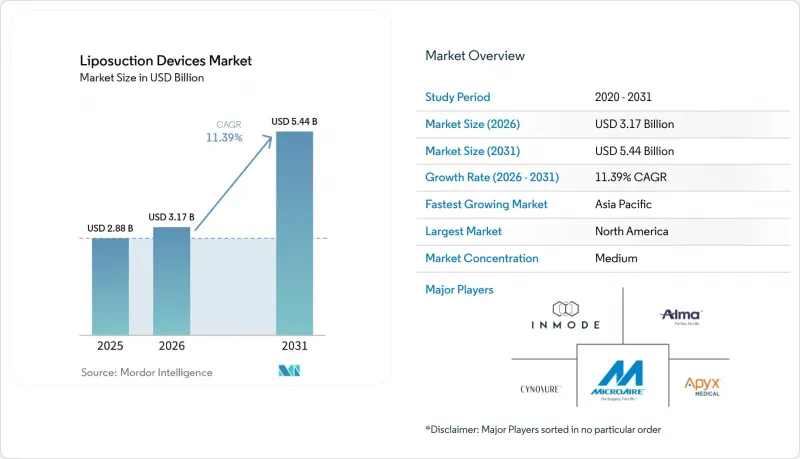

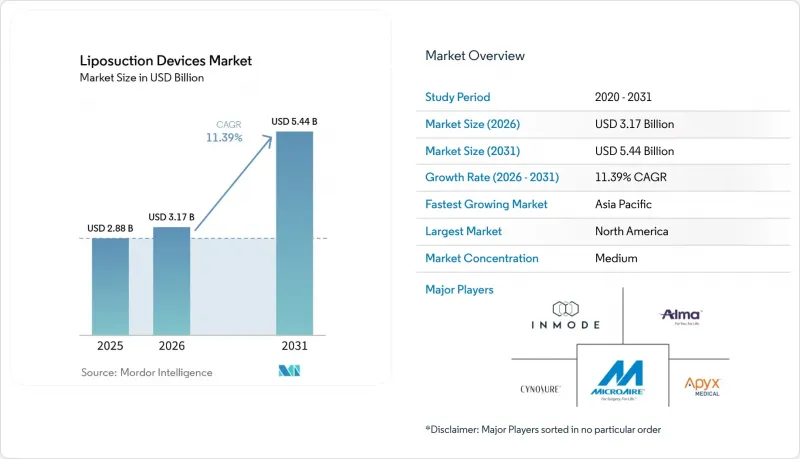

Mordor Intelligence에 의하면, 지방흡입 기기 시장 규모는 2025년 28억 8,000만 달러, 2026년 31억 7,000만 달러에서 2031년까지 54억 4,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 11.39%를 나타낼 것으로 예측됩니다.

본 보고서는 기술/방식(흡입식, 초음파식 등), 제품 유형(휴대용 시스템, 독립형 시스템), 최종 사용자(병원 등), 지역(북미, 유럽, 아시아·태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 지방흡입 기기 시장 동향 및 분석

지방흡입 시술 건수 사상 최고치 기록, 고해상도 바디 컨투어링으로의 전환

선진 지역의 시술 총 건수는 사상 최고치를 기록했으나, 그 배경에 있는 수요는 대량의 지방흡입보다는 운동선수처럼 탄탄한 바디라인을 만드는 쪽으로 변화하고 있습니다. 고해상도의 바디 컨투어링에는 섬유성 부위를 선택적으로 유화시키는 초음파 및 레이저 기기가 필수적입니다. ‘스키니 BBL’은 체질량지수(BMI)가 23 미만인 환자를 대상으로 한, 적은 양의 지방을 이식하면서 형태를 중시하는 지방 이식의 대표적인 사례입니다. 정밀한 지방 채취에 따라 클로즈드 루프 캐뉼라와 실시간 영상 진단의 중요성이 커지고 있으며, 제조업체들은 통합형 소형 콘솔 개발에 주력하고 있습니다. 세계 시술 동향의 분기점으로 미국의 확대에 반해 일부 신흥국에서는 성장세가 주춤하는 양상이 나타나고 있음은 환율 변동과 재량 지출의 변화가 전반적인 수요를 억제하지 않으면서 지역별 구성을 어떻게 변화시키는지를 보여주고 있습니다.

에너지 보조 요법의 급속한 보급

초음파, 파워, 레이저를 병용한 시스템은 수술 시간을 단축하고 외과의사의 피로를 덜어줍니다. MicroAire사의 PAL 플랫폼은 해당 회사가 실시한 시험에서 수동 흡입에 비해 분당 흡입량이 훨씬 더 많은 것으로 확인되었습니다. 레이저 기기는 열 응고 작용을 통해 내출혈을 줄이고 콜라겐 재생을 촉진함으로써, 단 한 번의 시술로 지방흡입과 피부 탄력 개선을 동시에 이루어낼 수 있게 해줍니다. 2025년 5월에 승인된 Apyx Medical사의 AYON은 헬륨 플라즈마를 유도하여 피하에서 제어된 응고를 수행하며, 이미 파워 어시스트 적응증 획득을 목표로 하고 있습니다. 여러 에너지원을 단일 콘솔로 통합함으로써 진료소의 설비 투자 비용을 절감하고 직원 교육을 간소화할 수 있어, 프리미엄 시장에서 기존의 흡입 전용 기기를 빠르게 대체하는 추세가 가속화되고 있습니다.

비침습적인 바디 컨투어링 대안이 외과적 지방흡입에 쓰이던 비용을 다른 곳으로 돌리고 있습니다.

크리오리포리시스, HIFU, 그리고 주사형 지방분해제는 회복 기간이 전혀 필요 없습니다는 점을 중시하는 위험을 회피하려는 성향의 고객층의 요구를 충족시키고 있습니다. 애비(AbbVie)사의 쿨스컬프팅(CoolSculpting)은 마취 없이 12주 만에 지방층을 8.6% 감소시켜, 원래라면 지방흡입 수술을 예약했을 환자들을 끌어들이고 있습니다. 메디컬 스파에 도입하는 것은 수술실에 투자하는 것보다 쉽지만, 일부 도시 시장에서는 재량 자금이 분산되어 기기 이용률이 낮아지는 경향이 있습니다.

부문별 분석

흡입 보조형 기기는 2025년 매출의 46.9%를 차지하고 연평균 성장률(CAGR) 12.1%를 나타낼 것으로 예측되며, 지방흡입 기기 시장 규모에서 주도적인 위치를 차지하고 있습니다. 초음파, 파워, 레이저 시스템이 정밀도 면에서 장점을 내세우고 있음에도 불구하고, 이 기술의 간편함, 낮은 초기 투자 비용, 그리고 외과의사의 익숙함이 시장 점유율을 지탱하고 있습니다.

에너지 보조형 플랫폼은 북미 및 서유럽에서 고해상도 및 섬유성 조직 사례에 대한 보급이 확대되고 있습니다. 레이저 및 플라즈마 방식은 응고와 탄력 강화 기능을 결합함으로써 시술의 부가가치를 높이고 있습니다. 그러나 병원이나 가격에 민감한 클리닉에서는 여전히 비용 효율이 높은 흡입 전용 콘솔이 주류를 이루고 있으며, 이로 인해 치료 방식의 전환이 지연되면서 기존 시스템의 지방흡입 기기 시장 점유율이 견조하게 유지되고 있습니다.

지역별 분석

북미는 2025년 매출의 52.86%를 차지했으며, 미국에서 34만 9,728건의 수술 건수와 ASC(외래수술센터(ASC))에서의 수술을 우대하는 CMS(미국 의료보험서비스센터)의 보상 방침이 명확해진 것이 이를 견인했습니다. 캐나다는 보완적인 수요를 제공하고 있으며, 멕시코는 비용 절감을 원하는 국경을 넘는 환자들을 끌어모으고 있습니다. 비침습적 치료법과의 경쟁이 가장 치열한 지역이지만, 에너지 보조형 기술 분야의 혁신 기업들은 여전히 이 지역에 본사를 두고 있으며, 고가 기기 판매를 뒷받침하고 있습니다.

유럽에서는 젊은 층의 관심을 식게 만드는 광고 규제와 주요 경제권에서의 거시경제적 신중한 태도로 인해 제약을 받고 있지만, 도입 속도는 완만하긴 해도 꾸준한 성장세를 보이고 있습니다. 독일의 8만 519건에 달하는 시술 건수가 유럽 전체의 규모를 지탱하고 있으며, 영국, 프랑스, 이탈리아가 상위권을 차지하고 있습니다. 더욱 엄격해진 마케팅 규제로 인해 클리닉들은 화려함보다는 안전성 입증을 중시하도록 유도되고 있으며, 이에 따라 실증 데이터가 공개된 초음파 및 RF 시스템을 도입하는 추세가 확대되고 있습니다.

아시아태평양은 태국과 한국의 의료 관광 회랑, 그리고 중국과 인도네시아 전역에서 확대되고 있는 도시 중산층에 힘입어 연평균 성장률(CAGR) 12.0%의 성장 궤도에 올라섰습니다. 중국의 규제 완화는 Solta가 2025년에 유통업체을 인수하도록 촉진하며, 장기적인 의지를 강조하는 것입니다. 2023년 시술 건수 기준으로 세계 4위를 차지한 인도는 영어로 제공되는 의료 서비스와 비용 면에서의 우위를 바탕으로, 지방흡입 기기 시장의 향후 성장에 있어 이 지역을 최전선에 위치시키고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the liposuction devices market size is projected to expand from USD 2.88 billion in 2025 and USD 3.17 billion in 2026 to USD 5.44 billion by 2031, registering a CAGR of 11.39% between 2026 to 2031.

This report is Segmented by Technology/Modality (Suction-Assisted, Ultrasound-Assisted, and More), Product Type (Portable Systems, Stand-Alone Systems), End User (Hospitals, and More), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Liposuction Devices Market Trends and Insights

Liposuction Volumes at Record Highs; Shift to High-Definition Contouring

Aggregate procedures reached historic highs in developed regions, yet underlying demand now centers on athletic etching rather than bulk extraction. High-definition sculpting depends on ultrasound and laser devices that selectively emulsify fibrous zones. The "skinny BBL" exemplifies low-volume, shape-focused grafting among patients with body mass indices below 23. Precision harvest elevates the role of closed-loop cannulae and real-time imaging, motivating manufacturers toward integrated, small-footprint consoles. Global procedure divergence-expansion in the United States versus softness in some emerging economies-illustrates how currency swings and shifts in discretionary spending alter the regional mix without suppressing overall demand.

Rapid Adoption of Energy-Assisted Modalities

Ultrasound-, power-, and laser-assisted systems shorten operating time and reduce surgeon fatigue; MicroAire's PAL platform extracted significantly more volume per minute than manual suction in company trials. Laser devices add thermal coagulation, reducing bruising and stimulating collagen renewal, enabling combined liposuction and tightening in a single session. Apyx Medical's AYON, cleared in May 2025, channels helium plasma for controlled subsurface coagulation and is already pursuing a power-assisted indication. Bundling multiple energy sources into a single console reduces practice capital outlay and simplifies staff training, spurring rapid replacement of legacy suction-only machines in premium markets.

Non-Invasive Body-Contouring Alternatives Divert Spend from Surgical Lipo

Cryolipolysis, HIFU, and injectable lipolytics satisfy a risk-averse cohort that values zero downtime. AbbVie's CoolSculpting delivers an 8.6% reduction in fat layer in 12 weeks with no anesthesia, siphoning patients who might otherwise book suction procedures. Medical-spa rollout is easier than surgical-suite investment, but it fragments discretionary dollars and tapers device utilization rates in some urban markets.

Other drivers and restraints analyzed in the detailed report include:

- Migration to Outpatient Settings Enabled by Tumescent Anesthesia

- APAC Demand Acceleration via Medical Tourism and Rising Middle-Class Incomes

- Regulatory and Safety Communications Temper Energy-Device Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Suction-assisted devices accounted for 46.9% of 2025 revenue and are projected to post a 12.1% CAGR, anchoring the liposuction devices market size leadership. The technique's simplicity, low capital entry, and surgeon familiarity support its share, even as ultrasound, power, and laser systems pitch precision benefits.

Energy-assisted platforms are penetrating high-definition and fibrous-tissue cases in North America and Western Europe. Laser and plasma variants bundle coagulation and tightening, thereby enhancing the procedure's value. Yet hospitals and price-sensitive clinics still default to cost-efficient suction-only consoles, slowing modal shift and keeping the liposuction devices market share of traditional systems resilient.

Geography Analysis

North America generated 52.86% of 2025 revenue, powered by 349,728 U.S. procedures and CMS reimbursement clarity that favors ASC-based operations. Canada supplies complementary demand, while Mexico attracts cross-border patients seeking cost relief. Non-invasive competition is strongest here, yet energy-assisted innovators remain headquartered in the region, sustaining premium device sales.

Europe delivered steadily, if slower, uptake, constrained by advertising curbs that dampen youthful interest and macroeconomic caution in major economies. Germany's 80,519-procedure base anchors continental volumes, with the United Kingdom, France, and Italy rounding out the top tier. Stricter marketing codes are nudging clinics to emphasize safety credentials over glamor, influencing modal mix toward ultrasound and RF systems with published evidence.

Asia-Pacific is on track for a 12.0% CAGR, driven by surgical tourism corridors in Thailand and South Korea, and by a swelling urban middle class across China and Indonesia. China's regulatory streamlining prompted Solta's 2025 distributor acquisition, underscoring long-run commitment. India, fourth worldwide in 2023 cases, benefits from English-language care and cost arbitrage, placing the region at the vanguard of future growth in the liposuction devices market.

- Alma Lasers

- Apyx Medical

- Ardo Medical

- BIcakcIlar

- Black & Black Surgical

- CHEIRON

- Cynosure

- DEKA

- Euromi

- Genesis Biosystems

- Human Med

- InMode

- M.D. Resource

- MicroAire

- Moller Medical

- Nouvag

- Solta Medical

- Tulip Medical Products

- Wells Johnson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Liposuction Volumes at Record Highs; Shift to High-Definition Contouring

- 4.2.2 Rapid Adoption of Energy-Assisted Modalities

- 4.2.3 Migration To Outpatient Settings Enabled by Tumescent Anesthesia and Safety Data

- 4.2.4 APAC Demand Acceleration Via Medical Tourism and Rising Middle-Class Incomes

- 4.2.5 Fat Grafting Use-Cases Drive Demand for Gentler Harvest Systems and Closed-Loop Processing

- 4.2.6 Post-Lipo Skin Tightening Becoming Standard of Care

- 4.3 Market Restraints

- 4.3.1 Non-Invasive Body Contouring Alternatives Divert Spend from Surgical Lipo

- 4.3.2 Regulatory And Safety Communications Temper Energy-Device Adoption and Claims

- 4.3.3 Procedure Risks and Medico-Legal Scrutiny, Especially In Combined Surgeries

- 4.3.4 Ad Restrictions for Cosmetic Interventions To Under-18s Curb DTC Funnels

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Suction-assisted liposuction

- 5.1.2 Ultrasound-assisted liposuction

- 5.1.3 Power-assisted liposuction

- 5.1.4 Laser-assisted liposuction

- 5.1.5 Water-jet assisted liposuction

- 5.1.6 RF-assisted lipo-coagulation

- 5.2 By Product Type

- 5.2.1 Portable Systems

- 5.2.2 Stand-alone Systems

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers (ASCs)

- 5.3.3 Cosmetic Surgery Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Alma Lasers

- 6.3.2 Apyx Medical

- 6.3.3 Ardo Medical

- 6.3.4 BIcakcIlar

- 6.3.5 Black & Black Surgical

- 6.3.6 CHEIRON

- 6.3.7 Cynosure

- 6.3.8 DEKA

- 6.3.9 Euromi

- 6.3.10 Genesis Biosystems

- 6.3.11 Human Med AG

- 6.3.12 InMode

- 6.3.13 M.D. Resource

- 6.3.14 MicroAire Surgical Instruments

- 6.3.15 Moller Medical

- 6.3.16 Nouvag

- 6.3.17 Solta Medical

- 6.3.18 Tulip Medical Products

- 6.3.19 Wells Johnson

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment