|

시장보고서

상품코드

2063493

흡입성 약물 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Inhalable Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

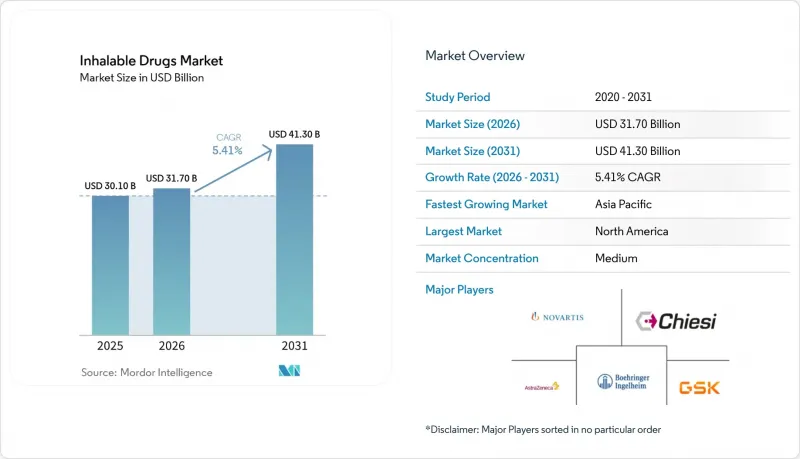

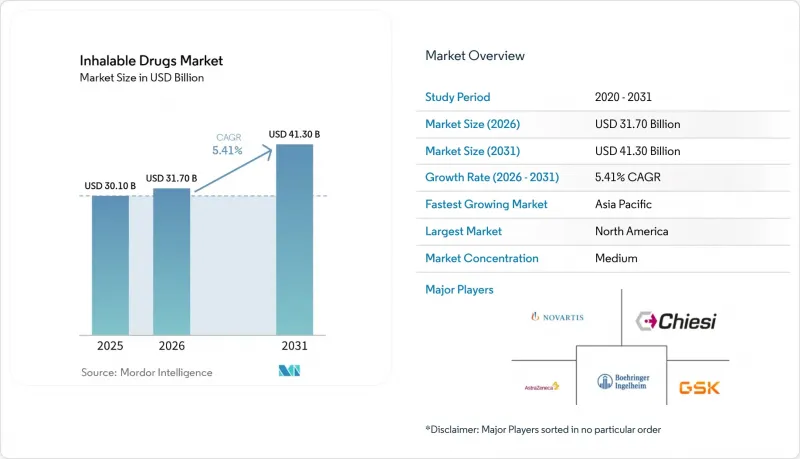

Mordor Intelligence에 의하면, 흡입성 약물 시장 규모는 2025년 301억 달러, 2026년 317억 달러에서 2031년까지 413억 달러로 확대되어 2026년부터 2031년까지 CAGR 5.41%를 나타낼 것으로 예측됩니다.

본 보고서는 적응증(천식, COPD, 낭포성 섬유증, 폐동맥 고혈압, 비결핵성 항산균 폐질환, 당뇨병), 제형(정량 분무식, 드라이 파우더, 네뷸라이저, 소프트 미스트), 최종 사용자(재택치료, 병원, 전문 클리닉), 유통 채널(소매, 병원, 온라인 약국), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계 흡입성 약물 시장 동향과 인사이트

천식 및 만성 폐쇄성 폐질환(COPD)의 전 세계적 부담 증가

미국 국립의학도서관의 2025년 기사에 따르면, 2050년까지 전 세계적으로 누적 155억 8,000만 건의 COPD 관련 악화가 발생할 것으로 예측되며, 이는 2025년 대비 584%의 상대적 증가를 의미합니다. LPG에 대한 보조금이 확대되고 있음에도 불구하고, 저소득 지역의 COPD 사례 중 40%는 여전히 실내에서 바이오매스를 연소하는 것이 원인입니다. 일본, 한국, 남유럽에서 고령화가 진행됨에 따라 다중 질환을 동시에 앓는 사례가 증가하고 있으며, 복합 흡입성 약물에 대한 수요가 높아지고 있습니다. 아시아태평양에서는 COPD 유병률이 연평균 2.1%씩 증가하고 있으며, 이는 호흡기과 진료 수용 능력을 초과하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 단시간 작용형 약물에 비해 높은 가격을 책정할 수 있는 유지 요법의 매출이 지속적으로 증가하고 있습니다.

고정 용량 듀얼/트리플 흡입기의 보급이 치료 성과를 향상시킵니다.

아스트라제네카의 KALOS 및 LOGOS 임상시험에서 3가지 유효 성분을 조합한 단일 흡입기를 사용한 경우, 이중 요법과 비교해 COPD 관련 입원이 24% 감소한 것으로 나타났으며, 이에 따라 독일과 영국에서는 보험 지급 기관에 의해 보험 적용 범위가 확대되었습니다. 키에지사의 505(b)(2) 경로를 통한 트리플 MDI 신청은 2026년 미국 승인을 목표로 하고 있으며, 현재 여러 기기를 병용하고 있는 120만 명의 환자층을 대상으로 하고 있습니다. 처방 의사들 사이에서는 조제 오류를 줄이고 6개월간 복약 지속률을 높이는 통합 요법에 대한 지지가 높아지고 있으며, 이는 단일제제인 LABA-ICS의 매출을 잠식하는 한편, 중증 환자군에서 브랜드 제품의 주도적 입지를 강화하고 있습니다.

치열해지는 제네릭 의약품 간의 경쟁과 가격 압박

여러 생물학적 동등성 의약품이 출시됨에 따라, 2022년부터 2025년까지 미국 내 MDI 처방 시장에서 제네릭 의약품의 점유율이 급격히 상승했고, 브랜드 의약품의 평균 판매 가격(ASP)은 3분의 1 수준으로 떨어졌습니다. 유럽이나 라틴아메리카에서는 직접적인 대체품이 없는 경우에도 입찰 제도에서 흡입기 가격이 제네릭 의약품 수준을 기준으로 삼게 된 반면, 미국의 PBM(의약품 혜택 관리 회사)은 최저 조달 비용 방식을 적용하고 있습니다. 이익률 감소로 인해 연구개발(R&D)은 진입 장벽이 높은 생물학적 제제와 의료기기의 결합으로 전환되고 있으며, 저분자 화합물의 점진적인 개선에는 충분한 자금이 투입되지 못하고 있습니다.

부문별 분석

COPD 매출은 연평균 성장률(CAGR) 5.83%로 확대되고 있으며, 2025년에는 흡입성 약물 시장 점유율 38.16%를 유지한 천식과 그 격차를 좁히고 있습니다. 신흥 시장에서 진단이 지연됨에 따라 환자들은 고가의 3제 병용 요법을 받을 수밖에 없으며, 또한 담배 연기에 노출됨에 따라 발병률은 계속 증가하고 있습니다. 낭포성 섬유증 치료제는 약 10만 명의 환자를 대상으로 하고 있으며, 하루에 한 번 투여하면 되는 만성 치료라는 장점이 있는 반면, 폐동맥 고혈압 흡입성 약물는 트레프로스티닐 DPI의 승인을 받아 2025년 매출에서 미미한 점유율을 기록했습니다. 비결핵성 항산균성 폐질환은 환경 내 에어로졸에 대한 노출로 인해 해마다 증가하고 있으며, 이로 인해 리포솜형 아미카신의 틈새 시장이 확대되고 있습니다. 당뇨병 흡입 요법은 보험사가 우선 주사 요법의 실패를 조건으로 삼고 있기 때문에 여전히 0.5% 미만의 미미한 점유율에 그치고 있습니다.

COPD의 진행에 따라, 제품 전략은 항염증제가 함유된 지속형 기관지 확장제로 재조정되고 있습니다. 유나이티드 테라퓨틱스(United Therapeutics)의 트레프로스티닐 DPI와 인스메드(InSmed)의 리포솜형 항생제는 환자 수가 적음에도 불구하고 견실한 가격 책정을 통해 이를 상쇄하며, 전신 투여 분야 및 희귀질환 분야로 전환되는 추세를 보이고 있습니다. 발병 연령이 높아짐에 따라, 각 제약사는 치료 지속률을 높이기 위해 원격 모니터링 및 투여 기술 지도 서비스를 패키지화하고 있으며, 이를 통해 가격만을 무기로 삼는 제네릭 의약품에 대한 진입 장벽이 형성되고 있습니다.

정량 분무 흡입기(MDI)는 2025년 흡입성 약물 시장에서 43.16%의 점유율로 1위를 차지하고, HFO-1234ze 추진제로의 전환에 따라 특허 기간이 연장됨에 따라 2031년까지 연평균 5.91%의 성장률을 보일 것으로 예측됩니다. 드라이 파우더 흡입기는 판매량에서 큰 점유율을 차지하며, 환경 의식이 높은 처방 의사들에게 지지를 받고 있지만, 흡기 유량 요건으로 인해 소아나 중증 COPD 환자에게는 사용이 제한되고 있습니다. 네뷸라이저는 조절이 어려운 병원 환경에서 여전히 필수적이며, 메쉬 기술 덕분에 치료 시간이 5분으로 단축되었습니다. 소프트 미스트 플랫폼은 50%의 폐 침착률을 달성하여 하루 1회 투여를 가능하게 합니다.

제품 포트폴리오 개편 비용과 추진제 공급 제약으로 인해, 기업들은 실제 사용 데이터를 수집할 수 있는 커넥티드 MDI로 전환해야 하는 상황에 직면해 있습니다. 이에 반해, 드라이 파우더 제제의 신규 진출기업들은 호흡 작동 방식의 간편함과 추진제를 일절 사용하지 않는다는 점을 강점으로 내세우고 있습니다. 따라서 경쟁 우위는 화학적 특성뿐만 아니라, 기기의 인체공학적 설계, 디지털 기능, 그리고 탄소 라벨 공개 여부에 따라 좌우될 것입니다.

지역별 분석

2025년 기준으로 북미는 46.18%의 점유율을 차지했습니다. 이는 특허 만료로 인해 제네릭 의약품 시장 침투가 진행되고 있으며, PBM(의약품 급여 관리 회사)이 가격 인하를 압박하고 있기 때문입니다. CMS(미국 의료보험서비스센터)의 연결형 기기 보험 급여는 Hailie 및 Digihaler 플랫폼의 보급을 가속화하며, 가격 하락을 부분적으로 상쇄하고 있습니다. 캐나다의 가격 협정에 따라 브랜드 제품 복합 흡입기의 비용이 최대 50% 절감된 반면, 멕시코에서는 적용 범위가 확대됨에 따라 제네릭 DPI(건조 분말 흡입기)의 판매량이 증가하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 6.10%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국은 2025년 보험 적용 목록에 18종의 흡입성 약물를 추가하여 환자의 본인 부담금을 대폭 줄였습니다. 인도의 ‘아유슈만 바라트’는 5억 명을 대상으로 하고 있지만, 농촌 지역의 유통 격차가 보급을 저해하고 있습니다. 지속적인 PM2.5 노출로 인해 COPD 발병률이 연간 2.1% 증가하고 있으며, 이에 따른 수요가 확대되고 있습니다. 일본에서는 비결핵성 항산균(NTM) 폐질환에 대한 리포솜형 아미카신이 승인된 반면, 호주에서는 3제 병용 요법에 대한 정부 지출을 억제하기 위한 위험 분담 계약이 체결되었습니다.

유럽은 큰 시장 점유율을 차지하고 있지만, 브랜드 제품의 가격을 제네릭 제품의 15% 이내로 제한하는 입찰 제도로 인해 그 성장세가 억제되고 있습니다. NHS의 탄소 발자국 데이터는 처방 의사들에게 건식 분말 흡입기로 전환할 것을 권장하고 있습니다. EMA의 저 GWP 지침은 MDI의 신속한 재조제를 촉진하고 있으며, 자본을 흡수하고 있습니다. 독일은 DiGA 규정에 따라 디지털 흡입기에 대해 보험 적용을 하고 있으며, 앱을 통해 비용 절감 효과가 입증될 경우 연간 250-400유로를 지급합니다. 중동 및 아프리카은 사우디아라비아의 ‘비전 2030’에 따른 지출에 힘입어 눈부신 성장을 보이고 있는 반면, 남미 지역의 성장은 브라질의 흡입기 보조금 및 아르헨티나에서의 DPI 국내 승인에 힘입어 지속되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the inhalable drugs market size is projected to expand from USD 30.10 billion in 2025 and USD 31.70 billion in 2026 to USD 41.30 billion by 2031, registering a CAGR of 5.41% between 2026 to 2031.

This report is Segmented by Indication (Asthma, COPD, Cystic Fibrosis, PAH, NTM Lung Disease, Diabetes), Dosage Form (Metered-Dose, Dry Powder, Nebulized, Soft Mist), End User (Homecare, Hospitals, Specialty Clinics), Distribution Channel (Retail, Hospital, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Inhalable Drugs Market Trends and Insights

Growing Global Burden of Asthma and COPD

According to a 2025 article by the National Library of Medicine, by 2050, it is projected that 15.58 billion cumulative COPD-related exacerbations will occur globally, a relative growth of 584% compared with 2025 . Indoor biomass combustion still accounts for 40% of COPD cases in low-income regions, even as LPG subsidies scale. Aging populations in Japan, South Korea, and Southern Europe are increasing multimorbidity, boosting demand for combination inhalers. COPD incidence is climbing 2.1% annually in Asia-Pacific, outpacing available pulmonology capacity. Together, these forces underpin sustained volume growth for maintenance therapies that command premium pricing relative to short-acting agents.

Uptake of Fixed-Dose Dual/Triple Inhalers Improving Outcomes

AstraZeneca's KALOS and LOGOS trials showed 24% fewer COPD-related hospitalizations with a single inhaler combining three active agents compared with dual therapy, prompting payer upgrades in Germany and the UK . Chiesi's triple MDI filing under the 505(b)(2) pathway targets U.S. approval in 2026 and a cohort of 1.2 million patients currently juggling multiple devices. Prescribers increasingly prefer integrated regimens that reduce pharmacy errors and improve six-month persistence, cannibalizing standalone LABA-ICS revenue but reinforcing branded leadership in severe disease.

Intensifying Generic Competition and Price Pressure

Generic share of U.S. MDI scripts jumped significantly from 2022 to 2025 as multiple bioequivalents launched, slashing branded ASPs by one-third. Tender systems in Europe and Latin America now benchmark inhaler prices to generic levels, even in the absence of direct substitutes, while PBMs in the U.S. enforce lowest-acquisition-cost formulas. Shrinking margins shift R&D toward high-barrier biologic-device combinations, leaving incremental small-molecule improvements underfunded.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Homecare and Digital/Smart Inhalers

- Broadening Access via Generics and Authorized Generics

- Inhaler Technique Errors and Adherence Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

COPD revenue is expanding at a 5.83% CAGR and is closing the gap with asthma, which retained 38.16% inhalable drugs market share in 2025. Late diagnoses in emerging markets push patients onto higher-priced triple regimens, and smoke exposure keeps incidence climbing. Cystic fibrosis therapies serve roughly 100,000 patients yet enjoy chronic daily dosing, while pulmonary arterial hypertension inhalables captured a modest share of 2025 revenue following treprostinil DPI approval. Non-tuberculous mycobacterial lung disease is advancing annually due to environmental aerosol exposure, widening the niche for liposomal amikacin. Diabetes inhalation therapy remains a sub-0.5% sliver because payers mandate failure on injections first.

COPD's acceleration realigns product strategy toward long-acting bronchodilators with anti-inflammatory co-formulation. United Therapeutics' treprostinil DPI and Insmed's liposomal antibiotic illustrate movement into systemic or orphan realms where robust pricing offsets small populations. As incidence skews older, developers bundle telemonitoring and technique-coaching services to bolster persistence, creating barriers to pure-price generics.

Metered-dose inhalation led with a 43.16% share of the inhalable drugs market in 2025 and will grow at 5.91% through 2031 as HFO-1234ze propellant conversions reset patent life. Dry-powder devices hold a significant share of volume and appeal to eco-conscious prescribers, yet inspiratory-flow demands limit pediatrics and severe COPD use. Nebulizers remain critical in hospital settings where coordination is impossible, and mesh technology reduces treatment time to 5 minutes. Soft-mist platforms achieve 50% lung deposition, supporting once-daily dosing.

Portfolio refresh costs and propellant supply constraints incentivize companies to pivot toward connected MDIs that capture real-world use data. Dry-powder entrants counter with breath-actuated simplicity and zero propellant footprint. Competitive positioning thus hinges on device ergonomics, digital overlays, and carbon-label disclosures rather than chemistry alone.

Geography Analysis

North America held a 46.18% share in 2025, as patent cliffs invite generic erosion and PBMs press for discounts. CMS reimbursement for connected devices accelerates adoption of Hailie and Digihaler platforms, partially offsetting price deflation. Canada's pricing alliance cut branded combination inhaler costs by up to 50%, while Mexico's expanded coverage lifts generic DPI volume.

Asia-Pacific is the fastest-growing region at a 6.10% CAGR. China added 18 inhalers to its 2025 reimbursement list, significantly slashing patients' out-of-pocket expenses. India's Ayushman Bharat covers 500 million people, but rural distribution gaps hamper uptake. Persistent PM2.5 exposure increases COPD incidence by 2.1% annually, expanding the addressable demand. Japan approved liposomal amikacin for NTM lung disease, while Australia struck risk-sharing deals to cap government spending on triple therapies.

Europe commands a significant share, tempered by tenders that pull branded prices within 15% of generics. NHS carbon footprint data motivates prescribers to switch to dry-powder devices. EMA low-GWP guidance spurs rapid MDI reformulations, absorbing capital. Germany reimburses digital inhalers under DiGA rules, paying EUR 250-400 annually when apps document savings. Middle East and Africa grow notabaly driven by Saudi Vision 2030 spending, while South America's rise follows Brazil's inhaler subsidies and Argentina's domestic DPI approval.

- AstraZeneca

- Boehringer Ingelheim

- Chiesi Farmaceutici

- Cipla

- Gilead Sciences

- Glenmark Pharmaceuticals

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Insmed

- Lupin

- MannKind

- Nephron Pharmaceuticals Corporation

- Novartis

- Organon LLC

- Orion

- Pharmaxis Ltd.

- Sandoz Group

- Teva Pharmaceutical Industries

- United Therapeutics

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Global Burden of Asthma And COPD

- 4.2.2 Uptake Of Fixed-Dose Dual/Triple Inhalers Improving Outcomes

- 4.2.3 Expansion Of Homecare and Digital/Smart Inhalers

- 4.2.4 Broadening Access Via Generics and Authorized Generics

- 4.2.5 Propellant Transition (low-GWP MDIs) Catalyzing Portfolio Refresh

- 4.2.6 Non-Respiratory Systemic Uses Via Inhalation (E.G., PAH DPI)

- 4.3 Market Restraints

- 4.3.1 Intensifying Generic Competition and Price Pressure

- 4.3.2 Inhaler Technique Errors and Adherence Gaps

- 4.3.3 Complex-Generic/Device Regulatory Hurdles Are Slowing Launches

- 4.3.4 Propellant Supply/Transition Constraints Elevating COGS

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Indication

- 5.1.1 Asthma

- 5.1.2 Chronic Obstructive Pulmonary Disease (COPD)

- 5.1.3 Cystic Fibrosis

- 5.1.4 Pulmonary Arterial Hypertension / PH-ILD

- 5.1.5 Non-tuberculous Mycobacterial (NTM) Lung Disease

- 5.1.6 Diabetes

- 5.2 By Dosage Form

- 5.2.1 Metered-Dose Inhalation

- 5.2.2 Dry Powder Inhalation

- 5.2.3 Nebulized Solutions

- 5.2.4 Soft Mist Inhalation

- 5.3 By End User

- 5.3.1 Homecare / Self-administration

- 5.3.2 Hospitals & Clinics

- 5.3.3 Specialty Clinics

- 5.4 By Distribution Channel

- 5.4.1 Retail Pharmacies

- 5.4.2 Hospital Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AstraZeneca plc

- 6.3.2 Boehringer Ingelheim International GmbH

- 6.3.3 Chiesi Farmaceutici S.p.A.

- 6.3.4 Cipla Ltd.

- 6.3.5 Gilead Sciences, Inc.

- 6.3.6 Glenmark Pharmaceuticals Ltd.

- 6.3.7 GSK plc

- 6.3.8 Hikma Pharmaceuticals PLC

- 6.3.9 Insmed Incorporated

- 6.3.10 Lupin Pharmaceuticals, Inc.

- 6.3.11 MannKind Corporation

- 6.3.12 Nephron Pharmaceuticals Corporation

- 6.3.13 Novartis AG

- 6.3.14 Organon LLC

- 6.3.15 Orion Corporation

- 6.3.16 Pharmaxis Ltd.

- 6.3.17 Sandoz

- 6.3.18 Teva Pharmaceutical Industries Ltd.

- 6.3.19 United Therapeutics Corporation

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment