|

시장보고서

상품코드

2063495

의료기기 라벨링 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Device Labeling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

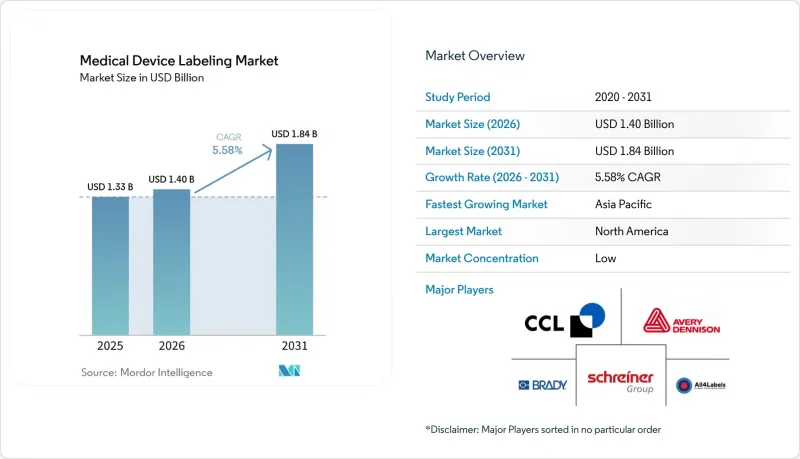

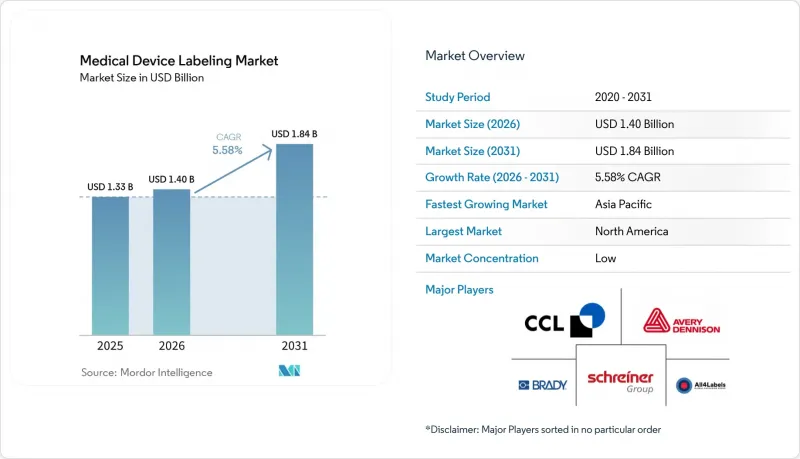

Mordor Intelligence에 의하면, 의료기기 라벨링 시장 규모는 2025년에 13억 3,000만 달러로 평가되었습니다. 2026년 14억 달러에서 2031년까지 18억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.58%를 나타낼 전망입니다.

본 보고서는 라벨 유형(감압 접착제/자가 접착식, 접착제 도포/습식 접착, 수축 슬리브, 인몰드), 용도(일회용 소모품, 모니터링·진단 기기, 치료·외과용 기구), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료기기 라벨링 시장 동향 및 인사이트

전 세계적인 UDI 의무화 및 데이터베이스 등록에 따라 라벨 데이터 및 듀얼 포맷 바코드에 대한 요건이 확대됨

미국 FDA는 2025년에 GUDID 시행을 강화하여 바코드 내용과 데이터베이스 필드 간에 불일치가 있을 경우 경고장을 발부했기 때문에 변환기 제조업체들은 현재 10mm×15mm 크기의 라벨에 이르기까지 2차원 기호를 검증하고 있습니다. 중국은 2024년에 UDI의 단계적 도입을 완료하고, 1등급 의료기기에 기계 판독 가능 식별자(UDI) 표기를 의무화했습니다. 이로 인해 수출업체들은 이중 언어 텍스트와 GS1 또는 HIBC 기호 체계를 반영하도록 라벨을 재설계할 수밖에 없게 되었습니다. 일본, 싱가포르, 말레이시아, 브라질도 동일한 체계를 채택하고 있어, 하나의 의료기기 모델에 대해 5유형 이상의 지역별 라벨 변형이 출하될 가능성이 있습니다. 이러한 규제로 인해 의료기기 제조업체들은 아트웍의 버전 관리 및 규제 변경 사항 추적을 자동화하는 클라우드 기반 라벨 관리 시스템으로의 전환을 서둘러야 하는 상황에 놓여 있습니다.

MDR/IVDR의 다국어 및 번역 규정에 따라 라벨의 SKU 수와 컨텐츠 양이 증가

2025년 7월에 발효된 EU 규정 2025/1234에 따르면, 의료용 기기의 경우 종이 사용 설명서를 eIFU로 대체할 수 있지만, 각 언어별로 라벨에 고유한 QR 링크를 기재해야 하기 때문에 SKU 수가 두 배로 늘어납니다. 단일 주입 펌프라 할지라도 EU 역내 판매를 위해 24가지 유형의 라벨 디자인이 필요한 경우가 있으며, 독일어로 인쇄된 재고는 법적으로 스페인으로 출하할 수 없기 때문에 재고 리스크가 높아집니다. 번역 업체에 따르면, 2024년 이후 의료기기 라벨링 프로젝트가 30% 급증했으며, 사내에서 언어 검증 서비스를 제공하는 컨버터는 인증 기간을 단축함으로써 계약을 수주하고 있습니다.

규정 준수 부담과 잦은 규제 변경으로 인해 라벨 제조업체의 비용과 시장 출시까지 걸리는 시간이 증가

EU는 2021년부터 2025년 사이에 89건의 지침 문서를 발간했으며, 이들 모두 라벨의 내용을 변경할 가능성이 있습니다. 한편, 인증 기관의 처리 지연은 12개월에 달하며, 수정할 때마다 5,000-1만 5,000달러의 비용이 드는 아트워크 수정을 어쩔 수 없이 해야 하는 상황입니다. 중국은 2024년에 14건의 UDI 공고를 발표했으나, 각 성별 시행 상황에 일관성이 없어 수출업체들의 불확실성이 커지고 있습니다. 중소 제조업체들은 매출의 상당 부분을 규제 대응에 할애하고 있는 반면, 다국적 기업의 경우 그 비율은 2%에 그치고 있어, 이로 인해 업계 재편이 가속화되고 있습니다.

부문별 분석

2025년 기준, 의료기기 라벨링 시장에서 압력 감지 라벨의 점유율은 57.37%를 차지했습니다. 이는 분당 300-600장의 라벨을 부착하는 라인과의 호환성, 그리고 감마선, 에틸렌옥사이드, 증기 멸균에 대한 내성이 주요 요인으로 작용하고 있습니다. 아크릴계 또는 고무계 접착제는 50 kGy의 방사선 조사를 받아도 황변하지 않고 접착 강도를 유지합니다. 접착제 도포형 또는 습식 접착 라벨 시장은 2031년까지 연평균 5.89%의 성장률을 나타낼 것으로 예상되며, 이는 가장 높은 성장률입니다. 이는 제약 회사가 액체 주사제를 유리 바이알에 충전할 때, 떼어내고 다시 밀봉할 수 있는 편의성보다 영구적인 접착력이 우선시되기 때문입니다. 습식 접착 시스템은 기판에 침투하여 기계적 결합을 형성함으로써 콜드체인에서 결로 발생 시 발생하는 박리를 방지하지만, 10-15초의 유지 시간이 필요하기 때문에 라인 속도는 분당 150-250개 단위로 떨어집니다.

2025년에는 수축 슬리브가 판매량에서 상당한 점유율을 차지했으며, 안전 바늘이 일체형으로 장착된 프리필드 주사기 등의 복합 제품에서 선호되고 있습니다. 이러한 제품의 경우 360도 그래픽 표시가 가능하기 때문에 30-40%의 가격 프리미엄이 정당화됩니다. 인몰드 라벨은 여전히 틈새 시장 제품이지만, 검체 컵의 블로우 성형이나 사출 성형 과정에서 부착되므로 성형 후 공정을 생략할 수 있습니다. 2024년에 발효될 EU 일회용 플라스틱 지침은 의료기기를 적용 대상에서 제외하고 있지만, 용기의 수지와 호환되는 재활용 가능한 표면재에 대한 평가를 장려하고 있습니다. UPM Raflatac은 2025년에 라이너리스 구조를 출시하여, 자재 폐기물을 15% 줄이고 운송 비용을 절감함으로써 지속가능성을 중시하는 제조업체들의 관심을 끌고 있습니다.

지역별 분석

2025년, 북미는 의료기기 라벨링 시장의 45.85%를 차지했으며, 그 배경에는 FDA의 UDI 시행 및 GUDID의 동기화 요건이 있습니다. 해당 청은 2024년에 국내 및 해외 제조업체를 대상으로 규격 미준수 사항에 대해 14건의 경고장을 발부했습니다. 캐나다는 2024년에 의료기기 규제를 FDA 기준에 부합하도록 조정하고, 라벨과 관련된 이상반응 보고를 의무화하는 한편, 퀘벡주에서는 프랑스어와 영어의 이중 언어 표기를 의무화했습니다. 멕시코의 COFEPRIS는 2025년에 UDI를 도입하여 설계를 간소화하는 한편, USMCA(미국·멕시코·캐나다 협정)에 따른 유통 과정에서 영어·프랑스어·스페인어 3개 언어 표기를 의무화함으로써 북미 규제 블록을 형성했습니다.

유럽에서는 MDR 및 IVDR로의 전환이 진행되고 있으며, 독일, 프랑스, 이탈리아, 스페인, 폴란드에서는 현지 언어로 작성된 사용 설명서의 제공이 의무화되었고, 라벨의 SKU가 세분화되고 있습니다. 영국의 UKCA 마크는 2024년부터 의무화되며, EU의 MDR을 준수하는 북아일랜드와는 별도로, 그레이트브리튼을 위한 라벨을 따로 준비해야 하므로 병행 재고 관리를 할 수밖에 없는 상황입니다. 2025년 7월에 발효되는 규정 2025/1234는 의료 종사자용 기기에 대해 eIFU를 허용하고 있지만, 각 언어별 QR 코드 및 URL에 대한 요건은 유지되고 있어 인쇄 비용을 절감하지 못한 채 디자인이 복잡해지고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.08%를 나타낼 것으로 예측되며, 이는 지역별로는 가장 높은 수치입니다. 중국은 2024년에 UDI 도입을 완료하고, NMPA 데이터베이스에 1등급 의료기기 식별자를 등록하도록 의무화하며, 듀얼 포맷 바코드 채택을 촉진하고 있습니다. 인도의 생산 연계형 인센티브 제도는 14억 달러를 국내 제조업에 투입하고 있으며, 현지에서 원자재를 조달하도록 장려하는 동시에 푸네, 아메다바드, 첸나이에 다국적 컨버터 기업의 투자를 유치하고 있습니다. 일본의 PMDA는 2024년에 eIFU를 승인하며 FDA 및 EU의 선례에 따랐으나, 라벨상의 일본어 표기 및 한자의 가독성에 관한 엄격한 기준은 유지했습니다. 중동 및 아프리카, 남미 및 아시아·태평양 지역의 소규모 시장은 2025년에 전반적으로 매출에서 상당한 비중을 차지했습니다. 브라질의 ANVISA는 2024년에 UDI 지침을 발표하고, 2026년까지 클래스 III 및 IV 의료기기에 대해 GS1 또는 HIBC에 따른 코딩을 의무화했습니다. 호주의 TGA는 2024년에 UDI 요건을 FDA 및 EU의 체계와 일치시킴으로써 태평양 지역의 설계 절차를 간소화했습니다. 한편, 한국의 식품의약품안전처(MFDS)는 수입품에 대해 한국어로 표시할 것을 의무화했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the medical device labeling market size was valued at USD 1.33 billion in 2025 and is estimated to grow from USD 1.40 billion in 2026 to reach USD 1.84 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

This report is Segmented by Label Type (Pressure-sensitive/Self-adhesive, Glue-applied/Wet-glue, Shrink Sleeves, In-Mold), Application (Disposable Consumables, Monitoring & Diagnostic Equipment, Therapeutic & Surgical Instruments), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Device Labeling Market Trends and Insights

Global UDI Mandates and Database Submissions Expand Label Data and Dual-Format Barcode Requirements

The U.S. FDA intensified GUDID enforcement in 2025, issuing warning letters when barcode content and database fields diverged, so converters now validate 2D symbols down to 10 mm X 15 mm labels. China finished its phased UDI rollout in 2024, requiring Class I devices to carry machine-readable identifiers, driving exporters to redesign labels for bilingual text and GS1 or HIBC symbologies . Japan, Singapore, Malaysia, and Brazil adopted similar frameworks, meaning one device model may ship with five or more regional label variants. These mandates push device firms toward cloud label-management systems that automate artwork versioning and regulatory change tracking.

MDR/IVDR Multi-Language and Translation Rules Increase Label SKUs and Content Volume

Under EU Regulation 2025/1234, effective July 2025, professional-use devices may replace paper booklets with eIFU, but each language still needs a unique QR link on the label, multiplying SKUs . A single infusion pump can require 24 label designs for the bloc, inflating inventory risk because German-printed stock cannot legally ship to Spain. Translation suppliers report a 30% surge in device-label projects since 2024, and converters that offer in-house language validation win contracts by shortening certification timelines.

Compliance Burden and Frequent Regulatory Updates Raise Cost/Time-to-Market for Labelers

The EU issued 89 guidance documents between 2021 and 2025, each potentially altering label content, while notified-body backlogs stretch to 12 months, forcing multiple artwork revisions that cost USD 5,000-15,000 per iteration. China published 14 UDI circulars in 2024, and inconsistent provincial enforcement adds uncertainty for exporters. Small manufacturers spend up to a notable share of sales on regulatory affairs versus 2% for multinationals, accelerating industry consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Rising Home-Use, Wearable, and POCT Devices Elevate Demand for Durable, Patient-Friendly Labels

- Increased Recall and Track-and-Trace Needs Accelerate 2D-Barcode-Rich UDI Labeling

- Fragmented Label-Converting Landscape Intensifies Pricing Pressure and Margin Squeeze

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure-sensitive labels held 57.37% of the medical device labeling market in 2025, driven by compatibility with 300-600 labels-per-minute application lines and gamma, ethylene-oxide, and steam sterilization. Acrylic or rubber adhesives maintain bond strength through 50 kGy irradiation without yellowing. Glue-applied or wet-glue labels are forecast to grow at 5.89% through 2031, the fastest rate, as pharmaceutical firms package liquid injectables in glass vials where permanent adhesion outweighs peel-and-reseal convenience. Wet-glue systems create mechanical bonds by penetrating substrates, preventing lift during cold-chain condensation, yet they require 10-15 second dwell times that slow lines to 150-250 units per minute.

Shrink sleeves represented a notable share of volume in 2025, favored for combination products such as pre-filled syringes with integrated safety needles, where 360-degree graphics justify a 30-40% premium. In-mold labels remain niche, applied during blow or injection molding of specimen cups, eliminating post-molding steps. The EU Single-Use Plastics Directive, effective in 2024, exempts medical devices but has prompted evaluation of recyclable face stocks that match container resin. UPM Raflatac launched a linerless construction in 2025 that cuts material waste by 15% and lowers freight costs, appealing to sustainability-focused manufacturers.

Geography Analysis

North America held 45.85% of the medical device labeling market share in 2025, anchored by FDA UDI enforcement and GUDID synchronization requirements. The agency issued 14 warning letters in 2024 for non-compliance, targeting domestic and foreign manufacturers. Canada aligned its Medical Devices Regulations with FDA standards in 2024 and introduced mandatory label-related adverse-event reporting, compelling bilingual French-English labeling for Quebec. Mexico's COFEPRIS adopted UDI in 2025, creating a North American regulatory bloc that simplifies design yet imposes trilingual English-French-Spanish obligations for USMCA distribution.

Europe navigates MDR and IVDR transitions that mandate local-language instructions in Germany, France, Italy, Spain, and Poland, fragmenting label SKUs. The UK's UKCA marking, mandatory in 2024, requires separate labels for Great Britain versus Northern Ireland, which follows EU MDR, forcing parallel inventories. Regulation 2025/1234, effective July 2025, permits eIFU for professional devices but retains QR-code and URL requirements for each language, multiplying designs without reducing print costs.

Asia-Pacific is forecast to grow at 6.08% through 2031, the fastest regional CAGR. China completed UDI rollout in 2024, mandating Class I device identifiers in the NMPA database and driving dual-format barcode adoption. India's Production Linked Incentive scheme channels USD 1.4 billion into domestic manufacturing, favoring local label procurement and attracting multinational converter investment in Pune, Ahmedabad, and Chennai. Japan's PMDA accepted eIFU in 2024, aligning with FDA and EU precedents, yet retained strict on-label Japanese-language and kanji legibility standards. Middle East and Africa, South America, and smaller Asia-Pacific markets collectively represented notable share of revenue in 2025. Brazil's ANVISA published UDI guidelines in 2024, requiring GS1 or HIBC coding for Class III and IV devices by 2026. Australia's TGA harmonized UDI requirements with FDA and EU frameworks in 2024, simplifying Pacific-region design, while South Korea's MFDS mandated Korean-language labeling for imports.

- All4Labels Group

- Avery Dennison

- Beontag

- Brady Corporation

- Brook & Whittle

- CCL Industries

- Cisper Electronics

- CleanMark Labels

- Domino Printing Sciences

- Fortis Solutions Group

- HERMA GmbH

- Inovar Packaging Group

- LINTEC Corporation

- Loftware

- Propper Manufacturing

- Resource Label Group

- RFiD Discovery

- SATO Holdings

- Schreiner Group

- Taylor Corporation

- UPM Raflatac

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global UDI Mandates and Database Submissions Expand Label Data and Dual-Format Barcode Requirements

- 4.2.2 MDR/IVDR Multi-Language and Translation Rules Increase Label SKUs And Content Volume

- 4.2.3 Rising Home-Use/Wearable and POCT Devices Elevate Demand for Durable, Patient-Friendly Labels

- 4.2.4 Increased Recall and Track-And-Trace Needs Accelerate 2D Barcode-Rich UDI Labeling

- 4.2.5 Adoption Of RFID/NFC Smart Labels for Item-Level Traceability in Surgical Kits and Implants

- 4.2.6 Sterile Processing Workflows Boost Usage of Indicator Labels and Documentation (SPD/CSSD)

- 4.3 Market Restraints

- 4.3.1 Compliance Burden and Frequent Regulatory Updates Raise Cost/Time-To-Market for Labelers

- 4.3.2 Fragmented Label Converting Landscape Intensifies Pricing Pressure and Margin Squeeze

- 4.3.3 Direct Part Marking (Permanent UDI) Displaces Some External Labels for Reusable Instruments

- 4.3.4 eIFU Adoption Reduces Paper Booklet/Leaflet Labeling for Professional-Use Devices

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD)

- 5.1 By Label Type

- 5.1.1 Pressure-sensitive

- 5.1.2 Glue-applied

- 5.1.3 Shrink sleeves

- 5.1.4 In-mold labels

- 5.2 By Application

- 5.2.1 Disposable consumables

- 5.2.2 Monitoring & diagnostic equipment

- 5.2.3 Therapeutic & surgical instruments

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 All4Labels Group

- 6.3.2 Avery Dennison

- 6.3.3 Beontag

- 6.3.4 Brady Corporation

- 6.3.5 Brook & Whittle

- 6.3.6 CCL Industries

- 6.3.7 Cisper Electronics

- 6.3.8 CleanMark Labels

- 6.3.9 Domino Printing Sciences

- 6.3.10 Fortis Solutions Group

- 6.3.11 HERMA GmbH

- 6.3.12 Inovar Packaging Group

- 6.3.13 LINTEC Corporation

- 6.3.14 Loftware

- 6.3.15 Propper Manufacturing

- 6.3.16 Resource Label Group

- 6.3.17 RFiD Discovery

- 6.3.18 SATO Holdings

- 6.3.19 Schreiner Group

- 6.3.20 Taylor Corporation

- 6.3.21 UPM Raflatac

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment