|

시장보고서

상품코드

2063498

생물학적 샘플 채취 키트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Biological Sample Collection Kits - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

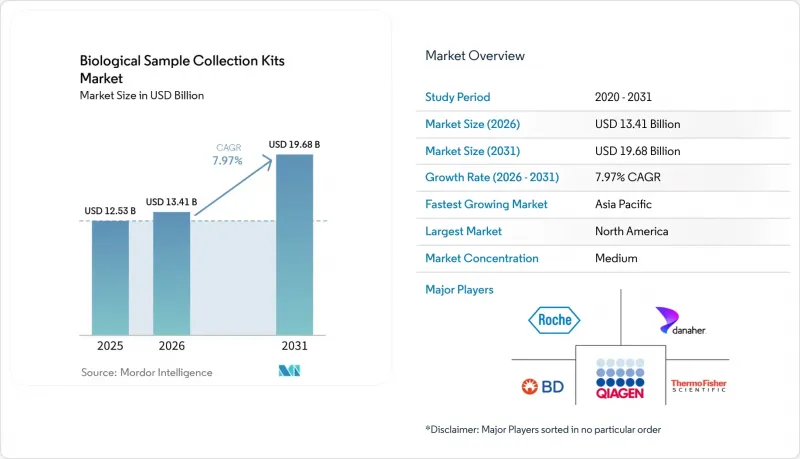

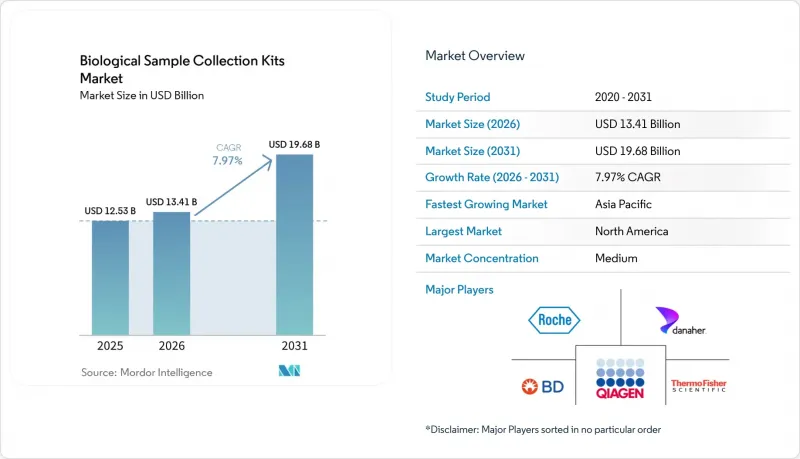

Mordor Intelligence에 의하면, 생물학적 샘플 채취 키트 시장 규모는 2025년 125억 3,000만 달러로 평가되었습니다. 2026년 134억 1,000만 달러에서 2031년까지 196억 8,000만 달러로 확대되어 2026-2031년 CAGR은 7.97%를 나타낼 것으로 예측됩니다.

본 보고서는 제품별(혈액, 면봉/바이러스 운반용, 타액, DBS, 구강 점막 면봉 DNA 등), 용도(진단, 조사, 바이오뱅크 등), 최종 사용자(병원, 진단실험실, 연구 기관, 바이오뱅크, 제약·바이오기술 기업, 원격의료 사업자), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 생물학적 샘플 채취 키트 시장 동향 및 인사이트

감염병 검사 수요가 지속되면서 기초적인 수요를 뒷받침하고 있습니다.

코로나19 사태가 진정된 후에도 호흡기 질환 및 성병 검사 프로그램이 여전히 검사 키트 발주의 주된 기반을 이루고 있습니다. CDC 기록에 따르면, 2024년 클라미디아, 임질, 매독의 총 환자 수는 220만 건에 달하고, 전년 대비 9% 감소했으나, 팬데믹 이전 수준을 상회하고 있습니다. 2025년 초, 인플루엔자 H3N2 서브클레이드 K 및 SARS-CoV-2 BA.3.2 계통의 유행으로 인해 지역별 검사 수요가 급증하면서, 면봉 및 바이러스 운반 키트에 대한 수요가 증가했습니다. WHO의 인플루엔자 네트워크는 표준화된 면봉 채취 프로토콜에 의존하고 있으며, 인플루엔자 A/B, RSV, SARS-CoV-2를 검출하는 다중 호흡기 패널에는 여러 표적에 걸쳐 핵산을 보호하는 검증된 키트가 필요합니다. 따라서 국가 데이터베이스에 정보를 제공하는 센티넬 연구소에서는 2028년까지 면봉 키트의 판매량이 연평균 5% 전후의 성장세를 유지할 것으로 예측됩니다. 각 제조업체들은 2021년부터 2022년에 나타났던 과잉 재고 사이클을 피하기 위해, 이러한 안정적인 수요와 재고 최적화 간의 균형을 맞추고 있습니다.

재택 및 원격 검체 채취로의 급속한 전환

자가 채취 기기는 진단 워크플로우를 혁신하고 있습니다. FDA는 2025년 5월, Teal Health사의 ‘Wand’를 가정용 HPV 선별 검사용으로 승인했습니다. 이 제품의 임상 의사들에 의한 검체 일치율은 96%이며, 대다수의 사용자는 자가 검사를 통해 선별 검사를 계속할 수 있다고 응답했습니다. 해당 기관이 2024년 9월에 발표한 지침에 따르면, 특정 제품에 대해 완전히 분산된 임상시험이 공식적으로 허용되어, 이를 통해 환자의 이동 부담이 줄어들고 피험자 등록 기간이 단축될 것입니다. 유럽 규제 당국은 시설 방문과 원격 검체 채취를 결합한 하이브리드형 설계를 권장하고 있습니다. 검체의 품질을 보장하기 위해 후원사는 여전히 참가자들에게 교육을 실시해야 하지만, 시설 운영 비용 절감을 통한 비용 절감 효과와 지리적으로 분산된 환자에 대한 접근성은 복잡성 증가를 상쇄하고도 남는 이점으로 작용하고 있습니다. 현재 텔레헬스 플랫폼에서는 검체 채취 키트에 동영상 안내와 반송용 선불 택배를 함께 제공하며, 분석을 위해 CLIA 인증 검사실과 직접 연계하는 서비스가 제공되고 있습니다.

IVDR 및 FDA 규정 준수 비용이 업계 재편의 압박 요인으로 작용

유럽의 체외진단용 의료기기 규정(IVDR)에 따라, 인증 기관의 감시 대상이 검사의 약 10%에서 80%-90%로 확대되어 인증에는 현재 13-18개월이 소요되고, 총 비용은 종종 5만 유로(5만 8,800달러)를 초과합니다. EUDAMED 데이터베이스는 2026년 5월 28일부터 의무화되며, 기업들은 라벨 정보와 모니터링 데이터를 업로드해야 합니다. 많은 제조업체들이 비용을 고려한 결과, 이미 일부 제품 라인을 단종함에 따라 기존 검사 키트의 일시적인 품귀 현상이 발생하고 있습니다.

미국에서도 유사한 압력이 가해지고 있으며, 자가 채취용 의료기기의 510(k) 신청 시 인체공학 데이터와 시판 후 관리 계획의 제출이 요구되고 있습니다. 그 때문에 전담 규제 대응 팀을 갖추지 못한 중소 벤더들은 합병을 추진하거나 사업에서 철수하고 있어, 업계의 집중화가 진행되고 있습니다.

부문별 분석

채혈 키트는 2025년 매출의 33.48%를 차지했으며, 이 생물학적 샘플 채취 시장 부문은 2031년까지 연평균 성장률(CAGR) 8.34%로 성장하고 있습니다. 병원들이 기존 설계에 비해 부상 위험을 71% 줄여주는 안전 바늘의 사용을 의무화하고 있어, 채혈 기기용 생물학적 샘플 채취 키트 시장이 확대되고 있습니다. 면봉과 바이러스 수송 키트는 호흡기 질환 및 성매개감염(STI) 감시에서 여전히 핵심적인 역할을 하고 있지만, 입찰에 따른 가격 압박에 직면해 있습니다. 타액 검사 키트의 경우, 소비자 직접 유전자 검사(DTC) 및 호르몬 검사에 대한 수요를 반영하여, 23andMe사는 FDA 승인을 받은 약물유전학 패널에 독자적인 튜브를 채택하고 있습니다.

특수한 형식은 밸류체인의 업스트림로 이동하고 있습니다. 한때 신생아 선별 검사에만 사용되던 건조 혈액 스팟 카드는 FDA의 2024년 생물분석 지침에 따라 현재는 분산형 약동학 연구를 지원하고 있습니다. 뺨 점막 면봉 DNA 키트는 여전히 법의학 및 친자 확인의 기반이 되고 있으며, 소변 채취 키트는 약물 검사를 뒷받침하고 있습니다. 대변 및 분변 미생물군집 검사 키트는 대장암 검진이나 염증성 장질환 모니터링 용도로 등장하고 있지만, 여전히 대부분의 제품은 연구 용도로 사용되고 있습니다. 이러한 키트에 대해 CLIA 인증을 취득할 수 있는 공급업체에게는 거대한 미개척 시장의 가능성이 열려 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 44.25%를 차지했으며, 이는 잘 구축된 진단 인프라와 높은 1인당 의료비를 반영한 것입니다. 미국 보건사회복지부는 2025년 H5N1 대책에 3억 600만 달러를 편성했으며, 그중 800만 달러를 키트 제조에 할당했습니다. CDC(미국 질병통제예방센터)의 역학·검사 역량 프로그램은 2024년에 주립 검사실 전체의 검체 물류 체계를 강화하기 위해 3억 6,400만 달러를 지원했습니다. 가정용 HPV 선별 검사 및 약리유전체학 검사에 대한 규제 당국의 승인으로 자가 채취가 점점 더 보편화되고 있는 반면, 분산형 임상시험의 후원사들은 냉동 운송을 피하기 위해 상온 보관이 가능한 튜브에 크게 의존하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 8.48%로 가장 빠르게 성장하고 있으며, 2025년 생물학적 샘플 채취 키트 시장에서 큰 점유율을 차지하고 있습니다. 인도의 PM-ABHIM은 2025 회계연도에 지역 연구소 건설을 위해 4,770 카롤 루피(5억 7,000만 달러)를 배정하여, 전년 대비 대폭 증가했습니다. 2026년도 연방 예산에서는 ‘Bio SHAKTI’를 위해 1,000곳의 시험 사이트 설립에 10,000 카롤 루피를 지원하기로 약속한 반면, ‘생산 연계형 인센티브(PLI)’ 제도에서는 체외진단용 의료기기를 위해 342억 루피가 투입되고 있습니다. 중국은 지역 유전체 센터를 확대하고 있으며, 2023년 말 일본에서 출시된 다항목 유전자 현장 진단 기기는 종양학 및 산전 검사 분야에서 타액·혈액 검사 키트에 대한 수요를 촉진하고 있습니다.

유럽 시장은 여전히 규모가 크지만, IVDR(체외진단 의료기기 규정)과 관련된 비용 증가로 인해 성장이 둔화되고 있으며, 많은 기업이 일부 제품의 판매를 중단하는 상황에 이르렀습니다. 인증 대기 줄과 인증 기관의 처리 능력 한계로 인해 시장 진입이 지연되고 있으며, 그 결과 시장 점유율은 기존 대기업에 쏠려 있습니다. 중동 및 아프리카 및 남미는 도입 초기 단계에 있습니다. 감시 활동 및 기부금을 통한 질병 대책 프로그램을 위한 정부 조달로 인해 기본 수요량은 안정적이며, 민간 진단 업계에서는 더 높은 품질의 검체 채취 키트가 필요한 분자 패널을 점차 도입하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the biological sample collection kits market size is projected to expand from USD 12.53 billion in 2025 and USD 13.41 billion in 2026 to USD 19.68 billion by 2031, registering a CAGR of 7.97% between 2026 to 2031.

This report is Segmented by Product (Blood, Swab/Viral Transport, Saliva, DBS, Buccal Swab DNA, and More), Application (Diagnostics, Research, Biobanking, and More), End User (Hospitals, Diagnostic Labs, Research Institutes, Biobanks, Pharma/Biotech, Telehealth Operators), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global Biological Sample Collection Kits Market Trends and Insights

Persistent Infectious-Disease Testing Volumes Sustaining Baseline Demand

Respiratory and sexually transmitted infection programs are still anchoring kit orders even after COVID-19 normalization. The CDC logged 2.2 million combined chlamydia, gonorrhea, and syphilis cases in 2024, a number higher than pre-pandemic levels despite a 9% yearly drop . Influenza H3N2 subclade K and the SARS-CoV-2 BA.3.2 lineage triggered regional testing surges in early 2025, boosting demand for swabs and viral-transport kits. WHO influenza networks rely on standardized swab protocols, and multiplex respiratory panels detecting influenza A/B, RSV, and SARS-CoV-2 require validated kits that protect nucleic acids across multiple targets. Sentinel laboratories feeding national databases are therefore expected to maintain mid-single-digit growth in swab kit volume through 2028. Manufacturers are balancing this steady demand with lean inventory practices to avoid the overstock cycles seen in 2021-2022.

Rapid Shift to At-Home and Remote Collection

Self-collection devices are reshaping diagnostic workflows. The FDA approved Teal Health's Wand for at-home HPV screening in May 2025, with 96% concordance with clinician samples, and the majority of users said home testing would keep them up to date with screening . The agency's September 2024 guidance formally permits fully decentralized trials for selected products, thereby reducing patient travel burdens and shortening enrollment timelines. European regulators endorse hybrid designs that mix site visits with remote sampling. Sponsors must still train participants to ensure specimen quality, yet cost savings from reduced site overhead and the ability to reach geographically dispersed patients outweigh the added complexity. Telehealth platforms now bundle collection kits with video guidance and prepaid returns, linking directly to CLIA laboratories for analysis.

IVDR and FDA Compliance Costs Creating Consolidation Pressure

Europe's In Vitro Diagnostic Regulation expanded notified-body oversight from roughly 10% of assays to 80%-90%, and certification now takes 13-18 months, with total fees often exceeding EUR 50, 000 (USD 58,800). The EUDAMED database becomes mandatory on 28 May 2026, compelling firms to upload labeling and surveillance data. A high number of manufacturers have already dropped some product lines after weighing the costs, leading to spot shortages of legacy kits.

Similar pressure exists in the United States, where 510(k) submissions for self-collection devices require human-factors data and post-market plans. Smaller vendors without dedicated regulatory teams are therefore pursuing mergers or exiting altogether, nudging industry concentration higher.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Genetic Testing

- Ambient-Stable Nucleic-Acid Chemistries Reducing Cold-Chain Dependence

- Raw-Material Volatility Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blood-collection kits accounted for 33.48% of 2025 revenue, and this segment of the biological sample collection market is growing at an 8.34% CAGR through 2031. The biological sample collection kits market for blood-collection devices is expanding as hospitals mandate safety needles that reduce injuries by 71% compared with legacy designs. Swab and viral-transport kits remain core to respiratory and STI surveillance, yet face tender-driven price compression. Saliva kits are capitalizing on direct-to-consumer genomics and hormone assays; 23andMe relies on proprietary tubes for its FDA-cleared pharmacogenetics panel.

Specialty formats are moving up the value chain. Dried blood-spot cards, once confined to newborn screening, now support decentralized pharmacokinetic studies following the FDA's 2024 bioanalytical guidance. Buccal swab DNA kits continue to underpin forensics and paternity testing, while urine collectors support drug screening. Stool and fecal microbiome kits are emerging for colorectal cancer screening and inflammatory bowel disease monitoring, yet most offerings still target research use. Vendors that can obtain CLIA validation for these kits hold significant white-space potential.

Geography Analysis

North America accounted for 44.25% of global revenue in 2025, reflecting entrenched diagnostic infrastructure and high per capita healthcare spending. The U.S. Department of Health and Human Services earmarked USD 306 million for H5N1 preparedness in 2025, including USD 8 million for kit manufacturing. The CDC's Epidemiology and Laboratory Capacity program supplied USD 364 million in 2024 to upgrade specimen logistics across state labs. Regulatory approvals for at-home HPV screening and pharmacogenomics tests are further normalizing self-collection, while decentralized-trial sponsors lean heavily on ambient-stable tubes to sidestep frozen shipping.

Asia-Pacific is the fastest-growing region, with a 8.48% CAGR, accounting for a significant share of the biological sample collection kits market in 2025. India's PM-ABHIM allocated INR 4,770 crore (USD 570 million) in FY 2025 to build district laboratories, a major year-on-year rise. The Union Budget 2026 pledged INR 10,000 crore for Bio SHAKTI to seed 1,000 trial sites, while the Production Linked Incentive scheme steers INR 34.2 billion toward in-vitro diagnostic devices. China is rolling out regional genomics centers, and Japan's multiplex genetic point-of-care devices, launched in late 2023, are stimulating demand for saliva and blood kits across oncology and prenatal testing.

Europe remains sizable, but growth is tempered by IVDR-related overheads, which have driven significant number of firms to discontinue some products. Certification queues and limited notified-body capacity prolong market entry, tilting the share toward large incumbents. The Middle East and Africa, plus South America, are early in the adoption curve; government procurements for surveillance and donor-funded disease programs keep baseline volumes stable, with private diagnostic chains gradually adding molecular panels that require higher-grade collection kits.

- Beckton Dickinson

- Cardinal Health

- COPAN Diagnostics

- Cytiva

- Exact Sciences

- Roche

- Greiner Bio-One

- Hardy Diagnostics

- HiMedia Laboratories

- Hologic

- Longhorn Vaccines & Diagnostics

- Medical Wire & Equipment

- Medline Industries

- Norgen Biotek

- OraSure Technologies / DNA Genotek

- Puritan Medical Products

- QIAGEN

- Revvity

- Sarstedt

- Spectrum Solutions

- Thermo Fisher Scientific

- Zymo Research

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Shift to At-Home/Remote Collection for Diagnostics and Decentralized Trials

- 4.2.2 Expansion Of Genetic Testing (NIPT, Pgx, Oncology) Requiring Validated Collection Kits

- 4.2.3 Ambient-Stable Nucleic-Acid Chemistries Reducing Cold-Chain Dependence

- 4.2.4 Persistent Infectious-Disease Testing Volumes (Respiratory, STI) Sustaining Kit Demand

- 4.2.5 Biobanking and Precision-Medicine Programs Standardizing Preanalytics

- 4.3 Market Restraints

- 4.3.1 IVDR/FDA Compliance Costs and Documentation Complexity for Self-Collection Devices

- 4.3.2 Post-Pandemic Inventory Normalization and Destocking Cycles

- 4.3.3 Price Pressure and Tender-Driven Commoditization In Swabs/VTM

- 4.3.4 Raw-Material Volatility (Medical-Grade Polymers, Flocking Fibers) Impacting Margins

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Blood Collection Kits

- 5.1.2 Swab And Viral Transport Kits

- 5.1.3 Saliva Collection Kits

- 5.1.4 Dried Blood Spot (DBS) Collection Cards/Kits

- 5.1.5 Buccal Swab DNA Collection Kits

- 5.1.6 Urine Collection Kits

- 5.1.7 Stool/Fecal Microbiome Collection Kits

- 5.2 By Application

- 5.2.1 Diagnostics

- 5.2.2 Research & Academia

- 5.2.3 Biobanking & Biorepositories

- 5.2.4 Clinical Trials & Decentralized Trials

- 5.2.5 Forensics & Law Enforcement

- 5.2.6 Direct-To-Consumer Genomics & Wellness Testing

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Academic & Research Institutes

- 5.3.4 Biobanks & Biorepositories

- 5.3.5 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of APAC

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of MEA

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Becton, Dickinson and Company (BD)

- 6.3.2 Cardinal Health

- 6.3.3 COPAN Diagnostics

- 6.3.4 Cytiva

- 6.3.5 Exact Sciences

- 6.3.6 F. Hoffmann-La Roche

- 6.3.7 Greiner Bio-One

- 6.3.8 Hardy Diagnostics

- 6.3.9 HiMedia Laboratories

- 6.3.10 Hologic

- 6.3.11 Longhorn Vaccines & Diagnostics

- 6.3.12 Medical Wire & Equipment

- 6.3.13 Medline Industries

- 6.3.14 Norgen Biotek

- 6.3.15 OraSure Technologies / DNA Genotek

- 6.3.16 Puritan Medical Products

- 6.3.17 QIAGEN

- 6.3.18 Revvity

- 6.3.19 Sarstedt

- 6.3.20 Spectrum Solutions

- 6.3.21 Thermo Fisher Scientific

- 6.3.22 Zymo Research

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment