|

시장보고서

상품코드

2063501

중환자실(ICU) 인공호흡기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Intensive Care Unit (ICU) Ventilators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

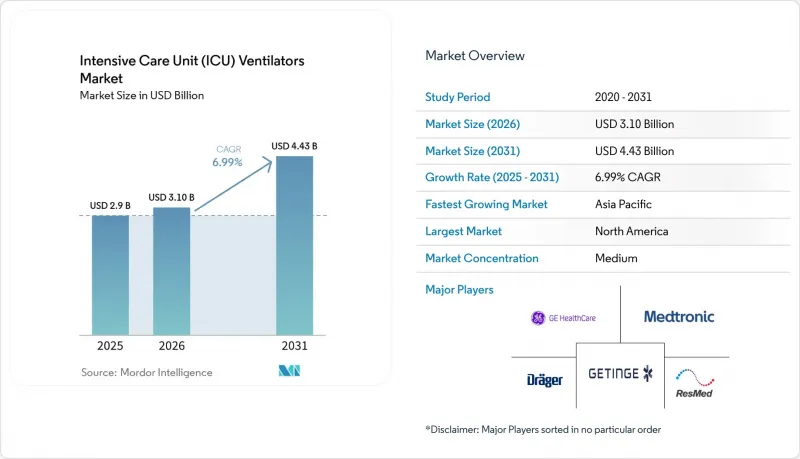

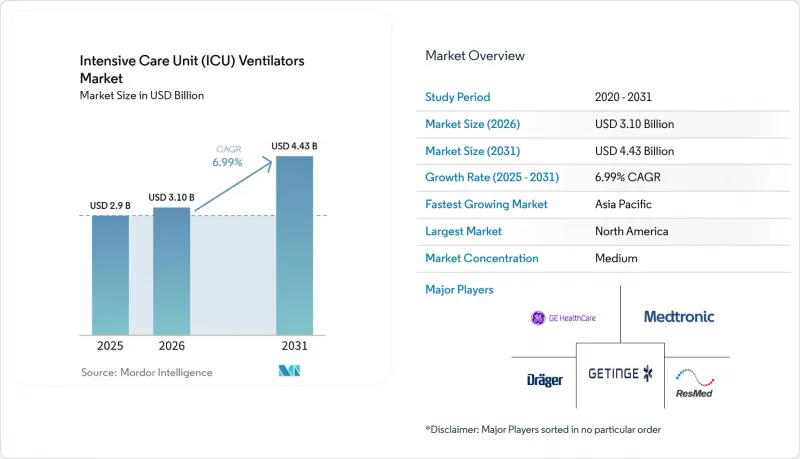

Mordor Intelligence에 의하면, 중환자실(ICU) 인공호흡기 시장 규모는 2025년 29억 달러로 평가되었습니다. 2026년에는 31억 달러로 확대되어 2031년까지 44억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.99%를 나타낼 전망입니다.

본 보고서는 모빌리티 유형(고정형, 휴대형), 제품 유형(하이엔드, 미드엔드, 로우엔드), 모드(용량 제어형 등), 환자 연령대(성인, 소아, 신생아), 인터페이스(침습적, 비침습적), 최종 사용자(병원 등), 기술(기계식 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 중환자실(ICU) 인공호흡기 시장 동향 및 인사이트

급성 호흡곤란 증후군(ARDS) 발생률의 급증

ARDS는 중환자실(ICU) 인공호흡기 시장의 주요 수요 요인으로 자리 잡고 있습니다. 미국의 발생률은 인구 10만 명당 64건이며, 이 질환은 전 세계 중환자실 입원 환자의 10%-15%를 차지하고 있습니다. 30%-50%에 달하는 높은 사망률로 인해, 폐 손상을 최소화하는 정밀한 인공호흡 관리가 임상 현장에서 중요하게 여겨지고 있습니다. 북미의 계절적 산불 연기와 남아시아의 지속적인 대기질 문제로 인해 ARDS 환자 수가 정점에 달하고 있습니다. OECD 국가들에서는 인구 고령화가 진행되는 가운데, 팬데믹 당시 비축해 둔 물품이 줄어들고 있음에도 불구하고 병원들은 교체 주기를 앞당기고 있습니다. 이러한 요인들이 복합적으로 작용하여, 수요가 급격히 증가하는 위기 상황 이외의 시기에도 기본적인 조달 수요가 유지되고 있습니다.

저·중소득 국가에서 정부 자금을 통한 중환자실 수용 능력 확대

저·중소득 국가에서는 중환자 치료 인프라에 여러 해에 걸친 예산을 배정하고 있습니다. 인도의 ‘아유슈만 바라트’ 프로그램에서는 2025-2026 회계연도에 64,180 카롤 루피를 예산으로 편성했으며, 그 중 12%가 지역 병원에 공급될 인공호흡기 구입에 배정되었습니다. ‘생산 연동형 인센티브(PLI)’ 제도에 따른 보조금에서는 증분 매출의 최대 5%가 환급되므로, 국내 조립 제품의 리드타임이 단축되고 있습니다. 2만 5,000달러 미만의 중저가형 기계식 인공호흡기는 기술적 요건을 충족하면서도 재정적 제약 조건에도 부합하여, 가격에 민감한 지역의 중환자실용 인공호흡기 시장을 확대되고 있습니다.

인공호흡기의 핵심 부품에 대한 공급망의 취약성

반도체 및 터빈 부족으로 인해 장비의 리드타임이 16-22주로 늘어났습니다. 공급망 회복탄력성에 관한 FDA 지침에서는 터빈과 압력 변환기가 고위험 부품으로 지목되고 있습니다. 정밀 가공된 티타늄 하우징은 독일과 일본의 일부 공급업체에 의존하고 있어, 휴대용 제품의 생산에 제약을 주고 있습니다. 미결 주문으로 인해 중환자실(ICU) 인공호흡기 시장에서 적시 납품이 차질을 빚고 있으며, 이로 인해 수익 창출에 제약을 받고 있습니다.

부문별 분석

휴대용 인공호흡기 시장은 2031년까지 연평균 성장률(CAGR) 7.50%를 나타낼 것으로 예측되며, 이 성장률은 중환자실용 인공호흡기 시장 전체의 평균 성장률인 6.99%를 상회합니다. 이러한 수요는 배터리 구동 시간과 터빈 송풍기를 중시하는 응급 서비스, 군 부대, 재택 간호로의 전환에서 비롯되고 있습니다. 휴대용 모델은 병원의 산소 배관이 필요하지 않기 때문에 더 광범위한 지역에서 사용할 수 있습니다. 2025년에 58.4%의 시장 점유율을 차지한 고정형 시스템은 통합 모니터링 네트워크를 갖춘 중증 환자용 중환자실(ICU)에서 여전히 필수적이지만, 선진국 시장공급 과잉으로 인해 교체 주기가 9년까지 길어지고 있습니다. 배터리 시험 기준을 명확히 한 FDA의 지침에 따라 승인 절차가 3개월 단축되었으며, 이로 인해 휴대용 제품 시장 출시가 가속화되어 중환자실(ICU) 인공호흡기 시장 내 점유율 확대를 뒷받침하고 있습니다.

고정식 유닛은 인공호흡기를 네트워크화된 경보 시스템이나 집중 가스 공급 시스템에 통합한 3차 의료 기관에서 여전히 주류를 이루고 있습니다. 유지보수 계약에서는 현재 원격 진단 및 소프트웨어 업그레이드가 중시되고 있어, 장비 교체 속도가 둔화되고 있음에도 불구하고 공급업체가 이익률을 유지하는 데 도움이 되고 있습니다. 지속가능성 목표가 더욱 엄격해지는 가운데, 대형 고정식 플랫폼조차도 저전력 소비 기준을 충족해야 하므로, 제조업체들은 터빈 개조나 기류 경로 최적화를 서둘러야 하는 상황에 놓여 있습니다. 이러한 업그레이드를 통해 고정형 기기의 기반은 여전히 그 중요성을 유지하는 한편, 휴대형 기기의 확대가 새로운 수익원을 개척함으로써 중환자실(ICU) 인공호흡기 시장의 이동성 환경에서 균형이 이루어지고 있습니다.

중급형 인공호흡기는 중저가 대에서 고급 모드를 요구하는 신흥 시장의 입찰에 힘입어 연평균 성장률(CAGR) 7.35%를 나타낼 것으로 전망됩니다. 현재 각 제조업체들은 2만 달러 미만의 기종에 기도압 해제 인공호흡 및 신경 조절식 호흡 보조 기능을 탑재하여, 고급 시스템과의 기능 격차를 좁히고 있습니다. 하이엔드 플랫폼은 원활한 전자건강기록(EHR) 통합과 첨단 모니터링이 필요한 4차 의료 기관에 힘입어, 2025년 중환자실(ICU) 인공호흡기 시장 규모의 52.1%를 차지했습니다. 그러나 중급 기종이 동등한 임상 성과를 내면서 가격 차이는 점차 줄어들고 있습니다.

저가형 기기는 지방의 진료소나 재난 대비 비축 분야에서 일정한 입지를 유지하고 있지만, 기능 세트가 제한적이며 새로운 ISO 경보 기준을 충족하지 못하기 때문에 판매량 측면에서 경쟁력이 제한되고 있습니다. 그 때문에 관심은 중급 모델로 쏠리고 있습니다. 각 기업은 AI 기반 이탈 알고리즘을 활용해 부가가치를 높이는 동시에 비용을 절감하고, 공공 조달 시장에서 중급 모델에 대한 수요를 확대함으로써 중환자실(ICU) 인공호흡기 시장 전체의 제품 구성을 재편하고 있습니다.

고급 인공호흡 모드 및 복합 인공호흡 모드는 2031년까지 연평균 성장률(CAGR) 7.42%를 나타낼 전망이며, 2025년에는 고주파 인공호흡 시장 점유율 48.6%를 넘어섰습니다. 이는 신생아 집중치료실(NICU)에서 조산아의 기압 손상을 최소화하기 위해 동기간적 강제 인공호흡(SIBV) 및 용적 보장 알고리즘이 채택되고 있기 때문입니다. 고주파 인공호흡은 중증 급성 호흡곤란 증후군(ARDS) 및 신생아 호흡곤란 증후군(RDS)의 주요 치료법으로 자리 잡고 있으며, 기도 내압의 최고치를 억제하면서 폐포의 재팽창을 유지하기 위해 분당 300-900회의 호흡을 제공합니다. 용적 제어 모드 및 압력 제어 모드는 성인 중환자실 환자의 대부분을 다루고 있으며, 의료진에게 친숙할 뿐만 아니라 모든 지역에서 규제 당국의 승인을 받았습니다. 각 제조업체들은 하이브리드형 플랫폼을 통해 이에 대응하고 있습니다. Dragerwerk사의 Babylog VN800은 고주파, 용량 제어 및 신경 조절 모드를 단일 기기에 통합하여, 다양한 환자층을 다루는 병원의 설비 투자 비용을 절감합니다.

지역별 분석

북미는 2025년에 37.2%의 점유율을 기록했으나, 재고 과잉으로 인한 공급 과잉이 장비 교체를 지연시키고 있어 향후 성장세는 완만해질 전망입니다. 이 지역은 AI를 활용한 폐쇄 루프 제어의 도입 및 터빈식 휴대용 기기의 보급에 있어 주도적인 입지를 차지하고 있습니다. 캐나다에서는 장비의 배출량을 평가하는 ‘카본 대시보드’의 시범 운영이 진행되고 있으며, 조달을 탄소 중립 목표 달성과 연계하고 있습니다. 각 벤더들은 중환자실(ICU) 인공호흡기 시장에서 서비스 수익을 창출하기 위해, 하드웨어와 분석 서비스 구독권을 묶어 판매하는 사례가 늘고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 7.23%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국은 Mindray와 Comen 등 국내 공급업체에 대한 승인 절차를 신속히 진행하고 있는 반면, 인도는 생산 장려 정책을 통해 2028년까지 15억 달러 규모의 의료기기 생산을 목표로 하고 있습니다. 아세안(ASEAN)의 규제 조화를 통해 승인까지 소요되는 기간이 6개월 단축되었습니다. 일본에서는 2025년에 65세 이상 인구가 27%에 달할 정도로 고령화가 진행되었으며, 폐렴이나 만성폐쇄성폐질환(COPD)으로 인한 중환자실 입원 환자 수가 여전히 높은 수준을 유지하고 있습니다. 이러한 추세에 따라, 중환자실(ICU) 인공호흡기 시장에서 해당 지역의 점유율이 확대되고 있습니다.

유럽에서는 의료기기 규정(MDR)에 따른 재인증 비용이 제품 라인당 평균 50만 유로가 듭니다. 높은 규정 준수 비용은 기존 제조업체에 유리하지만, 신제품 출시를 지연시키고 있습니다. 이탈리아와 스페인에서는 인공호흡기 비용을 자본 지출에서 운영비로 전환하는 리스 모델을 시범적으로 도입하여, 병원의 재정적 부담을 줄이면서도 중환자실용 인공호흡기 시장 수요를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the intensive care unit ventilators market size is expected to increase from USD 2.9 billion in 2025 to USD 3.10 billion in 2026 and reach USD 4.43 billion by 2031, growing at a CAGR of 6.99% over 2026-2031.

This report is Segmented by Mobility Type (Stationary, Portable), Product Type (High-End, Mid-End, Low-End), Mode (Volume-Controlled and More), Patient Age Group (Adult, Pediatric, Neonatal), Interface (Invasive, Non-Invasive), End-User (Hospitals and More), Technology (Mechanical, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Intensive Care Unit (ICU) Ventilators Market Trends and Insights

Surging Incidence of Acute Respiratory Distress Syndrome

ARDS remains a core demand driver for the ICU ventilators market. U.S. incidence stands at 64 per 100,000 population, and the condition accounts for 10%-15% of global ICU admissions. Mortality of 30%-50% keeps clinical focus on precision-titrated ventilation that limits lung injury. Seasonal wildfire smoke in North America and persistent air-quality challenges in South Asia elevate ARDS case peaks. As OECD populations age, hospitals front-load replacement cycles even while pandemic stockpiles depreciate. Together, these patterns sustain baseline procurement beyond crisis surges.

Government-Funded ICU Capacity Expansion in LMICs

Low- and middle-income countries allocate multiyear budgets to critical-care infrastructure. India's Ayushman Bharat program sets aside INR 64,180 crore for 2025-2026, with 12% geared to ventilators in district hospitals. Subsidies under the Production-Linked Incentive scheme reimburse up to 5% of incremental sales, shortening lead times for domestically assembled units. Mid-end mechanical ventilators priced under USD 25,000 meet technical requirements while aligning with fiscal constraints, expanding the ICU ventilators market in price-sensitive regions.

Supply-Chain Fragility for Critical Ventilator Components

Semiconductor and turbine shortages extend device lead times to 16-22 weeks. FDA guidance on supply resilience flags turbines and pressure transducers as high-risk parts. Precision-machined titanium housings rely on a limited vendor base in Germany and Japan, constraining portable production. Backlogs hamper timely fulfillment and limit revenue capture in the ICU ventilators market.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Turbine-Based Portable Ventilators

- Rapid Installation of AI-Driven Closed-Loop Ventilation

- Stringent Regulatory Re-Certification for Software-Driven Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Portable ventilators are forecast to grow at 7.50% CAGR through 2031, a rate that surpasses the 6.99% average for the ICU ventilators market. Demand arises from emergency services, military units, and home-care transitions that value battery autonomy and turbine blowers. Portable models bypass the hospital pipeline oxygen, enabling a broader geographic reach. Stationary systems, which captured 58.4% share in 2025, remain essential for high-acuity ICUs with integrated monitoring networks, yet overcapacity in developed markets lengthens their replacement intervals to nine years. The FDA guidance that clarifies battery testing streamlined approvals by three months, accelerating portable launches and supporting their climb within the ICU ventilators market.

Stationary units still dominate in tertiary hospitals that embed ventilators into networked alarm systems and centralized gas supplies. Maintenance contracts now emphasize remote diagnostics and software upgrades, helping vendors preserve margin despite slower unit turnover. As sustainability targets tighten, even large fixed platforms must meet lower wattage thresholds, nudging manufacturers to retrofit turbines and optimize airflow paths. These upgrades keep the stationary base relevant while portable expansion unlocks new revenue streams, balancing the mobility landscape of the ICU ventilators market.

Mid-end ventilators are projected to advance at a 7.35% CAGR, buoyed by emerging-market tenders that demand sophisticated modes at mid-tier prices. Manufacturers now embed airway pressure release ventilation and neurally adjusted ventilatory assist into sub-USD 20,000 units, narrowing functional gaps with high-end systems. High-end platforms held 52.1% share of the ICU ventilators market size in 2025, sustained by quaternary hospitals that require seamless EHR integration and advanced monitoring. Yet price premiums soften as mid-end units deliver comparable clinical outcomes.

Low-end devices maintain footholds in rural clinics and disaster stockpiles, but their limited feature sets and inability to meet new ISO alarm standards restrict volume-competitive focus, therefore, swings to mid-range models. Companies leverage AI-driven weaning algorithms to add value while holding costs, expanding mid-end traction in public procurement, and reshaping product mix across the ICU ventilators market.

Advanced and combined ventilation modes are expanding at 7.42% CAGR through 2031, outpacing high-frequency ventilation's 48.6% market share in 2025, as neonatal intensive care units adopt synchronized intermittent mandatory ventilation and volume-guarantee algorithms that minimize barotrauma in preterm infants. High-frequency ventilation remains the workhorse for severe ARDS and neonatal respiratory distress syndrome, delivering 300 to 900 breaths per minute to maintain alveolar recruitment while limiting peak airway pressures. Volume-controlled and pressure-controlled modes serve the bulk of adult ICU cases, offering clinician familiarity and regulatory approval across all geographies. Manufacturers are responding with hybrid platforms. Dragerwerk's Babylog VN800 offers high-frequency, volume-controlled, and neurally adjusted modes in a single device that reduce capital expenditure for hospitals managing diverse patient populations.

Geography Analysis

North America held 37.2% share in 2025, yet future growth is moderated by stockpile-driven overcapacity that delays fleet refresh. The region leads in AI-enabled closed-loop adoption and turbine portable penetration. Canada pilots carbon dashboards that score device emissions, tying procurement to net-zero milestones. Vendors increasingly package analytics subscriptions with hardware to unlock service revenue in the ICU ventilators market.

Asia-Pacific is the fastest-growing region at 7.23% CAGR through 2031. China issues accelerated clearances for domestic suppliers such as Mindray and Comen, while India's production incentives strive for USD 1.5 billion medical-device output by 2028.ASEAN harmonization trims regulatory timelines by six months. Japan's aging population, with 27% over 65 years in 2025, sustains ICU admissions for pneumonia and COPD. These dynamics enlarge the regional share of the ICU ventilators market.

Europe faces Medical Device Regulation recertification expenses averaging EUR 500,000 per line. High compliance cost favors incumbents but slows new product rollouts. Italy and Spain pilot leasing models that shift ventilator costs from capital to operating budgets, easing fiscal pressure on hospitals while maintaining flow in the ICU ventilators market.

- Air Liquide

- Allied Healthcare Products

- Bunnell Inc.

- Demcon

- Dragerwerk

- Fisher & Paykel Healthcare

- GE Healthcare

- Getinge

- Hamilton Medical

- ICU Medical

- Koninklijke Philips

- Medtronic

- Mindray Medical International Inc.

- Nihon Kohden

- Resmed

- Schiller

- Shenzhen Comen Medical Instruments

- Zoll Medical Corporation (Vyaire Medical Inc.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Incidence of Acute Respiratory Distress Syndrome (ARDS)

- 4.2.2 Government-Funded ICU Capacity Expansion in LMICs

- 4.2.3 Integration of Turbine-Based Portable Ventilators

- 4.2.4 Rapid Installation of AI-Driven Closed-Loop Ventilation

- 4.2.5 Rising Adoption of Non-Invasive Ventilation in General Wards

- 4.2.6 Hospital Sustainability Mandates for Energy-Efficient Fleets

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Fragility for Critical Ventilator Components

- 4.3.2 Stringent Regulatory Re-Certification for Software-Driven Units

- 4.3.3 Persistent Post-Pandemic ICU Overcapacity in Developed Markets

- 4.3.4 Uptake of High-Flow Nasal Cannula Curbing Ventilator Demand

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Mobility Type

- 5.1.1 Stationary Ventilators

- 5.1.2 Portable Ventilators

- 5.2 By Product Type

- 5.2.1 High-End ICU Ventilators

- 5.2.2 Mid-End ICU Ventilators

- 5.2.3 Low-End ICU Ventilators

- 5.3 By Mode

- 5.3.1 Volume-Controlled Ventilation

- 5.3.2 Pressure-Controlled Ventilation

- 5.3.3 High-Frequency Ventilation

- 5.3.4 Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation)

- 5.4 By Patient Age Group

- 5.4.1 Adult

- 5.4.2 Pediatric

- 5.4.3 Neonatal

- 5.5 By Interface

- 5.5.1 Invasive Ventilation

- 5.5.2 Non-Invasive Ventilation

- 5.6 By End-user

- 5.6.1 Hospitals

- 5.6.2 Ambulatory Surgical Centers

- 5.6.3 Specialty Clinics

- 5.6.4 Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation)

- 5.7 By Technology (Value)

- 5.7.1 Mechanical Ventilators

- 5.7.2 Pnematic Ventilators

- 5.7.3 Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation)

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 India

- 5.8.3.3 Japan

- 5.8.3.4 South Korea

- 5.8.3.5 Australia

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East and Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East and Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Air Liquide Medical Systems

- 6.3.2 Allied Healthcare Products Inc.

- 6.3.3 Bunnell Inc.

- 6.3.4 Demcon

- 6.3.5 Dragerwerk AG & Co. KGaA

- 6.3.6 Fisher & Paykel Healthcare Limited

- 6.3.7 GE Healthcare

- 6.3.8 Getinge AB

- 6.3.9 Hamilton Medical

- 6.3.10 ICU Medical Inc. (Smiths Medical)

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Medtronic plc

- 6.3.13 Mindray Medical International Inc.

- 6.3.14 Nihon Kohden Corporation

- 6.3.15 ResMed

- 6.3.16 Schiller AG

- 6.3.17 Shenzhen Comen Medical Instruments

- 6.3.18 Zoll Medical Corporation (Vyaire Medical Inc.)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment