|

시장보고서

상품코드

2063502

젖산 측정기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Lactate Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

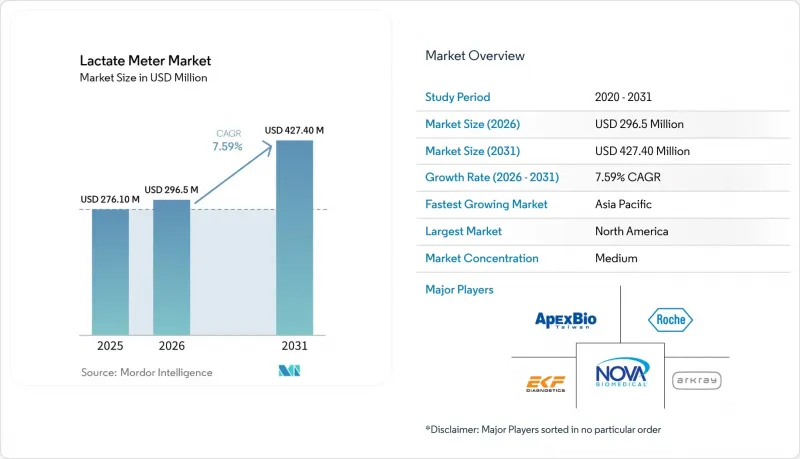

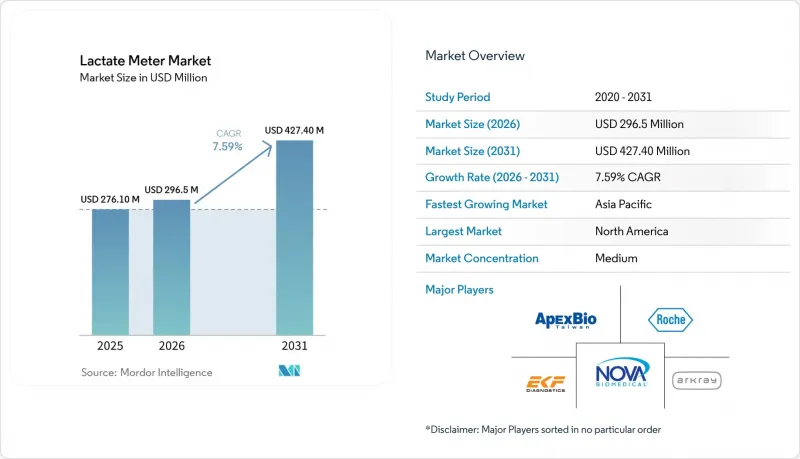

Mordor Intelligence에 의하면, 젖산 측정기 시장 규모는 2025년에 2억 7,610만 달러로 평가되었습니다. 2026년에 2억 9,650만 달러에서 2031년까지 4억 2,740만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 7.59%를 나타낼 전망입니다.

본 보고서는 제품 유형(휴대용 측정기, 벤치탑/테이블탑 분석기), 전원(건전지식, 충전식/재충전식), 기술(전기화학 센서, 광학 센서 등), 용도(의료 개입 등), 최종 사용자(병원 및 진료소 등) 및 지역(북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 젖산 측정기 시장 동향 및 인사이트

휴대형 및 연결형 POC 기기로의 급속한 전환

응급실에서는 젖산 측정 소요 시간을 30-45분에서 2분 미만으로 단축하기 위해 휴대용 측정기 도입이 표준화되어 있으며, ‘생존 패혈증 캠페인(Surviving Sepsis Campaign)’의 ‘1시간 차 번들’을 지원하고 있습니다. 전자 차트와 직접 연동함으로써 전사 오류가 제거되고, 젖산 클리어런스 추이 분석이 자동화됩니다. 공유 충전과 관련된 복잡한 물류 프로세스로 인한 교대 업무 인계를 피할 수 있기 때문에 배터리 구동 방식의 설계가 주류를 이루고 있습니다. FDA의 CLIA 면제 제도는 성능 기준을 변동계수 10% 미만으로 제한함으로써 시장 진입을 가속화하고 있습니다. 병원들이 사이버 보안상의 위험과 예측 유지보수의 이점을 저울질하는 가운데, 클라우드 연결에 대해서는 여전히 찬반 의견이 엇갈리고 있습니다. 그러나 각 벤더사는 미래를 내다보며 계속해서 기기에 블루투스 모듈을 탑재하고 있습니다. 이러한 전환으로 인해 소모품에 대한 수요가 증가하고 있습니다. 이는 각 휴대용 기기에 사용되는 스트립이 일회용이기 때문이며, 이로 인해 하드웨어 도입이 지속적인 수익으로 직결됩니다.

엘리트 및 아마추어 스포츠 프로그램에서의 도입 확대

측정기 가격이 300달러 미만으로 떨어지고, 테스트 스트립 비용이 2달러 미만으로 낮아지면서, 젖산 역치 테스트는 올림픽 훈련 센터에서 NCAA 프로그램과 아마추어 사이클링 클럽으로까지 확산되었습니다. 스페인과 독일의 엘리트 축구 아카데미에서는 현재 주 1회 테스트를 실시하여 인터벌 트레이닝의 강도를 개인별로 조정하고 있습니다. 이는 유전적 변이 때문에 고정 심박수 구간에서는 선수의 30%가 잘못 분류되기 때문입니다. 한국과 유럽연합(EU)에서는 웨어러블형 발한 젖산 측정 시범 사업이 진행되고 있으며, 이는 운동선수들의 비침습적 측정 방법에 대한 수요를 반영하고 있습니다. 스포츠 기관에서는 진단 예산을 통합하기 위해 혈당 수치와 헤모글로빈도 측정할 수 있는 다중 매개변수 플랫폼을 점점 더 선호하고 있습니다. 스포츠용 젖산 측정 기기를 규정하는 ISO 규격이 존재하지 않기 때문에 제조업체들은 장기간에 걸친 임상 검증 연구를 생략하고 있으며, 이로 인해 시장 출시까지의 기간은 단축되었지만 성능에 편차가 발생하고 있습니다.

자원이 부족한 환경에서 1회당 소모품 비용이 높다는 점

2-8달러에 달하는 스트립 가격은 47개 저소득국의 1일 의료비 상한선을 초과하고 있어, 임상의들은 검사를 제한할 수밖에 없습니다. 다항목 분석 장치는 비용 분산을 목표로 하고 있지만, 설비 투자 부담을 가중시키고 있습니다. 종이 기반 프로토타입은 1달러 미만의 가격을 약속하고 있지만, WHO의 사전 승인을 받지 못했으며, 동아프리카 판매업자의 마진으로 인해 소매 가격은 더욱 치솟고 있습니다. 검사의 제한은 패혈증의 조기 발견을 저해하고, 공공 의료기관 내 젖산 측정기 시장의 확장을 방해하고 있습니다.

부문별 분석

2025년에는 휴대용 기기가 젖산 측정기 시장의 63.50% 점유율을 차지했으며, 2분 미만의 검사 결과 보고 시간을 중시하는 응급 의료 업무 흐름에 힘입어 2031년까지 연평균 성장률(CAGR) 7.80%를 나타낼 전망입니다. 벤치탑형 분석 장치는 하루 최대 500개의 검체를 처리하는 중앙 검사실을 위해 제공되며, HL7 메시징을 통해 LIS(검사 정보 시스템)와 연동됩니다. 처리 능력이 뛰어나고 효소 드리프트를 줄여주는 광학 검출 방식을 채택하고 있지만, 초기 투자 비용과 18개월의 서비스 계약이 소규모 병원의 도입을 가로막고 있습니다. 스포츠 모니터링이나 수의학 현장에서는 코치나 수의사가 전원이 없는 환경에서 현장 검사를 수행하기 때문에 휴대용 기기가 주류를 이루고 있습니다. 한편, 벤치탑형 분석 장치는 제약 업계의 품질 관리(QC) 실험실에서 마이크로유체 칩을 기준 분석법과 비교 검증하는 데 있어 여전히 필수적인 역할을 하고 있습니다. 규제상의 이점이 휴대용 기기의 우위를 더욱 공고히 하고 있습니다. CLIA 면제 자격에 따라, 측정기의 변동계수가 10% 미만이면 조작자는 기능 시험을 면제받습니다.

2025년 매출의 78.60%를 차지한 것은 배터리식 측정기이며, 응급 의료 부문과 지방 진료소들이 충전 인프라가 필요 없는 일회용 알칼리 배터리를 중시하고 있기 때문에 연평균 성장률(CAGR) 8.00%를 나타낼 전망입니다. 충전식 플랫폼은 EU 그린딜과의 지속가능성 일관성을 추구하는 유럽의 스포츠 기관들로부터 지지를 받고 있습니다. 리튬이온식 유닛은 300-500회의 충방전 주기를 지원하지만, 배터리식 모델보다 100-150달러 비싸기 때문에 투자 회수 기간이 길어집니다. 미국 병원의 감염 관리 지침에 따라 충전기 공유가 권장되지 않기 때문에 일회용 제품에 대한 선호도가 높아지고 있습니다. 아시아태평양의 현장 진료소에서는 태양광 발전 방식을 이용한 충전기가 도입되고 있지만, 배터리식 제품의 판매 대수는 여전히 충전식 제품의 출하 대수를 웃돌고 있습니다. 리튬 공급망의 부품 부족은 충전식 제품의 비용 경쟁력을 약화시킬 가능성이 있으며, 이는 젖산 측정기 시장에서 배터리식 제품의 우위를 더욱 공고히할 것입니다.

지역별 분석

아시아태평양의 연평균 성장률(CAGR) 8.03%는 공중보건 프로그램을 통해 POC(현장) 진단이 3차 병원부터 군 단위 시설로 확대됨에 따라, 젖산 측정기 시장의 구조적 전환을 시사하고 있습니다. ‘건강 중국 2030’ 정책에 따라, 중국 내에서만 2030년까지 3,000개 이상의 군립 병원에 휴대용 측정기를 도입할 계획이며, 이 정책은 농촌 주민의 패혈증 조기 발견을 위해 젖산 검사를 포함하는 것입니다. 인도의 ‘아유슈만 바라트’ 개혁에 따라 15만 곳의 건강·웰니스 센터에 자금이 투입되고 있으며, 각 센터에는 젖산 스트립을 포함한 필수 진단 장비 예산이 편성되어 있습니다. 이로 인해 대량 주문이 발생하여 가격 탄력성이 향상되고 있습니다. 한국과 일본에서는 견고한 통신 인프라를 바탕으로 웨어러블 센서의 시범 도입이 가속화되고 있으며, 규제가 명확해지는 대로 해당 지역에서는 비침습적 진단 기술이 급속히 보급될 준비가 되어 있습니다.

북미는 확고히 자리 잡은 510(k) 승인 제도, 확립된 보험 환급 제도, 그리고 병원의 전자 진료 기록(EMR)과의 통합을 통해 기술적 리더십을 유지하고 있습니다. 미국에서는 구급차에 휴대용 측정기를 탑재한 응급의료 서비스가 제공되고 있으며, 유럽도 이제야 이를 따르기 시작하면서 병원 도착 전 단계 수요를 창출하고 있습니다. 캐나다의 각 주에서는 외딴 지역의 원주민 커뮤니티에서 POC 젖산 측정을 위한 보조금을 지급함으로써 지방 지역의 접근성을 확대되고 있습니다. 멕시코의 민간 병원 그룹은 미국 공급업체로부터 배터리식 측정기를 수입하고 있지만, 공공 부문에서의 도입은 여전히 테스트 스트립 비용 때문에 제한적입니다.

유럽의 성숙한 상환 제도는 폭발적인 성장이라기보다는 꾸준한 갱신 주기를 뒷받침하는 기반이 되고 있습니다. 독일의 DRG(진단 관련 그룹) 인센티브 제도는 신속한 젖산 수치 추적을 통해 중환자실(ICU) 입원 기간을 단축한 병원에 보상을 제공함으로써, POC의 처리 능력을 향상시키고 있습니다. 프랑스와 스페인은 GDPR(EU 개인정보보호규정)에 기반한 연결 기기의 사이버 보안 규정 준수에 중점을 두고 있으며, 클라우드 서비스 도입은 더딘 편이지만 로컬 데이터 저장 솔루션을 장려하고 있습니다. 영국에서는 NHS 잉글랜드의 패혈증 치료 프로토콜을 활용하여 트러스트(지역 의료권) 차원에서 휴대용 측정기 조달을 정당화하고 있지만, 예산 제약으로 인해 경쟁 입찰이 의무화되면서 테스트 스트립 가격 하락으로 이어지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the lactate meter market size is projected to be USD 276.10 million in 2025, USD 296.5 million in 2026, and reach USD 427.40 million by 2031, growing at a CAGR of 7.59% from 2026 to 2031.

This report is Segmented by Product Type (Handheld Meters, and Benchtop/Tabletop Analyzers), by Power Source (Battery-Operated, Chargeable/Rechargeable), by Technology (Electrochemical Sensors, Optical Sensors, and More), by Application (Medical Intervention, and More), by End-User (Hospitals & Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Lactate Meter Market Trends and Insights

Rapid Shift Toward Handheld and Connected POC Devices

Emergency departments have standardized handheld meters to compress lactate turnaround time from 30-45 minutes to under 2 minutes, supporting the Surviving Sepsis Campaign hour-1 bundle. Direct integration with electronic medical records eliminates transcription errors and automates lactate-clearance trending. Battery-operated designs dominate because they bypass shared charging logistics that complicate shift handover. The FDA's CLIA-waiver pathway accelerates market entry by limiting performance criteria to a coefficient of variation below 10%. Cloud connectivity remains polarizing as hospitals weigh cybersecurity exposure against predictive-maintenance benefits, yet vendors continue to embed Bluetooth modules to future-proof devices. The shift has raised consumable demand because each handheld strip is single-use, linking hardware adoption directly to recurring revenue.

Growing Adoption by Elite & Amateur Sports Programs

Lactate-threshold testing migrated from Olympic training centers to NCAA programs and amateur cycling clubs when meter pricing fell below USD 300 and strip costs dropped under USD 2. Elite soccer academies in Spain and Germany now conduct weekly tests to individualize interval workloads, noting that fixed heart-rate zones misclassify 30% of athletes due to genetic variability. Wearable sweat-lactate pilots run in South Korea and the European Union, reflecting athlete demand for non-invasive options. Sports institutes increasingly favor multi-parameter platforms that also capture glucose and hemoglobin to consolidate diagnostics budgets. Because no ISO standard governs sports lactate devices, vendors bypass lengthy clinical-validation studies, accelerating time-to-market but raising performance variability.

High Per-Test Consumable Cost in Low-Resource Settings

Strip prices between USD 2 and USD 8 exceed daily health-spending limits in 47 low-income countries, forcing clinicians to ration tests. Multi-analyte devices aim to amortize costs but raise capital requirements. Paper-based prototypes promise sub-USD 1 pricing yet lack WHO prequalification, and distributor mark-ups in East Africa push retail prices even higher. Rationing undermines early sepsis detection, limiting the lactate meter market in public-sector facilities.

Other drivers and restraints analyzed in the detailed report include:

- ICU Protocols Mandating Lactate Tracking for Sepsis Bundles

- Reimbursement Expansion for Emergency Lactate Testing (US & EU)

- Regulatory Uncertainty Over Non-Invasive Measurement Accuracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Handheld devices secured 63.50% of the lactate meter market share in 2025 and will climb at a 7.80% CAGR through 2031, bolstered by emergency workflows favoring sub-2-minute turnaround times. Benchtop analyzers serve central laboratories that process up to 500 daily samples and integrate with LIS under HL7 messaging. Despite higher throughput and optical detection that mitigates enzyme drift, their capital cost and 18-month service contracts deter small hospitals. Handheld units prevail in sports monitoring and veterinary practice because coaches and vets conduct field-side testing without power outlets. Benchtop analyzers remain indispensable in pharmaceutical QC labs, validating micro-fluidic chips against reference assays. Regulatory advantages amplify the handheld edge; CLIA-waived status exempts operators from proficiency testing if meters stay below 10% coefficient of variation.

Battery-operated meters controlled 78.60% of 2025 revenue and will grow at 8.00% CAGR as EDs and rural clinics value disposable alkaline cells that eliminate recharging infrastructure. Rechargeable platforms appeal to European sports institutes seeking sustainability alignment with the EU Green Deal. Lithium-ion units support 300-500 cycles but cost USD 100-150 more than battery models, extending payback periods. Infection-control protocols in U.S. hospitals discourage shared chargers, reinforcing disposable preference. Asia-Pacific field clinics adopt solar-assisted chargers, yet battery sales continue to outpace rechargeable shipments. Component shortages in lithium supply chains could erode rechargeables' cost advantage, further cementing battery dominance in the lactate meter market.

Geography Analysis

Asia-Pacific's 8.03% forecast CAGR signals a structural pivot in the lactate meter market as public-health programs extend POC diagnostics beyond tertiary hospitals into county-level facilities. China alone intends to outfit more than 3,000 county hospitals with handheld meters by 2030 under Healthy China 2030, a policy that embeds lactate testing into early sepsis recognition for rural populations. India's Ayushman Bharat transformation funds 150,000 health-and-wellness centers, each budgeted for essential diagnostics including lactate strips creating volume orders that improve price elasticity. South Korea and Japan accelerate wearable sensor trials facilitated by robust telecom infrastructure, positioning the region for rapid non-invasive adoption once regulatory clarity emerges.

North America retains technology leadership due to entrenched 510(k) clearances, established reimbursement, and hospital EMR integration. United States. emergency medical services equip ambulances with handheld meters, adding pre-hospital demand that Europe is only beginning to replicate. Canadian provinces subsidize POC lactate in remote Indigenous communities, widening rural access. Mexico's private-hospital groups import battery-operated meters from U.S. vendors, but public-sector uptake remains limited by strip costs.

Europe's mature reimbursement anchors steady replacement cycles rather than explosive growth. Germany's DRG incentives reward hospitals that shorten ICU stays via rapid lactate-clearance tracking, boosting POC throughput. France and Spain focus on connected-device cybersecurity compliance under GDPR, delaying cloud launches but encouraging local data-residency solutions. The United Kingdom leverages NHS England's sepsis pathway to justify trust-level procurement of handheld meters, although budget constraints enforce competitive tendering that squeezes strip pricing.

- Roche

- EKF Diagnostics Holdings PLC

- Nova Biomedical

- Arkray

- Sensa Core Medical Instrumentation Pvt. Ltd.

- ApexBio

- BST Bio Sensor Technology

- TaiDoc Technology

- Analox Instruments Ltd

- Xylem Inc.

- PKvitality

- TECOM Analytical Systems

- VivaChek Biotech

- Woodley Equipment Company

- Jorgensen Laboratories

- Abbott Laboratories

- Danaher

- Yellow Springs Instrument (YSI)

- Cosmed

- Bionime

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Shift Toward Handheld and Connected POC Devices

- 4.2.2 Growing Adoption by Elite & Amateur Sports Programs

- 4.2.3 ICU Protocols Mandating Lactate Tracking for Sepsis Bundles

- 4.2.4 Reimbursement Expansion for Emergency Lactate Testing (US & EU)

- 4.2.5 Wearable Sweat-Lactate Sensors Entering Pilot Deployments

- 4.2.6 Pharma R&D Using Micro-Fluidic Lactate Chips for Cell-Culture

- 4.3 Market Restraints

- 4.3.1 High Per-Test Consumable Cost in Low-Resource Settings

- 4.3.2 Regulatory Uncertainty Over Non-Invasive Measurement Accuracy

- 4.3.3 Data-Privacy Hurdles for Cloud-Connected Meters In EU

- 4.3.4 Supply-Chain Exposure to Specialty Enzymes & Membranes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Handheld Meters

- 5.1.2 Benchtop/Tabletop Analyzers

- 5.2 By Power Source

- 5.2.1 Battery-operated

- 5.2.2 Chargeable/Rechargeable

- 5.3 By Technology

- 5.3.1 Electrochemical Sensors

- 5.3.2 Optical Sensors

- 5.3.3 Biosensors

- 5.3.4 Other Technology

- 5.4 By Application

- 5.4.1 Medical Intervention

- 5.4.2 Sports Performance Monitoring

- 5.4.3 Veterinary

- 5.4.4 Other Applications

- 5.5 By End-user

- 5.5.1 Hospitals & Clinics

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Sports Institutes & Teams

- 5.5.4 Other End-User

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 F. Hoffmann-La Roche AG

- 6.3.2 EKF Diagnostics Holdings PLC

- 6.3.3 Nova Biomedical

- 6.3.4 Arkray, Inc.

- 6.3.5 Sensa Core Medical Instrumentation Pvt. Ltd.

- 6.3.6 ApexBio

- 6.3.7 BST Bio Sensor Technology

- 6.3.8 TaiDoc Technology Corporation

- 6.3.9 Analox Instruments Ltd

- 6.3.10 Xylem Inc.

- 6.3.11 PKvitality

- 6.3.12 TECOM Analytical Systems

- 6.3.13 VivaChek Biotech

- 6.3.14 Woodley Equipment Company

- 6.3.15 Jorgensen Laboratories

- 6.3.16 Abbott Laboratories

- 6.3.17 Danaher Corporation

- 6.3.18 Yellow Springs Instrument (YSI)

- 6.3.19 COSMED srl

- 6.3.20 Bionime Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment