|

시장보고서

상품코드

2063505

헬스케어 계약 관리 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Healthcare Contract Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

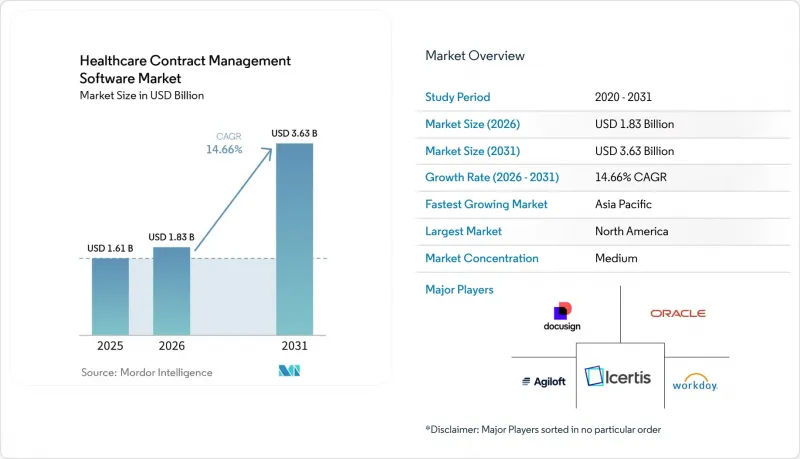

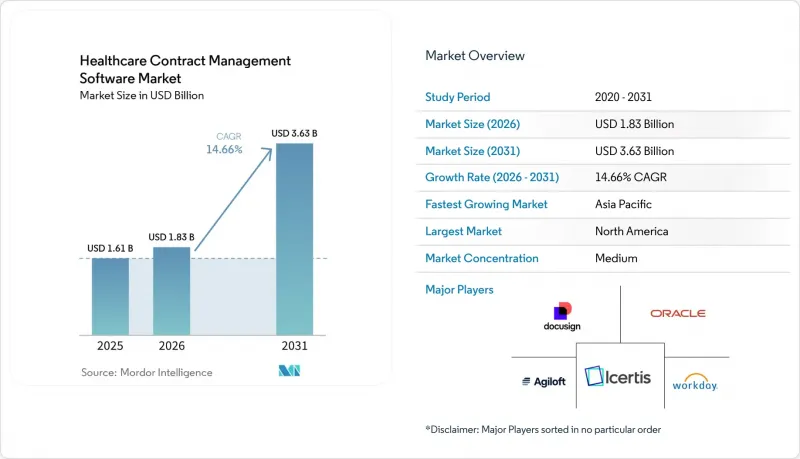

Mordor Intelligence에 의하면, 헬스케어 계약 관리 소프트웨어 시장 규모는 2025년 16억 1,000만 달러에서 2026년에는 18억 3,000만 달러로 확대되어 2031년까지 36억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 14.66%로 성장할 전망입니다.

본 보고서는 솔루션 유형(계약 수명주기 관리, 문서 관리, 벤더/공급업체 시스템, 기타), 도입 형태(클라우드, On-Premise), 최종 사용자(프로바이더, 기타), 조직 규모(대기업, 중견기업, 중소기업), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

전 세계 헬스케어 계약 관리 소프트웨어 시장 동향 및 인사이트

의료 분야의 규정 준수를 최우선으로 하는 디지털화(HIPAA/GDPR(EU 개인정보보호규정)에 기반한 CLM 도입)

개인정보 및 보안 감시가 강화됨에 따라, 조직들은 계약 거버넌스의 표준화를 지속적으로 요구받고 있습니다. HIPAA 요건에 따라 클라우드 제공업체, EHR 공급업체, 청구 서비스 업체 및 기타 파트너와 체결한 업무 제휴 계약(BAA)의 필요성이 높아지면서 정보 유출 위험을 줄이고 있습니다. 감사 및 사고 보고에 대한 기대가 높아지는 가운데, 병원과 보험사는 폴더, 공유 드라이브, 이메일을 통한 문서 작성을 단계적으로 폐지하고, 역할 기반 접근 제어와 기밀 기록에 대한 모든 조작을 기록하는 변경 불가능한 감사 추적을 갖춘 통합 저장소로 전환을 추진하고 있습니다. 자동화된 규정 준수 점검 및 갱신 알림을 통해 팀은 미체결된 BAA나 만료된 조항을 벌칙이 부과되기 전에 파악할 수 있습니다. 이를 통해 더 중요한 협상에 시간을 할애할 수 있게 되며, 심사 시 규정 위반 가능성을 줄일 수 있습니다. 이와 유사한 거버넌스상의 압박은 엄격한 개인정보 보호 및 보안 기준을 시행하는 다른 규제 관할 구역에서도 적용되고 있으며, 이로 인해 헬스케어 계약 관리 소프트웨어 시장 전반에 걸쳐 조항 라이브러리 자동화, 승인 절차 및 증거 수집의 필요성이 더욱 커지고 있습니다. 시스템 접근, ID 관리 및 직무 분담에 관한 정책이 성숙해짐에 따라, 조직은 법무, 컴플라이언스, 조달 및 IT 부서를 연계하여 계약 및 관련 의무에 관한 ‘단일한 진실’을 유지함으로써, 수작업에 의한 업무 인계 및 잠재적 위험을 줄이고 있습니다.

클라우드 퍼스트 도입과 구독형 가격 책정은 도입과 ROI 달성을 용이하게 합니다.

SaaS 플랫폼은 전용 하드웨어, 데이터베이스 관리 및 재해 복구 체계 구축을 불필요하게 만들어, 이를 통해 자원이 제한된 IT 팀이라도 예측 가능한 운영 비용과 신속한 가치 실현(Time to Value)을 달성하면서 엔터프라이즈급 CLM을 구축할 수 있게 해줍니다. 구독형 가격 정책과 간소화된 사용자 경험(UX) 덕분에 외래 진료소 및 행동 의료 기관의 도입 장벽이 낮아집니다. 한편, 확장 가능한 테넌트 환경과 지속적인 업데이트를 통해, 길어지는 패치 적용 주기 없이 보안 기준을 최신 상태로 유지할 수 있습니다. 또한, 의료 팀은 일반적인 생산성 제품군 및 업무 시스템과 연동되는 통합형 전자 서명, 워크플로우 라우팅, ID 관리 서비스의 이점을 활용하여 협상을 원활하게 진행하고 문서화를 확실하게 완료할 수 있습니다. 의사결정권자들이 대안을 검토하는 과정에서 클라우드 기반 CLM이 승인 절차를 가속화하고 원격 협업을 가능하게 하며, On-Premise 환경의 사일로화에서는 정량화하기 어려웠던 사이클 타임 및 병목 현상에 대한 분석 정보를 시각화한다는 점을 인식하고 있습니다. 이러한 기본 기능 덕분에, 위험이 적은 현대화 방안을 모색하는 중견/중소기업을 중심으로 헬스케어 계약 관리 소프트웨어 시장의 보급이 더욱 촉진될 것입니다.

레거시 IT 통합, 데이터 마이그레이션 및 보안 과제

여러 EHR, ERP 및 맞춤형 수익 주기 시스템을 포함하는 이종 혼합 환경은 데이터 매핑 및 인터페이스 설계를 복잡하게 만들어 도입 기간을 연장하거나, 전환 과정에서 병렬 처리 부담을 야기할 가능성이 있습니다. 팀은 하류 분석의 신뢰성을 높이고 대규모 감사에 대응할 수 있도록 레거시 필드의 표준화, 아카이브 저장소의 정리, 그리고 조항 메타데이터의 검증을 수행해야 합니다. HITRUST나 SOC 2 Type II와 같은 보안 인증은 의료 분야 조달 과정에서 필수 조건으로 요구되는 경우가 많으며, 증빙 자료나 관리 체계가 최신 상태가 아닐 경우 공급업체의 자격 박탈이나 승인 지연으로 이어질 수 있습니다. 대폭적인 맞춤 설정이나 독자적인 데이터 요구 사항을 가진 조직의 경우, 도입 일정이 장기화될 가능성이 있으며, 직원들이 변화와 일상 업무를 병행하는 과정에서 단기적인 ROI 달성이 지연될 우려가 있습니다. 구매자가 흩어져 있는 문서를 통합하거나, 임상, 재무, 공급망 워크플로우와 통합 및 조정하는 데 필요한 노력을 과소평가하는 경우, 이러한 현실이 헬스케어 계약 관리 소프트웨어 시장에 계속해서 역풍으로 작용하고 있습니다.

부문별 분석

계약 수명주기 관리 소프트웨어는 2025년에 47.66%의 시장 점유율을 차지해, 이는 다양한 헬스케어 계약의 작성, 협상, 체결 및 의무 관리에 대한 수요를 반영한 것입니다. 이 카테고리의 광범위한 적용 범위는 헬스케어 계약 관리 소프트웨어 시장에서 법무 및 영업 팀이 의료 서비스 제공업체, 보험사, 공급업체 전반에 걸쳐 일관된 거버넌스를 확대하기 위해 사용하는 템플릿, 조항 라이브러리 및 분석 기능의 제어 센터로서의 입지를 확고히 하고 있습니다. 계약 문서 관리 소프트웨어 시장은 2031년까지 연평균 성장률(CAGR) 14.74%를 기록하며 가장 빠르게 성장할 것으로 전망됩니다. 그 원인 중 하나로, 많은 중규모 병원들이 AI를 활용한 정보 추출 기능을 갖춘 중앙 저장소를 우선시하며, 기존의 폴더나 이메일을 기반으로 한 저장 공간을 검색이 가능한 단일하고 신뢰할 수 있는 정보원으로 통합하려고 하고 있다는 점을 들 수 있습니다. ERP 및 구매 시스템과 연동되는 벤더 및 공급업체 계약 관리 기능은 카탈로그 가격을 적용하고, 계약 외 지출에 플래그를 표시하여 시정 조치를 유도함으로써 비용 유출을 억제하고 부가가치를 높입니다. 규정 준수를 중시하는 솔루션은 BAA(업무 제휴 계약) 관리, 공정 시장 가치 벤치마크에 기반한 의사 보수 점검, 그리고 시스템 차원의 이해 상충 및 선서 진술서 모니터링에 있어 여전히 필수적입니다.

'기타'에는 조건부 규칙을 분석하여 가치 기반 계약에 대한 지급 시뮬레이션을 생성하는 AI 기반 분석 모듈과, 지출 거버넌스를 위한 실시간 대시보드에 정보를 제공하는 조달 통합 플랫폼이 포함됩니다. 생명과학 분야의 활용 사례는 계속해서 확대되고 있으며, 대형 제약사 및 의료기기 제조업체들은 차지백과 리베이트 처리를 대규모로 자동화하여 오류율을 낮췄다고 보고하고 있으며, 이는 신속한 투자 수익률(ROI)로 이어지고 있습니다. Contract Logix 및 기타 전문 기업들은 상세한 내역 관리를 통해, 복잡한 공급 계약 및 리베이트 추적과 관련된 제약 업계의 오랜 업무 흐름을 지원하고 있습니다. DiliTrust의 GxP(의약품 제조 품질 관리 기준)에 중점을 둔 기능과 분석은 유럽 제약 기업 고객사의 사이클 타임과 비용 개선으로 이어지고 있으며, 구조화된 템플릿과 거버넌스가 규제 대상 워크플로우에 어떤 이점을 제공하는지 보여주고 있습니다. 구매자들이 자사의 성숙도나 사업 범위에 맞추어 기능의 심도 있는 수준을 평가함에 따라, 이러한 솔루션 유형들은 전반적으로 헬스케어 계약 관리 소프트웨어 시장을 확대되고 있습니다.

클라우드 기반 도입은 2025년 매출의 50.48%를 차지하며, 연평균 성장률(CAGR) 16.23%로 성장하고 있습니다. 이는 업데이트, 통합 및 보안 기준 준수를 용이하게 하는 SaaS 운영 모델로의 전환을 반영한 것입니다. 팀은 유연한 확장성, 관리형 서비스, 빈번한 기능 릴리스의 이점을 활용하여 분산형 의료 환경에서 계약 체결을 가속화하는 AI 기능 및 전자 서명 워크플로우에 대한 접근성을 확대하는 동시에, 사내 IT 부서의 라이프사이클 부담을 줄일 수 있습니다. 또한, 클라우드를 도입한 조직에서는 법무, 컴플라이언스, 영업 각 팀이 수동 대조 작업 없이 활동을 기록하고 분석 데이터를 추출할 수 있는 공유 시스템을 통해 업무를 처리하기 때문에 부서 간 협업이 가속화되고 있습니다. 이러한 요인들로 인해 헬스케어 계약 관리 소프트웨어 시장은 조정된 워크플로우를 통해 가치 기반 의료(VBC) 및 조달 정책을 운영해야 하는 의료 제공업체와 보험사에 대한 접근성을 확대되고 있습니다.

On-Premise 및 하이브리드 모델은 레거시 시스템을 보유하고 있는 조직, 지역 내 상주 요건이 있는 조직, 또는 대규모 맞춤 설정을 수행하고 있는 조직에게 여전히 중요하며, 이러한 요인들은 마이그레이션 과정을 장기화시킬 가능성이 있습니다. 하이브리드 접근 방식은 대규모 시스템에서 인사, 재무, 공급망 각 모듈을 현장 임상 시스템과 통합함으로써, 계약 및 상업적 거버넌스의 현대화에 따른 업무에 미치는 영향을 완화하는 데 도움이 됩니다. 호스팅 선택과 관계없이, ID 및 액세스 위험을 줄이고, 승인 프로세스를 효율화하며, 감사 추적을 일원화하는 통합 설계도는 도입 과정에서 여전히 핵심적인 역할을 수행하고 있습니다. 예측 기간 동안, 상호 운용성 요구 사항과 분산형 업무 모델로 인해 조직들이 On-Premise 환경의 막대한 오버헤드 없이 표준화를 추구하는 가운데, 헬스케어 계약 관리 소프트웨어 시장에서 ‘클라우드 우선’ 추세가 계속해서 강화될 것으로 예측됩니다.

지역별 분석

북미는 2025년에 45.56%의 점유율을 차지했습니다. 이는 엄격한 개인정보 보호 규제의 시행, EHR(전자건강기록)의 본격적인 도입, 그리고 의무 추적의 필요성을 높이는 가치 기반 모델로의 조기 전환에 힘입은 결과입니다. BAA(업무 제휴 계약) 및 보안 인증에 대한 규제 당국의 강조에 따라, 제공업체 및 지불자(보험사) 전반에 걸쳐 중앙 집중식 저장소, 자동화된 관리, 그리고 상세한 감사 추적이 지속적으로 도입되고 있습니다. 지급자 모델과 연계된 계약 인텔리전스는 미국 내 조직이 청구 및 상환 일정을 지연시키지 않으면서도 복잡한 품질 지표와 지급 구조를 해석하는 데 도움이 됩니다. 또한, 조직은 처리 능력을 향상시키고 종이 문서로 인한 위험과 낭비를 줄이기 위해 전자 서명 및 워크플로우 조정의 효율화에도 주력하고 있으며, 이는 계약 실무의 지속적인 현대화를 뒷받침하고 있습니다. 이러한 요인들로 인해 헬스케어 계약 관리 소프트웨어 시장은 통합 의료 제공 네트워크 및 지역 시스템 전반에 걸친 성과 및 규정 준수 노력의 중심적인 위치를 계속해서 차지하고 있습니다.

유럽에서는 개인정보 보호, 보안, 상호운용성이 우선 과제로 자리 잡고 있으며, 국가 및 기업 차원의 디지털화 추진이 착실히 진행되고 있습니다. 이 지역의 생명과학 및 의료기기 제조업체들은 GxP를 준수하는 관리 체계, 감사 대응 체계, 그리고 표준화된 조항 라이브러리와 거버넌스를 통해 가치를 입증하는 분석 기능을 중시하고 있습니다. 규제 대상 산업을 대상으로 하는 공급업체들은 지역별 요건에 부합하는 다국어 지원 및 개인정보 보호 인증을 제공하며, 이는 국경을 초월한 도입과 일관된 정책 이행을 촉진하고 있습니다. 또한, 조직이 통일된 관리 체제 하에서 공급업체, 연구시설, 파트너와의 계약을 효율화함에 따라 전자 서명 및 통합 워크플로우의 도입도 확대되고 있습니다. 유럽의 바이어들이 보다 광범위한 데이터 거버넌스 프로그램과 병행하여 계약 업무를 조정함에 따라, 이러한 기능들은 헬스케어 계약 관리 소프트웨어 시장을 강화하고 있습니다.

아시아태평양은 의료 시스템이 ‘디지털 퍼스트’ 치료 모델과 분석 및 AI를 위한 데이터 정비를 추구하는 가운데, 2031년까지 연평균 성장률(CAGR) 15.3%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 지역적 파트너십을 통해, 제공업체 네트워크가 AI를 활용한 워크플로우의 공동 설계나 운영 준비를 위한 예측 데이터 관리와 같은 노력을 통해 커넥티드 케어의 목표와 계약을 어떻게 조화시키고 있는지가 명확히 드러납니다. 조직이 표준화된 워크플로를 우선시하고, 수동 라우팅 및 종이 중심 프로세스를 제거함에 따라 전자 서명, 중앙 집중식 저장소 및 즉시 사용 가능한 통합 기능의 도입이 확대되고 있습니다. 의료 서비스 제공업체 및 보험사가 프로그램 참여와 디지털 업무를 확대함에 따라, 다양한 계약을 관리하기 위한 안전한 클라우드 플랫폼, 구조화된 메타데이터, 강력한 분석 기능에 대한 수요가 증가하면서 헬스케어 계약 관리 소프트웨어 시장이 그 혜택을 누리고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the healthcare contract management software market size is expected to increase from USD 1.61 billion in 2025 to USD 1.83 billion in 2026 and reach USD 3.63 billion by 2031, growing at a CAGR of 14.66% over 2026-2031.

This report is Segmented by Solution Type (Contract Lifecycle Management, Document Management, Vendor/Supplier Systems, and, Others), Deployment (Cloud, On-Premises), End-User (Providers, and, Others), Organization Size (Large, Mid-Market, Small), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Value (USD).

Global Healthcare Contract Management Software Market Trends and Insights

Compliance-First Digitalization in Healthcare (HIPAA/GDPR-driven CLM adoption)

Heightened privacy and security oversight keeps pushing organizations to standardize contract governance, with HIPAA requirements elevating the need for executed Business Associate Agreements across cloud providers, EHR vendors, billing services, and other partners to reduce breach exposure.As audit and incident reporting expectations increase, hospitals and payers are phasing out folders, shared drives, and email-driven authoring in favor of centralized repositories with role-based access and immutable audit trails that document every action on sensitive records. Automated compliance checks and renewal alerts help teams surface missing BAAs and outdated clauses before they turn into penalties, which preserves time for higher-value negotiations and reduces the probability of non-compliance during reviews. The same governance pressures apply in other regulated jurisdictions that enforce strict privacy and security standards, which reinforces the case for automated clause libraries, approvals, and evidence capture across the healthcare contract management software market. As system access, identity management, and segregation of duties policies mature, organizations align legal, compliance, procurement, and IT to maintain a single version of truth for contracts and associated obligations, reducing manual handoffs and hidden risk.

Cloud-First Rollouts and Subscription Pricing Ease Deployment & ROI

SaaS platforms remove the need for dedicated hardware, database administration, and disaster recovery buildouts, which helps lean IT teams stand up enterprise-grade CLM with predictable operating spend and faster time to value. Subscription pricing and simplified UX lower barriers for ambulatory clinics and behavioral health organizations, while scalable tenancy and continuous updates keep security baselines current without lengthy patch cycles. Healthcare teams also benefit from integrated eSignature, workflow routing, and identity services that connect common productivity suites and line-of-business systems to keep negotiations moving and documentation complete. As decision-makers weigh alternatives, they see that cloud CLM accelerates approvals, enables remote collaboration, and surfaces analytics on cycle times and bottlenecks that were difficult to quantify with on-premises silos. These fundamentals support broader adoption of the healthcare contract management software market among mid-market and small enterprises seeking lower-risk modernization paths.

Legacy IT Integration, Data Migration, and Security Hurdles

Heterogeneous estates that include multiple EHRs, ERPs, and custom revenue-cycle systems complicate data mapping and interface design, which can extend rollouts and create parallel-process burdens during migration. Teams must normalize legacy fields, clean archival repositories, and validate clause metadata to ensure downstream analytics are reliable and auditable at scale. Security certifications such as HITRUST and SOC 2 Type II are often table stakes in healthcare procurement and can disqualify vendors or delay approvals if evidence and controls are not current. Implementation timelines may stretch for organizations with heavy customizations or sovereign data needs, which can slow near-term ROI as staff balance transformation with daily operations. These realities remain a headwind for the healthcare contract management software market when buyers underestimate the effort required to centralize scattered documents and align integrations with clinical, financial, and supply workflows.

Other drivers and restraints analyzed in the detailed report include:

- Operational Efficiency and Cost Containment Imperatives in Providers & Payers

- AI-Enabled Contract Analytics, Obligation Tracking, and Risk Scoring

- High Implementation/Customization Costs and Change Management Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contract Lifecycle Management Software held 47.66% in 2025, reflecting demand for end-to-end authoring, negotiation, execution, and obligation management across diverse healthcare agreements. The category's breadth positions it as the control center for templates, clause libraries, and analytics that legal and commercial teams use to scale consistent governance across providers, payers, and suppliers within the healthcare contract management software market. Contract Document Management Software is projected to grow the fastest at 14.74% CAGR to 2031, in part because many mid-market hospitals prioritize central repositories with AI-powered extraction to consolidate legacy folders and email-based storage into a searchable single source of truth. Vendor and supplier contract management capabilities that connect to ERP and purchasing systems increase value by enforcing catalog pricing and flagging off-contract spend for corrective action that curbs leakage. Compliance-oriented solutions remain essential for BAA management, physician compensation checks against fair-market-value benchmarks, and monitoring of conflicts and attestations at the system level.

"Others" includes AI-driven analytics modules that parse conditional rules and produce payout simulations for value-based arrangements as well as procurement-integrated platforms that feed real-time dashboards for spend governance. Life sciences use cases continue to grow, with large pharma and device companies automating chargebacks and rebates at scale and reporting error-rate reductions that translate into rapid ROI. Contract Logix and other specialists support long-standing pharmaceutical workflows for complex supply agreements and rebate tracking through granular line-item management. DiliTrust's GxP-focused features and analytics have been associated with cycle-time and cost improvements for European pharma clients, showing how regulated workflows benefit from structured templates and governance. These solution types collectively expand the healthcare contract management software market as buyers match capability depth to their maturity and scope.

Cloud-based deployments accounted for 50.48% of 2025 revenues and are growing at a 16.23% CAGR, which reflects a shift to SaaS operating models that ease updates, integration, and security baselines. Teams benefit from elastic scale, managed services, and frequent feature releases that reduce the lifecycle burden on internal IT while expanding access to AI features and eSignature workflows that accelerate contracting in distributed care settings. Cloud adopters also see faster cross-functional collaboration because legal, compliance, and commercial teams route work from a shared system that logs activity and extracts analytics without manual reconciliation. These factors help the healthcare contract management software market broaden reach among providers and payers that need to operationalize VBC and procurement policies through orchestrated workflows.

On-premises and hybrid models remain relevant for organizations with legacy estates, local residency mandates, or extensive customizations, which can extend migration paths. Hybrid approaches help large systems harmonize HR, finance, and supply chain modules with on-site clinical systems to reduce disruption as they modernize contracting and commercial governance. Integration blueprints that reduce identity and access risks, streamline approvals, and centralize audit artifacts remain central to adoption, regardless of hosting choice. Over the forecast period, interoperability requirements and distributed work models are expected to keep cloud-first momentum strong within the healthcare contract management software market as organizations pursue standardization without heavy on-premises overheads.

Geography Analysis

North America commanded 45.56% in 2025, supported by stringent privacy enforcement, mature EHR adoption, and early movement into value-based models that increase obligation tracking needs. Regulatory emphasis on BAAs and security certifications sustains adoption of centralized repositories, automated controls, and rich audit trails across providers and payers. Contract intelligence tied to payer models helps U.S. organizations interpret complex quality measures and payment structures without slowing claims or reimbursement timelines. Organizations also focus on streamlined eSignature and workflow orchestration to improve throughput and reduce paper-based risk and waste, which supports continued modernization of contracting practices. These factors keep the healthcare contract management software market central to performance and compliance initiatives across integrated delivery networks and regional systems.

Europe shows steady momentum as privacy, security, and interoperability priorities continue to advance digitization agendas at national and enterprise levels. Life sciences and device manufacturers in the region emphasize GxP-aligned controls, audit readiness, and analytics that demonstrate value from standardized clause libraries and governance. Vendors serving regulated industries offer multi-language support and privacy certifications that fit regional requirements, which encourages cross-border deployments and consistent policy execution. eSignature and integrated workflow adoption also expands as organizations streamline agreements with suppliers, research sites, and partners under unified controls. These capabilities strengthen the healthcare contract management software market as European buyers coordinate contracting alongside broader data governance programs.

Asia-Pacific is projected to be the fastest-growing region at 15.3% CAGR through 2031 as health systems pursue digital-first care models and data readiness for analytics and AI. Regional partnerships highlight how provider networks align contracting with connected-care objectives, such as initiatives to co-design AI-enabled workflows and predictive data management for operational readiness. Adoption of eSignature, centralized repositories, and out-of-the-box integrations grows as organizations eliminate manual routing and paper-heavy processes in favor of standardized workflows. As providers and payers scale program participation and digital operations, the healthcare contract management software market gains from demand for secure cloud platforms, structured metadata, and strong analytics to govern diverse agreements.

- Agiloft

- CobbleStone Software

- Compliatric

- Contract Logix

- ContractWorks

- Corcentric

- Coupa CLM

- DocuSign CLM

- FinThrive

- GHX

- Icertis

- Infor

- Infosys Helix

- Ironclad

- Ivalua

- JAGGAER

- Ntracts

- Oracle

- Premier

- SAP Ariba

- SirionLabs

- symplr

- Vizient

- Workday

- Zycus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Compliance-First Digitalization in Healthcare (HIPAA/GDPR-driven CLM adoption)

- 4.2.2 Cloud-First Rollouts and Subscription Pricing Ease Deployment & ROI

- 4.2.3 Operational Efficiency and Cost Containment Imperatives in Providers & Payers

- 4.2.4 AI-Enabled Contract Analytics, Obligation Tracking, and Risk Scoring

- 4.2.5 Value-Based Care and Payer-Provider Contracting Complexity

- 4.2.6 Procurement-EHR/ERP Integration Linking Contract Terms to Spend & Reimbursement

- 4.3 Market Restraints

- 4.3.1 Legacy IT integration, Data Migration, and Security Hurdles

- 4.3.2 High Implementation/Customization Costs and Change Management Gaps

- 4.3.3 Fragmented Ownership Across Legal, Supply Chain, and Compliance Slows Governance

- 4.3.4 Overlap with Revenue-Cycle/Payer Contract Modeling Tools Creates Substitution

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Solution Type

- 5.1.1 Contract Lifecycle Management Software

- 5.1.2 Contract Document Management Software

- 5.1.3 Vendor & Supplier Contract Management Systems

- 5.1.4 Compliance & Regulatory Contract Management Systems

- 5.1.5 Others

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By End-User

- 5.3.1 Healthcare Providers

- 5.3.2 Healthcare Payers

- 5.3.3 Pharmaceuticals & Medical Devices

- 5.3.4 Others

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Mid-market Enterprises

- 5.4.3 Small Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Agiloft

- 6.3.2 CobbleStone Software

- 6.3.3 Compliatric

- 6.3.4 Contract Logix

- 6.3.5 ContractWorks

- 6.3.6 Corcentric

- 6.3.7 Coupa CLM

- 6.3.8 DocuSign CLM

- 6.3.9 FinThrive

- 6.3.10 GHX

- 6.3.11 Icertis

- 6.3.12 Infor

- 6.3.13 Infosys Helix

- 6.3.14 Ironclad

- 6.3.15 Ivalua

- 6.3.16 JAGGAER

- 6.3.17 Ntracts

- 6.3.18 Oracle

- 6.3.19 Premier Inc.

- 6.3.20 SAP Ariba

- 6.3.21 SirionLabs

- 6.3.22 symplr

- 6.3.23 Vizient

- 6.3.24 Workday

- 6.3.25 Zycus

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment