|

시장보고서

상품코드

2063506

심장 냉동 절제 장치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cardiac Cryoablation Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

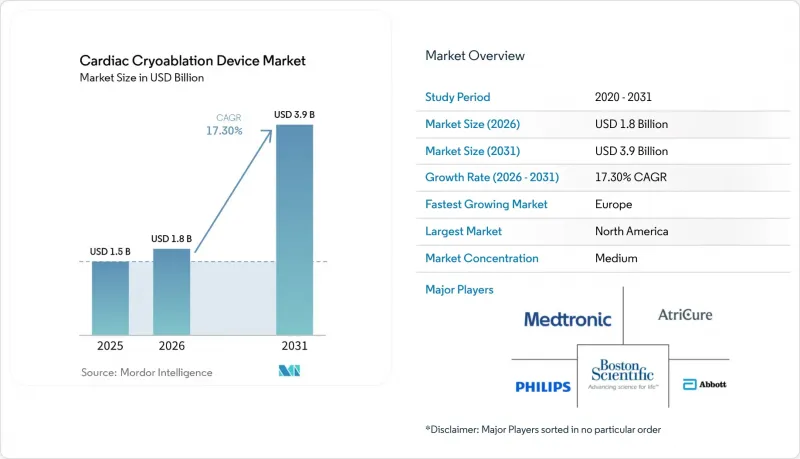

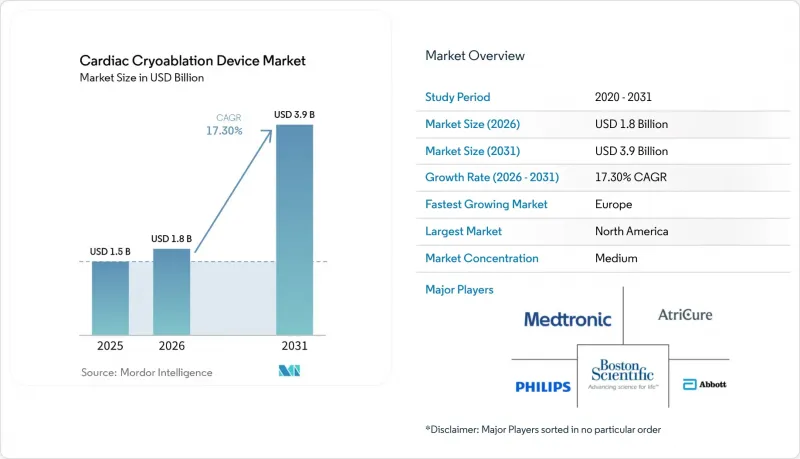

Mordor Intelligence에 의하면, 심장 냉동 절제 장치 시장 규모는 2025년에 15억 달러, 2026년에 18억 달러, 2031년까지 39억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 17.30%로 성장할 것으로 전망됩니다.

본 보고서는 기술별(N2O 기반 크라이오 풍선, 초점 크라이오 카테터, 외과용 크라이오 등), 제품별(카테터/풍선, 콘솔, 시스 등), 적응증별(발작성 심방세동, 지속성 심방세동, 상심실성 빈맥, 심실성 빈맥), 최종 사용자(3차 의료기관, 지역 병원, 외래수술센터(ASC)), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

전 세계 심장 냉동 절제 장치 시장 동향 및 인사이트

미국 내 ASC의 적용 범위와 외래 치료로의 전환

2025년 11월 CMS 최종 규정에 따라, 종합적인 심방세동 절제술 코드인 CPT 93656이 ASC 목록에 추가되었으며, 기관 지급액이 2만 4,532달러로 책정되었습니다. 이는 입원 환자 대상 요금을 상회하여 외래 환자 수의 급증으로 이어지고 있습니다. 크라이오발룬 수술의 평균 소요 시간은 122분인 반면, 고주파(RF) 수술은 160분으로, 이를 통해 초과 근무 시간이 줄어들어 ASC의 처리 능력 모델에 부합합니다. 2026년 초의 예약 데이터에 따르면, ASC에서는 시설당 하루 2건의 크라이오어블레이션 시술이 추가로 예약되어 있으며, ASC의 매출은 연평균 성장률(CAGR) 17.88%로 증가할 것으로 예측됩니다. 캐나다의 각 주와 서유럽의 여러 보험사들도 이와 유사한 당일 AF 치료 절차를 시범적으로 도입하고 있어, 북미의 성공 모델이 다른 지역으로 확산될 가능성을 시사하고 있습니다.

1차 선택적 절제술의 근거와 조기 개입

FDA가 Arctic Front Advance 풍선을 1차 치료법으로 승인하고, STOP-AF First 및 EARLY-AF 임상시험에서 75-82%의 부정맥 없는 생존율을 확인함에 따라, 절제술은 구제적 치료에서 초기 치료로 전환되었습니다. 젊은 연령층에서 구조적으로 건강한 심방에서는 1회 시술로 내구성이 향상되어 비용이 많이 드는 재시술을 줄이고, 수요를 앞당기고 있습니다. 2024년 독일의 비용-효용 모델에 따르면, 증분 비용-효용 비율이 QALY당 1,037유로로 산출되었으며, 이는 지역의 지불 의향액 기준치를 크게 하회하여 치료 경로의 초기 단계에서 시행되는 절제술에 대한 지불 주체의 수용성을 뒷받침하고 있습니다.

심방세동 절제술에서 PFA 대체 요법의 위험성

2025년 1월 『NEJM』지에 게재된 SINGLE SHOT CHAMPION 임상시험에서는 PFA의 재발률이 37.1%인 반면, 냉동 요법의 재발률은 50.7%로 보고되었으며, 장치 비용이 23% 더 비싸음에도 불구하고, 병원들은 PFA 콘솔 도입을 서둘러 진행하고 있습니다. 미국의 의사 설문조사에 따르면, 2026년에는 심방세동 절제술의 68%에서 PFA가 채택될 것으로 예상되며, 냉동 치료 장치 공급업체들이 시장 점유율을 지키기 위한 유예 기간은 점점 줄어들고 있습니다. 유럽에서도 유사한 추세가 나타나고 있으며, CE 마크를 획득한 PFA 카테터는 1만 7,000건 이상의 실제 임상 사례에서 식도 손상이 전혀 발생하지 않았음을 보여주고 있어, 냉동 요법과의 의료법적 대비가 뚜렷해지고 있습니다.

부문별 분석

2025년, 심장 냉동 절제 장치 시장 점유율의 55.30%를 아산화질소 냉동 풍선 시스템이 차지했습니다. 이는 재현성이 높은 원샷 폐정맥 격리를 가능하게 하는 메드트로닉사가 10년 전에 출시한 콘솔 기반 시스템이 주도하고 있습니다. 외래수술센터(ASC)가 발작성 심방세동(AF) 치료 워크플로우를 위해 콘솔을 도입함에 따라, 냉동 풍선 기술을 활용한 심장 냉동 절제 장치 시장은 꾸준히 성장할 것으로 예측됩니다. 심실빈맥(VT) 치료용 초저온 크라이오(작동 온도 -196°C) 시장은 17.95%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되며, 이는 충분한 치료를 받지 못하고 있는 구조적 심장 질환 환자층을 대상으로 새로운 수익원을 개척하게 될 것입니다.

각 콘솔 제조업체들은 PFA(폐동맥 폐쇄) 시장에서의 경쟁을 막기 위해 기능 확장 소프트웨어와 통합 매핑 기능을 순차적으로 추가하고 있습니다. 중국의 액체 질소 풍선은 병원의 ‘그린 수술실’ 위원회로부터 공감을 불러일으키는 지속가능성 브랜딩을 선보이고 있습니다. 포컬 냉동 카테터는 상심실성 빈맥 치료에 있어 틈새 시장에서 유용성을 유지하고 있지만, 판매량이 적은 데다 RF(고주파) 기술의 접촉력 관련 발전까지 더해지면서 성장 여지는 제한적입니다. 외과적 냉동 요법은 여전히 지침에서 권장되고 있지만, 보급률은 낮은 편이며, 수술실 업무 흐름의 관성이나 대동맥 클램프로 인한 시간 손실 등의 요인으로 인해 보급이 저해되고 있습니다.

카테터와 풍선은 2025년 매출의 62.18%를 차지하고 있으며, 시술 건수 증가가 소모품 수요 증가와 직결되기 때문에 연평균 성장률(CAGR) 17.86%를 기록하며 콘솔을 계속해서 앞지를 것으로 전망됩니다. POLARx FIT와 같은 확장형 풍선은 장치 교체 횟수를 줄여 경제적 및 인체공학적 가치를 높여줍니다. 콘솔 판매와 연계된 심장 냉동 절제 장치 시장 규모는 ASC(외래수술센터(ASC))로의 전환에 따라 확대될 전망이지만, 다중 에너지 플랫폼을 둘러싼 불확실성으로 인해 설비 투자 예산은 여전히 민감한 상황에 놓여 있습니다. 동봉된 시스나 매핑 카테터는 단일 상환 코드로 통합되는 경향이 강해지고 있어, 개별 가격 책정이 압박을 받는 한편, 벤더 종속 현상은 더욱 공고해지고 있습니다.

일회용 스캐빈징 호스, 압력 라인, 멸균 슬리브는 예측 가능하지만 마진이 낮은 수익을 창출하고 있습니다. 아산화질소 배출에 대한 환경적 감시가 액세서리의 추가적인 재설계를 촉진할 가능성이 있습니다. 동결 데이터 피드를 외부 3D 매핑 시스템과 연동하는 통합 플랫폼은 전기생리학자의 인지적 부담을 줄여줄 뿐만 아니라, 향후 제품 로드맵을 형성할 가능성이 높습니다.

지역별 분석

북미는 CMS의 외래 진료 관련 결정과 메드트로닉의 확립된 콘솔 제품군에 힘입어 2025년 매출의 46.17%를 차지했습니다. 미국의 검사실에서는 반나절 단위로 예측 가능한 냉동 치료 소요 시간을 바탕으로, ASC(외래수술센터(ASC))로의 전환이 빠르게 진행되고 있습니다. 캐나다에서의 보급은 주별 예산 차이로 인해 제약을 받고 있습니다. 온타리오주와 퀘벡주의 전문센터에서는 활기를 띠고 있지만, 전국적인 통일성은 부족합니다. 멕시코는 민간 보험사의 지배적 지위와 제한된 전기생리학 인프라로 인해 뒤처져 있습니다.

유럽은 연평균 성장률(CAGR) 17.76%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. POLARx FIT의 조기 CE 마크 획득과 독일 및 영국에서 나온 비용 대비 효과에 대한 긍정적인 데이터 덕분에, PFA가 시장에 진입하는 상황에서도 냉동 요법의 경쟁력은 유지되고 있습니다. 독일의 워크플로우 모델링을 통해 구체적인 인력 배치의 효율성이 입증된 반면, 영국의 국민보건서비스(NHS)에서는 높은 장치 비용과 낮은 재절제율을 저울질하며 검토하고 있습니다. 남유럽 시장은 지역 심장 네트워크 프로그램을 바탕으로 성장하고 있지만, 상환 제도의 불균일성이 성장 속도를 둔화시키고 있습니다.

아시아태평양은 상황이 제각각입니다. 일본에서는 발작성 및 지속성 심방세동의 두 적응증에 대해 PMDA의 승인을 획득했으며, 이는 개선된 버전의 풍선을 전 세계적으로 출시하기 위한 발판이 되고 있습니다. 중국에서는 새로 승인된 액체 질소 시스템이 가격 및 환경 측면에서 경쟁을 불러일으키며, 2선 도시에서의 이용 확대로 이어지고 있습니다. 호주와 한국에서는 3차 의료기관에서 수요가 견조하지만, ASC(외래수술센터(ASC))의 인프라는 아직 발전 단계에 있습니다. 인도 및 동남아시아의 많은 지역에서는 본인 부담 모델로 인한 제약이 여전히 남아 있어, 보급은 도시 지역의 지정 의료기관으로 한정되어 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the cardiac cryoablation device market size is projected to be USD 1.5 billion in 2025, USD 1.8 billion in 2026, and reach USD 3.9 billion by 2031, growing at a CAGR of 17.30% from 2026 to 2031.

This report is Segmented by Technology (Cryoballoon N2O-Based, Focal Cryo Catheters, Surgical Cryo, and More), Product (Catheters/Balloons, Consoles, Sheaths, and More), Indication (Paroxysmal AF, Persistent AF, SVT, VT), End User (Tertiary Hospitals, Community Hospitals, ASC), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

Global Cardiac Cryoablation Device Market Trends and Insights

ASC Coverage and Outpatient Shift in the United States

The November 2025 CMS final rule moved comprehensive AF ablation code CPT 93656 onto the ASC list with a USD 24,532 facility payment, eclipsing the inpatient tariff and catalyzing an outpatient surge. Cryoballoon procedures average 122 minutes, compared with 160 minutes for radiofrequency (RF), reducing overtime and aligning with ASC throughput models . Early 2026 scheduling data show ASCs booking two additional cryo cases per lab per day, expanding ASC revenue at a projected 17.88% CAGR. Canadian provinces and several Western European payers are piloting similar day-case AF pathways, hinting at an export of a North American playbook.

First-Line Ablation Evidence and Earlier Intervention

FDA first-line clearance for the Arctic Front Advance balloon, together with STOP-AF First and EARLY-AF results showing 75-82% arrhythmia-free survival, shifted ablation from salvage to upfront care . Younger, structurally intact atria yield higher single-procedure durability, trimming costly repeat interventions and pulling forward demand. A 2024 German cost-utility model pegged incremental cost-effectiveness at EUR 1,037 per QALY, well below regional willingness-to-pay thresholds, reinforcing payers' openness to ablation early in the pathway.

PFA Substitution Risk for AF Ablation

The January 2025 NEJM SINGLE SHOT CHAMPION trial reported 37.1% recurrence for PFA versus 50.7% for cryo, propelling hospitals to fast-track PFA console buying even at 23% higher device cost . U.S. physician surveys indicate PFA penetration climbing toward 68% of AF ablations in 2026, tightening the window for cryo vendors to defend share. Europe mirrors the trend as CE-cleared PFA catheters demonstrate zero esophageal injury in 17,000-plus real-world cases, sharpening medico-legal contrast with cryo.

Other drivers and restraints analyzed in the detailed report include:

- New Cryo System Approvals and Installed Base Expansion

- Workflow Efficiency and Reproducibility of Single-Shot Cryo

- Safety Events (Esophageal Injury, Phrenic Nerve Palsy) and IFU Updates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, nitrous oxide cryoballoon systems accounted for 55.30% of the cardiac cryoablation device market share, anchored by Medtronic's decade-old console-based system that enables reproducible single-shot pulmonary vein isolation. The cardiac cryoablation device market for cryoballoon technology is expected to grow steadily as ASCs acquire consoles for paroxysmal AF workflows. Ultra-low-temperature cryo for VT, operating at -196 °C, is projected to log the fastest 17.95% CAGR, opening a new revenue lane for underserved structural heart disease populations.

Console makers are layering incremental software and integrated mapping to hold off PFA cannibalization. Chinese liquid-nitrogen balloons bring sustainability branding that resonates with hospital "green OR" committees. Focal cryo catheters retain niche utility for supraventricular tachycardia, yet their modest volume, coupled with RF's contact-force advances, limits upside. Surgical cryo remains guideline-endorsed but under-penetrated, held back by operating-room workflow inertia and cross-clamp penalties.

Catheters and balloons accounted for 62.18% of 2025 revenue and will continue to outpace consoles at a 17.86% CAGR, as procedure growth directly scales consumable pull-through. Expandable balloons such as POLARx FIT reduce device exchanges, adding economic and ergonomic value. The cardiac cryoablation device market size attached to console sales will rise in tandem with ASC migration, though capital budgets remain sensitive to uncertainty around multi-energy platforms. Ancillary sheaths and mapping catheters are increasingly bundled into single reimbursement codes, compressing stand-alone pricing but cementing vendor lock-in.

Disposable scavenging hoses, pressure lines, and sterile sleeves generate predictable but low-margin revenue; environmental scrutiny of nitrous oxide exhaust may spur additional redesigns of accessories. Integrated platforms that align cryo data feeds with external 3-D mapping systems lower cognitive load for electrophysiologists and are likely to shape future product roadmaps.

Geography Analysis

North America delivered 46.17% of 2025 revenue, buoyed by CMS's outpatient ruling and Medtronic's entrenched console fleet. U.S. labs are fast-tracking ASC conversions, aided by predictable cryo timings that fit half-day blocks. Canadian adoption is constrained by provincial budgetary variances; specialist centers in Ontario and Quebec show momentum, yet cross-country uniformity is absent. Mexico lags due to private-payer dominance and limited EP infrastructure.

Europe is the fastest-growing region at a 17.76% CAGR. Early CE-mark access to POLARx FIT and supportive cost-effectiveness data from Germany and the U.K. have kept cryo competitive even as PFA enters. Germany's workflow modeling demonstrates tangible staffing efficiencies, while the U.K.'s National Health Service weighs higher device cost against lower re-ablation rates. Southern European markets expand on the back of regional cardiac network programs, although reimbursement heterogeneity tempers the pace.

Asia-Pacific presents a mixed landscape. Japan, with PMDA approvals for both paroxysmal and persistent AF indications, serves as a global launch pad for incremental balloon refinements. China's newly approved liquid-nitrogen systems inject price and eco-credential competition, widening access in tier-2 cities. Australia and South Korea display steady tertiary-hospital demand, but ASC infrastructure is nascent. India and much of Southeast Asia remain constrained by cash-pay models, limiting penetration to urban referral centers.

- Abbott Laboratories

- Adagio Medical

- APT Medical

- AtriCure

- Biosense Webster

- Boston Scientific

- Cryofocus Medtech

- Hejeya (Beijing) Medical Device

- Japan Lifeline

- Koninklijke Philips

- Medtronic

- MicroPort EP

- Shanghai Antec Medical Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ASC Coverage, Outpatient Shift In The US

- 4.2.2 First-Line Ablation Evidence and Earlier Intervention

- 4.2.3 New Cryo System Approvals and Installed Base Expansion

- 4.2.4 Workflow Efficiency and Reproducibility of Single-Shot Cryo

- 4.2.5 VT Opportunity From Ultra-Low-Temperature Cryo

- 4.2.6 China/Local Entrants Accelerate Access and Price Competition

- 4.3 Market Restraints

- 4.3.1 PFA Substitution Risk for AF Ablation

- 4.3.2 Safety Events (Esophageal Injury, PNP) And IFU Updates

- 4.3.3 FDA Post-Approval Evidence Requirements for New Systems

- 4.3.4 Underutilization Of Surgical Ablation Despite Guidelines

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Cryoballoon ablation (N2O-based)

- 5.1.2 Focal cryoablation catheters

- 5.1.3 Surgical cryoablation (probes/clamps; N2O/Argon)

- 5.1.4 Ultra-low-temperature cryo for VT (emerging)

- 5.2 By Product

- 5.2.1 Cryoablation catheters/balloons

- 5.2.2 Cryo consoles/generators

- 5.2.3 Steerable sheaths/introducers

- 5.2.4 Inner-lumen circular mapping catheters (cryo workflows)

- 5.2.5 Ancillary disposables

- 5.3 By Indication

- 5.3.1 Paroxysmal atrial fibrillation (PVI)

- 5.3.2 Persistent atrial fibrillation (PVI-centric)

- 5.3.3 SVT/AVNRT (focal cryo)

- 5.3.4 Ventricular tachycardia (ULTC)

- 5.4 By End User

- 5.4.1 Tertiary/academic hospitals & EP labs

- 5.4.2 Community hospitals

- 5.4.3 Ambulatory surgery centers (ASC)

- 5.4.4 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 Adagio Medical

- 6.3.3 APT Medical

- 6.3.4 AtriCure, Inc.

- 6.3.5 Biosense Webster

- 6.3.6 Boston Scientific Corporation

- 6.3.7 Cryofocus Medtech

- 6.3.8 Hejeya (Beijing) Medical Device

- 6.3.9 Japan Lifeline

- 6.3.10 Koninklijke Philips N.V.

- 6.3.11 Medtronic Plc

- 6.3.12 MicroPort EP

- 6.3.13 Shanghai Antec Medical Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment