|

시장보고서

상품코드

2063513

형광증백제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Optical Brighteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

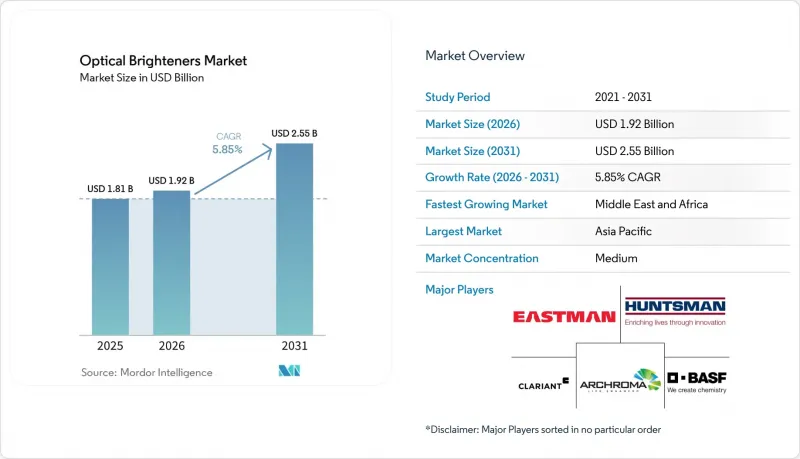

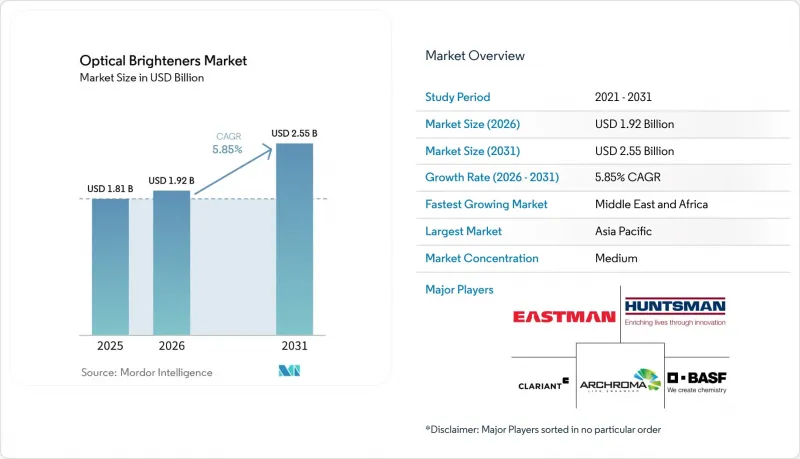

Mordor Intelligence에 의하면, 형광증백제 시장 규모는 2025년 18억 1,000만 달러, 2026년 19억 2,000만 달러에서 2031년까지 25억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.85%를 나타낼 것으로 예측됩니다.

본 보고서는 화학물질의 유형(트리아진·스틸벤 계열, 쿠마린 계열 등), 용도(섬유용 형광증백제, 세제용 형광증백제 등), 최종 사용자 산업(섬유 및 의류, 소비재, 포장, 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 형광증백제 시장 동향 및 인사이트

세탁용 세제 시장에서 형광증백제 수요 증가

현재 액체 세제는 전 세계 가정용 세탁 시장 매출의 절반 이상을 차지하고 있으며, 소형 농축 세제로의 전환 추세에 따라 세탁 1회당 형광증백제 사용량이 증가하고 있습니다. 제형 제조업체는 일반적으로 부피 비율로 0.1-0.5%를 첨가하고 있지만, 저온 세탁이나 인산염이 함유되지 않은 빌더를 사용할 경우 형광 효과를 유지하기 위해서는 CBS-X와 같은 고순도의 트리아진·스틸벤계 형광증백제가 필요합니다. 가정용 세정 제품 분야의 4대 다국적 기업이 세제 매출의 약 60%를 독점하고 있으며, 이러한 과점적 구매력은 형광증백제 공급업체로 하여금 이익률을 훼손하지 않으면서도 엄격한 생분해성 기준을 충족하도록 강요하고 있습니다. 노보네시스사는 2024년, 액체와 분말 모두에 사용할 수 있는 크로스 매트릭스형 형광증백제 ‘Luminous’를 출시하며, 다국적 브랜드의 SKU(재고 관리 단위) 감축을 목표로 한 새로운 연구개발 노력을 선보였습니다. 또한, 유럽과 미국의 소매업체들이 운영하는 프리미엄 자체 브랜드 역시 시장을 선도하는 브랜드의 미학에 부합하기 위해 형광증백제를 채택하고 있으며, 이로 인해 형광증백제 시장의 견고한 판매 기반이 확립되었습니다.

아시아·태평양 지역의 섬유 및 의류 제조업 확대

베트남, 인도, 방글라데시의 지역 밸류체인에서는 방적보다 후가공 공정의 생산 능력이 급속히 확대되고 있으며, 형광증백제 소비는 다운스트림 공정인 염색·세탁 시설로 이동하고 있습니다. 베트남의 탄소중립 로드맵이나 인도의 기능성 섬유 생산 연계 인센티브(PLI)와 같은 정부 프로그램을 통해, 재활용 섬유 가공 과정에서 손실된 백색도를 회복하기 위해 여전히 형광증백제에 의존하고 있는 절수형 염색 라인에 대한 투자가 촉진되고 있습니다. 이집트 소크나 산업단지에서는 2026년부터 1만 5,000톤의 원단 생산이 추가될 예정이며, 중동 수요가 더욱 확대될 전망입니다. 이러한 클러스터 인근에 기술 서비스 연구소를 설립하는 공급업체는 색상 매칭이나 공정상의 문제 해결이 여전히 관계 기반에 의존하고 있기 때문에 형광증백제 시장에서 확고한 시장 점유율을 확보할 수 있습니다.

스틸벤의 독성 및 잔류성에 관한 전 세계의 엄격한 규제

유럽연합 집행위원회는 2025년, 규정(EU) 2019/1021의 부속서 I에 UV-328을 추가하고, 2029년까지 1mg/kg으로 단계적으로 낮춰지는 미량 함유 기준을 도입했습니다. 중국 환경보호부령 제12호는 2026년까지 성분 공개를 의무화하고 있어, 기존 제품에 대한 지적재산권 보호를 약화시키고 있습니다. 중국 및 대만산 스틸벤에 대한 반덤핑 관세를 유지하기로 한 미국의 결정은 공급망 지연을 초래하고, 입고 비용을 상승시키고 있습니다. 이러한 조치들은 종합적이고 종합적인 불순물 프로파일링 및 수명 주기에 관한 자료 제출을 요구하고 있으며, 중소기업에게는 큰 비용 부담이 되기 때문에 본래라면 건전한 성장이 예상되던 형광증백제 시장의 성장을 둔화시키고 있습니다.

부문별 분석

트리아진계 스틸벤은 폭넓은 배합과의 호환성과 높은 형광 양자 수율을 강점으로 삼아, 2025년 형광증백제 시장 점유율의 58.15%를 차지했습니다. 세제용 등급의 CBS-X는 백색 지수 130 이상을 달성할 수 있으며, pH 7-11 범위에서 안정성을 유지하기 때문에 판매량 측면에서 선도적인 위치를 차지하고 있습니다. 쿠마린 계열은 화장품 및 저융점 포장용 코팅 분야에서 낮은 가공 온도 임계값 덕분에 배합 업체들로부터 선호받고 있어, 2031년까지 연평균 성장률(CAGR) 6.61%로 성장할 것으로 전망됩니다. 이 두 가지 주요 그룹 외에도, OB-1 등의 벤조옥사졸린 계열은 280℃ 이상의 열안정성이 필수적인 재활용 플라스틱 컴파운드 용도로 사용되며, 확고한 틈새 시장을 유지하고 있습니다.

이미다졸린, 디아졸, 피라졸린 등 제2그룹에 속하는 화학 물질은 특수 섬유 마감, 특히 내염소성 스포츠웨어 분야에서 전반적으로 확고한 입지를 유지하고 있습니다. 장시성에서 진행된 시범 규모의 마이크로 리액터 프로젝트에서는 피라졸린 중간체의 수율이 96%에 달했으며, 이는 스틸벤계 화합물과의 비용 경쟁력 측면에서 기술적 여지가 있음을 시사하고 있습니다. 배출 규제가 강화되는 가운데, 기존 공장을 연속 유동 시스템으로 개조할 수 있는 공급업체는 저탄소 제품 라인을 판매함으로써 형광증백제 시장에서의 점유율을 더욱 확대할 가능성이 있습니다.

지역별 분석

2025년 전 세계 형광증백제 시장 매출액 중 아시아태평양이 58.76%를 차지했습니다. 이는 중국의 연간 소비량이 11만 6,000톤에 달하고, 세제의 프리미엄화가 지속되고 있기 때문입니다. ‘이산화탄소 배출량 정점 도달 및 탄소 중립’ 목표와 더욱 엄격해진 폐수 규제의 영향으로 장쑤성과 절강성에서 생산 능력을 합리화함에 따라, 이미 저가대 생산량의 약 12%가 중단되었으며, 이에 따라 지역 수급 균형이 타이트해지고 있습니다. 인도에서는 Rossari Biotech의 연간 2만 2,100톤 증산 계획이 진행 중이며, 2026년부터는 공급량이 증가할 전망이지만, 그 대부분은 현지 섬유 산업 거점에 배정되어 있습니다. 아세안 의류 부문, 특히 베트남에서는 고도의 후가공에 대한 투자가 진행되고 있으며, 이로 인해 1미터당 형광증백제 수요가 증가하고 있습니다.

유럽과 북미는 형광증백제 시장에서 점유율은 작지만, 규제 측면에서의 영향력은 매우 큽니다. 2030년까지 지속될 미국의 반덤핑 관세로 인해, 국내 생산과 다각화된 공급망을 우대하는 이중 가격 체계가 정착되고 있습니다. EU에서는 UV-328에 대한 부속서 I의 잔류성 유기 오염 물질(POP) 규제 및 임박한 퍼플루오로알킬 물질(PFAS) 관련 법규로 인해, 가공업체들은 저이동성 스틸벤 대체재의 사전 인증을 추진하고 있으며, 이는 견고한 분석 연구소를 보유한 생산자들에게 선점 우위를 제공합니다.

중동 및 아프리카은 2031년까지 연평균 성장률(CAGR) 6.87%를 기록하며 가장 높은 성장률을 보일 것으로 전망됩니다. 이는 사우디아라비아의 ‘비전 2030’에 기반한 섬유 프로젝트와 이집트 소크나 지역이 주도하고 있습니다. 성장의 기반이 되는 소규모의, 온화한 기후에 적합한 액체형 세제를 채택하는 지역 내 세제 공장이 늘어나면서 그 성장은 더욱 가속화되고 있습니다. 남미 수요를 뒷받침하는 것은 브라질이며, 솔베이사가 산토 안드레 공장에 2,000만 달러를 투자해 추진하는 현대화 프로젝트는 특수 폴리아미드 마감재 수요를 확보하기 위한 것으로, 간접적으로 해당 지역의 형광증백제 시장 수요를 촉진하게 될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the optical brighteners market size is projected to expand from USD 1.81 billion in 2025 and USD 1.92 billion in 2026 to USD 2.55 billion by 2031, registering a CAGR of 5.85% between 2026 to 2031.

This report is Segmented by Chemical Type (Triazine-Stilbenes, Coumarins, and More), Application (Textile Whitening, Detergent Brightener, and More), End-User Industry (Textile and Apparel, Consumer Products, Packaging, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Optical Brighteners Market Trends and Insights

Rising Demand for Optical Brighteners in Laundry Detergents

Liquid detergents now generate more than half of global household laundry revenue, and the trend toward compact concentrates increases optical brightener intensity per wash. Formulators typically dose 0.1-0.5% by volume, yet colder cycles and phosphate-free builders require higher-purity triazine-stilbenes such as CBS-X to maintain fluorescence. The four largest home-care multinationals collectively command about 60% of detergent sales, creating oligopsonistic buying power that forces brightener suppliers to meet stringent biodegradability criteria without eroding margins. Novonesis introduced "Luminous" in 2024, a cross-matrix brightener designed for both liquids and powders, signaling renewed R&D aimed at reducing Stock Keeping Units (SKUs) for multinational brands. Retailers' private-label premium ranges in Europe and the U.S. are also adopting optical brighteners to match brand-leader aesthetics, cementing a durable volume base for the optical brighteners market.

Expansion of Textile and Apparel Manufacturing in Asia-Pacific

Regional value chains in Vietnam, India, and Bangladesh are scaling finishing capacity faster than spinning, shifting brightener consumption downstream into dyeing and wash-houses. Government programs such as Vietnam's net-zero road map and India's Production Linked Incentive for technical textiles are spurring investment in water-efficient dyeing lines that still depend on fluorescent agents to restore whiteness lost during recycled-fiber processing. Egypt's Sokhna industrial zone will add 15, 000 tons of fabric output from 2026, further widening Middle Eastern pull. Suppliers that localize technical-service labs near these clusters gain a defensible share of the optical brighteners market because shade matching and process troubleshooting remain relationship-driven.

Stringent Global Regulations on Stilbene Toxicity and Persistence

The European Commission added UV-328 to Annex I of Regulation (EU) 2019/1021 in 2025, introducing staged trace limits that cascade to 1 mg/kg by 2029. China's MEE Order 12 compels public disclosure of formulations by 2026, eroding intellectual-property shields for legacy products. The U.S. decision to retain antidumping duties on Chinese and Taiwanese stilbenes lengthens supply chains and raises landed costs. Collectively, these measures require comprehensive impurity profiling and life-cycle dossiers, expenses that smaller firms struggle to absorb, thereby tempering the optical brighteners market's otherwise healthy expansion.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Recycled-Paper and Packaging Brightness Requirements

- Adoption to Mask Discoloration in Recycled Plastics Streams

- Digitalization Cutting Printing-Paper Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Triazine-stilbenes captured 58.15% of the 2025 optical brighteners market share on the strength of broad formulary compatibility and high fluorescence quantum yields. Detergent-grade CBS-X can reach whiteness indexes above 130 and maintains stability from pH 7 to 11, ensuring continued volume leadership. Coumarins are forecast to advance at a 6.61% CAGR through 2031 as formulators prefer their lower-temperature processing thresholds for cosmetics and low-melt packaging coatings. Beyond the two headline groups, benzoxazolines such as OB-1 serve recycled-plastic compounding where more than 280 °C thermal stability is mandatory, sustaining a reliable niche.

Second-tier chemistries, such as imidazolines, diazoles, and pyrazolines, collectively keep a foothold in specialty textile finishing, especially chlorine-resistant sportswear. Pilot microreactor projects in Jiangxi Province demonstrate 96% yields for pyrazoline intermediates, suggesting technology headroom for cost parity with stilbenes. As emission caps tighten, suppliers able to retrofit legacy plants with continuous-flow systems may unlock incremental optical brighteners market share by marketing low-carbon product lines.

Geography Analysis

Asia-Pacific accounted for 58.76% of the global optical brighteners market revenue in 2025, driven by China's 116,000-ton annual consumption and sustained detergent premiumization. Capacity rationalization in Jiangsu and Zhejiang, spurred by dual-carbon targets and stricter wastewater rules, has already shuttered an estimated 12% of low-end output, tightening regional balances. India's ongoing 22,100 tonnes per annum (tpa) expansion by Rossari Biotech will provide incremental supply from 2026, yet is largely earmarked for local textile hubs. ASEAN's garments sector, especially in Vietnam, is investing in advanced finishing, which lifts per-meter brightener demand.

Europe and North America collectively hold a modest optical brighteners market share but wield outsized regulatory influence. The continuation of U.S. antidumping duties through 2030 locks in a two-tier price system that favors domestic output and diversified supply chains. In the EU, Annex I Persistent Organic Pollutants (POP) restrictions on UV-328 and impending Per- and Polyfluoroalkyl Substances (PFAS) legislation are persuading converters to prequalify low-migration stilbene replacements, granting early-mover advantage to producers with robust analytical labs.

The Middle-East and Africa post the fastest 6.87% CAGR to 2031, led by Saudi Arabia's woven-fabric projects under Vision 2030 and Egypt's Sokhna zone. Growth, though from a smaller base, is amplified by regional detergent factories that increasingly adopt liquid formats suitable for warmer climates. Brazil anchors South American demand, where Solvay's USD 20 million modernization of Santo Andre is designed to capture specialty polyamide finishing demand, indirectly stimulating the regional optical brighteners market volumes.

- 3V Sigma S.p.A.

- Archroma

- Aron Universal Limited

- BASF

- Blankophor GmbH & Co. KG

- Brilliant Group Inc.

- CLARIANT

- DayGlo Color Corp.

- Deepak Nitrite Limited

- Eastman Chemical Company

- Huntsman International LLC

- Keystone Aniline Corp.

- KISCO (Kyung-In Synthetic Corp.)

- Kolorjet Chemicals Pvt Ltd

- Meghmani Organics Ltd

- Milliken & Company

- RPM International Inc.

- Sarex Chemicals

- Shandong Raytop Chemical Co. Ltd

- Teh Fong Min International Co. Ltd

- United Specialities Pvt Ltd

- Zhejiang Transfar Whyyon Chemical Co Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for optical brighteners in laundry detergents

- 4.2.2 Expansion of textile and apparel manufacturing in Asia-Pacific

- 4.2.3 Growth in recycled-paper and packaging brightness requirements

- 4.2.4 Adoption to mask discoloration in recycled plastics streams

- 4.2.5 Use in security printing/anti-counterfeiting inks

- 4.3 Market Restraints

- 4.3.1 Stringent global regulations on stilbene-based toxicity and persistence

- 4.3.2 Digitalisation cutting printing-paper demand

- 4.3.3 R&D cost of eco-friendly bio-based substitutes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Chemical Type

- 5.1.1 Triazine-Stilbenes

- 5.1.2 Coumarins

- 5.1.3 Imidazolines

- 5.1.4 Diazoles

- 5.1.5 Benzoxazolines

- 5.1.6 Other Chemical Types

- 5.2 By Application

- 5.2.1 Textile Whitening

- 5.2.2 Detergent Brightener

- 5.2.3 Paper Brightening

- 5.2.4 Fiber Whitening

- 5.2.5 Cosmetics and Personal Care

- 5.2.6 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Textile and Apparel

- 5.3.2 Consumer Products

- 5.3.3 Packaging

- 5.3.4 Other End-user Industries (Security and Safety, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3V Sigma S.p.A.

- 6.4.2 Archroma

- 6.4.3 Aron Universal Limited

- 6.4.4 BASF

- 6.4.5 Blankophor GmbH & Co. KG

- 6.4.6 Brilliant Group Inc.

- 6.4.7 CLARIANT

- 6.4.8 DayGlo Color Corp.

- 6.4.9 Deepak Nitrite Limited

- 6.4.10 Eastman Chemical Company

- 6.4.11 Huntsman International LLC

- 6.4.12 Keystone Aniline Corp.

- 6.4.13 KISCO (Kyung-In Synthetic Corp.)

- 6.4.14 Kolorjet Chemicals Pvt Ltd

- 6.4.15 Meghmani Organics Ltd

- 6.4.16 Milliken & Company

- 6.4.17 RPM International Inc.

- 6.4.18 Sarex Chemicals

- 6.4.19 Shandong Raytop Chemical Co. Ltd

- 6.4.20 Teh Fong Min International Co. Ltd

- 6.4.21 United Specialities Pvt Ltd

- 6.4.22 Zhejiang Transfar Whyyon Chemical Co Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment