|

시장보고서

상품코드

2063515

클린룸 장갑 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cleanroom Gloves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

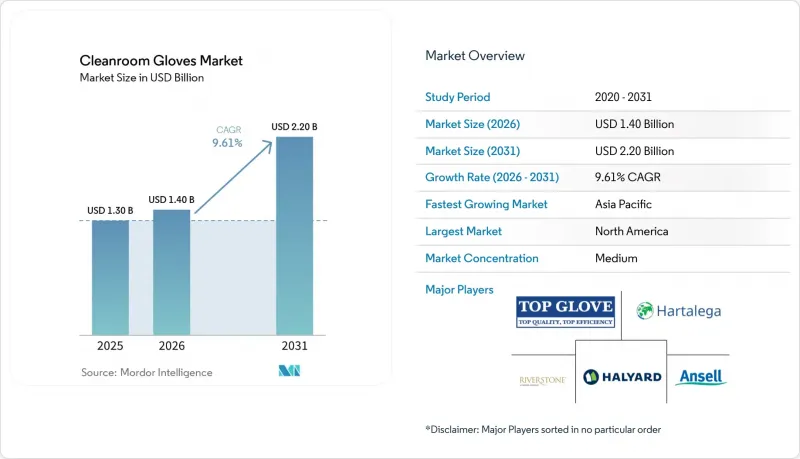

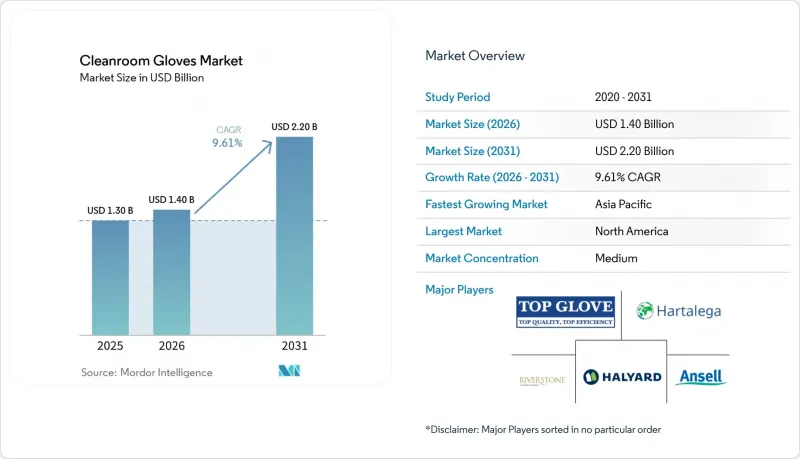

Mordor Intelligence에 의하면, 클린룸 장갑 시장 규모는 2025년에 13억 달러로 평가되었고 2026년 14억 달러에서 2031년까지 22억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.61%를 나타낼 전망입니다.

본 보고서는 소재별(니트릴 등), 최종 이용 산업별(반도체 및 마이크로전자, 제약, 생명공학, 의료기기 제조, 플랫 패널 디스플레이 및 광전자 등), 멸균 상태별(비멸균, 멸균), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 클린룸 장갑 시장 동향 및 인사이트

반도체 팹의 확장 및 오염 관리 강화

TSMC의 1,650억 달러 규모 피닉스 콤플렉스를 대표로 하는 전 세계 웨이퍼 팹 프로젝트는 1입방미터당 0.1µm 이상의 입자를 10개 미만으로 억제해야 하는 4nm에서 2nm로의 미세화 공정으로 전환되고 있습니다. ISO 클래스 1-2 청정실에서는 구리 배선 및 고유전율(high-k) 절연체의 수율을 유지하기 위해 정전기 방전(ESD) 대책이 마련되어 있으며, 이온 방출이 적은 니트릴 장갑이 요구되고 있어, 이로 인해 메가팹 1곳당 연간 수천만 장의 장갑 발주량이 증가하고 있습니다. SEMI는 2028년까지 프런트엔드 생산 능력이 상당한 연평균 성장률(CAGR)을 보일 것으로 전망하고 있으며, AI에 의해 가속화되는 노드 성장은 매우 두드러질 것으로 보입니다. 이는 직접적으로 운영자의 가동 시간 연장과 장갑 소비량 증가로 이어질 것입니다. 2026년 2월에 검증 절차가 완료된 인도의 마이크론 ATMP 공장은 첨단 패키징 분야의 지리적 확장과 적층 가공 장갑에 대한 수요 증가를 여실히 보여주고 있습니다.

바이오의약품 무균 제조에 대한 규제 강화

Annex 1의 58페이지에 걸친 개정 및 USP 797의 2023년 업데이트에 따라, 각 배치의 시작 및 종료 시 장갑의 무결성 검사가 의무화되었으며, 또한 고위험 조제 작업의 경우 분기별로 손가락 끝 샘플링을 실시해야 합니다. ISPE 2026 무균 제조 컨퍼런스에서 발표된 검증 데이터에 따르면, 배치당 장갑 소비량이 증가하고 있는 것으로 나타났습니다. 2주 만에 가동 가능한 모듈식 클린룸은 규정 준수 대응을 가속화하며, 북미 및 서유럽에서 단기적인 주문 급증을 부추기고 있습니다.

NBR/아크릴로니트릴-부타디엔 원료 가격 변동

2025년 4분기, 일본의 NBR 현물 가격은 톤당 3,574달러에 달하고, 미국 가격보다 40% 높았습니다. 이로 인해 장갑의 단위 원가에서 원자재비가 차지하는 비중이 약 30%로 상승했습니다. Top Glove사와 Hartalega사는 이익률을 안정화하기 위해 자사 라텍스 공장 건설과 3억 링깃 규모의 원료 설비 투자로 대응하고 있습니다.

부문별 분석

2025년 생산량에서 니트릴이 63.10%를 차지하여, 소재별로는 클린룸 장갑 시장에서 가장 큰 규모를 기록했습니다. 이 부문은 2031년까지 연평균 성장률(CAGR) 9.95%로 확대될 것으로 예상되며, 라텍스, 네오프렌, 폴리이소프렌, 비닐을 능가하는 성장세를 보일 것으로 전망됩니다. 클린룸 장갑 시장에서 점유율 1위를 차지하고 있는 이 기업은 천연 고무보다 3배 높은 내천자성을 갖추고 있으며, 반도체 및 배터리 공장에 적용되는 IEC 61340-5-1 규격의 정전기 임계값을 완벽하게 준수하고 있습니다. 2025년 7월에 출시된 Top Glove의 무할로겐 제품 라인은 3nm 이하 웨이퍼 노드에서 염소계 부식 위험을 제거하고, ISO 14644-1의 입자 수 상한 기준을 충족시키는 것을 목표로 한 혁신의 훌륭한 사례입니다.

라텍스는 알레르기 및 규제상의 이유로 시장 점유율이 계속 줄어들고 있는 반면, 폴리이소프렌은 단백질 알레르겐을 포함하지 않으면서도 라텍스와 같은 촉감을 구현함으로써 외과 분야에서 수요를 확보하고 있습니다. Medline사가 2025년에 출시한 ‘SensiCare’는 뛰어난 항암제 투과 저항성을 바탕으로, 종양학 분야의 약제 조제 분야에서 폴리이소프렌이 틈새 시장에서 두각을 나타내고 있음을 보여주었습니다. 네오프렌은 가혹한 화학 물질에 노출되는 특수 용도로 여전히 선택되고 있는 반면, 비닐은 천공 강도가 부차적인 요소가 되는 저위험 가운 착용실에서 선호되고 있습니다. INTCO사의 Syntex와 같은 하이브리드 합성 소재는 니트릴과 비닐을 혼합하여, 일반적인 전자기기 조립에 필요한 ISO 클래스 7 청정도 기준을 충족하는 중가대 대안을 제공합니다.

지역별 분석

북미는 2025년 매출의 38.19%를 차지했으며, 애리조나주, 오하이오주, 뉴욕주에서 웨이퍼 제조 및 첨단 패키징 클러스터 형성을 촉진한 CHIPS법에 따른 527억 달러 규모의 보조금이 그 원동력이 되었습니다. 2023년 USP 797 개정 이후, 503A 및 503B 약국을 위한 모듈식 클린룸이 보급되면서, 전미 약 7,500곳의 조제 시설에서 무균 장갑의 도입이 가속화되었습니다. 캐나다는 의료기기의 니어쇼어링을 활용해 수요 증가를 포착했으며, 멕시코에서는 자동차 배터리 공장이 ISO 클래스 7 드라이룸을 도입함에 따라 장갑 출하량이 증가했습니다.

아시아태평양은 가장 빠른 성장 궤도를 보이고 있으며, 2031년까지의 연평균 성장률(CAGR)은 10.15%로 예측됩니다. 인도의 182억 달러 규모 ‘반도체 미션’을 통해 마이크론은 2026년 2월 사난드에서 ATMP(반도체 제조 공정) 가동을 시작했습니다. 한편, 말레이시아의 주요 니트릴 장갑 제조업체인 할타레가, 리버스톤, 코산 등은 AI 주도형 데이터센터 건설 수요에 대응하기 위해 생산 능력을 확대했습니다. 중국이 미국산 수입품에 25%의 관세를 부과하고 있으며, FDA가 수입 경보를 발령함에 따라 조달처가 말레이시아와 태국의 제조업체로 전환되면서, 해당 지역공급 우위가 더욱 강화되고 있습니다. 또한, ESD 대응 니트릴 장갑을 지정하고 있는 한국과 일본의 전기차 배터리 기가팩토리의 존재 역시 해당 지역의 클린룸 장갑 시장을 더욱 견인하고 있습니다.

유럽의 성장은 EU 반도체법에 따른 430억 유로 규모의 지원 체계와 2023년 부속서 1의 시행에 힘입고 있습니다. 독일, 프랑스, 영국이 새로운 바이오의약품 공장 건설을 주도하고 있는 반면, 스칸디나비아 국가들의 PFAS 규제는 이미 PFAS가 포함되지 않은 장갑의 시범 도입을 촉진하고 있습니다. Hartalega사와 Sempermed사는 최근 독일의 백신 생산 거점과 다년간공급 계약을 체결하며 공급업체 다각화를 시사하고 있습니다. 동유럽은 동남아시아와의 임금 격차가 줄어들면서 일회용 장갑 위탁 생산의 제2 거점으로 부상하고 있습니다.

중동 및 아프리카 및 남미는 생산량 측면에서는 아직 발전 단계에 있지만, 일부 지역에서 성장세가 가속화되고 있습니다. 사우디아라비아의 ‘비전 2030’에 포함된 의약품 진흥 정책에는 ISO 클래스 7 장갑이 필요한 무균 인슐린 펜 생산 라인이 포함되어 있습니다. 브라질 ANVISA(국가위생감독청)에 제출된 정형외과용 임플란트 승인 신청이, 규모는 작지만 현지 클린룸 설비 확충을 촉진하고 있습니다. 리버스톤사는 2025 회계연도 4분기 클린룸 부문 매출이 2억 5,070만 링깃에 달했다고 보고했으며, 라틴아메리카 및 GCC 국가로의 납품이 증가하고 있는 점으로 미루어 볼 때, 아직 개척되지 않은 지역 시장이 존재함이 부각되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the cleanroom gloves market size was valued at USD 1.30 billion in 2025 and is estimated to grow from USD 1.40 billion in 2026 to reach USD 2.20 billion by 2031, at a CAGR of 9.61% during the forecast period (2026-2031).

This report is Segmented by Material (Nitrile, and More), End-Use Industry (Semiconductor & Microelectronics, Pharmaceuticals, Biotechnology, Medical Device Manufacturing, Flat Panel Display & Optoelectronics, and More), Sterility (Non-Sterile, Sterile), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Cleanroom Gloves Market Trends and Insights

Semiconductor Fab Expansions And Contamination Control Intensity

Global wafer-fab projects, typified by TSMC's USD 165 billion Phoenix complex, are scaling from 4 nm toward 2 nm geometries that tolerate fewer than 10 particles ≥0.1 µm per cubic meter. ISO Class 1-2 suites require ESD-safe, low-ion nitrile gloves to preserve yield in copper interconnects and high-k dielectrics, pushing annual glove orders into the tens of millions per megafab. SEMI forecasts a significant percentage CAGR in front-end capacity through 2028, while AI-accelerated nodes grow significantly, translating directly into longer operator hours and higher glove turnover. India's Micron ATMP plant, validated in February 2026, highlights the geographic spread of advanced packaging and the demand for additive gloves.

Biopharma Aseptic Manufacturing Tightening

Annex 1's 58-page revision and USP 797's 2023 update require glove-integrity tests at the start and end of each batch, plus quarterly fingertip sampling for high-risk compounding. Validation data showcased at the ISPE 2026 Aseptic Conference indicate a uplift in glove consumption per batch . Modular cleanrooms that commission in two weeks accelerate compliance, intensifying near-term ordering spikes in North America and Western Europe.

NBR/Acrylonitrile-Butadiene Feedstock Price Volatility

NBR spot prices hit USD 3,574/t in Japan during Q4 2025, 40% above U.S. levels, lifting the raw-material cost share to roughly 30% of glove unit economics. Top Glove and Hartalega have responded with captive latex plants and RM 300 million feedstock CAPEX to stabilize margins.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Latex To Nitrile In Cleanrooms

- Growth In Cleanroom-Intensive Medical Device Manufacturing

- Qualification/Validation Lock-In Slows Supplier Switching

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nitrile held 63.10% of 2025 volume, translating into the largest cleanroom gloves market size among material classes. The segment is projected to expand at a 9.95% CAGR to 2031, outpacing latex, neoprene, polyisoprene, and vinyl. The cleanroom gloves market share leader offers triple the puncture resistance of natural rubber and full compliance with IEC 61340-5-1 electrostatic thresholds that govern semiconductor and battery plants. Top Glove's halogen-free line, launched in July 2025, exemplifies innovation aimed at eliminating chlorine-based corrosion risks in sub-3 nm wafer nodes, keeping pace with ISO 14644-1 particle ceilings.

Latex continues to retreat on allergy and regulatory grounds, while polyisoprene captures surgical demand by replicating latex feel without protein allergens. Medline's 2025 SensiCare launch illustrated polyisoprene's niche ascent in oncology drug preparation thanks to superior chemotherapy permeation resistance. Neoprene remains a specialty choice for aggressive chemical exposure, while vinyl is preferred for low-risk gowning rooms where puncture strength is secondary. Hybrid synthetics like INTCO's Syntex blend nitrile and vinyl to offer a mid-priced option that meets ISO Class 7 cleanliness for general electronics assembly.

Geography Analysis

North America retained 38.19% of 2025 revenue, powered by USD 52.7 billion in CHIPS Act subsidies that catalyzed wafer-fab and advanced-packaging clusters in Arizona, Ohio, and New York. Modular cleanrooms for 503A and 503B pharmacies proliferated after the 2023 USP 797 revision, accelerating the adoption of sterile gloves among the roughly 7,500 compounding facilities nationwide. Canada leveraged medical-device nearshoring to capture incremental demand, and Mexico saw glove shipments rise as automotive battery plants introduced ISO Class 7 dry rooms.

Asia-Pacific posts the fastest trajectory, with a 10.15% CAGR projected to 2031. India's USD 18.2 billion Semiconductor Mission enabled Micron's Sanand ATMP launch in February 2026, while Malaysia's nitrile-glove majors-Hartalega, Riverstone, and Kossan expanded capacity to serve AI-driven data-center buildouts. China's 25% U.S. tariff exposure and FDA import alerts redirect procurement toward Malaysian and Thai producers, reinforcing regional supply dominance. The cleanroom gloves market in the region is further boosted by Korean and Japanese EV battery gigafactories that specify ESD-rated nitrile gloves.

Europe's growth benefits from the EU Chips Act's EUR 43 billion framework and 2023 Annex 1 enforcement. Germany, France, and the U.K. lead new biologics plants, while Scandinavian PFAS regulations are already prompting PFAS-free glove trials. Hartalega and Sempermed recently secured multi-year supply agreements with German vaccine sites, signaling supplier diversification. Eastern Europe emerges as a secondary hub for disposable-glove contract manufacturing as wage-cost differentials narrow against Southeast Asia.

Middle East & Africa and South America remain nascent in volume terms yet show isolated accelerants. Saudi Arabia's Vision 2030 pharmaceutical push includes sterile insulin-pen production lines that require ISO Class 7 gloves. Brazil's ANVISA pipeline for orthopedic implants is spurring local cleanroom upgrades, albeit from a small base. Riverstone cited RM 250.7 million in 4QFY25 cleanroom segment revenue, with Latin America and GCC deliveries on the rise, underscoring untapped geographic pockets.

- Ansell

- Cardinal Health

- CleanPro/Blue Thunder (distributors)

- CT International

- Thermo Fisher Scientific

- Halyard

- Hartalega

- Honeywell (Isolator/Glovebox)

- Kossan Rubber Industries

- Piercan

- Protective Industrial Products (QRP)

- Riverstone Holdings

- Sempermed

- SHIELD Scientific

- Showa Group

- STAXS

- Supermax

- TechNiGlove

- Top Glove

- Valutek

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Semiconductor Fab Expansions and Contamination Control Intensity

- 4.2.2 Biopharma Aseptic Manufacturing Tightening (Annex 1/USP 797)

- 4.2.3 Shift From Latex to Nitrile in Cleanrooms (Allergy, ESD, Extractables)

- 4.2.4 Growth In Cleanroom-Intensive Medical Device Manufacturing

- 4.2.5 EV Battery Dry-Room Buildouts Needing ESD-Safe Gloves

- 4.2.6 PFAS-Free and Low-Ion Formulations Opening Premium Niches

- 4.3 Market Restraints

- 4.3.1 NBR/Acrylonitrile-Butadiene Feedstock Price Volatility

- 4.3.2 Qualification/Validation Lock-In Slows Supplier Switching

- 4.3.3 Particulation/Extractables Limits Raise Costs and Scrap

- 4.3.4 Robotics And Gloveless Isolators Reducing Manual Touchpoints

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Nitrile (NBR)

- 5.1.2 Natural Rubber (Latex)

- 5.1.3 Neoprene (Polychloroprene)

- 5.1.4 Polyisoprene

- 5.1.5 Vinyl (PVC)

- 5.2 By End-use Industry

- 5.2.1 Semiconductor & Microelectronics

- 5.2.2 Pharmaceuticals

- 5.2.3 Biotechnology

- 5.2.4 Medical Device Manufacturing

- 5.2.5 Flat Panel Display & Optoelectronics

- 5.2.6 Others

- 5.3 By Sterility

- 5.3.1 Non-sterile

- 5.3.2 Sterile

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Ansell

- 6.3.2 Cardinal Health

- 6.3.3 CleanPro/Blue Thunder (distributors)

- 6.3.4 CT International

- 6.3.5 Thermo Fisher Scientific

- 6.3.6 Halyard

- 6.3.7 Hartalega

- 6.3.8 Honeywell (Isolator/Glovebox)

- 6.3.9 Kossan Rubber Industries

- 6.3.10 Piercan

- 6.3.11 Protective Industrial Products (QRP)

- 6.3.12 Riverstone Holdings

- 6.3.13 Sempermed

- 6.3.14 SHIELD Scientific

- 6.3.15 Showa Group

- 6.3.16 STAXS

- 6.3.17 Supermax

- 6.3.18 TechNiGlove

- 6.3.19 Top Glove Corporation

- 6.3.20 Valutek

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment