|

시장보고서

상품코드

2063516

합성 흡수성 봉합사 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Synthetic Absorbable Sutures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

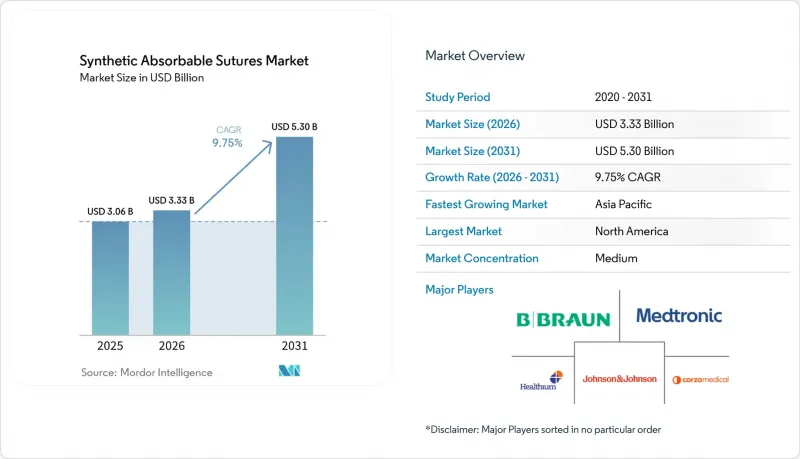

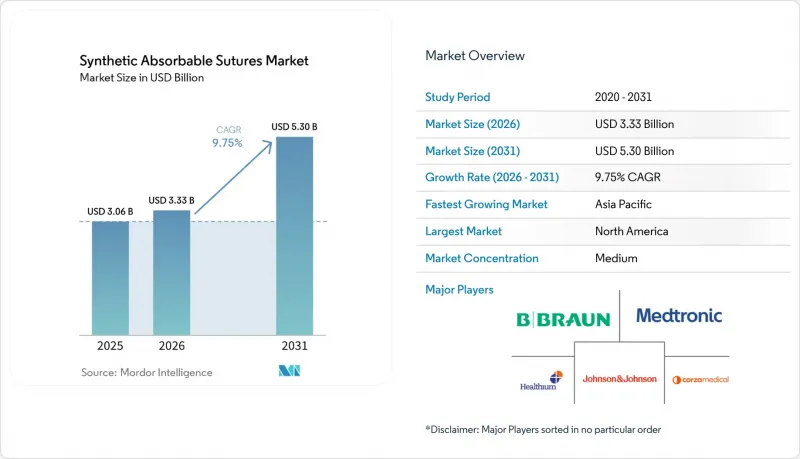

Mordor Intelligence에 의하면, 합성 흡수성 봉합사 시장 규모는 2025년에 30억 6,000만 달러, 2026년에 33억 3,000만 달러, 2031년까지 53억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 9.75%로 성장할 것으로 전망됩니다.

본 보고서는 소재별(폴리글락틴 910, 폴리글리콜산, 폴리그레카프론 25 등), 용도별(일반외과, 정형외과, 심혈관·흉부 외과, 산부인과 등), 최종 사용자별(병원, 외래수술센터(ASC), 전문 클리닉), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 합성 흡수성 봉합사 시장 동향 및 인사이트

수술 건수 증가와 고령화

인구 고령화와 만성 질환 유병률 증가에 따라 수술 건수가 늘어나고 있습니다. 이탈리아에서는 2023년에 12만 2,777건의 선택적 인공 고관절 전치환술이 시행되었으며, 이는 2001년 대비 80% 증가한 수치로, 모델 예측에 따르면 2050년까지 20% 더 증가할 것으로 전망됩니다. 인도의 의료 시장은 2025년에 6,380억 달러에 달할 전망이며, 민간 의료기관은 2029년까지 34,000개의 신규 병상을 확보할 계획으로, 이를 통해 더 많은 선택적 수술이 가능해질 것입니다. 당뇨병 및 심혈관 질환 환자 수가 증가함에 따라, 분해 속도가 조절되는 흡수성 봉합재에 대한 수요가 높아지고 있습니다.

저침습 수술 및 외래 수술로의 전환

현재 로봇 수술이나 복강경 수술에서는 모노필라멘트 봉합사나 바브가 달린 봉합사가 요구되고 있으며, 결찰 절차가 간소화되고 있습니다. 미국에서 실시된 22만 4,307건의 로봇 수술에 대한 조사에 따르면, 결찰이 필요 없는 기기의 사용은 대장·직장 수술에서 3배 증가했으며, 합병증 증가를 초래하지 않으면서 수술실 체류 시간을 최대 19.1분 단축시켰습니다. 외래수술센터(ASC)는 이러한 효율성을 활용하여, 당일 수술 증가를 촉진하는 보험 급여의 균등화 조치로 인한 혜택을 누리고 있습니다.

스테이플러, 접착제 및 에너지를 이용한 봉합법과의 경쟁

피브린 접착제 시장 규모는 2029년까지 9억 3,468만 달러에 달할 것으로 예상되며, 탈장 교정술, 안과 수술, 혈관 수술에서 수술 시간을 단축할 가능성이 있습니다. 스테이플러는 흉부 수술을 신속하게 진행하게 하며, 초음파 실러는 결찰의 필요성을 없애줍니다. 봉합사는 장력의 분산과 서서히 흡수되는 특성이 필수적인 상황에서 여전히 우위를 점하고 있으며, 각 공급업체들은 현재 시장 점유율을 지키기 위해 봉합사와 지혈제를 세트로 판매하고 있습니다.

부문별 분석

2025년 합성 흡수성 봉합사 시장에서 폴리글락틴 910은 매출의 34.58%를 차지했습니다. 이 소재의 편조 구조는 결찰의 안정성을 보장하지만, 표면에 세균이 쉽게 부착된다는 문제가 있습니다. 현재 외과의사들은 폴리글레카프로론 25와 같은 모노필라멘트 봉합사로 전환하고 있으며, 해당 시장은 연평균 성장률(CAGR) 10.54%로 성장할 것으로 전망됩니다. 이러한 변화는 저침습 폐쇄술 분야의 합성 흡수성 봉합사 시장의 장기적인 성장을 뒷받침할 것입니다. 폴리디옥사논은 180일간의 체내 잔류 기간이 조직 재형성을 촉진하기 때문에 정형외과 및 심혈관외과 분야에서 프리미엄 틈새 시장을 유지하고 있습니다.

이 혁신의 핵심은 항균 코팅과 바브 형상에 있습니다. 메릴사의 ‘2024 New Edge Sutures’는 실리콘 다층 코팅과 특허를 취득한 선단 형상을 결합하여 조직에 가해지는 저항을 줄여줍니다. 클로르헥시딘을 함침시킨 글리코마 631 실에 대한 조사는 차세대 제품의 차별화를 예고합니다.

지역별 분석

북미는 2025년 매출의 46.46%를 차지하며, 미국에서는 가치 기반 구매 제도(VBP) 하에서 발생하는 페널티를 완화하기 위해 항균 제품 및 바브가 부착된 제품에 대한 의존도가 높아지고 있습니다. EPA의 에틸렌옥사이드 사용량 90% 감축 조치로 인해 과산화수소를 이용한 멸균에 대한 관심이 높아지고 있지만, 단기적으로는 비용 상승으로 이어질 가능성이 있습니다.

유럽에서는 수술 건수가 성숙 단계에 접어들어 중앙 조달을 통한 입찰로 인해 가격이 압박받고 있지만, MDR(의료기기 규정)이라는 장벽이 기존 브랜드를 보호하고 있습니다. B. Braun의 Aesculap 사업부는 21억 6,000만 유로(25억 4,000만 달러)의 매출을 기록했으며, 생체적합성 의료기기 외에도 바브가 장착된 Symmcora 제품 라인의 확대를 추진하고 있습니다. 아시아태평양은 연평균 성장률(CAGR) 10.01%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 인도의 의료 기술 발전과 Healthium사의 스리시티 내 신규 공장은 OEM 생산 능력 확대와 수출에 대한 의지를 보여주고 있습니다. 중국의 입찰 제도는 국내 브랜드를 우대하는 반면, 일본과 호주에서는 바브가 부착된 제품에 대한 수요가 여전히 높은 수준을 유지하고 있습니다. 중동 및 아프리카 및 남미 지역 시장 점유율은 낮지만, GCC 국가들의 제왕절개 수요나 브라질의 산과 분야 등 환율 변동의 영향을 받지 않는 지역에서는 수요가 지속되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the synthetic absorbable sutures market size is projected to be USD 3.06 billion in 2025, USD 3.33 billion in 2026, and reach USD 5.30 billion by 2031, growing at a CAGR of 9.75% from 2026 to 2031.

This report is Segmented by Material (Polyglactin 910, Polyglycolic Acid, Poliglecaprone 25, and More), Application (General Surgery, Orthopedic Surgery, Cardiovascular & Thoracic Surgery, Gynecology & Obstetrics, and More), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Synthetic Absorbable Sutures Market Trends and Insights

Rising Surgical Procedure Volumes And Aging Populations

Procedure counts climb as populations age and chronic disease prevalence rises. Italy performed 122,777 elective total hip arthroplasties in 2023, up 80% since 2001, and models predict a further 20% rise by 2050. India's healthcare market reached USD 638 billion in 2025, and private systems plan 34,000 new beds by FY2029, supporting more elective surgeries. Growing diabetic and cardiovascular patient pools heighten demand for absorbable closure products with controlled degradation.

Migration To Minimally Invasive And Outpatient Surgeries

Robotic and laparoscopic approaches now require monofilament or barbed sutures, reducing the number of knot-tying steps. A U.S. review of 224,307 robotic cases showed that the use of knotless devices tripled in colorectal surgery and cut operating-room time by up to 19.1 minutes, without increased complications. Ambulatory surgical centers leverage these efficiencies and benefit from reimbursement parity that drives more same-day procedures.

Competition From Staplers, Adhesives, And Energy-Based Closure

Fibrin glues could reach USD 934.68 million by 2029 and cut OR time in hernia repair, eye surgery and vascular work. Staplers speed thoracic procedures, while ultrasonic sealers remove the need for ligatures. Sutures keep their edge where tension distribution or slow absorption is vital, and vendors now bundle sutures with hemostatics to defend share.

Other drivers and restraints analyzed in the detailed report include:

- Adoption Of Antibacterial Absorbable Sutures To Cut SSI Risk

- Rapid Uptake Of Knotless/Barbed Absorbable Sutures In Robotic/MIS Closures

- Tender-Driven Price Pressure And Commoditization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyglactin 910 accounted for 34.58% of 2025 revenue in the synthetic absorbable sutures market. The material's braided structure assures knot security, but its surface harbors bacteria. Surgeons are now pivoting toward monofilaments such as Poliglecaprone 25, forecast to grow at a 10.54% CAGR. This shift underpins the long-term expansion of the synthetic absorbable sutures market size among minimally invasive closures. Polydioxanone retains a premium niche in orthopedic and cardiovascular work because its 180-day retention profile supports tissue remodeling.

Innovation centers on antimicrobial layering and barbed geometry: Meril's 2024 New Edge Sutures fuse silicon multi-coating with a patented point to lessen tissue drag. Research into chlorhexidine-impregnated glycomer 631 threads signals next-wave differentiation.

Geography Analysis

North America accounted for 46.46% of 2025 revenue, with the United States relying on antibacterial and barbed products to mitigate infection penalties under value-based purchasing . EPA's 90% ethylene oxide cut widens interest in hydrogen peroxide sterilization, yet may raise costs in the near term.

Europe shows mature procedure volumes; centralized tenders squeeze prices, but MDR barriers shelter established brands. B. Braun's Aesculap unit posted EUR 2.16 billion (USD 2.54 billion) in revenue and is pushing barbed Symmcora lines alongside biosurgicals. Asia-Pacific is the fastest-growing region at a 10.01% CAGR. India's med-tech push and Healthium's new plant in Sri City illustrate OEM capacity gains and export ambitions. Chinese tender systems favor domestic labels, while Japan and Australia retain premium barbed uptake. The Middle East & Africa and South America contribute smaller shares, but pockets such as GCC cesarean demand and Brazilian obstetrics sustain volume where currency swings permit.

- Advanced Medical Solutions

- Atramat

- B. Braun Melsungen AG.

- Corza Medical

- DemeTECH

- Dolphin Sutures

- Healthium Medtech

- Johnson & Johnson

- Katsan

- MANI, Inc.

- Medtronic

- Meril Life Sciences

- Peters Surgical

- Riverpoint Medical

- SERAG-WIESSNER

- SMI AG

- Teleflex Medical OEM

- Universal Sutures

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Surgical Procedure Volumes and Aging Populations

- 4.2.2 Migration To Minimally Invasive and Outpatient Surgeries

- 4.2.3 Adoption Of Antibacterial Absorbable Sutures to Cut the SSI Risk

- 4.2.4 Orthopedic And Cardiovascular Surgery Burden Expanding, and Closure Demand

- 4.2.5 Rapid Uptake of Knotless/Barbed Absorbable Sutures in Robotic/MIS Closures

- 4.2.6 OEM/Private-Label Capacity in EMS Accelerating Synthetic Absorbable Penetration

- 4.3 Market Restraints

- 4.3.1 Competition From Staplers, Adhesives, And Energy-Based Closure

- 4.3.2 Tender-Driven Price Pressure and Commoditization

- 4.3.3 Regulatory Scrutiny of Triclosan and Divergent Hospital Antimicrobial Policies

- 4.3.4 EtO sterilization rules are raising compliance costs and lead-time risks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Polyglactin 910 (PGLA 910)

- 5.1.2 Polyglycolic Acid (PGA)

- 5.1.3 Poliglecaprone 25 (PGCL)

- 5.1.4 Polydioxanone (PDO)

- 5.1.5 Polyglyconate

- 5.1.6 Glycomer 631

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Orthopedic Surgery

- 5.2.3 Cardiovascular & Thoracic Surgery

- 5.2.4 Gynecology & Obstetrics

- 5.2.5 Gastrointestinal & Colorectal

- 5.2.6 Plastic & Reconstructive

- 5.2.7 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers (ASCs)

- 5.3.3 Specialty Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Advanced Medical Solutions

- 6.3.2 Atramat

- 6.3.3 B. Braun Melsungen AG.

- 6.3.4 Corza Medical

- 6.3.5 DemeTECH Corporation

- 6.3.6 Dolphin Sutures

- 6.3.7 Healthium Medtech

- 6.3.8 Johnson & Johnson

- 6.3.9 Katsan

- 6.3.10 MANI, Inc.

- 6.3.11 Medtronic Inc.

- 6.3.12 Meril Life Sciences

- 6.3.13 Peters Surgical

- 6.3.14 Riverpoint Medical

- 6.3.15 SERAG-WIESSNER

- 6.3.16 SMI AG

- 6.3.17 Teleflex Medical OEM

- 6.3.18 Universal Sutures

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment