|

시장보고서

상품코드

2063540

유전자 분석 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Genetic Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

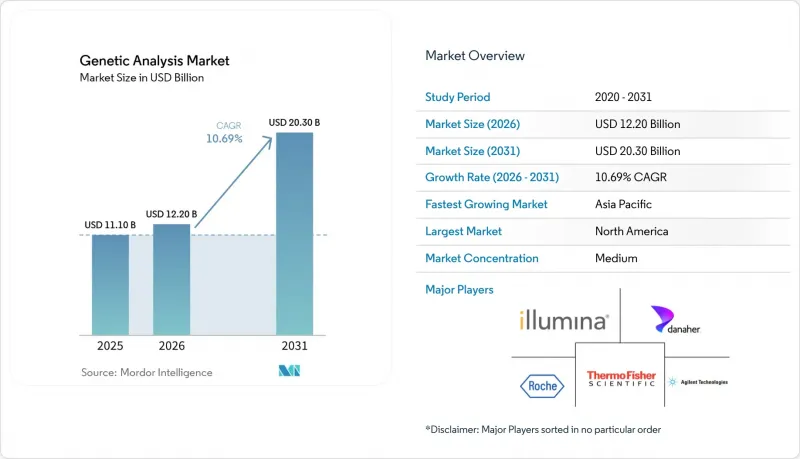

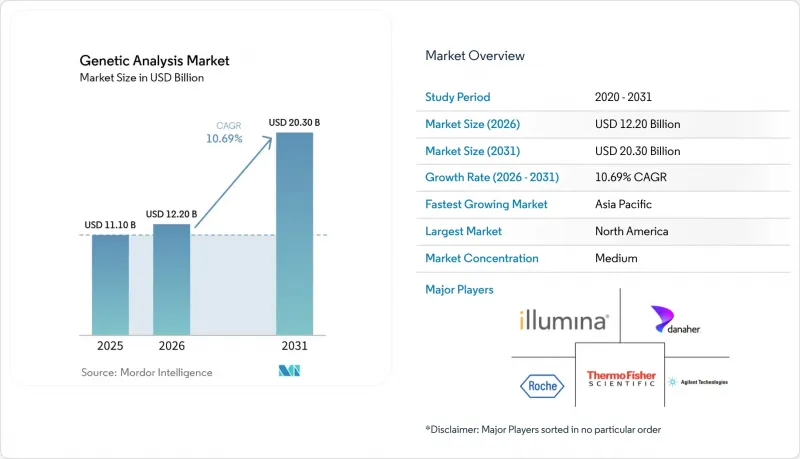

Mordor Intelligence에 의하면, 유전자 분석 시장 규모는 2025년 111억 달러에서 2026년에는 122억 달러로 확대되어 2031년까지 203억 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 10.69%로 성장할 전망입니다.

본 보고서는 제품 및 서비스(장비 및 시스템, 소모품 및 시약 등), 기술(PCR/QPCR, NGS 쇼트 리드, 롱 리드 시퀀싱 등), 용도(임상 진단, 약리유전체학 등), 최종 사용자(병원 및 클리닉 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 유전자 분석 시장 동향과 인사이트

시퀀싱 비용의 감소로 인해 유전체당 비용이 절감되었습니다.

전체 유전체 염기서열 분석 비용은 2013년 이후 96% 하락했으며, 2025년에는 검체당 200-600달러에 달할 것으로 전망됩니다. 또한, 퍼시픽 바이오사이언스가 계획 중인 SPRQ-Nx 플랫폼은 2026년 하반기까지 비용을 300달러 미만으로 낮추는 것을 목표로 하고 있습니다. 영국, 인도, 중국에서 신생아 및 성인을 대상으로 한 대규모 연구가 확대됨에 따라, 각 벤더 기업들은 하드웨어 판매 중심의 비즈니스 모델에서 소모품 및 소프트웨어의 정기 구독 모델로 전환하고 있습니다. 그 예로, 퍼시픽 바이오사이언스가 2025년 4분기에 소모품 매출이 55% 증가했다고 보고한 사실을 들 수 있습니다. GenomeIndia와 같은 신흥 시장에서의 프로젝트는 유전체당 비용의 감소가 인구 다양성을 대상으로 한 연구의 길을 열어줄 것임을 보여주고 있습니다. 그 결과, 도입 기반이 확대되고 지속적인 수익원이 창출되며, 유전자 분석 시장이 안정화될 것입니다.

임상 보험 급여 및 CDx 승인 확대

CMS는 2026년 1월부터 일루미나(Illumina)사의 ‘TruSight Oncology Comprehensive’에 대해 2,989.55달러를 지급하기로 결정했습니다. 또한, 메디케어도 2026년 3월부터 네오제노믹스사의 500개 유전자 액체 생검을 보험 적용 대상으로 지정했습니다. UnitedHealthcare 등 민간 보험사들도 이에 발맞추어 보험 계약을 갱신하며, 고처리량 시퀀서 도입을 위한 검사실 투자를 촉진하고 있습니다. Guardant 360 CDx 및 기타 대규모 패널에 대한 FDA의 승인은 보다 광범위한 검사가 비용이 많이 드는 생검 재실시를 줄일 수 있음을 보험사들에게 보여주고 있습니다. 이러한 추세는 유전자 분석 시장에서 처리되는 검사 건수를 증가시켜, 자동화 워크플로우 솔루션에 대한 수요를 뒷받침하고 있습니다.

데이터 개인정보 보호 및 국경을 넘는 데이터 전송에 대한 제약

2027년까지 운영될 ‘유럽 헬스 데이터 스페이스(European Health Data Space)’에 따라, 공급업체는 EU 내 클라우드에 데이터를 호스팅하고 엄격한 동의 요건을 충족해야 할 의무가 있습니다. 이로 인해 규정 준수 비용이 증가하여, 자본력이 있는 기업이 유리한 입장에 서게 됩니다. 소규모 검사 기관들은 통합이나 철수를 피할 수 없게 될 가능성이 있으며, 유전자 분석 시장의 성장 속도는 둔화되겠지만, 그 방향성에는 영향을 미치지 않을 것입니다.

부문별 분석

정기적인 시약 키트는 2025년 매출의 58.9%를 차지하며, 검사실 현장의 유전자 분석 시장 규모를 뒷받침하고 있습니다. 롱 리드 및 공간 분석 플랫폼으로의 장비 업그레이드가 연평균 성장률(CAGR) 12.4%를 뒷받침하고 있으며, 번들로 제공되는 소프트웨어 구독 서비스가 고객사당 평균 거래액을 끌어올리고 있습니다. 시약, 소프트웨어, 서비스를 통합한 생태계가 공급업체의 가격 결정력을 뒷받침하고 있습니다.

연구소가 고처리량 및 멀티오믹스 워크플로로 전환함에 따라, 장비와 시스템은 교체 시기에 접어들고 있습니다. 수익이 소모품을 중심으로 집중되어 있기 때문에 공급업체들은 설비 투자 주기를 무사히 헤쳐 나갈 수 있으며, 유전자 분석 시장은 꾸준한 성장 궤도를 유지하고 있습니다.

2025년 기준으로, 쇼트 리드 NGS는 유전자 분석 시장 점유율의 32.2%를 차지했으나, 롱 리드 시퀀싱은 2031년까지 연평균 성장률(CAGR) 14.0%로 성장하여 가장 빠르게 확대되는 부문이 될 것으로 예측됩니다. 페이싱 및 구조적 변이 규명에 대한 임상적 수요가 증가함에 따라, 퍼시픽 바이오사이언스(Pacific Biosciences)와 옥스포드 나노포어(Oxford Nanopore)의 장비가 종양학 및 희귀질환 검사실에 도입되고 있습니다. 한편, 디지털 PCR은 유전자 치료의 품질 관리(QC) 분야에서 그 활용이 확대되고 있습니다. 기술 구성이 세분화되고 있는 가운데, 서로 다른 데이터 스트림을 통합하여 유전자 분석 시장의 입지를 확대할 수 있는 정보학 계층이 요구되고 있습니다.

지역별 분석

2025년, 북미는 유전자 분석 시장 점유율의 43.29%를 차지했습니다. 높은 보험 보상 수준, 병원 및 검사실 간의 긴밀한 네트워크, 그리고 종합적인 유전체 프로파일링의 조기 도입이 이 지역 수요를 뒷받침하고 있습니다. 메디케어·메디케이드 서비스 센터(CMS)는 2026년 1월부터 일루미나(Illumina)사의 ‘TruSight Oncology Comprehensive’ 검사에 대해 2,989.55달러의 지급액을 책정함으로써, 종양학 진료 분야에서 광범위한 다중 유전자 패널의 도입을 가속화하고 있습니다. 로슈가 2030년까지 미국 내 신규 생산 시설 및 AI 주도 연구개발 시설에 500억 달러를 투자하겠다는 약속은 시장의 장기적인 성장 궤도에 대한 확신을 뒷받침하고 있습니다. 2031년까지는 북미가 최대의 수익원으로 남아 있을 것으로 보이지만, 종양학 및 희귀질환 검사가 포화 상태에 가까워짐에 따라 성장은 둔화될 것으로 예상되며, 업체들의 초점은 약물유전체학, 산전 선별검사 및 인구 건강 분야로 옮겨갈 것입니다.

아시아태평양은 대규모 공공 유전체 프로그램의 뒷받침을 받아 2026년부터 2031년까지 연평균 성장률(CAGR) 12.97%로 가장 높은 성장률을 나타낼 것으로 전망됩니다. 중국의 ‘국가 유전체 뱅크’는 현재 1,000만 건 이상의 유전체 데이터를 보유하고 있으며, 연구 및 임상 시퀀싱을 모두 지원하고 있습니다. 인도의 ‘GenomeIndia’ 이니셔티브는 1만 건의 유전체 분석을 완료했으며, 전 세계 데이터베이스에서 충분히 대표되지 않은 남아시아계 조상 집단의 포괄성을 확대할 계획입니다.

유럽에서는 각국 간의 협력 프로그램 외에도, 회원국 간 국경을 초월한 유전체 데이터 공유를 표준화하는 ‘유럽 헬스 데이터 스페이스(European Health Data Space)’가 활용되고 있습니다. NHS 유전체 의료 서비스는 2024년에 81만 건 이상의 검사를 실시한 반면, Genomics England는 신생아 10만 명과 성인 15만 명을 대상으로 유전체 염기서열 분석을 수행하며, 전장 유전체 검사를 일상 진료에 도입하고 있습니다. 이 지역들 외에도 걸프 연안 국가들, 남아프리카, 브라질에서는 유전체 센터의 규모 확대가 진행되고 있지만, 라틴아메리카와 동유럽의 일부 지역에서는 보험 급여 격차로 인해 여전히 단기적인 보급이 제한되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the genetic analysis market size is expected to increase from USD 11.10 billion in 2025 to USD 12.20 billion in 2026 and reach USD 20.30 billion by 2031, growing at a CAGR of 10.69% over 2026-2031.

This report is Segmented by Product & Service (Instruments & Systems, Consumables & Reagents, and More), Technology (PCR/QPCR, NGS Short-Read, Long-Read Sequencing, and More), Application (Clinical Diagnostics, Pharmacogenomics, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, APAC, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Genetic Analysis Market Trends and Insights

Declining Sequencing Costs Compress Cost-per-Genome

Whole-genome sequencing prices have dropped 96% since 2013, reaching USD 200-600 per sample in 2025, and Pacific Biosciences' planned SPRQ-Nx platform aims to push costs below USD 300 in late 2026. As large newborn and adult studies in the United Kingdom, India, and China ramp up, vendors are pivoting from a hardware-sale mindset to recurring-reagent and software subscriptions, evidenced by Pacific Biosciences reporting 55% consumables growth in Q4 2025. Emerging-market projects such as GenomeIndia illustrate that lower per-genome costs open doors for population diversity studies. The result is a deeper installed base and recurring revenue streams that stabilize the genetic analysis market.

Expanding Clinical Reimbursement and CDx Approvals

CMS set a USD 2,989.55 payment for Illumina's TruSight Oncology Comprehensive, effective January 2026, while Medicare also covered NeoGenomics' 500-gene liquid biopsy in March 2026. Private insurers such as UnitedHealthcare updated policies accordingly, catalyzing laboratory investment in higher-throughput sequencers. FDA approvals for Guardant 360 CDx and other large panels are teaching payers that broader tests reduce costly repeat biopsies. The trend escalates volumes flowing through the genetic analysis market and underpins demand for automated workflow solutions.

Data Privacy and Cross-Border Transfer Constraints

The European Health Data Space, operational through 2027, forces vendors to host data on EU-resident clouds and meet strict consent requirements, inflating compliance costs and favoring capital-rich players. Smaller labs may consolidate or exit, tempering pace but not direction of growth for the genetic analysis market.

Other drivers and restraints analyzed in the detailed report include:

- National Genomics Programs Integrating WGS into Care

- AI-Enabled Variant Interpretation Accelerates Insights

- High Capital Investment Requirements for Laboratory Infrastructure and Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recurring reagent kits generated 58.9% of 2025 revenue, anchoring the genetic analysis market size at the laboratory bench. Instrument upgrades to long-read and spatial platforms support a 12.4% CAGR, and bundled software subscriptions are lifting average account value. Integrated ecosystems that lock in reagents, software, and service underpin vendor pricing power.

Instruments & systems are entering a replacement phase as labs shift to higher throughput and multiomics workflows. Revenue clustering around consumables allows vendors to weather capital-spending cycles, keeping the genetic analysis market on a steady growth track.

Short-read NGS held 32.2% of the genetic analysis market share in 2025, but long-read sequencing is forecast to be the fastest segment with 14.0% CAGR through 2031. Clinical need for phasing and structural-variant clarity is bringing Pacific Biosciences and Oxford Nanopore into oncology and rare-disease labs. Meanwhile, digital PCR is expanding in gene-therapy QC. The technology mix is fragmenting, requiring informatics layers that can harmonize heterogeneous data streams and broaden the genetic analysis market footprint.

Geography Analysis

North America captured 43.29% of the genetic analysis market share in 2025. High reimbursement levels, dense hospital and laboratory networks, and early use of comprehensive genomic profiling sustain regional demand. The Centers for Medicare & Medicaid Services set a USD 2,989.55 payment for Illumina's TruSight Oncology Comprehensive test effective January 2026, accelerating the adoption of broad multi-gene panels in oncology practices. Roche's USD 50 billion commitment to new U.S. manufacturing and AI-driven R&D facilities through 2030 underscores confidence in the market's long-term trajectory. While North America will remain the largest revenue contributor through 2031, growth is expected to moderate as oncology and rare-disease testing nears saturation, shifting vendor emphasis toward pharmacogenomics, prenatal screening, and population-health applications.

Asia-Pacific is projected to log the fastest 12.97% CAGR between 2026 and 2031, fueled by large-scale public genomics programs. China's National GeneBank now houses data from more than 10 million genomes, supporting both research and clinical sequencing. India's GenomeIndia initiative has completed 10,000 genomes and plans to broaden coverage of South Asian ancestry groups that are under-represented in global databases.

Europe benefits from coordinated country programs and the European Health Data Space, which standardizes cross-border genomic data sharing across member states. The NHS Genomic Medicine Service delivered more than 810,000 tests in 2024, while Genomics England is sequencing 100,000 newborns and 150,000 adults, weaving whole-genome testing into routine care. Beyond these regions, Gulf states, South Africa, and Brazil are scaling genomics centers, though reimbursement gaps in parts of Latin America and Eastern Europe still limit near-term uptake.

- 10x Genomics

- Agilent Technologies

- Azenta

- BGI / MGI Tech

- Bio-Rad Laboratories

- Danaher

- Eurofins

- Roche

- Guardant Health

- Helix

- Illumina

- LabCorp

- Myriad Genetics

- Natera

- New England Biolabs (NEB)

- Novogene

- Oxford Nanopore Technologies

- Pacific Biosciences

- QIAGEN

- Quest Diagnostics

- Revvity

- Takara Bio

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining Sequencing Costs Compress Cost-Per-Genome

- 4.2.2 Expanding Clinical Reimbursement and CDX Approvals

- 4.2.3 National Genomics Programs Integrating WGS Into Care

- 4.2.4 EU New Genomic Techniques Enabling Agri-Genomics

- 4.2.5 AI-Enabled Variant Interpretation Accelerates Insights

- 4.2.6 Rising Liquid Biopsy Adoption for MRD And Early Detection

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-Border Transfer Constraints (GDPR Etc.)

- 4.3.2 China HGR Rules Constrain Cross-Border Genomics

- 4.3.3 Reimbursement Variability for Comprehensive CGP/WGS

- 4.3.4 Data Localization and Sovereign Cloud Requirements

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Instruments & Systems

- 5.1.2 Consumables & Reagents

- 5.1.3 Software & Bioinformatics Services

- 5.2 By Technology

- 5.2.1 PCR/qPCR

- 5.2.2 Next-Generation Sequencing (short-read)

- 5.2.3 Long-read Sequencing (SMRT, Nanopore)

- 5.2.4 Sanger Sequencing

- 5.2.5 Microarrays

- 5.2.6 Cytogenetics (Karyotyping, FISH)

- 5.2.7 Genotyping & Gene Expression (non-NGS)

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.2 Pharmacogenomics

- 5.3.3 Agriculture & Animal Genomics

- 5.3.4 Forensics & Human Identification

- 5.3.5 Consumer/Ancestry & Wellness

- 5.3.6 Research Applications (functional, transcriptomics, single-cell)

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Diagnostic & Reference Laboratories

- 5.4.3 Academic & Research Institutes

- 5.4.4 Pharmaceutical & Biotechnology Companies

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 10x Genomics

- 6.3.2 Agilent Technologies

- 6.3.3 Azenta Life Sciences

- 6.3.4 BGI / MGI Tech

- 6.3.5 Bio-Rad Laboratories

- 6.3.6 Danaher Corporation

- 6.3.7 Eurofins Scientific

- 6.3.8 F. Hoffmann-La Roche

- 6.3.9 Guardant Health

- 6.3.10 Helix

- 6.3.11 Illumina

- 6.3.12 Labcorp

- 6.3.13 Myriad Genetics

- 6.3.14 Natera

- 6.3.15 New England Biolabs (NEB)

- 6.3.16 Novogene

- 6.3.17 Oxford Nanopore Technologies

- 6.3.18 Pacific Biosciences

- 6.3.19 QIAGEN

- 6.3.20 Quest Diagnostics

- 6.3.21 Revvity

- 6.3.22 Takara Bio

- 6.3.23 Thermo Fisher Scientific

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment