|

시장보고서

상품코드

2063548

의료용 수액백 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Medical Fluid Bags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

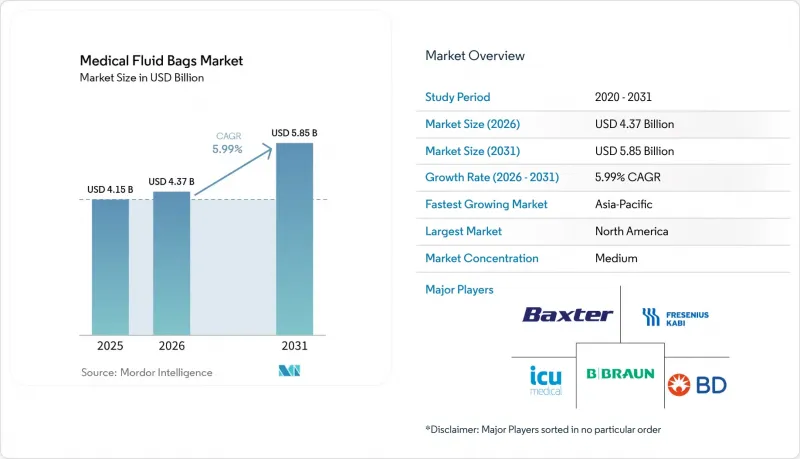

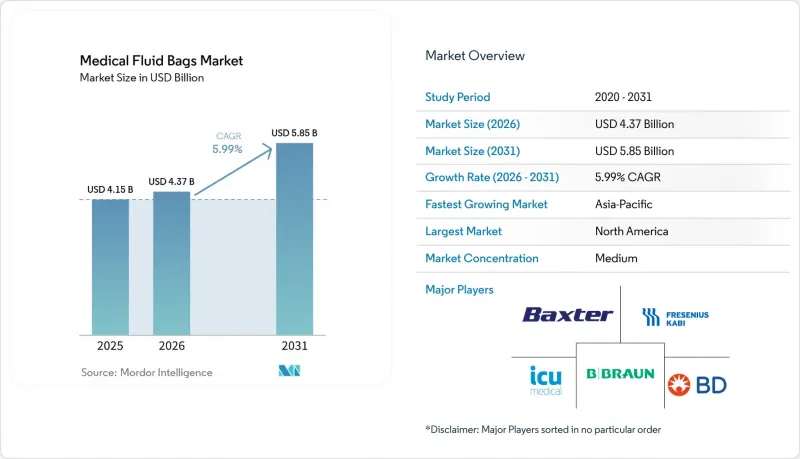

Mordor Intelligence에 의하면, 의료용 수액백 시장 규모는 2025년 41억 5,000만 달러, 2026년 43억 7,000만 달러에서 2031년까지 58억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.99%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(수액백 등), 소재(DEHP 가소화 PVC 및 DEHP 무첨가 등), 용량(250ml 이하 등), 챔버 유형(싱글 챔버 등), 최종 사용자(병원 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 의료용 수액백 시장 동향 및 분석

수술 건수 증가와 만성 질환으로 인한 부담 증가로 인해, 정맥 주사 요법, 수혈 및 투석 이용이 증가하고 있습니다.

의료용 수액백 시장은 관리형 수액 요법, 투석액 및 혈액 성분 수혈이 필요한 만성 질환의 지속적인 증가에 힘입어 계속해서 성장하고 있습니다. 병원과 외래 진료 센터는 시술 중 및 시술 후 확실한 정맥 내 수분 공급과 전해질 관리에 의존하고 있으며, 이것이 모든 의료 현장에서 매일 소비되는 수액백의 기초를 뒷받침하고 있습니다. 외래 및 재택 환경에서의 투석 및 수액 요법의 확대는 투여 과정을 간소화하는 표준화된 백 형태와 내구성이 뛰어난 커넥터의 이용 사례를 늘리고 있습니다. 치료가 회복 과정의 초기 단계로 접어들면서, 약물 위원회와 임상 팀은 투약 오류를 줄이고 병상 옆 업무 흐름을 신속하게 하기 위해 키트 및 표시 기준을 표준화하고 있습니다. 상환 정책은 여전히 사용 패턴을 결정하는 강력한 요인으로 작용하며, 상환 규정이 병원 외 치료를 우대하는 경우, 제품 설계를 간병인이 사용하기 편리하도록 맞춘 공급업체가 의료용 수액백 시장에서 점유율을 확대하는 경향을 보입니다.

외래 수술과 재택 간호의 확대가 유연하고 가벼운 가방형 제품에 대한 수요를 이끌고 있습니다.

외래 수술 증가는 단기 입원 회복 치료 및 당일 안전한 퇴원 절차에 통합할 수 있는 가볍고 휴대성이 뛰어난 프리필드 시스템에 대한 수요를 이끌고 있습니다. 재택 수액 요법 및 장기 간호 서비스의 확대에 따라, 비의료인 간병인도 무균성을 해치지 않고 다룰 수 있는 안전한 포트와 색상 구분, 명확한 용량 표시를 갖춘 유연한 디자인을 선호하는 경향이 있습니다. 이러한 설계상의 선호에 따라, 재택 간호용 제품군에서 일반적으로 사용되는 펌프나 중력식 세트와의 호환성을 유지하면서, 변조 방지 기능을 강화하고 역류를 줄이는 방식의 채택이 확대되고 있습니다. 라벨의 가시성을 높이고 직관적인 커넥터를 채택하는 의료기기 제조업체는 교대 근무를 하는 직원이나 가족 간병인의 교육 시간을 단축하고 실수를 줄일 수 있습니다. 의료용 수액백 시장이 취급 및 보관 제약이 각기 다른 경증 치료 환경에 적응해 감에 따라, 이러한 변화는 용량 선택과 챔버 구성에 계속해서 영향을 미치고 있습니다.

복잡한 무균 제조, 검증 및 규제 준수가 비용과 시장 출시까지의 시간을 늘리고 있습니다.

무균 장벽의 무결성 및 공정 검증에 대한 요구 사항은 신제품 도입이나 라인 변경에 추가적인 비용과 시간을 소요시켜 상용화를 지연시킬 가능성이 있습니다. 포장 검증 및 밀봉 성능 적합성 평가는 재료, 설비 또는 공정 매개변수가 변경될 때마다 재시험이 필요하며, 문서화나 시험 조건의 미비 사항은 출시 전 시정 조치를 초래할 수 있습니다. 동시에, 에틸렌옥사이드(EtO) 멸균에 관한 새로운 배출 기준으로 인해, 영구적인 완전 밀폐 장치나 연속 모니터링 등의 제어 기능을 추가하기 위한 설비 투자가 필요하게 되며, 이는 연구개발(R&D) 예산을 압박하고, 설치 기간 동안 생산 처리량을 저하시킵니다. 여러 사업장을 보유한 제조업체의 경우, 단계적인 개조를 통해 시스템 전체의 위험은 줄어들지만, 업그레이드를 위해 멸균 챔버의 가동이 중단되기 때문에 국부적인 병목 현상은 여전히 발생합니다. 이러한 현실로 인해 의료용 수액백 시장에서 중소기업의 규정 준수 달성 장벽이 높아지고 있으며, 확립된 품질 관리 시스템과 멸균 파트너십을 갖춘 기업이 유리한 입장에 서 있습니다.

부문별 분석

의료용 수액백 시장에서 정맥 내 수액백은 응급, 외과 및 수액 치료 현장에서 수분 공급 및 전해질 관리의 표준 수단으로서 2025년에 42.90%의 시장 점유율을 차지했습니다. 이러한 기반을 바탕으로, 생산 라인 가동률은 안정적으로 유지되는 한편, 틈새 카테고리는 치료 프로토콜에 부합하는 전문적인 역할로 성장하고 있습니다. 표준화된 멀티챔버 형식을 기반으로 한 비경구 영양 백은 임상팀이 조제 과정을 ‘사용 준비 완료형’ 디자인으로 통합함으로써 실수 위험과 준비 시간을 줄일 수 있기 때문에 연평균 성장률(CAGR) 7.34%로 성장할 것으로 전망됩니다. 병원에서는 지질, 아미노산, 포도당을 위한 통합 구획을 표준화하고 있으며, 이를 통해 투여 효율이 향상되고 병상에서의 투여 절차도 간소화됩니다. 채혈 및 보관 백은 혈액 성분 처리와 재고 관리에 여전히 필수적인 역할을 하고 있으며, 투석액 백과 요도 배액 백은 입원 및 재택 환경에서의 만성기 치료 과정에 적합합니다.

의료용 수액백 시장은 검증된 품질 시스템과 일관된 공급 실적을 중시하는 조달 경향을 반영하고 있으며, 이는 전 세계적인 제조 및 서비스 네트워크를 갖춘 기존 기업들에게 유리하게 작용하고 있습니다. 장내 영양 주머니와 수술용 배액 주머니는 일회 사용이 필수적인 종양학, 소화기내과, 수술 후 관리와 같은 분야에서 특정한 역할을 수행하고 있습니다. 구매자는 변경 관리에 따른 부담을 최소화하기 위해 라벨의 명확성, 무단 개봉 방지 스티커, 그리고 기존 펌프 및 부속품과의 호환성을 중요하게 여깁니다. 포장 및 무균 장벽에 대한 검증은 제품 전환 시 여전히 걸림돌로 작용하고 있으며, 이로 인해 바쁜 병원 약국의 변경 속도가 더뎌지고 있습니다. 예측 기간 동안 의료용 수액백 시장에서는 감염 관리 및 서비스 비용에 대응하기 위한 TPN 키트의 도입이 지속될 것으로 보이지만, 기존의 정맥 주입 솔루션은 모든 의료 현장에서 일상적인 수액 요법의 기반으로서 계속 자리매김할 것입니다.

의료용 수액백 시장에서 DEHP 가소화형 및 DEHP 무첨가형 PVC는 모두 오랜 기간에 걸친 임상 실적과 밀봉재와의 호환성이 용이하다는 점 덕분에 2025년에는 46.23%의 시장 점유율을 차지했습니다. 한편, 병원 및 국가 기관들이 낮은 추출물 함량과 민감도가 높은 환자층을 위한 프탈레이트 대체재에 중점을 두는 가운데, 폴리올레핀 다층 공압출 소재 시장은 연평균 성장률(CAGR) 8.65%로 성장할 것으로 전망됩니다. 2030년부터 캘리포니아주에서 특정 의료기기에 대한 DEHP 사용이 금지됨에 따라, 비PVC 제품 라인 계획이 가속화되고 있으며, 조달 팀은 신생아 및 산과 치료 분야에서 보다 조기 전환을 추진하고 있습니다. 또한, 임상 데이터에 따르면 대체 가소제나 폴리올레핀 기재를 사용할 경우, 지질 함유 용액으로의 용출량이 대폭 감소하는 것으로 나타났으며, 이는 생체 적합성을 우선시하는 장기적인 의사결정을 뒷받침하는 것입니다.

PVC에서 다층 PP 또는 PE로 금형 및 공정을 전환하려면 압출, 밀봉, 포트 용접을 재조정해야 하므로, 규모의 경제 효과를 얻기까지 초기 비용이 증가합니다. 화학적 호환성과 투명성이 결정적인 요소가 되는 분야에서는 EVA가 여전히 중요한 역할을 하고 있지만, 혈액 성분 처리와 같은 고부하 용도에서는 엘라스토머 블렌드나 코폴리에스테르가 사용되고 있습니다. CMR 물질을 규제하는 EU 의료기기 규정은 남아 있는 PVC 제품군에 대해 프탈레이트를 사용하지 않는 배합을 채택해야 한다는 규정 준수상의 근거를 더욱 강화하고 있습니다. 이러한 요소들을 종합해 보면, 안전성 프로파일, 규제 방향성 및 총 소유 비용(TCO) 산정을 통해 일상적인 용도부터 전문적인 용도에 이르기까지 의료용 수액백 시장의 더 큰 점유율이 폴리올레핀 및 프탈레이트를 사용하지 않는 플랫폼으로 이동하고 있습니다.

지역별 분석

2025년 북미는 의료용 수액백 시장에서 45.34%의 점유율을 차지했습니다. 이는 확립된 병원 네트워크, 민감한 환자 집단을 위한 검증된 비PVC 제품의 광범위한 도입, 그리고 단일 거점 위험에 대한 노출을 줄이기 위한 공급망 노력에 힘입은 결과입니다. 재료 제한 및 지속가능성 요건을 시행하고 있는 주들은 병원들이 프탈레이트 무사용 제품으로 전환하도록 장려하고 있으며, 캘리포니아주의 의료기기를 대상으로 한 DEHP 금지 조치는 조달 일정을 이끌어가는 대표적인 사례가 되고 있습니다. 해당 지역에서는 상업용 멸균 장치에 배기가스 제어 장치가 도입됨에 따라 단기적인 멸균 설비 개보수가 예정되어 있으며, 이러한 프로젝트로 인해 일시적인 공급 부족 상황이 발생할 가능성이 있습니다. 이를 통해 여러 거점에서의 생산 능력과 다양한 계약 멸균 파트너십의 가치가 높아집니다. 투자 결정은 공급 확보의 필요성에 따라 좌우되고 있으며, 그 결과 중요한 수액에 대한 수입 의존도를 낮추기 위해 국내에서 새로운 생산 능력을 확보하고, 정부가 목표가 명확한 지원을 실시했습니다. 이러한 요소들이 복합적으로 작용함에 따라, 의료용 수액백 시장 전반에서 계약을 수주하는 데 있어 품질 관리 체계와 납품 실적이 더욱 중요해지고 있습니다.

유럽에서는 MDR(의료기기 규정)의 시행과 화학물질 안전성 심사에 따라, 프탈레이트 에스테르가 함유된 PVC에서 규정을 준수하는 화학물질이나 폴리올레핀 다층 소재로의 전환이 점차 진행되고 있습니다. 이러한 규제에서는 추출물 및 용출물에 대한 상세한 문서화가 요구되는 경우가 많으며, 견고한 시험 프로그램과 안정성 데이터를 보유한 공급업체가 유리합니다. 조달팀은 입찰 평가 시 제품 수명 주기 전반에 걸친 환경적 영향도 고려하고 있으며, 재활용이 가능한 기판 및 첨가제 사용량을 줄인 설계에 대한 관심을 높이고 있습니다. 의료기기 제조업체들이 진화하는 기대에 부응하기 위해 제품 라인업을 갱신하는 가운데, 구매자들은 교육 및 설비 투자 부담을 줄이기 위해 기존 기기와의 하위 호환성을 중시하고 있습니다. 그 결과, 의료용 수액백 시장에서 유럽의 규정 준수 기준 및 지속가능성 우선 과제를 충족하는 제품 라인으로의 꾸준한 합리화가 진행되고 있습니다.

아시아태평양에서는 국내 제조 역량이 성숙 단계에 접어들었고, 정부가 의료 분야의 회복탄력성 강화를 위해 현지 생산을 지원하고 있는 만큼, 2031년까지 연평균 성장률(CAGR) 8.01%로 확대될 것으로 전망됩니다. 급속한 도시화가 진행되고 있는 지역에서 투석 및 영양 요법의 이용 확대는 앞으로도 생산 능력의 구성과 제품 형태에 계속 영향을 미칠 것입니다. 지역 내 각 제조업체들은 공공 및 민간 채널을 불문하고 입찰 자격을 획득하기 위해 비PVC 제품 라인을 확대하고 국제 품질 기준을 적용해 나가고 있습니다. 대국에서의 유통 모델은 여전히 결정적인 요소이며, 지역 의료 종사자들의 선호도와 물류 요건에 제품을 맞출 수 있는 기업은 시장에서 더 신속하게 입지를 다질 수 있을 것입니다. 아시아태평양의 의료용 수액백 시장은 병원 인프라에 대한 지속적인 투자와 해당 지역 내 고소득 국가에서 가정 간호 프로그램이 확산되고 있는 점으로부터도 혜택을 받고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the medical fluid bags market size is projected to expand from USD 4.15 billion in 2025 and USD 4.37 billion in 2026 to USD 5.85 billion by 2031, registering a CAGR of 5.99% between 2026 to 2031.

This report is Segmented by Product Type (Intravenous Bags, and More), Material (PVC DEHP-Plasticized and DEHP-Free, and More), Capacity (Up To 250 ML, and More), Chamber Type (Single-Chamber, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Fluid Bags Market Trends and Insights

Rising Surgical Volumes and Chronic Disease Burden Increasing IV Therapy, Transfusion and Dialysis Utilization

The medical fluid bags market continues to benefit from the persistent rise in chronic conditions that require controlled fluid therapy, dialysis solutions, and blood component transfusions. Hospitals and outpatient centers depend on reliable IV hydration and electrolyte management during and after procedures, which sustains the baseline for daily bag consumption across care settings. Growth in dialysis and infusion therapy in ambulatory and home environments expands the use cases for standardized bag formats and durable connectors that simplify administration. As care shifts earlier in the recovery pathway, formulary committees and clinical teams are standardizing kits and labeling conventions to reduce administration errors and speed bedside workflows. Reimbursement policy remains a strong determinant of use patterns, and when reimbursement rules favor out-of-hospital care, suppliers that align product design to caregiver ease-of-use tend to gain share within the medical fluid bags market.

Expansion of Ambulatory Surgery and Home-Care Shifting Demand to Flexible, Lightweight Bag Formats

Ambulatory surgery growth drives demand for lightweight, portable, prefilled systems that can integrate into short-stay recovery and safe discharge protocols the same day. Home infusion and long-term care growth favor flexible designs with secure ports, color coding, and clear volume markings that non-clinical caregivers can handle without compromising asepsis. These design preferences lift adoption of formats that enhance tamper evidence and reduce backflow while maintaining compatibility with pumps and gravity sets common in home-care inventory. Device makers that improve clarity of labels and implement intuitive connectors reduce training time and errors for rotating staff and family caregivers. This shift continues to influence capacity choices and chamber configurations as the medical fluid bags market adapts to lower-acuity care settings with different handling and storage constraints.

Complex Sterile Manufacturing, Validation and Regulatory Compliance Raising Cost and Time-to-Market

Sterile barrier integrity and process validation expectations add cost and time to new product introductions and line changes, which can delay commercialization. Packaging validations and seal performance qualifications drive repeat testing whenever materials, equipment, or process parameters change, and gaps in documentation or challenge conditions can prompt remediation before release. In parallel, new emission limits for EtO sterilization require capital projects to add controls like permanent total enclosures and continuous monitoring, which diverts budgets from R&D and slows throughput during installation. For multi-site manufacturers, staggered retrofits reduce systemic risk, but local bottlenecks still occur as chambers go offline for upgrades. These realities raise the compliance threshold for smaller firms and favor players with established quality systems and sterilization partnerships in the medical fluid bags market.

Other drivers and restraints analyzed in the detailed report include:

- Material Shift to Non-PVC, DEHP-Free Formats Accelerating Replacement Demand in Mature Markets

- Aging Population Elevating Incidence of Urinary Incontinence and Transfusion Needs

- PVC Disposal and Leachables Scrutiny and Resin Price Volatility Pressuring Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intravenous bags commanded 42.90% share in 2025 as the default modality for hydration and electrolyte management across emergency, surgical, and infusion settings in the medical fluid bags market. This foundation keeps line utilization steady while niche categories grow into specialized roles aligned to therapy protocols. Parenteral nutrition bags, supported by standardized multi-chamber formats, are projected to grow at 7.34% CAGR as clinical teams consolidate compounding steps into ready-to-activate designs that cut error risk and preparation time. Hospitals standardize around integrated compartments for lipids, amino acids, and glucose, which also improve distribution efficiency and simplify bedside activation procedures. Blood collection and storage bags remain essential to component processing and inventory management, while dialysis solution and urinary drainage bags align to chronic-care pathways in inpatient and home settings.

The medical fluid bags market reflects procurement preferences that reward validated quality systems and consistent delivery performance, which supports incumbents with global manufacturing and service footprints. Enteral feeding and surgical drainage bags play targeted roles tied to oncology, gastroenterology, and post-surgical care where single-use norms remain non-negotiable. Buyers emphasize labeling clarity, tamper-evident seals, and compatibility with existing pumps and accessories to minimize change-management overhead. Packaging and sterile barrier validations remain a gating factor for product switch-outs, which tempers the speed of change in busy hospital pharmacies. Over the forecast period, the medical fluid bags market will likely see continued adoption of TPN kits that address infection control and cost-to-serve, while legacy IV solutions continue to anchor everyday fluid therapy across care settings.

PVC, both DEHP-plasticized and DEHP-free variants, held 46.23% share in 2025 due to long clinical familiarity and straightforward seal compatibility in the medical fluid bags market. At the same time, polyolefin multilayer co-extrusions are projected to grow at 8.65% CAGR as hospitals and national bodies emphasize low-extractables profiles and alternatives to phthalates in sensitive populations. California's ban of DEHP in specified medical devices beginning 2030 intensifies planning for non-PVC lines, with procurement teams pushing earlier conversions in neonatal and maternal care pathways. Clinical data also show far lower migration into lipid-containing solutions when alternative plasticizers or polyolefin substrates are used, which supports long-horizon decisions that prioritize biocompatibility.

Tooling and process transitions from PVC to multilayer PP or PE demand recalibration of extrusion, sealing, and port welding, which raises upfront costs before scale benefits arrive. EVA retains a role where chemical compatibility and clarity are decisive, while elastomeric blends and copolyesters see use in high-stress applications like blood component processing. EU device rules that restrict CMR substances add to the compliance case for non-phthalate formulations within the remaining PVC cohort. Taken together, safety profiles, regulatory direction, and total cost-of-ownership calculations are moving a larger share of the medical fluid bags market toward polyolefin and non-phthalate platforms across routine and specialty applications.

Geography Analysis

North America held 45.34% share of the medical fluid bags market in 2025, supported by entrenched hospital networks, broad adoption of validated non-PVC lines for sensitive patient groups, and supply-chain initiatives that reduce exposure to single-site risk. States that implement material restrictions and sustainability requirements are nudging hospitals toward phthalate-free options, and California's device-focused DEHP ban is a visible example guiding procurement calendars. The region faces near-term sterilization retrofit activity as commercial sterilizers install emissions controls, and these projects can create temporary allocation environments that increase the value of multi-site capacity and diversified contract sterilization partnerships. Investment decisions are shaped by the need for supply assurance, which has led to new onshore capacity commitments and targeted government support to reduce import dependence for critical fluids. These elements together reinforce the role of quality systems and delivery performance in contract awards across the medical fluid bags market.

In Europe, MDR enforcement and chemical safety reviews reinforce a gradual pivot away from phthalate-containing PVC toward compliant chemistries and polyolefin multilayers. These regulations often require deeper documentation on extractables and leachables, which favors suppliers with robust testing programs and stability data. Procurement teams also weigh lifecycle environmental impacts in tender scoring, stimulating interest in recyclable substrates or designs with reduced additive loadings. With device-makers updating portfolios to meet evolving expectations, buyers place value on backward compatibility with existing hardware to limit training and capital needs. The overall effect is a steady rationalization of product lines to those that meet European compliance norms and sustainability priorities within the medical fluid bags market.

Asia-Pacific is projected to expand at 8.01% CAGR through 2031 as domestic manufacturing capacity matures and governments support local production to strengthen healthcare resilience. Expanded dialysis use and nutrition therapy in fast-urbanizing centers will continue to influence capacity mixes and product formats. Regional producers are scaling non-PVC lines and applying international quality frameworks to qualify for tenders across public and private channels. Distribution models in large countries remain decisive, and players that match product to regional clinician preferences and logistics requirements can gain quicker traction. The medical fluid bags market in Asia-Pacific also benefits from ongoing investment in hospital infrastructure and the spread of home-care programs in higher-income economies within the region.

- Amsino International, Inc.

- B. Braun

- Baxter

- Beckton Dickinson

- Cardinal Health

- Coloplast

- Convatec

- Fresenius

- Grifols

- ICU Medical

- JW Life Science Corp.

- MacoPharma

- Medline Industries

- Nipro

- Otsuka

- Poly Medicure Ltd.

- PolyCine GmbH

- Sippex IV Bag

- Technoflex

- Teleflex

- Terumo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising surgical volumes and chronic disease burden increasing IV therapy, transfusion and dialysis utilization

- 4.2.2 Expansion of ambulatory surgery and home-care shifting demand to flexible, lightweight bag formats

- 4.2.3 Material shift to non-PVC, DEHP-free formats accelerating replacement demand in mature markets

- 4.2.4 Aging population elevating incidence of urinary incontinence and transfusion needs

- 4.2.5 EPA 2024 EtO sterilizer standards catalyzing retooling and alternative-sterilant ready bag adoption

- 4.2.6 EU REACH/MDR phthalate (DEHP) authorization timeline driving non-PVC conversion programs

- 4.3 Market Restraints

- 4.3.1 Complex sterile manufacturing, validation and regulatory compliance raising cost and time-to-market

- 4.3.2 PVC disposal/leachables scrutiny and resin price volatility pressuring margins

- 4.3.3 Sterilization capacity constraints during EtO retrofits risk intermittent supply bottlenecks

- 4.3.4 EVA/PP resin supply concentration and tariff exposure elevating input cost risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Intravenous (IV) bags

- 5.1.2 Parenteral nutrition (TPN) bags

- 5.1.3 Enteral feeding bags

- 5.1.4 Blood collection and storage bags

- 5.1.5 Urinary drainage bags (leg, bedside)

- 5.1.6 Dialysis/peritoneal dialysis solution bags

- 5.1.7 Surgical/wound drainage and suction canister liners

- 5.1.8 Enema/irrigation bags

- 5.2 By Material

- 5.2.1 PVC (DEHP-plasticized; DEHP-free)

- 5.2.2 Polyolefin multilayer (PP/PE co-extrusions)

- 5.2.3 EVA (ethylene-vinyl acetate)

- 5.2.4 Copolyester ether (COPE)

- 5.2.5 Thermoplastic elastomers (TPU/TPE)

- 5.3 By Capacity

- 5.3.1 Up to 250 mL

- 5.3.2 250-500 mL

- 5.3.3 500-1,000 mL

- 5.3.4 Above 1,000 mL

- 5.4 By Chamber Type

- 5.4.1 Single-chamber

- 5.4.2 Dual-chamber

- 5.4.3 Triple / Multi-chamber

- 5.5 By End User

- 5.5.1 Hospitals (tertiary/community)

- 5.5.2 Ambulatory surgical centers

- 5.5.3 Blood banks / transfusion centers

- 5.5.4 Home healthcare / long-term care

- 5.5.5 Clinics & physician offices

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Amsino International, Inc.

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Baxter International Inc.

- 6.3.4 Becton, Dickinson and Company (BD)

- 6.3.5 Cardinal Health

- 6.3.6 Coloplast A/S

- 6.3.7 ConvaTec Group PLC

- 6.3.8 Fresenius Kabi AG

- 6.3.9 Grifols S.A.

- 6.3.10 ICU Medical, Inc.

- 6.3.11 JW Life Science Corp.

- 6.3.12 Macopharma

- 6.3.13 Medline Industries, LP

- 6.3.14 Nipro Corporation

- 6.3.15 Otsuka Pharmaceutical Co., Ltd.

- 6.3.16 Poly Medicure Ltd.

- 6.3.17 PolyCine GmbH

- 6.3.18 Sippex IV Bag

- 6.3.19 Technoflex

- 6.3.20 Teleflex Incorporated

- 6.3.21 Terumo Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment