|

시장보고서

상품코드

2063550

의료용 콜드체인 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare Cold Chain - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

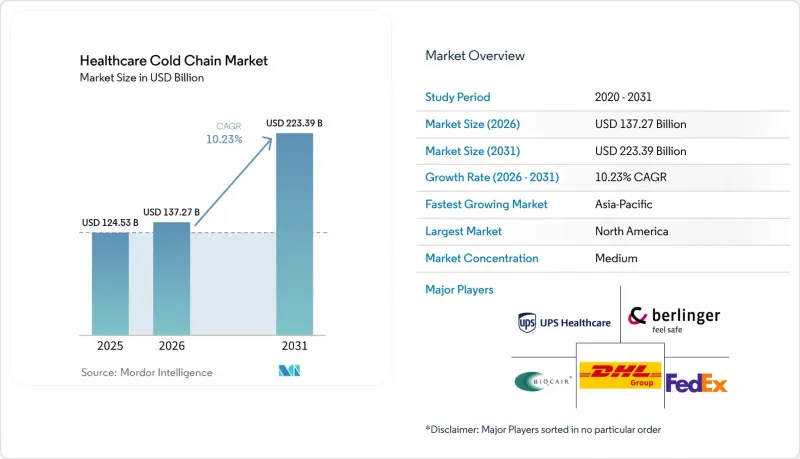

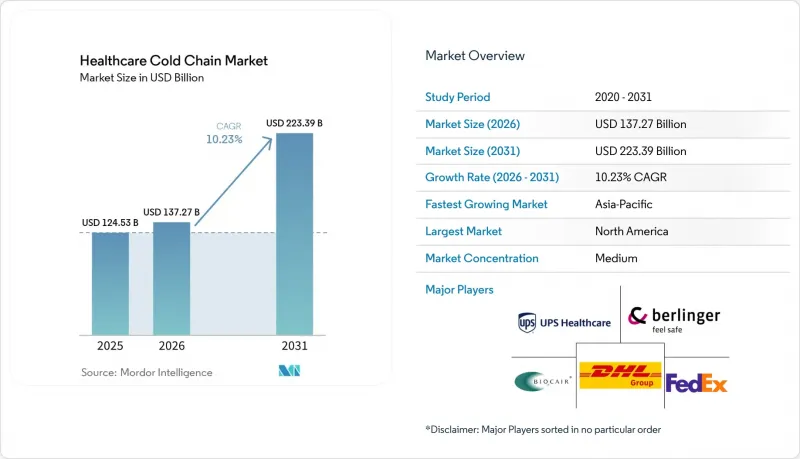

Mordor Intelligence에 의하면, 의료용 콜드체인 시장 규모는 2025년 1,245억 3,000만 달러로 평가되었습니다. 2026년 1,372억 7,000만 달러에서 2031년까지 2,233억 9,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.23%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(백신, 바이오의약품, 임상시험용 시료, 혈액·혈장 제제, 세포 및 유전자 치료), 서비스 유형(운송, 보관·창고, 기타), 최종 사용자(제약 및 바이오의약품 기업, 병원·의료 제공업체, 기타), 지역(북미, 유럽, 기타)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계의 의료용 콜드체인 시장 동향 및 인사이트

바이오의약품 및 전문의약품 수요 증가로 콜드체인 인프라 구축이 가속화되고 있습니다.

2018년부터 2023년까지 승인된 의약품의 43%가 냉장 또는 냉동 보관이 필요했던 점을 고려할 때, 바이오의약품은 현재 의료용 콜드체인 시장에서 투자 우선순위로 자리 잡고 있습니다. 이에 따라 충전 및 마무리 공정부터 라스트 마일까지 운영상의 엄격함이 요구되고 있습니다. 온도 편차는 단백질 기반 치료제의 품질을 저하시킬 가능성이 있으므로, 검증된 보관 및 운송 경로의 적합성 평가와 지속적인 온도 모니터링은 제품의 무결성과 환자의 안전을 지키는 데 있어 매우 중요합니다. USP 1079와 같은 규정 준수 체계는 보관 및 운송 과정에서의 위험 기반 관리를 강화하고, 최악의 상황을 반영한 견고한 성능 적합성 평가를 요구하고 있습니다. WHO의 백신 포장 및 운송 지침과 PQS 장비 사양 또한 의료용 콜드체인 시장의 국제 운송을 위한 장비 선정, 인수 시험, 운송 경로 절차에 반영되어 있습니다. 이에 발맞추어 포장 분야에 대한 투자도 확대되고 있으며, 업계 공급업체들은 더욱 엄격한 적합성 기준을 준수하는 단열 운송 용기, 상변화 소재, 진공 단열 패널 분야에서 수년에 걸쳐 꾸준한 성장이 이어지고 있다고 보고하고 있습니다. 바이오의약품 파이프라인이 지속적인 보충 주기, 더 광범위한 지리적 유통, 제조업체 및 3PL(제3자 물류업체) 전반에 걸친 더욱 엄격한 규정 준수 기준을 유지하고 있기 때문에 의료용 콜드체인 시장은 이러한 변화의 혜택을 누리고 있습니다.

전 세계 백신 보급 확대가 분산형 콜드체인 네트워크를 견인하고 있습니다.

예방접종 프로그램의 확대가 의료용 콜드체인 시장을 재편하고 있습니다. Gavi의 지원을 받는 국가들에서는 2024년에 7,200만 명의 어린이들이 보호받았으며, 2억 5,500만 달러의 공동 자금 조달을 기록했습니다. 이는 백신 예산에 대한 각국의 지속적인 자율성을 보여주는 것입니다. 저소득 국가에서의 HPV 백신 접종률은 2019년 3%에서 2024년에는 25%로 상승했으며, 2024년에는 3,260만 명의 소녀가 예방접종을 받아 전년도보다 2배 이상 증가했습니다. 이로 인해 지방 차원의 냉장 운송 및 보관에 대한 수요가 증가하고 있습니다. Gavi는 또한 2024년 홍역 및 DTP3 예방접종률에 대한 진전 상황을 보고했으나, 여전히 예방접종을 받지 못한 어린이들이 있는 지역이 남아 있으며, 이는 취약한 환경이나 분쟁의 영향을 받는 지역에서 견고한 라스트 마일용 장비 및 전력 솔루션의 필요성을 여실히 보여주고 있습니다. WHO의 ‘예방접종 기본 프로그램’에서는 강제 공기 순환 기능, 백업 전원, 고온·저온 구역을 파악하기 위한 온도 매핑 기능을 갖춘 의료용 냉장고를 권장하고 있으며, 이러한 기능들은 모두 1차 의료 센터의 재고 관리 효율성을 높여줍니다. WHO의 PQS(예방접종 품질 기준)에 따른 사전 인증을 받은 태양광 직결식 백신용 냉장고 및 냉동고는 전력망이 연결되지 않은 지역에서도 신뢰할 수 있는 성능을 발휘하며, 분산형 네트워크의 에너지 복원력 확보라는 우선순위에도 부합합니다. 프로그램의 대상 범위가 확대되고 더 많은 항원이 도입됨에 따라, 특히 국가 예방접종 프로그램 및 협력 기관의 경우, 의료용 콜드체인 시장은 공급량 확대, 장비 교체, 운송 경로 확충 등의 혜택을 누리고 있습니다.

높은 운영 비용과 인프라 비용이 용량 확대를 제약하고 있습니다.

냉장 전력 소비가 창고의 주요 부하이며, 에너지 비용이 의료용 콜드체인 시장의 냉장 보관 운영 비용에서 큰 비중을 차지하기 때문에 운영 비용이 단기적인 이익률 구조에 큰 부담으로 작용하고 있습니다. 또한, 공급업체 측에서는 2019년 이후 임대료의 꾸준한 상승과 용량 부족이 보고되고 있으며, 이로 인해 보유 비용이 증가하고 기존 부동산의 네트워크 설계가 복잡해지고 있습니다. 노동력은 여전히 구조적인 부담으로 작용하고 있으며, GxP 교육을 이수한 인력이 부족하고 임금 수준이 상승함에 따라 보관 및 운송 분야에서 자동화 및 디지털 감시에 대한 의존도가 높아지고 있습니다. 온도 편차는 심각한 경제적 위험을 초래하고 있으며, 업계 관계자들의 추산에 따르면 콜드체인 문제로 인한 연간 손실이 막대하기 때문에 의료용 콜드체인 시장에서 더욱 우수한 포장, 가시성, 표준 작업의 중요성이 더욱 커지고 있습니다. 안구건조증스나 액체 질소의 조달도 운송 경로 차원에서 불안정해질 수 있으므로, 화주들은 공급을 안정화하기 위해 조달처를 다각화하고 충전 절차를 최적화하고 있습니다. 포장 사양은 보다 엄격한 인증 기준 하에서 운송 경로의 성능을 유지하기 위해 고성능 단열재 및 상변화 소재의 사용과 함께 지속적으로 발전하고 있으며, 이러한 추세는 공급업체의 지침과 고객의 검증 프로그램을 통해 뒷받침되고 있습니다.

부문별 분석

2025년, 정기 예방접종과 팬데믹 대책이 꾸준한 공급과 라스트 마일 운송을 견인한 결과, 백신은 의료용 콜드체인 시장 점유율의 37.23%를 차지했습니다. Gavi의 지원을 받는 국가들에서는 2024년에 7,200만 명의 어린이들이 보호받았으며, 사상 최대 규모의 공동 자금 조달을 달성함에 따라 각국 및 지역의 창고에서 처리량이 증가했습니다. 2024년에는 저소득 국가 전체의 HPV 백신 접종률이 25%에 달했으며, 같은 해 3,260만 명의 소녀가 백신을 접종받았습니다. 이로 인해 지역 창고와 진료소에서 2℃-8℃ 조건의 보관 용량에 대한 지속적인 수요가 확대되었습니다. WHO의 ‘예방접종 기본 프로그램’은 설비 및 운영 기준을 정하고, 가정용 냉장고에서 강제 공기 순환 기능과 비상 전원을 갖춘 의료용 등급의 장치로 업그레이드하는 방안을 제시하고 있습니다. 온도 요건은 항원의 유형에 따라 다릅니다. 대부분의 백신은 2°C-8°C에서 운송되지만, 일부 바이러스 백신은 냉동 상태로 운송되며, mRNA 제품의 경우 초저온 보관이 필요한 경우가 있으므로, 의료용 콜드체인 시장에서는 보관 라인의 설계를 제품 라벨 표시 및 적합성 증명과 일치시켜야 합니다. WHO의 PQS(사전 적격성 평가) 인증을 획득한 태양광 발전식 직결형 냉장고·냉동고는 Off-grid 지역의 서비스 연속성을 향상시키고, 가스통이나 불안정한 상용 전원에 대한 의존도를 줄여줍니다.

세포 및 유전자 치료는 승인, 후기 임상시험, 초저온 처리가 필요한 전문적인 물류 시스템에 힘입어 2031년까지 가장 급격한 성장세를 보일 전망입니다. 프로그램 확대와 시설 증설에 따라, 세포 및 유전자 치료용 의료 콜드체인 시장 규모는 2031년까지 연평균 성장률(CAGR) 10.80%로 확대될 것으로 전망됩니다. -150°C 이하의 극저온 운송에서는 다단계 인증, GPS 추적, ‘배치 오브 원(Batch of One)’ 워크플로우에서 혼동을 방지하기 위한 신원 체인 관리 기능을 갖춘 액체 질소 드라이 쉬퍼가 필수적입니다. 상업 운송은 1회 운송당 가치가 높기 때문에 의료용 콜드체인 시장의 위험 완화 조치의 일환으로, 이 플레이북에서는 듀어, 운송 경로, 운송업체에 대한 중복성을 중시하고 있습니다. 2025년 6월 Cryoport가 CRYOPDP를 DHL에 매각함에 따라 전문 택배 업체의 사업 범위가 확대된 동시에, Cryoport는 통합형 재생의료 서비스 및 보관 업무에 집중할 수 있게 되었으며, CGT(세포 및 유전자 치료) 고객을 위한 네트워크 선택지도 강화되었습니다. 후기 임상시험이 진행 중이므로, 제품화가 진행됨에 따라 제조 거점, 치료 센터, 지역 물류 센터와 연계된 검증된 초저온 운송 네트워크에 대한 수요가 높아질 것으로 보입니다.

지역별 분석

북미는 바이오의약품 제조 분야에서 미국의 주도적 입지, FDA 규정을 준수하는 견고한 컴플라이언스 체계, IoT를 활용한 가시화 기술의 광범위한 도입에 힘입어 2025년 의료 콜드체인 시장의 38.60%를 차지했습니다. 이 지역은 물류 센터, 의료 전용 차량, 의료 콜드체인 시장에서 CGT 및 바이오의약품 포트폴리오의 복잡성에 부합하는 전문적인 저온 운송 서비스에 대한 대규모 투자의 혜택을 누리고 있습니다. Cencora사의 10억 달러 규모의 프로그램에는 2027년 봄에 개장 예정인 오하이오주의 53만 제곱피트 규모의 전국 물류 센터와 2026년 가을에 예정된 앨라배마주의 냉장 용량 대폭 확충이 포함되어 있으며, 이를 통해 처리 능력과 회복탄력성이 향상될 것입니다. UPS 헬스케어의 Frigo Trans·BPL 인수는 범유럽 노선에서의 온도 관리 역량을 확대하고, 극저온부터 실온 관리에 이르기까지 유럽행 화물을 취급하는 북미 화주들에게 통합적인 서비스 범위를 강화할 것입니다. 실시간 가시화 및 경로 최적화에 지속적으로 주력함으로써, 각 사업자는 의료용 콜드체인 시장에서 예외 발생률을 낮추고 정시 배송률을 안정화하는 것을 목표로 하고 있습니다.

유럽은 엄격한 GDP(의약품 유통 적정 기준) 요건과 독일, 스위스, 영국에서의 바이오의약품에 대한 활발한 수요 덕분에 규정 준수를 충족하는 물류의 주요 허브로 자리매김하고 있습니다. DHL이 항공 화물 콜드체인 네트워크 확장을 위해 시행하는 20억 유로(11억 6,000만 달러) 규모의 프로그램에는 브뤼셀과 신시내티를 연결하는 전용 777형 화물기와, BRUcargo 내 의약품 전용 구역이 포함되어 있으며, 이를 통해 의료용 콜드체인 시장에서 미국과의 양방향 연결성이 강화될 것입니다. UPS는 Frigo Trans·BPL을 통해 유럽 내 콜드체인 역량을 확대했습니다. 이를 통해 -196°C에서 +25°C 범위를 아우르는 인증된 운송 경로와 창고가 추가되어, 인계 시 관리가 강화됩니다. Cencora는 파트너십과 2026년에 계획된 신규 시설을 통해 범유럽 물류 네트워크를 확충하고 있으며, 이를 통해 의료용 콜드체인 시장에서 전문 물류 및 임상시험용 의약품 공급에 대한 선택지가 늘어나고 있습니다. 업계의 투자 동향과 규제 조화를 바탕으로, 감사 대응 체계, 검증된 설비, 조정된 예외 처리에 주력하는 한편, 서비스 수준이 지속적으로 향상되고 있습니다.

아시아태평양은 중국과 인도의 제조업체들이 사업을 확장하는 데 더해, 싱가포르, 일본, 한국과 같은 지역 허브들이 전문 역량을 강화함에 따라 2031년까지 연평균 성장률(CAGR) 13.89%를 기록하며 지역별 가장 높은 성장률을 보일 것으로 전망됩니다. 따라서 첨단 치료 및 임상 연구를 위한 GMP 준수 보관·초저온 서비스를 갖춘 시설이 늘어남에 따라, 아시아태평양의 의료용 콜드체인 시장 규모는 확대될 전망입니다. DHL은 2030년까지 아시아태평양에 5억 유로를 투자할 계획이며, 2026년 2월에는 투아스 바이오메디컬 파크 인근에 극저온부터 상온까지의 전문적인 온도 구역을 갖춘 1,000만 유로 규모의 의약품 전용 허브를 싱가포르에 개설했습니다. 이 싱가포르 시설에는 생물학적 제제, 백신, 임상시험의 물류를 지원하는 GMP 준수 인프라가 갖춰져 있어, 의료용 콜드체인 시장에서 지역 핵심 거점으로서의 입지를 공고히 하고 있습니다. 동남아시아 각국 정부는 필리핀의 새로운 냉장 창고 건설이나 인도네시아의 태양광 발전 설비 및 원격 측정 기술을 활용한 경로 최적화 등, 용량 확대와 디지털화에 투자하고 있으며, 이를 통해 폐기 위험을 줄이고 가시성을 높이고 있습니다. WHO의 지침은 여전히 장비 선정 및 인증에 영향을 미치고 있으며, 의료용 콜드체인 시장에서 의료 시스템이 라스트 마일의 신뢰성을 높이는 데 기여하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the healthcare cold chain market size is projected to expand from USD 124.53 billion in 2025 and USD 137.27 billion in 2026 to USD 223.39 billion by 2031, registering a CAGR of 10.23% between 2026 to 2031.

This report is Segmented by Product Type (Vaccines, Biopharmaceuticals, Clinical Trial Materials, Blood & Plasma Products, and Cell & Gene Therapies), Service Type (Transportation, Storage & Warehousing, and More), End User (Pharmaceutical & Biopharma Companies, Hospitals & Healthcare Providers and More), and Geography (North America, Europe, and More). The Market and Forecasted in Terms of Value (USD).

Global Healthcare Cold Chain Market Trends and Insights

Rising Demand for Biologics and Specialty Drugs Accelerates Cold Chain Infrastructure

Biologics now anchor investment priorities in the healthcare cold chain market as 43% of drugs approved over 2018 2023 required refrigerated or frozen handling, which raises operating rigor from fill finish to last mile. Temperature excursions can degrade protein-based therapies, so validated storage, lane qualification, and continuous temperature monitoring are central to protecting product integrity and patient safety. Compliance frameworks such as USP 1079 reinforce risk-based controls for storage and transportation and call for robust performance qualification that reflects worst-case conditions. WHO vaccine packaging and shipping guidance, together with PQS equipment specifications, also inform equipment choices, acceptance testing, and lane procedures for international shipments in the healthcare cold chain market. Packaging investment is scaling in response, with industry vendors reporting strong multi-year growth in insulated shippers, phase change materials, and vacuum insulated panels aligned to tougher qualification standards. The healthcare cold chain market benefits from this shift since biologics pipelines sustain recurring replenishment cycles, wider geographic distribution, and tighter compliance baselines across manufacturers and 3PLs.

Global Vaccine Expansion Drives Distributed Cold Chain Networks

Expanded immunization programs are reshaping the healthcare cold chain market as Gavi-supported countries protected 72 million children in 2024 and recorded USD 255 million in co-financing, which signals durable national ownership of vaccine budgets. HPV coverage in lower-income countries rose from 3% in 2019 to 25% in 2024, with 32.6 million girls immunized in 2024, more than double the prior year, which increases demand for refrigerated transport and storage at subnational levels.Gavi also reported progress on measles and DTP3 coverage in 2024, though pockets of zero-dose children remain, which underscores the need for resilient last-mile equipment and power solutions in fragile and conflict-affected settings. WHO's Essential Program on Immunization recommends medical-grade refrigerators with forced air circulation, backup power, and temperature mapping to identify hot and cold spots, all of which improve inventory integrity in primary health centers. WHO PQS prequalified solar direct drive vaccine refrigerators and freezers offer reliable performance in off-grid locations and align with energy resilience priorities in distributed networks. As programs widen coverage and introduce more antigens, the healthcare cold chain market gains from scaled replenishment, upgraded equipment fleets, and broader transport lanes, especially for national immunization programs and partners.

High Operational and Infrastructure Costs Constrain Capacity Expansion

Operating costs weigh on near-term margin structure as refrigeration power is the dominant warehouse load, and energy expenses make up a large share of cold storage operating costs for the healthcare cold chain market. Vendors also report steady rent inflation and capacity tightness since 2019, which lifts carrying costs and complicates network design in legacy real estate. Labor remains a structural pressure where GxP-trained roles are scarce, and wage rates rise, which increases dependence on automation and digital monitoring in storage and in transit. Temperature excursions impose major economic risk as industry sources estimate significant annual losses from cold chain failures, which reinforces the case for better packaging, visibility, and standard work in the healthcare cold chain market. Dry ice and liquid nitrogen procurement can also be volatile at the corridor level, so shippers diversify sources and optimize charging protocols to stabilize supply. Packaging specifications continue to evolve with the use of high-performance insulation and phase change materials to hold lane performance under more stringent qualification regimes, a trend reinforced by supplier guidance and customer validation programs.

Other drivers and restraints analyzed in the detailed report include:

- IoT, Real Time Visibility, and Predictive Analytics Transform Passive Monitoring into Active Intervention

- Cell and Gene Therapy Scale Up Requires ULT and Cryogenic Networks

- Regulatory Complexity and Fragmented Compliance Standards Elevate Administrative Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vaccines accounted for 37.23% of the healthcare cold chain market share in 2025 as routine immunization and pandemic preparedness drove steady replenishment and last-mile traffic. Gavi-supported countries protected 72 million children in 2024 and achieved record co-financing, which boosted volumes across countries and subnational warehouses. HPV coverage climbed to 25% in 2024 across lower-income countries, with 32.6 million girls vaccinated that year, which widened recurring demand for 2°C to 8°C capacity in district stores and clinics. WHO's Essential Program on Immunization frames equipment and operating standards and guides the upgrade path from domestic fridges to medical-grade units with forced air circulation and backup power. Temperature requirements differ by antigen class as most vaccines ship at 2°C to 8°C while some viral vaccines ship frozen, and mRNA products may need ultra cold lanes, so lane design must align with product label and qualification evidence in the healthcare cold chain market. WHO PQS prequalified solar direct drive refrigerators and freezers improve service continuity in off-grid areas and reduce dependence on bottled gas or unstable mains power.

Cell and gene therapies post the steepest growth trajectory through 2031, supported by approvals, late stage trials, and specialized logistics that require cryogenic handling. The healthcare cold chain market size for cell and gene therapies is projected to expand at a 10.80% CAGR through 2031 as programs scale and more centers come online. Cryogenic shipping under -150°C relies on liquid nitrogen dry shippers with multilayer qualification, GPS tracking, and chain of identity controls to eliminate mix ups in batch of one workflows. Commercial shipments carry high value per movement, so playbooks emphasize redundancy on dewars, lanes, and carriers as part of risk mitigation in the healthcare cold chain market. Cryoport's sale of CRYOPDP to DHL in June 2025 broadened the specialty courier footprint while allowing Cryoport to focus on integrated regenerative medicine services and storage, and it strengthened network options for CGT customers. With more late phase trials in flight, commercial launches will add to demand for validated cryogenic networks that integrate with manufacturing sites, treatment centers, and regional depots.

Geography Analysis

North America holds 38.60% of the 2025 healthcare cold chain market, supported by U.S. leadership in biologics manufacturing, strong FDA-aligned compliance practices, and broad adoption of IoT visibility. The region benefits from large-scale investments across distribution centers, dedicated healthcare fleets, and specialized cryogenic services that match the complexity of CGT and biologics portfolios in the healthcare cold chain market. Cencora's USD 1 billion program includes a 530,000 square foot national distribution center in Ohio that is scheduled for spring 2027 and a large increase in refrigerated capacity in Alabama scheduled for fall 2026, which lifts throughput and resilience. UPS Healthcare's acquisitions of Frigo Trans and BPL expand temperature-controlled capabilities within Pan European corridors and reinforce integrated coverage for North American shippers with Europe-bound flows, ranging from cryogenic to controlled room temperatures. With continued emphasis on real-time visibility and route optimization, operators aim to compress exception rates and stabilize on-time performance in the healthcare cold chain market.

Europe is a major hub for compliant distribution due to rigorous GDP expectations and strong biologics consumption across Germany, Switzerland, and the United Kingdom. DHL's EUR 2 billion (USD 1.16 billion) program to expand its airfreight cold chain network includes a dedicated 777 freighter between Brussels and Cincinnati and pharma only zones at BRUcargo, which enhances bidirectional connectivity with the United States in the healthcare cold chain market. UPS expanded its European cold chain capability via Frigo Trans and BPL, which adds certified lanes and warehousing that span -196°C to +25°C and tightens control across handoffs. Cencora is improving its Pan European logistics footprint through partnerships and new facilities planned for 2026, which increases options for specialty distribution and trial supply in the healthcare cold chain market. Industry investment patterns and regulatory alignment continue to raise service standards while keeping focus on audit readiness, validated equipment, and orchestrated exception handling.

Asia Pacific is projected to post the fastest regional growth rate at a 13.89% CAGR through 2031 as manufacturers scale in China and India and as regional hubs in Singapore, Japan, and South Korea add specialized capacity. The healthcare cold chain market size in Asia Pacific is therefore set to expand as more facilities come online with GMP compliant storage and cryogenic services for advanced therapies and clinical research. DHL allocated EUR 500 million for Asia Pacific through 2030 and opened a EUR 10 million dedicated pharmaceutical hub in Singapore in February 2026 with specialized temperature zones from cryogenic to ambient near Tuas Biomedical Park. The Singapore facility includes GMP compliant infrastructure that supports biologics, vaccines, and clinical trial logistics, which strengthens a regional anchor for the healthcare cold chain market. Governments in Southeast Asia are investing in capacity and digitalization, including new cold stores in the Philippines and route optimization with solar powered equipment and telemetry in Indonesia, which reduce spoilage risk and raise visibility. WHO guidance continues to shape equipment selection and qualification, helping health systems raise last mile reliability in the healthcare cold chain market.

- Berlinger & Co. AG

- Biocair International Ltd.

- Cencora, Inc.

- CEVA Logistics AG

- Controlant ehf.

- Cryoport, Inc.

- DHL Group (Deutsche Post AG)

- DSV A/S

- ELPRO?BUCHS AG

- FedEx Corporation

- Kerry Logistics Network Limited

- Kuehne+Nagel International AG

- Nippon Express Holdings, Inc.

- Sensitech (Carrier)

- SF Express Co., Ltd.

- UPS Healthcare (United Parcel Service, Inc.)

- Yusen Logistics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Biologics and Specialty Drugs

- 4.2.2 Global Vaccine Expansion and Immunization Programs

- 4.2.3 Growth of Clinical Trials and Decentralized/Direct-To-Patient Logistics

- 4.2.4 Technological Advancements in IoT, Real-Time Visibility, and Analytics

- 4.2.5 Sustainability Mandates Reshaping Procurement and Packaging

- 4.2.6 Cell & Gene Therapy Scale-Up Requiring ULT/Cryogenic Networks

- 4.3 Market Restraints

- 4.3.1 High Operational and Infrastructure Costs

- 4.3.2 Regulatory Complexity and Compliance Burden

- 4.3.3 Dry ice/LN2 Supply Volatility and Cost Shocks

- 4.3.4 Certified Lane/Airport Capacity Bottlenecks for Pharma Air Cargo

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Vaccines

- 5.1.2 Biopharmaceuticals

- 5.1.3 Clinical Trial Materials

- 5.1.4 Blood & Plasma Products

- 5.1.5 Cell & Gene Therapies

- 5.2 By Service Type

- 5.2.1 Transportation

- 5.2.2 Storage & Warehousing

- 5.2.3 Packaging solutions

- 5.2.4 Monitoring & tracking systems

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biopharma Companies

- 5.3.2 Hospitals & Healthcare Providers

- 5.3.3 Research & Academic Institutes

- 5.3.4 CROs / Clinical Trial Organizations

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Berlinger & Co. AG

- 6.3.2 Biocair International Ltd.

- 6.3.3 Cencora, Inc.

- 6.3.4 CEVA Logistics AG

- 6.3.5 Controlant ehf.

- 6.3.6 Cryoport, Inc.

- 6.3.7 DHL Group (Deutsche Post AG)

- 6.3.8 DSV A/S

- 6.3.9 ELPRO?BUCHS AG

- 6.3.10 FedEx Corporation

- 6.3.11 Kerry Logistics Network Limited

- 6.3.12 Kuehne+Nagel International AG

- 6.3.13 Nippon Express Holdings, Inc.

- 6.3.14 Sensitech (Carrier)

- 6.3.15 SF Express Co., Ltd.

- 6.3.16 UPS Healthcare (United Parcel Service, Inc.)

- 6.3.17 Yusen Logistics Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment