|

시장보고서

상품코드

2063551

헬스케어 스마트 라벨 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare Smart Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

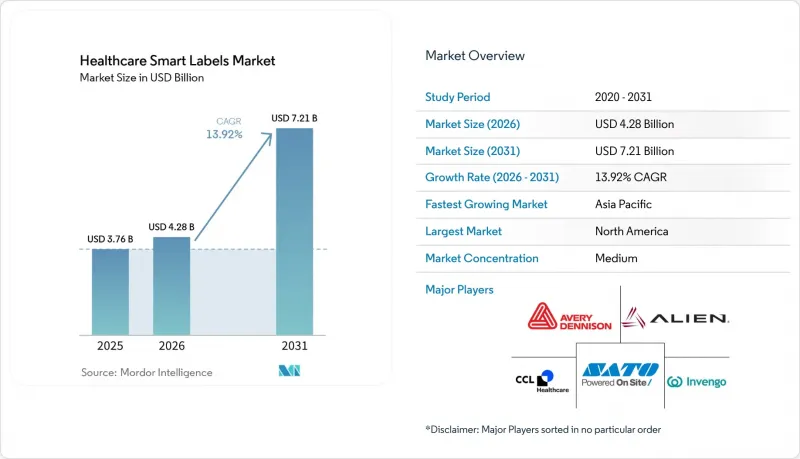

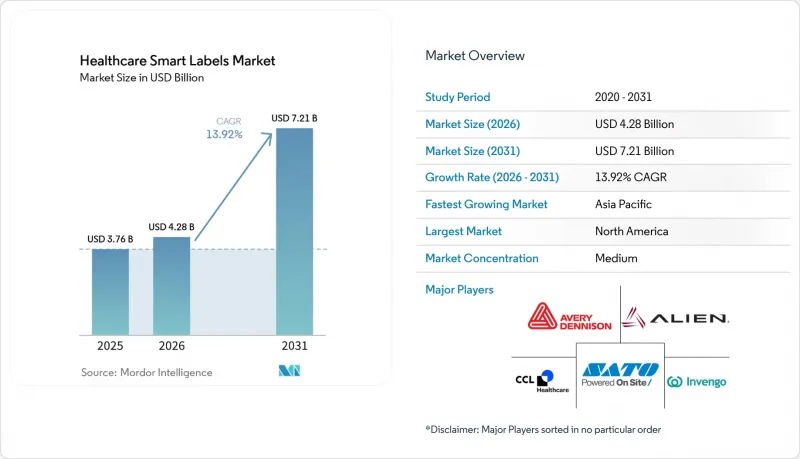

Mordor Intelligence에 의하면, 헬스케어 스마트 라벨 시장 규모는 2025년 37억 6,000만 달러로 평가되었습니다. 2026년 42억 8,000만 달러에서 2031년까지 72억 1,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 13.92%를 나타낼 것으로 예측됩니다.

본 보고서는 기술별(RFID 라벨, NFC(고주파) 태그 등), 구성 요소별(배터리, 마이크로프로세서/IC, 송수신기, 센서, 메모리), 용도별(의약품 추적·일련번호 부여, 콜드체인 모니터링 등), 최종 사용자별(병원, 제약회사 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계의 헬스케어 스마트 라벨 시장 동향 및 인사이트

DSCSA/EU FMD의 일련번호 부여 의무화가 품목별 라벨링을 가속화

미국과 유럽의 시리얼화 요건으로 인해 품목 단위 라벨링 수요가 계속해서 증가하고 있습니다. DSCSA는 상호 운용 가능한 전자 추적 시스템을 중시하는 반면, EU의 FMD는 EMVS를 통한 포장 단위 검증에 의존하고 있습니다. DSCSA의 강화된 유통 보안 프레임워크에서는 거래 파트너들이 일련번호가 부여된 데이터를 교환하고 의심스러운 제품을 조사할 것을 요구하고 있으며, 이에 따라 제약사와 유통업체들은 단품 포장 및 케이스에 대한 바코드 및 RFID 기반 식별자의 표준화를 추진하고 있습니다. EU에서는 FMD 아키텍처에 따라 처방약에 고유 식별자와 위조 방지 장치가 도입되어 있으며, 병원 약국을 포함한 조제 시설에서의 검증 과정에서 기계 판독이 가능한 2차원 데이터 매트릭스 라벨이 표준으로 자리 잡고 있습니다. 기업들이 규정 준수를 유지하기 위해 라벨링 시스템을 업데이트하고 확장함에 따라, 이러한 요건들은 헬스케어 스마트 라벨 시장에 견고한 기반을 마련하고 있습니다. 상호 운용 가능한 데이터를 향한 운영상의 추진은 EPCIS 기반의 데이터 교환과도 부합하며, 그 결과 기업 시스템과 원활하게 통합할 수 있는 시리얼화된 바코드나 RAIN RFID가 선호되고 있습니다.

제약 업계에서 위조 방지 및 유용 방지의 우선순위

제약 업계의 이해관계자들은 스마트 라벨을 활용하여 위조를 방지하고, 부정 유통을 감지하며, 신속한 리콜을 가능하게 하고 있습니다. 여기에는 시리얼화 및 변조 방지 기능에 더해, 모바일 기반 검증 기능이 결합되어 있습니다. 보건 당국은 위조 의약품이 여전히 위협이 되고 있다고 계속 경고하고 있으며, 판매 단위별로 그리고 2차 포장에도 안전하고 스캔 가능한 라벨이 필요하다고 강조하고 있습니다. 상품 수준의 바코드와 NFC 태그는 도매업체, 제3자 물류업체, 병원 약국에 걸쳐 진위 확인 및 보관 이력 추적을 지원합니다. 이와 동시에, RFID는 창고나 의료 현장에서의 자동 재고 조사 및 위치 추적을 가능하게 하여, 고가의 치료제 재고 감소 억제 및 이상 감지에 기여합니다. 이러한 기능들이 서로 시너지를 발휘하여, 규제 대상인 전체 밸류체인 전반에 걸친 오류 및 위험 노출을 줄임으로써 헬스케어 스마트 라벨 시장을 강화합니다.

라벨 리더 소프트웨어에 이르기까지 높은 도입 및 인프라 비용

총 소유 비용에는 라벨, 인레이, 리더기, 프린터, 인코딩 및 검증 스테이션은 물론, EPCIS 이벤트의 수집 및 교환에 필요한 소프트웨어가 포함됩니다. 병원 및 의약품 유통 거점은 규정 준수를 확보하기 위한 직원 교육 및 변경 관리를 포함하여, 시스템 통합 및 프로세스 변경에 필요한 예산을 확보해야 합니다. 수동형 RFID 시스템은 장기적으로는 비용을 절감할 수 있지만, 리더기나 인프라에 대한 초기 투자는 특히 소규모 시설의 경우 여전히 걸림돌이 되고 있습니다. 배터리나 첨단 센서가 내장된 능동형 BLE 태그는 단가가 높기 때문에 ROI가 즉시 명확해지는 이용 사례의 범위가 좁아집니다. 이러한 경제적 요인으로 인해, 특히 제품의 가치 밀도가 중간 수준인 분야에서 헬스케어 스마트 라벨 시장의 도입이 지연될 가능성이 있습니다.

부문별 분석

2025년, QR 코드 및 2D 데이터 매트릭스 라벨은 헬스케어 스마트 라벨 시장에서 41.23%의 점유율을 차지하며 기술 부문 1위를 유지했습니다. 이는 병원 및 약국에서 DSCSA 및 EMVS에 대한 단위별 검증 과정에서 이러한 라벨이 핵심적인 역할을 하고 있음을 반영합니다. 2026년부터 2031년에 걸쳐 바이오의약품 및 백신의 확대에 따라, 또한 이해관계자들이 콜드체인 이동 과정에서의 단위별 상태 가시화를 간편하게 요구함에 따라, 온도 및 관련 조건을 감지하는 센싱 라벨이 연평균 성장률(CAGR) 14.65%로 가장 빠르게 성장할 것으로 예측됩니다. RAIN RFID는 의료 현장에서의 자동 계수 및 캐비닛 관리를 위해 지속적으로 확대되고 있는 반면, NFC는 인증 및 정보 접근 과정에서 환자 주도의 탭 조작을 보완하고 있습니다. EAS는 소매점이나 특수 치료를 시행하는 병원의 약국 등, 물품의 보안이 요구되는 상황에서 활용되고 있습니다. 다중 기술 전략은 여전히 보편적으로 사용되고 있으며, 임상 팀과 물류 팀은 2차원 바코드를 스캔하는 한편, 재고 관리 팀은 RFID를 통한 자동화를 실시함으로써 헬스케어 스마트 라벨 시장의 회복력을 유지하고 있습니다.

데이터 표준이 발전함에 따라, EPCIS 2.0은 시리얼화와 센서 이벤트의 통합을 가능하게 하여, 규제 대상 워크플로우에서 센서 라벨 및 RFID 도입의 투자 대비 효과를 높여줍니다. 이러한 통합을 통해 상태 데이터를 고유 식별자와 기본적으로 연동하여 거래 파트너 간에 교환할 수 있게 됨으로써, 센싱의 유용성이 높아집니다. BLE를 활용한 병원용 RTLS(실시간 위치 정보 시스템)의 도입은 RFID 및 바코드를 보완하여, 고정된 병목 현상을 넘어 가시성을 확대합니다. 이러한 상황에서 헬스케어 스마트 라벨 업계의 기술 선택은 병상에서의 검증, 자동 계수, 또는 단위 수준의 콜드체인 보장 등 이용 사례의 우선순위에 따라 이루어집니다. 이러한 복합적인 동향은 저비용 2차원 바코드가 여전히 널리 보급되는 한편, 헬스케어 스마트 라벨 시장에서 영향력이 큰 용도 분야에서는 센싱 및 RFID의 점유율이 확대되는 균형 잡힌 구도를 뒷받침하고 있습니다.

2025년 기준으로 마이크로프로세서와 IC는 부품 구성의 42.96%를 차지했으며, 이는 밸류체인 내 가치 창출을 주도하는 RFID, NFC 및 첨단 센서 태그 설계에 널리 채택되고 있음을 반영합니다. 콜드체인의 확대, 특수 치료제 취급, 그리고 임상 텔레메트리 활용 사례가 제조, 유통, 의료 서비스 각 분야에서 확대됨에 따라, 센서 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 14.82%로 성장할 것으로 전망됩니다. 메모리와 트랜시버는 온도 변동이나 가혹한 RF 환경에서도 신뢰성 높은 판독 및 데이터 보존을 실현하기 위한 필수 요소로 자리 잡고 있습니다. 배터리는 지속적인 브로드캐스트나 상태 기록이 필요한 활성 BLE 및 특수 라벨에 사용되지만, 에너지 수확 기술의 발전으로 인해 시간이 지남에 따라 배터리 교체 필요성은 줄어들고 있습니다. 이러한 구성 요소들의 동향은 헬스케어 스마트 라벨 시장에서 상태 인식형 라벨링으로의 지속적인 전환을 촉진하고 있습니다.

EPCIS 2.0이 센서 이벤트를 지원함에 따라, 센서와 직렬화 데이터를 결합한 솔루션이 증가하고 있으며, 이를 통해 별도의 사용자 정의 데이터 모델 없이도 통합 가치를 높일 수 있게 되었습니다. IC의 감도, 조정된 안테나, 그리고 교정된 센서 소자에 기반하여 금속이나 액체 위에서도 신뢰할 수 있는 라벨을 구현하는 부품은 병원이나 의약품 유통 센터에 유용합니다. 소형 바이알이나 곡면용으로 부품 스택을 최적화한 공급업체들은 기존 태그로는 어려웠던 새로운 설치 장소를 개척하고 있습니다. 이러한 발전은 헬스케어 스마트 라벨 업계의 센서 및 고성능 IC 발전을 촉진하는 한편, 헬스케어 스마트 라벨 시장에 더욱 다양한 솔루션을 제공합니다.

지역별 분석

북미는 2025년에 43.14%를 차지했으며, 이는 DSCSA(의약품 안전 추적법)에 따른 일련번호 부여, 병원의 디지털화, 그리고 모든 의료 현장에서 RFID 및 BLE 인프라의 적극적인 도입에 힘입은 결과입니다. 아시아태평양은 지역 의료 시스템이 병원 자동화를 확대하고, 생물학적 제제 생산을 늘리며, 세계 거래 파트너들의 기대에 부응하여 시리얼화를 도입함에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 14.76%를 기록하며 성장할 것으로 전망됩니다. 유럽에서는 EMVS 검증 및 임상 물류 분야에서 선택적으로 도입된 RFID와 2차원 바코드 스캔을 병원 업무 흐름에 적용함으로써 꾸준한 수요가 유지되고 있습니다. 이러한 지역별 수요 패턴은 규격과 인프라 투자가 통합되는 과정에서 헬스케어 스마트 라벨 시장을 뒷받침하고 있습니다.

북미에서는 미국이 DSCSA의 상호운용성 요건과 RFID 지원 캐비닛 및 재고 관리 시스템에 대한 병원의 투자를 주도하고 있는 반면, 캐나다와 멕시코는 병원 및 유통 업무 분야의 디지털 대응 역량을 강화하고 있습니다. 유럽에서는 독일, 영국, 프랑스, 이탈리아, 스페인이 규정 준수 및 공급 보장을 위해 일관된 패키지 단위 검증과 창고 내 스캔을 추진하고 있습니다. 그 밖에도 유럽에서는 병원들이 스캔 및 검증 장비를 교체하고, 전문 치료의 양과 가치가 증가함에 따라 시장이 확대되고 있습니다.

아시아태평양 전체를 보면, 중국은 시리얼화와 의료 물류 기술의 규모를 확대하고 있으며, 인도는 제약 제조 및 CDMO(위탁 개발·제조) 역량을 강화하고 있습니다. 한편, 일본, 호주, 한국은 병원 운영 측면에서 높은 디지털 성숙도를 유지하고 있습니다. 그 밖의 아시아태평양에서는 RFID와 바코드를 결합한 업무 프로세스가 도입되어 있으며, 대부분의 경우 고가 제품이나 콜드체인 운송 분야에서 먼저 시작되고 있습니다. 중동 및 아프리카에서는 GCC(걸프협력회의) 회원국들이 규정 준수에 부합하는 라벨 표시를 요구하는 병원의 현대화 및 전문 의약품 수입을 주도하고 있는 반면, 남아프리카에서는 약국과 병원을 대상으로 한 추적성 시스템에 대한 투자가 확대되고 있습니다. 남미에서는 브라질과 아르헨티나가 전문 의약품의 유통 및 병원 내 바코드 검증을 확대하고 있으며, 반품 처리 및 콜드체인 관리의 발전에 따라 상태 감지형 라벨에 대한 관심이 높아지고 있습니다. 이러한 동향들이 맞물려, 지역을 불문하고 헬스케어 스마트 라벨 시장의 다양한 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the healthcare smart labels market size is projected to expand from USD 3.76 billion in 2025 and USD 4.28 billion in 2026 to USD 7.21 billion by 2031, registering a CAGR of 13.92% between 2026 to 2031.

This report is Segmented by Technology (RFID Labels, NFC (High Frequency) Tags, and More), Component (Batteries, Microprocessors / ICs, Transceivers, Sensors and Memory), Application (Drug Tracking & Serialization, Cold-Chain Monitoring, and More), End User (Hospitals, Pharmaceutical Companies, and More), and Geography (North America, Europe, and More). The Market and Forecasted in Terms of Value (USD).

Global Healthcare Smart Labels Market Trends and Insights

DSCSA/EU FMD Serialization Mandates Accelerate Item-Level Labeling

Serialization requirements in the United States and Europe continue to lift demand for item-level labeling, with DSCSA emphasizing interoperable, electronic tracing and the EU FMD relying on pack-level verification through EMVS. The DSCSA enhanced distribution security framework requires trading partners to exchange serialized data and investigate suspect products, which encourages pharmaceutical manufacturers and distributors to standardize barcodes and RFID-based identifiers on unit packages and cases. In the EU, the FMD architecture implements unique identifiers and anti-tamper devices on prescription medicines, making machine-readable 2D DataMatrix labels a default for verification at dispensing points, including hospital pharmacies. These requirements create a durable baseline for the healthcare smart labels market as companies refresh and expand labeling systems to remain compliant. The operational push for interoperable data also aligns with EPCIS-based exchange, which in turn favors serialized barcodes and RAIN RFID that integrate smoothly with enterprise systems.

Anti-Counterfeiting and Diversion Control Priorities in Pharma

Pharmaceutical stakeholders use smart labels to deter counterfeiting, detect diversion, and enable rapid recalls, with serialization and tamper-evidence working alongside mobile verification. Health authorities continue to warn that falsified medical products remain a threat, reinforcing the need for secure, scannable labels on each saleable unit as well as on secondary packaging. Item-level barcodes and NFC tags support authentication and chain-of-custody checks across wholesalers, third-party logistics providers, and hospital pharmacies. In parallel, RFID enables automated counting and location tracking in warehouses and care settings, which helps reduce shrinkage and detect anomalies in high-value therapies. These capabilities together strengthen the healthcare smart labels market by reducing error and risk exposure across the regulated supply chain.

High Implementation and Infrastructure Cost Across Labels/Readers/Software

Total cost of ownership includes labels and inlays, readers and printers, encoding and verification stations, and the software needed to capture and exchange EPCIS events. Hospitals and pharma distribution sites must budget for systems integration and process changes, including staff training and change management to ensure compliance. Passive RFID systems can lower costs over time, but upfront investment in readers and infrastructure remains a barrier, especially for smaller facilities. Active BLE tags that incorporate batteries or advanced sensors carry higher unit costs, which narrows the range of use cases where ROI is immediately clear. These economic factors can delay some deployments in the healthcare smart labels market, particularly where the value density of products is moderate.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biologics/Vaccines Cold-Chain Needs Temperature-Indicating Labels

- Healthcare Digitalization and RFID/NFC Adoption in Hospitals and Pharma

- Data Privacy, Security, and Interoperability Hurdles (HIPAA/GDPR/EPCIS)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, QR Code and 2D DataMatrix labels led with 41.23% of the healthcare smart labels market share in technology, reflecting their central role in DSCSA and EMVS verification at the unit level in hospitals and pharmacies. Over 2026-2031, sensing labels that capture temperature and related conditions are projected to grow fastest at a 14.65% CAGR as biologics and vaccines expand, and stakeholders seek simple unit-level condition visibility across cold-chain movements. RAIN RFID continues to scale for automated counting and cabinet management in care settings, while NFC complements with patient-initiated taps for authentication and information access. EAS overlaps where item security is required in retail and hospital pharmacy settings that handle specialty therapies. Multi-technology strategies remain common, so clinical and logistics teams can scan 2D barcodes while inventory teams automate with RFID, preserving resilience in the healthcare smart labels market.

As data standards evolve, EPCIS 2.0 enables combined serialization and sensor events that increase the return from sensor labels and RFID deployments in regulated workflows. This integration makes sensing more attractive since condition data can be natively associated with unique identifiers and exchanged across trading partners. Hospital RTLS deployments that leverage BLE are complementary to RFID and barcodes, broadening visibility beyond fixed choke points. In this context, technology choices align with use-case priorities such as bedside verification, automated counting, or unit-level cold-chain assurance in the healthcare smart labels industry. The combined trajectory supports a balanced mix in which low-cost 2D barcodes remain ubiquitous while sensing and RFID gain share in high-impact applications of the healthcare smart labels market.

Microprocessors and ICs accounted for 42.96% of the component stack in 2025, reflecting their presence across RFID, NFC, and advanced sensor tag designs that drive value capture in the supply chain. Sensors are projected to grow at a 14.82% CAGR during 2026-2031 as cold-chain expansion, specialty therapy handling, and clinical telemetry use cases scale across manufacturing, distribution, and care delivery. Memory and transceivers remain essential enablers of reliable reads and data retention across temperature excursions and challenging RF environments. Batteries appear in active BLE and specialty labels where continuous broadcasting or condition logging is required, although energy-harvesting trends reduce the need for battery replacements over time. These component trends favor a durable shift toward condition-aware labeling in the healthcare smart labels market.

As EPCIS 2.0 supports sensor events, more solutions pair sensors with serialization data, which increases integration value without requiring custom data models. Hospitals and pharma distribution centers benefit when components enable labels that are reliable on metals and liquids, which depend on IC sensitivity, tuned antennas, and calibrated sensor elements. Vendors that optimize component stacks for small vials and curved surfaces unlock new footprints where conventional tags struggled. These advances reinforce the trajectory for sensors and high-performance ICs in the healthcare smart labels industry while the healthcare smart labels market attracts more solution diversity.

Geography Analysis

North America accounted for 43.14% in 2025, supported by DSCSA-driven serialization, hospital digitalization, and strong adoption of RFID and BLE infrastructure across care settings. Asia-Pacific is projected to grow at a 14.76% CAGR during 2026-2031 as regional healthcare systems scale hospital automation, expand biologics manufacturing, and adopt serialization in line with global trading partner expectations. Europe maintains robust demand through EMVS verification and hospital workflows that operationalize 2D barcode scanning with selective RFID adoption in clinical logistics. These regional demand patterns sustain the healthcare smart labels market as standards and infrastructure investments converge.

In North America, the United States sets the pace with DSCSA interoperability requirements and hospital investments in RFID-enabled cabinets and inventory systems, while Canada and Mexico raise digital readiness in hospital and distribution operations. In Europe, Germany, the United Kingdom, France, Italy, and Spain drive consistent pack-level verification and warehouse scanning for compliance and supply assurance. The rest of Europe expands as hospitals refresh scanning and verification equipment, and as specialty therapies grow in volume and value.

Across Asia-Pacific, China scales serialization and healthcare logistics technology, India deepens pharma manufacturing and CDMO capabilities, and Japan, Australia, and South Korea maintain high digital maturity in hospital operations. The Rest of Asia-Pacific introduces blended RFID and barcode workflows, often starting with high-value products and cold-chain shipments. In the Middle East and Africa, GCC markets lead with hospital modernization and specialty imports that require compliant labeling, while South Africa progresses with pharmacy and hospital traceability investments. In South America, Brazil and Argentina expand specialty distribution and hospital barcode verification, while returns processing and cold-chain management lift interest in condition-aware labels. These trends collectively sustain diversified growth in the healthcare smart labels market across regions.

- Alien Technology LLC

- AVERY DENNISON

- Beontag

- Brady Corporation

- CCL Industries Inc.

- Checkpoint Systems

- HID Global (GuardRFID)

- Identiv Inc.

- Impinj Inc.

- Invengo Information Technology Co. Ltd.

- NXP Semiconductors

- SATO Holdings Corporation

- Schreiner MediPharm

- SpotSee

- Stora Enso Intelligent Packaging

- Tageos

- Timestrip UK Ltd.

- TSC Printronix Auto ID

- Wiliot

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 DSCSA/EU FMD Serialization Mandates Accelerate Item-Level Labeling

- 4.2.2 Anti-Counterfeiting and Diversion Control Priorities in Pharma

- 4.2.3 Expansion of Biologics/Vaccines Cold-Chain Needs Temperature-Indicating Labels

- 4.2.4 Healthcare Digitalization and RFID/NFC Adoption in Hospitals and Pharma

- 4.2.5 EPCIS 2.0 and Interoperable Data Exchange Enable Sensorized Smart Labels

- 4.2.6 Ambient IoT/BLE Sensing Brings Unit-Level Condition Visibility

- 4.3 Market Restraints

- 4.3.1 High Implementation and Infrastructure Cost Across Labels/Readers/Software

- 4.3.2 Data Privacy, Security, and Interoperability Hurdles (HIPAA/GDPR/EPCIS)

- 4.3.3 RFID Performance Challenges on Vials/Liquids/Metal-Rich Environments

- 4.3.4 Fragmented Standards and Compliance Workflows Across DSCSA/UDI/EMVS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 RFID Labels (RAIN UHF)

- 5.1.2 NFC (High Frequency) Tags

- 5.1.3 Sensing Labels

- 5.1.4 Electronic Article Surveillance (EAS)

- 5.1.5 QR Code / 2D Barcode Labels (DataMatrix, QR)

- 5.2 By Component

- 5.2.1 Batteries

- 5.2.2 Microprocessors / ICs

- 5.2.3 Transceivers

- 5.2.4 Sensors

- 5.2.5 Memory

- 5.3 By Application

- 5.3.1 Drug Tracking & Serialization

- 5.3.2 Cold-chain Monitoring

- 5.3.3 Medical Equipment Tracking

- 5.3.4 Patient Identification & Safety

- 5.3.5 Laboratory Sample Tracking

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Pharmaceutical Companies

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Pharmacies & Retail Pharmacies

- 5.4.5 Contract Manufacturers (CMOs/CDMOs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Alien Technology LLC

- 6.3.2 Avery Dennison Corporation

- 6.3.3 Beontag

- 6.3.4 Brady Corporation

- 6.3.5 CCL Industries Inc.

- 6.3.6 Checkpoint Systems

- 6.3.7 HID Global (GuardRFID)

- 6.3.8 Identiv Inc.

- 6.3.9 Impinj Inc.

- 6.3.10 Invengo Information Technology Co. Ltd.

- 6.3.11 NXP Semiconductors

- 6.3.12 SATO Holdings Corporation

- 6.3.13 Schreiner MediPharm

- 6.3.14 SpotSee

- 6.3.15 Stora Enso Intelligent Packaging

- 6.3.16 Tageos

- 6.3.17 Timestrip UK Ltd.

- 6.3.18 TSC Printronix Auto ID

- 6.3.19 Wiliot

- 6.3.20 Zebra Technologies Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment